The Institute of Chartered Accountants of India ( ICAI ) has clarified that there is NOT a bar in the revised Code of Ethics on acceptance of more than 15% fees from a single client.

The ICAI has said that some members have expressed their concern on one of the provisions contained in Paragraph R410.4 of the Volume-I of revised Code of Ethics on measures for addressing self-interest threats resulting from the dependence of Fees from a single client.

The ICAI clarified that there is NOT a bar in the revised Code of Ethics on acceptance of more than 15% fees from a single client. There is the only requirement of disclosure, and taking safeguards prescribed therein, if the total gross annual professional fees from the audit client and its related entities represent more than 15% of the total fees received by the firm expressing the opinion on the financial statements of the client for two consecutive years.

Accordingly, the Audit may be continued while taking safeguards as mentioned in the said Paragraph. The ICAI further clarified that this rule would not apply in case of audit of Government Companies, public undertakings, nationalized banks, public financial institutions, or where appointments are made by Government; OR where the total gross annual fees of the Firm does not exceed five lakhs of rupees.

It may also be relevant to note that the rule applies ONLY where such Fees are received from an AUDIT CLIENT.

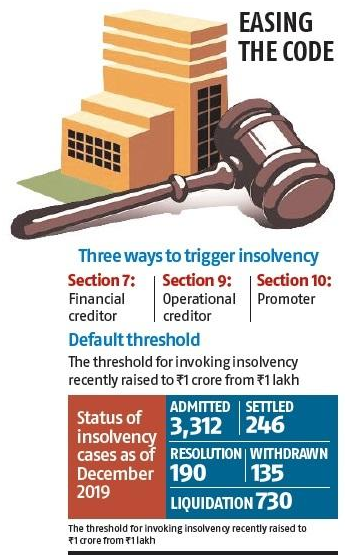

As per existing norms, if a payment default exceeds 90 days then the lender concerned has to refer the account for resolution under IBC or any other mechanism permitted by the Reserve Bank of India (RBI). The lender does not have the option to restructure the loan.

The government has decided to suspend insolvency and bankruptcy proceedings for at least six months owing to challenges businesses are facing due to the Covid-19 pandemic.

A new Section is likely to be added to the Insolvency and Bankruptcy Code (IBC).

It will suspend Sections 7, 9, and 10, which are used to trigger insolvency proceedings for six months or a period not exceeding one year from the date they commence, the official said.

A new Section is likely to be added to the Insolvency and Bankruptcy Code (IBC).

It will suspend Sections 7, 9, and 10, which are used to trigger insolvency proceedings for six months or a period not exceeding one year from the date they commence, the official said.

Section 7 of the Code enables

financial creditors to start insolvency proceedings against a company while

Section 9 gives operational creditors these powers.

Under Section 10, the promoter of the company can trigger insolvency proceedings against his or her own concern.

All the three Sections will cease to be effective for six months or further.

The provision is likely to require a change in the Act, according to experts.

“This is a positive step for companies.

But for companies, which were otherwise already in stress and could have found resolution under the IBC, their resolution may also be delayed due to this suspension,” said Anshul Jain, partner, PwC India.

Jain also said it needed to be seen if this move would have a positive impact on privately negotiated transactions on mergers and acquisitions.

In March, Union Finance Minister Nirmala Sitharaman had indicated the government would consider suspending the IBC for a few months if the Covid situation persisted and caused stress to businesses.

Already, the default threshold for stressed companies facing insolvency has been increased from Rs 1 lakh to Rs 1 crore.

In March, Union Finance Minister Nirmala Sitharaman had indicated the government would consider suspending the IBC for a few months if the Covid situation persisted and caused stress to businesses. Already, the default threshold for stressed companies facing insolvency has been increased from Rs 1 lakh to Rs 1 crore.

RBI is also likely to question the auditor on whether the SBI proposal would have any ‘material impact’ on the existing accounts of Yes Bank

The Reserve Bank of India will check if troubled lender Yes Bank’s auditor had raised any alarm in the past year. The apex bank has been in touch with the auditor and will look into whether they had specifically issued any warning in the past 12 months.

