Institute of Chartered Accountants of India enable generation of UDIN (Unique Document Identification Number) for certification by its members

A provision for generating UDIN in bulk for Certificates has been incorporated in UDIN Portal.

Using this facility now the members will be able to generate UDIN in bulk (uptil 300 UDINs) for various types of Certificates in one go. It can be done through uploading of excel file.

Process for bulk UDIN

Step-wise complete process for generating bulk UDINs is as under:

i) After login, from the Menu bar, click on Bulk UDIN for Certificates. Minimum 3 certificates and Maximum 300 certificates can be generated using this procedure.

ii) Download template file from Download Template button and open in Excel. Please note that the .xlsx file can be opened in Excel 2007 and later versions.

iii) Select Certificate type from drop down.

iv) Input dates in the format as per your system/computer (generally it is in mm/dd/yyyy or as 10 June 2020). Excel will format dates automatically in required format i.e dd-mm-yyyy. Do not use copy paste in this cell.

v) Fill in all the parameters and values.

vi) Save the file.

vii) Click on the upload file on the Certificate Form on UDIN Portal.

viii) Select the file just saved now.

ix) Portal will populate the data in the Form. Verify the data so populated.

x) If correct, Send and Verify OTP and Submit.

xi) Alternatively, the option of filling the details of Type of Certificates, Dates and key fields etc. is available on the form itself.

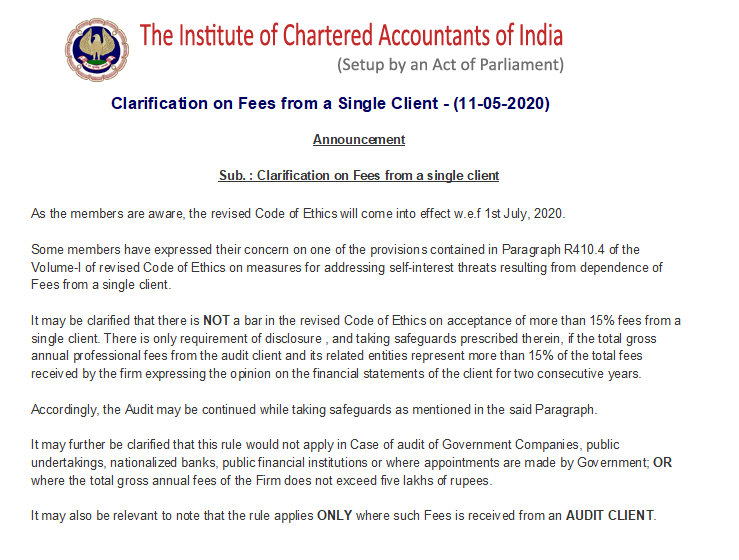

The Institute of Chartered Accountants of India ( ICAI ) has clarified that there is NOT a bar in the revised Code of Ethics on acceptance of more than 15% fees from a single client.

The ICAI has said that some members have expressed their concern on one of the provisions contained in Paragraph R410.4 of the Volume-I of revised Code of Ethics on measures for addressing self-interest threats resulting from the dependence of Fees from a single client.

The ICAI clarified that there is NOT a bar in the revised Code of Ethics on acceptance of more than 15% fees from a single client. There is the only requirement of disclosure, and taking safeguards prescribed therein, if the total gross annual professional fees from the audit client and its related entities represent more than 15% of the total fees received by the firm expressing the opinion on the financial statements of the client for two consecutive years.

Accordingly, the Audit may be continued while taking safeguards as mentioned in the said Paragraph. The ICAI further clarified that this rule would not apply in case of audit of Government Companies, public undertakings, nationalized banks, public financial institutions, or where appointments are made by Government; OR where the total gross annual fees of the Firm does not exceed five lakhs of rupees.

It may also be relevant to note that the rule applies ONLY where such Fees are received from an AUDIT CLIENT.

RBI is also likely to question the auditor on whether the SBI proposal would have any ‘material impact’ on the existing accounts of Yes Bank

The Reserve Bank of India will check if troubled lender Yes Bank’s auditor had raised any alarm in the past year. The apex bank has been in touch with the auditor and will look into whether they had specifically issued any warning in the past 12 months.

According to a report in The Economic Times, RBI has been in touch with auditor BSR & Co and wants to know if it had raised any red flag relating to the health of Yes Bank or any other issue. The auditor is part of KPMG India. The central bank is also likely to question the auditor on whether the SBI proposal would have any ‘material impact’ on the existing accounts of Yes Bank.

