GST Network (GSTN), the company handling IT infrastructure for the indirect tax regime, has from October 10 started issuing refunds to exporters for Integrated GST (IGST).

Exporters can soon start claiming refunds for GST paid in August and September as GSTN will this week launch an online application for processing of refund, its Chief Executive Officer Prakash Kumar said today.

GST Network (GSTN), the company handling IT infrastructure for the indirect tax regime, has from October 10 started issuing refunds to exporters for Integrated GST (IGST) they paid for the month of July, after matching GSTR-3B and GSTR-1.

For August and September, while the initial return GSTR- 3B has already been filed, the final return GSTR-1 has not yet been filed.

“A separate online app for claiming Integrated GST (IGST) refunds for August and September would be made available on GSTN portal this week,” Kumar told .

GSTN has developed the app wherein exporters can save and upload their sales data which are part of GSTR-1 after filling up export details in Table 6A.

The table will be then extracted separately and after exporters digitally sign it, it would automatically go to the customs department.

The customs department will then validate the information provided in the table with the shipping bill data and also the taxes paid in GSTR-3B. The refund amount would be either credited to exporter’s bank account through ECS or a cheque would be issued.

As per data, 55.87 lakh GSTR-3B returns were filed for July, 51.37 lakh for August and over 42 lakh for September. Preliminary returns GSTR-3B for a month is filed on the 20th day of the next month after paying due taxes.

Thereafter, final returns in form GSTR-1, 2, 3 are filed by businesses giving invoice wise details of sales. The final return filing for August and September has not started yet.

Over July-August, an estimated Rs 67,000 crore has accumulated as the Integrated GST (IGST), of which only about Rs 5,000-10,000 crore will be due as refunds to exporters.

The Goods and Services Tax (GST), the amalgamation of over a dozen indirect taxes like excise duty and VAT, does not provide for any exemption, and so exporters are required to first pay Integrated-GST (IGST) on manufactured goods and claim refunds after exporting them. This had put severe liquidity crunch, particularly on aggregators or merchant exporters.

To ease their problems, the GST Council earlier this month decided a package for them that includes extending the Advance Authorisation / Export Promotion Capital Goods (EPCG) / 100 per cent EOU (Export Oriented Unit) schemes to sourcing inputs from abroad as well as domestic suppliers till March 31, thus not requiring to pay IGST.

The government is aiming to clear pending GST refunds of exporters by November-end. The first cheque after processing of July refunds was issued on October 10.

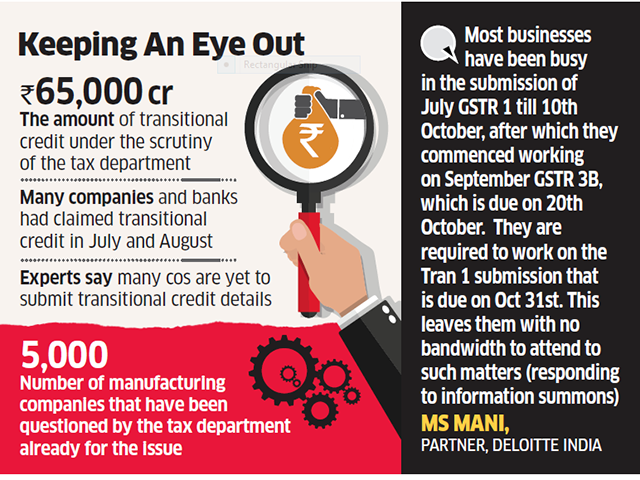

Of the total Rs 95,000 crore GST collected in July, about Rs 65,000 crore was claimed in refunds or transitional credit.

The tax department has sought explanations from banks and financial institutions, including multinationals, on transitional credit claimed by them in July under the goods and services tax (GST) regime, two people with direct knowledge of the matter said. Deputy commissioners and assistant commissioners (central tax) have issued ‘information summons’ in the last seven days seeking data in five specific areas “by e-mail/hard copy”.

These include past sales tax records; summary of closing balance of tax (as of June); description of the nature of credits; details of vendor invoices prior to July 1; and details of payments made to vendors and service providers after July 1. Transitional credit refers to tax credits on sales tax, excise and valued-added tax accumulated before July 1 on pre-GST stock.

Such credit can be set off against liabilities of the July-started GST.