According to a report in The Economic Times, RBI has been in touch with auditor BSR & Co and wants to know if it had raised any red flag relating to the health of Yes Bank or any other issue. The auditor is part of KPMG India. The central bank is also likely to question the auditor on whether the SBI proposal would have any ‘material impact’ on the existing accounts of Yes Bank.

On Friday, the RBI announced a reconstruction scheme for the bank. It said that SBI that has expressed interest to invest in the troubled bank would do so to the extent of holding 49 per cent shareholding. The apex bank said that SBI’s investment in Yes Bank would not impact the employees and their current terms of employment.

BSR and Co was appointed as Yes Bank’s auditor after RBI banned SR Batliboi & Co for a year. The RBI had stated that the firm that was part of EY was banned due to “lapses identified in a statutory audit assignment carried out by the firm”.

RBI put restrictions on Yes Bank on March 6, allowing its customers to withdraw only Rs 50,000 for a month. The apex bank relaxed the guidelines subsequently. On Tuesday, the bank permitted its credit card customers to pay their credit card dues and loan obligations from other bank accounts. It allowed NEFT payments to clear loan EMIs and make credit card payments. The bank had, before that, allowed customers to withdraw money from ATMs of other banks.

The government had issued new norms for auditors, seeking more disclosures in reports, a move which comes after a series of corporate scams and frauds surfaced over the past few years.

CARO 2020 – Companies (Auditor’s Report) Order, 2020

MCA in place of existing the Companies (Auditor’s Report) Order, 2016, has notified CARO 2020 after consultation with the National Financial Reporting Authority constituted under section 132 of the Companies Act, 2013.

Auditor’s report to contain matters specified in paragraphs 3 and 4. – Every report made by the auditor under section 143 of the Companies Act on the accounts of every company audited by him, to which this Order applies, for the financial years commencing on or after the 1st April, 2019, shall in addition, contain the matters specified in paragraphs 3 and 4, of the CARO 2020.

Provided this Order shall not apply to the auditor’s report on consolidated financial statements except clause (xxi) of paragraph 3.

It shall come into force on the date of its publication in the Official Gazette.

CARO 2020 – Key changes/highlights

Matters to be included in auditor’s report, in CARO 2020 – the reporting clauses are more extensive and detailed than were in CARO2016

Unlike CARO 2016, which required reporting on all fixed assets, new reporting requirements pays attention to Property, Plant, Equipment and intangible assets.

Reporting on revaluation of Property, Plant and Equipments by company

Reporting of proceedings under the Benami Transactions (Prohibition) Act, 1988.

Reporting of compliances if company was sanctioned working capital limits in excess of Rs.5 crores or more from banks or financial institutions.

– whether the quarterly returns or statements filed by the company with such banks or financial institutions are in agreement with the books of account of the Company, if not, to give details;

Reporting of investments in or in providing of any guarantee or security or granting any loans or advances to companies, firms, Limited Liability Partnerships or any other parties.

Reporting of compliances with RBI directives and the provisions the Companies Act with respect to deemed deposits.

Reporting with respect to transactions not recorded in the books of account surrendered or disclosed as income in the income tax proceedings.

Comprehensive reporting requirement for default in the repayment of loans / other borrowings or in the payment of interest

– whether the company is a declared wilful defaulter by any bank or financial institution or other lender;

– whether term loans were applied for the purpose for which the loans were obtained; if not, the amount of loan so diverted and the purpose for which it is used may be reported;

– whether funds raised on short term basis have been utilised for long term purposes, if yes, the nature and amount to be indicated

Reporting on treatment by auditor of whistle-blower complaints received during the year by the company

Reporting on internal audit system

– whether the company has an internal audit system commensurate with the size and nature of its business;

– whether the reports of the Internal Auditors for the period under audit were considered by the statutory auditor;

Reporting on cash losses

Reporting on resignation of the statutory auditors

Reporting on uncertainty of company capable of meeting its liabilities

Reporting transfer of unspent CSR amount to Fund specified in Schedule VII

Reporting on qualifications or adverse remarks by the auditors in the CARO reports of companies included in the consolidated financial statements

It is expected that CARO, 2020 will improve the overall quality of reporting by the auditors and thereby lead to “greater transparency and faith in the financial affairs of the companies.”

