The Ministry of Corporate Affairs (MCA) has again extended the due date of filing Annual Return and Financial Statement.

The MCA has again relaxed the levy of additional fees for filing of e-forms AOC-4, AOC-4 (CFS), AOC-4, AOC-4 XBRL AOC-4 Non-XBRL till 15.03.2022 and for filing of e-forms MGT-7/MGT-7A for the financial year ended on 31.03.2021 till 31.03.2022.

MGT-7 is an electronic form provided by the Ministry of Corporate affairs to all the corporates in order to fill their annual return details. This e-form is maintained by the Registrar of Companies via electronic mode and on the basis of the statement of correctness given by the company.

Form AOC 4 is used to file the financial statements for each financial year with the Registrar of Companies (ROC). In the case of consolidated financial statements, the company shall file the AOC 4.

Keeping in view the extension of timelines for audit/ tax audit and finalization of accounts under the Income Tax Act, 1961, this extension was very much required to synchronize with the inter-connected chain of events.

Accordingly, the ROC annual return due date for FY 2020-21 stands extended for companies, without payment of additional fee, as under:

MCA grants extension of time for filing Annual Financial Statements (AOC-4) and Annual Returns (MGT-7) without additional fees.

The Ministry of Corporate Affairs has recently granted the much-needed relief by extending the dates for filing of the 5 important e-forms with the removal of additional fees on the e-forms, namely Forms Annual Financial Statements -AOC-4, AOC-4 (CFS), AOC-4, AOC-4 XBRL AOC-4 Non-XBRL, and Annual Returns -MGT -7 / MGT -7A, filing to the Financial Year ended 31st March 2021 under the Companies Act 2013.

The extended due dates for filing of e-forms such as AOC-4, AOC-4 (CFS), AOC-4 XBRL, AOC-4 Non-XBRL are 15th February 2022 and for filing of e-forms such as MGT-7, and MGT-7A are 28th February 2022, for all stakeholders, without any additional fees.

The extension of due dates has been done as per the demand of the stakeholders for the filing of financial statements for the financial year ended 31.03.2021.

The AIS captures information on almost all financial transactions done in the previous financial year. The idea is to give taxpayers a comprehensive statement on their transactions that they can refer to while filing their income tax returns

The income tax department (I-T dept) on Monday rolled out the new annual information statement (AIS) on the compliance portal. This annual statement provides a comprehensive view of information to a taxpayer and the facility to submit online feedback.

The new annual information statement (AIS) includes additional information linked to interest, dividend, securities transactions, mutual fund transactions, foreign remittance information and other such transactions.

The income tax department has clarified that till the new annual information statement is validated and is completely operational, Form 26AS will continue to be available on the TRACES portal. The tax department also added that the reported information has been processed to remove duplicate information.

If the taxpayer feels that the information is incorrect, relates to another person/year, duplicate or such other a facility has been provided to submit online feedback. “The taxpayers are requested to view the information shown in annual information statement (AIS) and provide feedback if the information needs modification,” the Central Board of Direct Taxes (CBDT) said.

The new AIS can be accessed by clicking on the link ‘Annual Information Statement (AIS)’ under the ‘Services’ tab on the new Income tax e-filing portal (https://www.incometax.gov.in).

How AIS will be helpful?

AIS provides for a simplified taxpayer information summary (TIS) which shows the aggregated value for the taxpayer for the ease of filing returns.

If the taxpayer submits feedback on the annual information statement (AIS), the derived information in TIS will be automatically updated in real-time.

This derived information in taxpayer information summary (TIS) will be used for pre-filling of return which shall be implemented in a phased manner.

If the ITR has been filed but some information has not been included, the return may be revised to reflect the correct information as shown in TIS.

In case there is a variation, the taxpayer may rely on the information displayed on the TRACES portal for the purpose of filing of ITR.

In comparison to Form 26AS, AIS is a more comprehensive single reference document and can be modified by taxpayers if the information is incorrect.

Annual Information Statement (AIS) provides complete and detailed information related to interest, dividend, securities/ mutual funds transactions.

GST collection in October crosses ₹1.3 lakh crore, second highest ever

The gross GST revenue collected in the month of October 2021 exceeded ₹1.3 lakh crore. The GST revenues for October is the second highest ever since introduction of GST, second only to that in April 2021, which related to year-end revenues. The revenues for the month of October 2021 are 24% higher than the GST revenues in the same month last year.

The gross GST revenue collected in the month of October 2021 exceeded ₹1.3 lakh crore. The GST revenues for October is the second highest ever since introduction of GST, second only to that in April 2021, which related to year-end revenues. The revenues for the month of October 2021 are 24% higher than the GST revenues in the same month last year.