Taxmen suspect some companies are misusing the provision and have filed fake returns to claim high transitional credits. Of the total Rs 95,000 crore GST collected in July, about Rs 65,000 crore was claimed in refunds or transitional credit. The move comes about two weeks after tax officers questioned manufacturing companies on transitional credit claimed by them.

ET was the first to report on September 21that about 5,000 such companies had been questioned by the taxman over transitional credit claims. For now, tax officers are only scrutinising transition credit for sales tax and excise. The data obtained from the banks and financial institutions will be examined for any discrepancies.

The firms said they haven’t been given much time to provide the information. “We had received the notice few days back and haven’t been able to submit it due to the enormity of information sought,” said the finance head of a major multinational bank. “A tax officer called me today (on Friday) and asked me to submit the required documents by Saturday.”

The finance head cited the tax officer as saying the transitional credit claimed by the bank was high. “I tried to explain that transitional credit has to be viewed in the context of our monthly tax outgo. But we will be submitting the required information nevertheless by Saturday,” he said. Experts said many companies are yet to submit transitional credit details, which has to be done through the Transform.

“Since the date for filing the Tran-1 form has been extended to October 31, it would be prudent to commence any enquiries thereafter,” said MS Mani, partner, Deloitte India. “It is advisable to consider the data submitted in the Tran-1 form and then enquire into those cases where any anomalies are detected instead of subjecting the entire data submitted by erstwhile service tax payers to any form of scrutiny.”

The pressure on tax officials increased after a letter by a senior member of the Central Board of Excise and Customs (CBEC) was sent on Wednesday to all tax commissioners. ET has seen the letter. “In view of the urgency of the matter kindly have the verification of transitional credit completed on priority (in respect of list of taxpayers forwarded on 11/9/2017) and a report on the same to be sent on this office not later than 15/10/2017,” the letter read. The letter also asked tax officers to submit a detailed analysis of transitional credit claims. This is expected to be submitted by November 3.

The Central Board of Excise and Customs had in September sent a list to all commissioners and joint commissioners that included state-wise details of companies, the GST number and transition credit amount. Tax officers had started calling all the companies whose transitional credit numbers seemed high to them.

GST Council has considered the implementation experience of the last 3 months and gave relief to small traders, says Arun jaitley.

More than three months after the Goods and Services (GST) was introduced, the GST Council made a number of big changes today, to give some relief to small and medium businesses (SMEs) on filing and payment of taxes. The panel also eased rules for exporters and cut tax rates on some items. Those businesses with annual turnover of up to Rs 1.5 crore and which constitute 90 percent of the taxpayer base but pay only 5-6 percent of overall tax, have been permitted to file quarterly income returns. “GST Council has considered the implementation experience of the last 3 months and gave relief to small traders… Compliance burden of medium and small taxpayers in GST has been reduced,” Finance Minister Arun Jaitley said. The SMEs had earlier complained of tedious compliance burden under the new regime. Below is the full text of the recommends made by GST today:

The GST Council, in its 22nd Meeting which was held today in the national capital under Chairmanship of the Union Minister of Finance and Corporate Affairs, Shri Arun Jaitley has recommended the following facilitative changes to ease the burden of compliance on small and medium businesses:

Composition Scheme

1. The composition scheme shall be made available to taxpayers having annual aggregate turnover of up to Rs. 1 crore as compared to the current turnover threshold of Rs. 75 lacs. This threshold of turnover for special category States, except Jammu & Kashmir and Uttarakhand, shall be increased to Rs. 75 lacs from Rs. 50 lacs. The turnover threshold for Jammu & Kashmir and Uttarakhand shall be Rs. 1 crore. The facility of availing composition under the increased threshold shall be available to both migrated and new taxpayers up to 31.03.2018. The option once exercised shall become operational from the first day of the month immediately succeeding the month in which the option to avail the composition scheme is exercised. New entrants to this scheme shall have to file the return in FORM GSTR-4 only for that portion of the quarter from when the scheme becomes operational and shall file returns as a normal taxpayer for the preceding tax period. The increase in the turnover threshold will make it possible for greater number of taxpayers to avail the benefit of easier compliance under the composition scheme and is expected to greatly benefit the MSME sector.

2. Persons who are otherwise eligible for composition scheme but are providing any exempt service (such as extending deposits to banks for which interest is being received) were being considered ineligible for the said scheme. It has been decided that such persons who are otherwise eligible for availing the composition scheme and are providing any exempt service, shall be eligible for the composition scheme.