The Institute of Chartered Accountants of India (ICAI) today clarified that, Chartered Accountants joining Unrecognized ‘Networks’ for Professional Work amounts may result in Disciplinary Proceedings.

The ICAI has said that, It has come to the knowledge of the Institute that many members in practice are joining/associating themselves with “Networks” which are other than the Networks registered with the Institute, with the mutual referral of professional work being the main objective of such Networks, among others.

The ICAI has clarified that associations with ‘Network’ as a medium of referral of professional work is permissible only if the Network is registered with the Institute, comprising only of Chartered Accountants/ Chartered Accountant Firms, and governed by the Institute’s Network Guidelines,‟ attention is also drawn towards following provisions of Chartered Accountants Act, 1949:

Clause (2) of Part I of First Schedule to the Act

A Chartered Accountant in practice shall be deemed to be guilty of professional misconduct, if he pays or allows or agrees to pay or allow, directly or indirectly, any share, commission or brokerage in the Fees or profits of his professional business, to any person other than a member of the Institute or a partner or a retired partner or the legal representative of a deceased partner, or a member of any other professional body or with such other persons having such qualifications as may be prescribed, for the purpose of rendering such professional services from time to time in or outside India.

Explanation — In this item, “partner” includes a person residing outside India with whom a chartered accountant in practice has entered into a partnership which is not in contravention of the item (4) of this Part;

Clause (3) of Part I of First Schedule to the Act

A Chartered Accountant in practice shall be deemed to be guilty of professional misconduct, if he accepts or agrees to accept any part of the profits of the professional work of a person who is not a member of the Institute: Provided that nothing herein contained shall be construed as prohibiting a member from entering into profit sharing or other similar arrangements, including receiving any share commission or brokerage in the fees, with a member of such professional body or other person having qualifications, as is referred to in item (2) of this Part;

Clause (5) of Part I of First Schedule to the Act

A Chartered Accountant in practice shall be deemed to be guilty of professional misconduct, if he secures, either through the services of a person who is not an employee of such Chartered Accountant or who is not his partner or by means which are not open to a chartered accountant, any professional business. Provided that nothing herein contained shall be construed as prohibiting any arrangement permitted in terms of items (2), (3) and (4) of this Part;

Clause (6) of Part I of First Schedule to the Act

A Chartered Accountant in practice shall be deemed to be guilty of professional misconduct if he solicits clients or professional work either directly or indirectly by circular, advertisement, personal communication or interview or by any other means: Provided that nothing herein contained shall be construed as preventing or prohibiting – (i) any chartered accountant from applying or requesting for or inviting or securing professional work from another chartered accountant in practice; or

(ii) a member from responding to tenders or enquiries issued by various users of professional services or organisations from time to time and securing professional work as a consequence;

In view of the above provisions, it is not permissible for members in practice to join Networks (by whatever name called) other than the Networks registered with the Institute.

Members may note that joining such Networks as mentioned above may result in noncompliance of the above-stated provisions of the Act resulting in disciplinary proceedings in accordance with the provisions of the Act.

Capital markets regulator Sebi on Wednesday said its actions against auditors for faulty audits are within its “Parliamentary mandate”, and there is no question of “turf wars” on this issue.

SEBI Chairman Ajay Tyagi said the watchdog is working only to protect the interests of investors and limiting its actions to auditors of publicly listed firms.

In 2018, the regulator banned Price Waterhouse for two years from auditing any listed firm for its role in the Satyam Computer Services scam. However, the audit firm had successfully challenged the same in the Securities Appellate Tribunal and got the order quashed.

“It is our parliamentary mandate I would say to see that it is done and there is no trouble there. It goes to the basic issue of investor protection being the parliamentary mandate of Sebi,” he noted.

In November, the Supreme Court stayed a SAT order which had held that Sebi does not have the power to bar auditors.

“Our position is very simple — if they’re auditing listed companies based on which investors are investing, and if we find that that work has not been done properly and in investors’ interest, some audit firms should not be allowed to audit for sometime of the listed companies,” Tyagi said at an event here.

According to Tyagi, audit firms are important gatekeepers who help companies put out results and financial performance to the stock exchanges, based on which investors take the call whether to invest or not.