“This is very much in line with the trend in economic recovery. This is also evident from the trend in the e-way bills generated every month since the second wave. The revenues would have still been higher if the sales of cars and other products had not been affected on account of disruption in supply of semi-conductors,” the government said in a statement.

The government settled ₹27,310 crore to CGST and ₹22,394 crore to SGST from IGST as regular settlement. The total revenue of Centre and the States after regular settlements in the month of October 2021 is ₹51,171 crore for CGST and ₹52,815 crore for the SGST.

During the month, revenues from import of goods was 39% higher and the revenues from domestic transaction (including import of services) are 19% higher than the revenues from these sources during the same month last year.

Indian stock market benchmark Sensex was up over 600 points in noon trade. A private survey released earlier in the day showed India’s manufacturing sector activities gained further strength in October as companies scaled up production and stepped up input purchasing in anticipation of further improvements in demand.

The seasonally adjusted IHS Markit India Manufacturing Purchasing Managers’ Index (PMI) rose from 53.7 in September to 55.9 in October, pointing to the strongest improvement in overall operating conditions since February.

Robust gains in new work aided production growth in October as output and new orders expanded at fastest rates in seven months, while business optimism hit a six-month high, the survey said.

Extension of last date to file e-forms AOC-4, AOC-4 CFS, AOC-4 XBRL, AOC-4 Non-XBRL and MGT-7/7A for the FY 2020-21 to 31.12.2021

On October 29, 2021, the Ministry of Corporate Affairs (MCA) has announced the relaxation in levy of additional fees in filing of e-forms AOC-4, AOC-4 (CFS), AOC-4, AOC-4 XBRL AOC-4 Non-XBRL and MGT-7 / MGT-7A for the financial year ended on March 31, 2021 under the Companies Act, 2013.

It has been decided no additional fees shall be levied upto 31st December 2021 for the filing of e-forms in respect of the financial year ended on 31.03.2021.

During the said period, only normal fees shall be payable for the filing of the aforementioned e-forms.

Keeping in view of various requests received from stakeholders regarding relaxation on levy of additional fees for annual financial statement filings required to be done for the financial year ended on 31.03.2021, it has been decided that no additional fees shall be levied upto 31.12.2021 for the filing of e-forms AOC-4, AOC-4 (CFS), AOC-4 XBRL, AOC-4 Non-XBRL and MGT-7/MGT-7A in respect of the financial year ended on 31.03.2021. During the said period, only normal fees shall be payable for the filing of the aforementioned e-forms.

Further to the extension of time for holding of Annual General Meeting (AGM) for the financial year ended on 31/03/2021, granted by MCA on 23 rd September, 2021 by two months, this relaxation is now announced by MCA to facilitate the filing of Annual Financial Statements by the stake holders.

