The government, in creating disciplinary mechanisms, could consider bringing in disclosure norms for auditors with respect to non-audit services and fees charged by them

The Ministry of Corporate Affairs is planning to amend the Chartered Accountants Act to build disciplinary mechanisms for removing possible conflicts of interest between audit firms and companies they audit.

The government is also looking at ways to address the gaps in the law with respect to network entities of which audit firms are part.

“We need to strengthen the Chartered Accountants Act. Many entities need to be brought within the regulatory remit to create accountability and transparency,” a senior government official told Business Standard.

The government, in creating disciplinary mechanisms, could consider bringing in disclosure norms for auditor with respect to non-audit services and fees charged by them

A government-appointed panel on regulating auditors and the networks had suggested that the fee from non-audit services should not be more than 50% of the audit fee.

India is considering tougher rules for audit firms, including a cap on the number of listed companies they can examine, according to a person with knowledge of the matter, as the government seeks to tighten oversight after a recent spate of governance lapses.

In India, 70% of the about 1,800 companies that trade on the National Stock Exchange are audited by firms affiliated to EY, Deloitte & Touche, KPMG and PWC, according to Delhi-based Prime Database. Current rules stipulate that individual auditors can examine accounts of up to 20 companies, though there is no limit on number of audits for the company.

The Big Four in India operate through a network of local chartered accountants firms. One way for them is to partner as a member of a local firm. They can also allow their brand name to be used by sub-licensee of a member local firm. The ministry hasn’t decided if the cap on audits will be at the group level or on each member firm, the person said.

The government is planning to expand the list of services which can’t be offered by statutory auditors under the Companies Act. Currently, statutory auditors can’t offer nine services, directly or indirectly, including internal audit, investment banking, and actuarial services. There is no restriction on providing services such as taxation or restructuring and valuation.

One option is to tweak the present cap on fees that can be generated through offering non-audit services, the person said. This cap, fixed in 2002, says fees from non-audit work can’t be more than the aggregate statutory audit fees. A spokeswoman for the corporate affairs ministry declined to comment.

A government-appointed panel on regulating auditors and the networks had suggested that the fee from non-audit services should not be more than 50% of the audit fee.

Deloitte Ban

Governance lapses and negligence has loaded the nation’s banks with one of the world’s worst piles of bad debt. In some cases, allegations of fund diversion have surfaced, while the founders of some shadow banks have faced accusations of accepting kickbacks in exchange for loans.

The corporate affairs ministry earlier this month sought a ban on Deloitte Haskins & Sells and BSR & Co. for their role as auditors to IL&FS Financial Services, a part of the IL&FS Group that was seized by the government last year after a string of debt defaults.

Deloitte in an emailed statement said it’s fully compliant with Indian audit standards, while BSR said it would defend its position in accordance with the law.

Meanwhile, the banking regulator forbid EY affiliate S. R. Batliboi & Co. from taking on bank audits for a year and, in 2018, the markets watchdog banned the local unit of PricewaterhouseCoopers LLP for two years in relations to work from a decade earlier.

Clarification on Auditor’s Certificate on Return of Deposits pursuant to Rule 16 of the Companies (Acceptance of Deposits) Rules, 2014

This has reference to Rule 16 of the Companies (Acceptance of Deposits) Rules, 2014 and further amendments.

In this regard, the Ministry of Corporate Affairs vide its letter no. File No: P-01/08/2013- CL-V Vol. VI dated June 24, 2019 has clarified on the matter as under:

The Auditor’s Certificate is mandatory only in case of return of deposits.

For filing particulars of transactions not considered as deposits information contained therein as on 31st March of that year need not be from the duly audited Financial Statement.

Only in case of Return of Deposit information contained therein as on 31st March of that year should be from duly audited financial statement of the company.

Also in order to provide guidance to members, the Auditing and Assurance Standards Board of ICAI has issued Illustrative Auditor’s Certificate on Return of Deposits, which is available on the below cited link:

With a spate of corporate irregularities coming to the fore, the Centre has decided to make disclosure norms more stringent. Corporate India is now required to submit details of transactions involving the receipt of money or loans taken by them, which are otherwise not considered deposits.

Every company other than Government company to which these rules apply, shall on or before the 29th day of June, of every year, file with the Registrar, a return in Form DPT–3 along with the fee as provided in Companies (Registration Offices and Fees) Rules, 2014 and furnish the information contained therein as on the 31st day of March of that year duly audited by the auditor of the company.

Form DPT–3 shall be used for filing return of deposit or particulars of transaction not considered as a deposit or both by every company other than Government company.

Due Date of the Form DPT-3 – Return of Deposits: Every company shall on or before the 30th day of June, of every year, file a return of deposit with the Registrar and furnish the information contained therein as on the 31st day of March of that year duly audited by the auditor of the company.

Due Date of the Form DPT-3 (ONE TIME): Form DPT-3 one time Due Date – all companies would be required to file Form DPT-3 one-time on or before the 29th June 2019

DPT-3 Due Date (EVERY YEAR): Form DPT-3 every year on or before 30th June of the preceding year.

Auditor of Company prepare the financial statements which include the following (Audited Copy)

Balance sheet,

Profit and loss account

Income and expenditure account

Cash flow statement

Statement of changes in equity

Due Date: 29th May 2019

Penalty On the defaulting company A fine of minimum Rs. 1 crore or twice the amount of deposit so accepted, whichever is lower, which may extend to Rs.10 crores; and

Every Officer who is in default: Imprisonment up to seven years and with a fine of not less than Rs. 25 lakh which may extend to Rs. 2 crores.