“It is not our case that Sebi is the agency which registers or regulates the auditors. It is nothing like that… We are not de-registering auditors. We don’t have the authority and we don’t wish to have that authority,” he said.

He also made it clear that Sebi’s expectation is that faulty audits should not lead to inflated profits or dividends.

Regarding IPO market, Tyagi said there has been an improvement in activities lately and that nearly a dozen issues of over Rs 15,000 crore are in the pipeline.

The regulator has given its wish-list for the budget to the finance ministry, includes ways to increase the activities in the corporate bond market, he said.

On November 18, 2019 the Companies (Meetings of Board and its Powers) Second Amendment Rules, 2019 (“Amendment Rules“) amended certain threshold limits prescribed by the Rules.

The central government notified the Companies (Meetings of Board and its Powers) Second Amendment Rules, 2019 on 18 November 2019. The amendment rules amend sub-clause 3 of rule 15 of the Companies (Meetings of Board and its Powers) Rules, 2014. The amendment rules alter the various transaction thresholds within which the board may authorize a related party transaction without referring the matter to the shareholders pursuant to section 188(1) (Related party transactions) of the Companies Act, 2013.

Rule 15 provides for conditions applicable to the board taking up, discussing and approving a related party contract or arrangement. The first proviso to section 188(1) of the act provides that no contract or arrangement which exceeds certain monetary thresholds, in relation to the company’s paid-up share capital or otherwise, may be entered into without the prior approval of the shareholders by a resolution. The thresholds in relation to this proviso to section 188(1) of the act are prescribed by the rules and have been amended through the amendment rules as follows:

For a contract or arrangement in relation to a sale, purchase or supply of any goods, previously the threshold, was the lower of: (1) 10% or more of the turnover of the company; or (2)₹1 billion. The amendment rules have relaxed the threshold and fixed it at 10% or more of turnover of the company.

Similarly, for a contract or arrangement for selling or otherwise disposing of, or buying property of any kind, previously the threshold for requiring a shareholder resolution was the lower of: (1) 10% or more of the turnover of the company; or (2)₹1 billion. The amendment rules have relaxed the threshold and fixed it at 10% or more of turnover of the company.

The amendment rules has similarly amended the threshold for a contract or arrangement in relation to leasing of property any kind, and in relation to availing or rendering of any services (directly, or through the appointment of an agent). The amendment rules now fix the threshold at 10% or more of turnover of the company.

Accordingly, the ministry has relaxed the thresholds and made it simpler for companies to ensure ease of business, and the ease of entering into related party transactions.

Nature of Related Party Transactions

Earlier Threshold Limit*

Amended Threshold Limit*

Sale, purchase or supply

of any goods or material (directly or through an agent).

Amounting to ten percent (10%) or more of turnover or Rs. 100 Crore, whichever is lower.

Amounting to ten percent (10%) or more of the turnover of the company.

Selling or otherwise

disposing of, or buying, property of any kind (directly or through an agent).

Amounting to ten percent (10%) or more of net worth or Rs. 100 Crore, whichever is lower.

Amounting to ten percent (10%) or more of the turnover of the company.

Leasing of property of

any kind.

Amounting to ten percent (10%) or more of net worth or 10 percent (10%) or more of turnover Rs. 100 Crore, whichever is lower.

Amounting to ten percent (10%) or more of the turnover of the company.

Availing or rendering of any services (directly or through an agent)

Amounting to ten percent(10%)or more of turnover or Rs. 50 Crore, whichever is lower

Amounting to ten percent (10%) or more of the turnover of the company

*limits specified above shall apply for transaction or transactions to be entered into either individually or taken together with the previous transactions during a financial year.

Appointment to any

office or place of profit in the company, subsidiary company or associate company

Remuneration exceeding

Rs. 2,50,000 per month

No Change

Underwriting the

subscription of any securities or derivatives of the company

Remuneration exceeding

one percent (1%) of net worth

The Institute of Chartered Accountants of India ( ICAI ) has clarified that there is NOT a bar in the revised Code of Ethics on acceptance of more than 15% fees from a single client.

The Institute of Chartered Accountants of India ( ICAI ) has clarified that there is NOT a bar in the revised Code of Ethics on acceptance of more than 15% fees from a single client.