On Friday, the RBI announced a reconstruction scheme for the bank. It said that SBI that has expressed interest to invest in the troubled bank would do so to the extent of holding 49 per cent shareholding. The apex bank said that SBI’s investment in Yes Bank would not impact the employees and their current terms of employment.

BSR and Co was appointed as Yes Bank’s auditor after RBI banned SR Batliboi & Co for a year. The RBI had stated that the firm that was part of EY was banned due to “lapses identified in a statutory audit assignment carried out by the firm”.

RBI put restrictions on Yes Bank on March 6, allowing its customers to withdraw only Rs 50,000 for a month. The apex bank relaxed the guidelines subsequently. On Tuesday, the bank permitted its credit card customers to pay their credit card dues and loan obligations from other bank accounts. It allowed NEFT payments to clear loan EMIs and make credit card payments. The bank had, before that, allowed customers to withdraw money from ATMs of other banks.

The government had issued new norms for auditors, seeking more disclosures in reports, a move which comes after a series of corporate scams and frauds surfaced over the past few years.

CARO 2020 – Companies (Auditor’s Report) Order, 2020

MCA in place of existing the Companies (Auditor’s Report) Order, 2016, has notified CARO 2020 after consultation with the National Financial Reporting Authority constituted under section 132 of the Companies Act, 2013.

Auditor’s report to contain matters specified in paragraphs 3 and 4. – Every report made by the auditor under section 143 of the Companies Act on the accounts of every company audited by him, to which this Order applies, for the financial years commencing on or after the 1st April, 2019, shall in addition, contain the matters specified in paragraphs 3 and 4, of the CARO 2020.

Provided this Order shall not apply to the auditor’s report on consolidated financial statements except clause (xxi) of paragraph 3.

It shall come into force on the date of its publication in the Official Gazette.

CARO 2020 – Key changes/highlights

Matters to be included in auditor’s report, in CARO 2020 – the reporting clauses are more extensive and detailed than were in CARO2016

Unlike CARO 2016, which required reporting on all fixed assets, new reporting requirements pays attention to Property, Plant, Equipment and intangible assets.

Reporting on revaluation of Property, Plant and Equipments by company

Reporting of proceedings under the Benami Transactions (Prohibition) Act, 1988.

Reporting of compliances if company was sanctioned working capital limits in excess of Rs.5 crores or more from banks or financial institutions.

– whether the quarterly returns or statements filed by the company with such banks or financial institutions are in agreement with the books of account of the Company, if not, to give details;

Reporting of investments in or in providing of any guarantee or security or granting any loans or advances to companies, firms, Limited Liability Partnerships or any other parties.

Reporting of compliances with RBI directives and the provisions the Companies Act with respect to deemed deposits.

Reporting with respect to transactions not recorded in the books of account surrendered or disclosed as income in the income tax proceedings.

Comprehensive reporting requirement for default in the repayment of loans / other borrowings or in the payment of interest

– whether the company is a declared wilful defaulter by any bank or financial institution or other lender;

– whether term loans were applied for the purpose for which the loans were obtained; if not, the amount of loan so diverted and the purpose for which it is used may be reported;

– whether funds raised on short term basis have been utilised for long term purposes, if yes, the nature and amount to be indicated

Reporting on treatment by auditor of whistle-blower complaints received during the year by the company

Reporting on internal audit system

– whether the company has an internal audit system commensurate with the size and nature of its business;

– whether the reports of the Internal Auditors for the period under audit were considered by the statutory auditor;

Reporting on cash losses

Reporting on resignation of the statutory auditors

Reporting on uncertainty of company capable of meeting its liabilities

Reporting transfer of unspent CSR amount to Fund specified in Schedule VII

Reporting on qualifications or adverse remarks by the auditors in the CARO reports of companies included in the consolidated financial statements

It is expected that CARO, 2020 will improve the overall quality of reporting by the auditors and thereby lead to “greater transparency and faith in the financial affairs of the companies.”