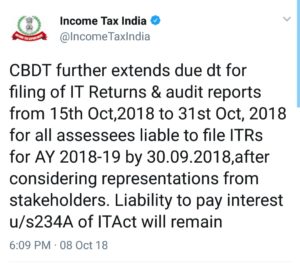

The Central Board of Direct Taxes (CBDT) has further extended due date for filing Income Tax Returns and Audit Reports to October 31st.

The due date for filing of Income Tax Returns and Audit Reports for Assessment Year 2018-19 is 30th September, 2018 for certain categories of taxpayers.

The CBDT had earlier extended the date for filing of Income Tax Returns and various reports of Audit to 15th October 2018.

Upon consideration of representations from various stakeholders, CBDT further extends the ‘due date’ for filing of Income Tax Returns as well as reports of Audit (which were required to be filed by the said specified date) from 15th October, 2018 to 31st October, 2018 in respect of the said categories of taxpayers.

However, as specified in earlier order dated 24.09.2018, assessees filing their return of income within the extended due date shall be liable for levy of interest as per provisions of section 234A of the Income-tax Act, 1961.

SEBI has proposed giving the board of directors of the company the authority to take appropriate action after conducting an investigation against the individual or firm that violates any regulations or submits a false certificate or report.

India’s capital market regulator has proposed amendments to tighten laws governing auditors and other third-party individuals hired by listed companies for auditing financial results, among other things.

The Kotak Committee, formed to come up with proposals for improving corporate governance, last year recommended that the Securities and Exchange Board of India (SEBI) should have clear powers to act against auditors and other third-party individuals or firms with statutory duties under the securities law.

Auditing lapses have caused several frauds to go unnoticed for years and the capital market regulator has had no direct control on the auditing firms.

SEBI has proposed giving the board of directors of the company the authority to take appropriate action after conducting an investigation against the individual or firm that violates any regulations or submits a false certificate or report.

The proposed changes come months after Punjab National Bank, India’s second largest state-run lender, stunned markets after uncovering a $2 billion loan fraud that had gone undetected for years.

Merchant bankers, credit rating agencies, custodians, among others, are registered and regulated by SEBI but chartered accountants, company secretaries, valuers and monitoring agencies do not come under any direct regulators.

The amendments would mean auditors must ensure certificates or reports issued by them are true in all material respects and they must exercise all due care, skill and diligence with respect to all processes involved in issuance of the report or certificate.

The auditors would be responsible to report in writing to the audit committee of the listed company or the compliance officer on any violation of the securities law they noticed.

In January, SEBI barred Price Waterhouse from auditing listed companies in India for two years after an investigation into a nearly decade-old accounting fraud case in a software services company that became India’s biggest corporate scandal.

SEBI has sought feedback and comments on the draft regulations over the next 30 days.

The Union Budget 2018-19 has rationalised the I-T Act provision relating to prosecution for failure to furnish returns.

Seeking to crackdown on shell companies, the government has proposed to remove exemption available to firms with tax liability of up to Rs 3,000 from filing I-T returns beginning next fiscal.

The Union Budget 2018-19 has rationalised the I-T Act provision relating to prosecution for failure to furnish returns.

Thus, a managing director or a director in charge of the company during a particular financial year could be liable for prosecution in case of any lapse in filing I-T returns for any financial year beginning April 1.

“The income tax departments would now track investments by these companies. Also, the focus will be on those firms that show less profit and also those who file I-T returns for the first time,” a senior finance ministry official said.

There are around 12 lakh active companies in the country, out of which about 7 lakh are filing their returns, including annual audited report, with the ministry of corporate affairs. Of this, about 3 lakh companies show ‘nil’ income.

The Section 276CC of the Income Tax Act provided that if a person wilfully fails to furnish in due time the return of income, he shall be punishable with imprisonment and fine.

However, no prosecution could be initiated if the tax liability of an assessee does not exceed Rs 3,000.

The government has amended the provision with effect from April 1, 2018 and removed the exemption available to companies.

“In order to prevent abuse of the said proviso by shell companies or by companies holding benami properties, it is proposed to amend the provisions… so as to provide that the said sub-clause shall not apply in respect of a company,” it said.

The official said that as many as 5 lakh are companies not filing returns and they could be a potential source of money laundering. “These could be small firms which are engaged in honest business, but there could be some which are a potential threat. We have to look into the data.”

Nangia & Co Managing Partner Rakesh Nangia said though the amendment has been brought about to prevent abuse by shell companies/benami properties, checks similar to those placed in the law for invoking GAAR, should be in place to avoid genuine hardship.

“Though the taxman may be driven by compulsions to ensure proper tax compliance, care must be taken while taking such action. In most developing countries, prosecution for tax matters is applied only in cases of serious tax frauds and not in general compliance matters,” Nangia said.

The Budget announcement follows the recommendation of the task force on shell companies, which was set up in February last year.

In the government’s fight against black money, shell companies have come to the fore as they are seen as potential for money laundering.

Till the end of December 2017, over 2.26 lakh companies were deregistered by the MCA for various non-compliances and being inactive for long.

Shell companies are characterised by nominal paid-up capital, high reserves and surplus on account of receipt of high share premium, investment in unlisted companies, no dividend income and high cash in hand.

Also, private companies as majority shareholders, low turnover and operating income, nominal expenses, nominal statutory payments and stock in trade, minimum fixed asset are some of the other characteristics.

Since last year, the Central Board of Direct Taxes (CBDT) — the apex policy making body of the I-T department — has been sharing with the MCA specific information like PAN data of corporates, Income Tax returns (ITRs), audit reports and statement of financial transactions (SFT) received from banks.