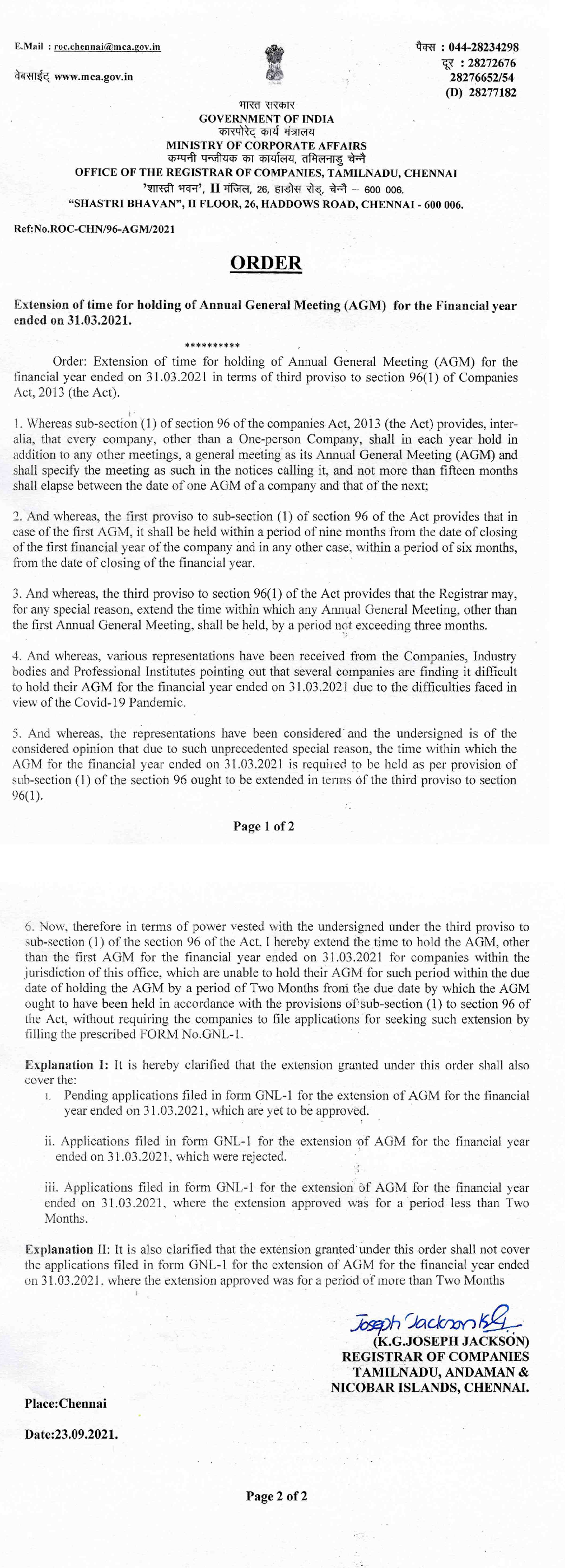

MCA has extended the Due Date for Holding of AGMs by the companies, by 2 months from the original due date in respect of the financial year 2020-21 ended on 31/03/2021. Accordingly, respective ROCs have issued extension Orders, which are available at the link below:

MCA Office Memorandum dt. 23/09/2021: Extension of time for holding of Annual General Meeting (AGM) for the Financial year ended on 31/03/2021

1. The Central Government has received representations seeking extension of time for holding Annual General Meeting (AGM) for the financial year 2020-21 ending on 31/03/2021 citing many difficulties faced due to second wave of Covid-19 and consequent lockdowns etc.

2. Accordingly, it has been decided to advise the Registrar of Companies (RoCs) to accord approval for extension of time for a period of two Months beyond the due date by which companies are required to conduct their AGMs for the financial year 2020-21 ended on 31/03/2021.

3. Kindly find enclosed a copy of the standard template for the order to be issued by RoCs under third proviso to sub-section (1) of section 96 of the Companies Act, 2013 ( the Act) for granting extension of time for conducting of AGM for the Financial Year 2020-21 ended on 31/03/2021.

4. Please take this action with utmost urgency and issue order before the close of the office today and forward the copy of the order to this office before for consolidation and uploading it on the MCA21 website. Also display this order on the Notice Board of your respective offices.

5. This issues with approval of the Competent Authority.

The extension of time by two months issued by ROC, Chennai is as below. The respective ROCs in the country have issued orders under third proviso to sub-section (1) of section 96 of the Companies Act, 2013 granting extension of time by 2 months for conducting of AGM for the Financial Year 2020-21 ended on 31/03/2021.

The extension of time by two months issued by ROC, Chennai is as below. The respective ROCs in the country have issued orders under third proviso to sub-section (1) of section 96 of the Companies Act, 2013 granting extension of time by 2 months for conducting of AGM for the Financial Year 2020-21 ended on 31/03/2021.

• This is the second time this financial year the government has extended the deadline of filing ITR for individuals whose accounts are not required to be audited. • The ITR filing deadline has been extended due to the many technical issues related to the government’s newly launched tax filing portal. • The deadline of filing belated/revised ITR has been extended by two months to March 31, 2022.

The government on Thursday extended the deadline to file income tax return (ITR) for FY 2020-21 by 3 months to December 31, 2021 from September 30, 2021. The extension of the deadline is for those individuals whose accounts are not required to be audited and who usually file their income tax return using ITR-1 or ITR-4 forms, as applicable.

In a statement, the Finance Ministry said that the decision has been on consideration of difficulties reported by the taxpayers and other stakeholders in filing of Income Tax Returns and various reports of audit for the Assessment Year 2021-22 under the Income Tax Act, 1961.

The income tax return (ITR) filing deadline for FY 2020-21 for individuals has already been extended, from the normal deadline of July 31, 2021. However, the new income tax e-filing portal has been marred by glitches and other problems from inception. Finance minister Nirmala Sitharaman has given Infosys, the company which set up the new income tax portal, time till September 15, 2021 to fix all the problems.

Last year too, the government has extended the due date of filing ITR for individuals four times – first from July 31 to November 30, 2020, then to December 31, 2020, and finally to January 10, 2021.