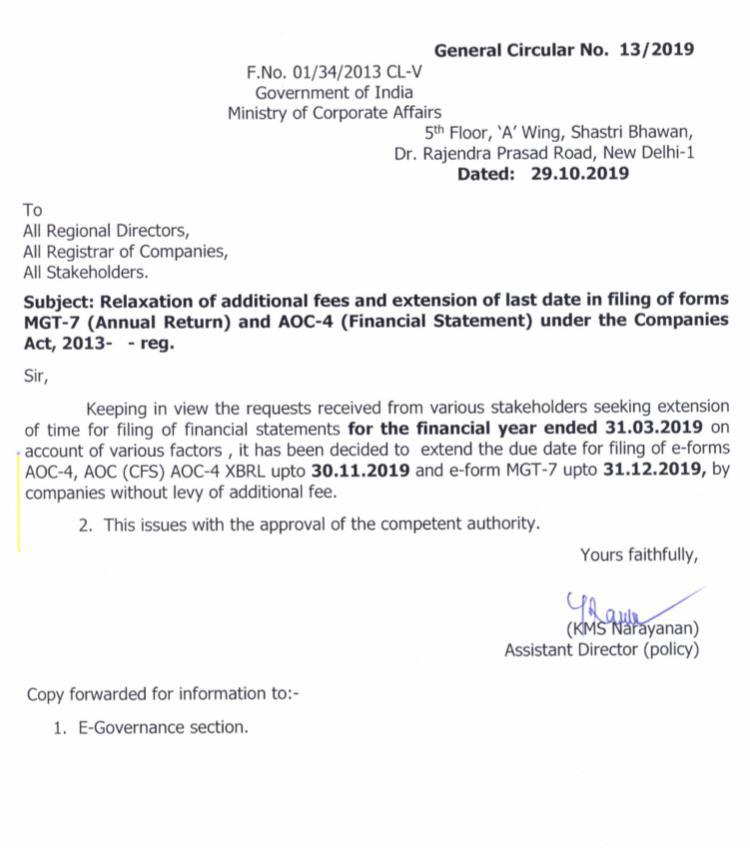

MCA extends due date for filing of AOC 4 and MGT 7 (Financial Statements & Annual Return)

MCA has notified that the due date for filing of financial statements and annual return in e-forms AOC 4, AOC (CFS) and AOC-4 XBRL upto 30 Nov. 2019 and e-form MGT 7 up to 31 Dec. 2019 by companies without levy of additional fee, in view of the practical difficulties faced by various stakeholders and the requests from various professional bodies and businesses, as under:

The due dates for filing Financial Statements – AOC-4, was 30 Oct,2019 and for the Annual Returns – MGT-7 was 30 Nov,2019. Both these are now relaxed by additional 1 more month for filing with Ministry of Corporate Affairs, without levy of additional fee.

Clarification on Auditor’s Certificate on Return of Deposits pursuant to Rule 16 of the Companies (Acceptance of Deposits) Rules, 2014

This has reference to Rule 16 of the Companies (Acceptance of Deposits) Rules, 2014 and further amendments.

In this regard, the Ministry of Corporate Affairs vide its letter no. File No: P-01/08/2013- CL-V Vol. VI dated June 24, 2019 has clarified on the matter as under:

The Auditor’s Certificate is mandatory only in case of return of deposits.

For filing particulars of transactions not considered as deposits information contained therein as on 31st March of that year need not be from the duly audited Financial Statement.

Only in case of Return of Deposit information contained therein as on 31st March of that year should be from duly audited financial statement of the company.

Also in order to provide guidance to members, the Auditing and Assurance Standards Board of ICAI has issued Illustrative Auditor’s Certificate on Return of Deposits, which is available on the below cited link:

ICAI have launched Unique Document Identification Number (UDIN) facility which is a unique number, which will be generated by the system for every document certified/ attested by a Chartered Accountant and registered with the UDIN portal available at https://udin.icai.org/ with effect from 1st July 2018.

It has been noticed that financial statements and documents were being certified/attested by third persons, in lieu of Chartered Accountants. As these statements are being relied upon by the authorities as true statements and certificates, UDIN can be generated by a practicing CA by registering his/her documents/ certificates on UDIN Portal for verification.

A practicing Chartered Accountant can generate a UDIN for certificate/ document attested by him either in individual capacity or as a partner.

At present, this facility is recommendatory. But ICAI is mulling to make the same compulsory in near future, so as to curb the menace of fake or forged documents.

No change is possible in the data already registered by a Chartered Accountant in the online system. Therefore, members are requested to thoroughly check the details in preview option before submission of their application.

Information filled in can be edited/ modified any number of times before the submission. But once it is submitted, it cannot be edited.

The UDIN once generated can be withdrawn or cancelled with narration. Hence if any user search for this UDIN, appropriate narration indicated by Member with the date of revoke will be displayed for reference.