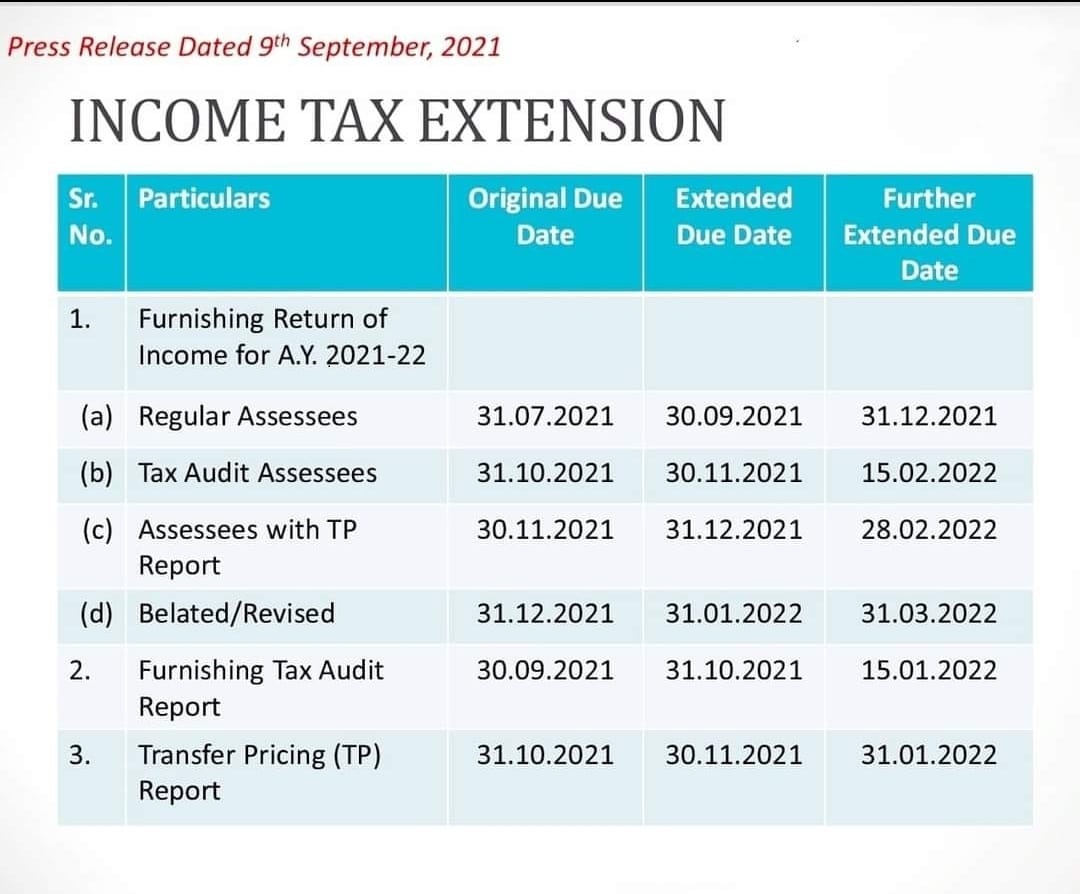

“On consideration of difficulties reported by the taxpayers in filing of Income Tax Returns(ITRs) & Audit reports for AY 2021-22 under the ITAct, 1961, CBDT further extends the due dates for filing of ITRs & Audit reports for AY 21-22. Circular No.17/2021 dated 09.09.2021 issued,” I-T Department tweeted on Thursday.

The due date of furnishing of report of audit under any provision of the Act for the previous year 2020-21, has been extended to January 15, 2022.

The due date of furnishing report from an accountant by persons entering into international transaction or specified domestic transaction under section 92E of the Act for the previous year 2020-21, is now January 31, 2022.

Again, the IT Department has decided to extend the due date of furnishing of Return of Income for the AY 2021-22, to February 15, 2022, among several other extensions.

The due date of furnishing of Return of Income for the Assessment Year 2021-22, which was December 31, 2021 has also been extended to February 28, 2022.

The due date of furnishing of belated or revised return of Income for the AY 2021-22 has been further extended to March 31, 2022.

Missing the ITR filing deadline would have had penal consequences. A late filing fee of Rs 5,000 would be levied if the ITR is filed by an individual after the expiry of the deadline.

Do keep in mind that government has also extended the deadline of filing belated ITR by one month from new deadline of December 31, 2021, to January 31, 2022. If the ITR is not filed by January 31, 2022, then the individual will not be able to file ITR for FY 2020-21, unless a notice is issued by the income tax department.

A late filing fee of Rs 5,000 along with penal interest at the rate of 1 per cent per month will be levied on the non-payment of tax dues in this case.

The MCA has again relaxed the levy of additional fees for filing of e-forms AOC-4, AOC-4 (CFS), AOC-4, AOC-4 XBRL AOC-4 Non-XBRL till 15.03.2022 and for filing of e-forms MGT-7/MGT-7A for the financial year ended on 31.03.2021 till 31.03.2022.

The MCA has again relaxed the levy of additional fees for filing of e-forms AOC-4, AOC-4 (CFS), AOC-4, AOC-4 XBRL AOC-4 Non-XBRL till 15.03.2022 and for filing of e-forms MGT-7/MGT-7A for the financial year ended on 31.03.2021 till 31.03.2022.