3. A Group of Ministers (GoM) shall be constituted to examine measures to make the composition scheme more attractive.

Relief for Small and Medium Enterprises

4. Presently, anyone making inter-state taxable supplies, except inter-State job worker, is compulsorily required to register, irrespective of turnover. It has now been decided to exempt those service providers whose annual aggregate turnover is less than Rs. 20 lacs (Rs. 10 lacs in special category states except J & K) from obtaining registration even if they are making inter-State taxable supplies of services. This measure is expected to significantly reduce the compliance cost of small service providers.

5. To facilitate the ease of payment and return filing for small and medium businesses with annual aggregate turnover up to Rs. 1.5 crores, it has been decided that such taxpayers shall be required to file quarterly returns in FORM GSTR-1,2 & 3 and pay taxes only on a quarterly basis, starting from the Third Quarter of this Financial Year i.e. October-December, 2017. The registered buyers from such small taxpayers would be eligible to avail ITC on a monthly basis. The due dates for filing the quarterly returns for such taxpayers shall be announced in due course. Meanwhile, all taxpayers will be required to file FORM GSTR-3B on a monthly basis till December, 2017. All taxpayers are also required to file FORM GSTR-1, 2 & 3 for the months of July, August and September, 2017. Due dates for filing the returns for the month of July, 2017 have already been announced. The due dates for the months of August and September, 2017 will be announced in due course.

6. The reverse charge mechanism under sub-section (4) of section 9 of the CGST Act, 2017 and under sub-section (4) of section 5 of the IGST Act, 2017 shall be suspended till 31.03.2018 and will be reviewed by a committee of experts. This will benefit small businesses and substantially reduce compliance costs.

7. The requirement to pay GST on advances received is also proving to be burdensome for small dealers and manufacturers. In order to mitigate their inconvenience on this account, it has been decided that taxpayers having annual aggregate turnover up to Rs. 1.5 crores shall not be required to pay GST at the time of receipt of advances on account of supply of goods. The GST on such supplies shall be payable only when the supply of goods is made.

8. It has come to light that Goods Transport Agencies (GTAs) are not willing to provide services to unregistered persons. In order to remove the hardship being faced by small unregistered businesses on this account, the services provided by a GTA to an unregistered person shall be exempted from GST.

Other Facilitation Measures

9. After assessing the readiness of the trade, industry and Government departments, it has been decided that registration and operationalization of TDS/TCS provisions shall be postponed till 31.03.2018.

10. The e-way bill system shall be introduced in a staggered manner with effect from 01.01.2018 and shall be rolled out nationwide with effect from 01.04.2018. This is in order to give trade and industry more time to acclimatize itself with the GST regime.

11. The last date for filing the return in FORM GSTR-4 by a taxpayer under composition scheme for the quarter July-September, 2017 shall be extended to 15.11.2017. Also, the last date for filing the return in FORM GSTR-6 by an input service distributor for the months of July, August and September, 2017 shall be extended to 15.11.2017.

12. Invoice Rules are being modified to provide relief to certain classes of registered persons.

While the number of businesses registered for the goods and services tax (GST) has crossed 90 lakh, much higher than tax base in the previous regime, filing of even the interim (summarised) returns and tax payments are not keeping pace.

While the number of businesses registered for the goods and services tax (GST) has crossed 90 lakh, much higher than tax base in the previous regime, filing of even the interim (summarised) returns and tax payments are not keeping pace. Just over 30 lakh taxpayers have filed the interim return (GSTR-3B) for August, before the stipulated September 20 deadline, GST Network (GSTN) chairman Ajay Bhushan Pandey told FE. The glitches plaguing GSTN, the inability of a sizeable section of SMEs to comply and a general lackadaisical tendency among taxpayers are said to be reasons for the slack in the return-filing process. But the filing pace for August was not much slower than it for July GST — by August 20, the initial deadline for GST payment for July, only 32 lakh taxpayers filed the interim return and made tax payments; the figure rose to 39 lakh by August 29, the extended deadline without penal interest, and then to 49 lakh till date.

While about Rs 92,300 crore was collected as GST for July till August 20, a similar amount has been paid by the taxpayers till Wednesday for August GST, sources said. To make things easier for the business, the GST Council had extended the last dates for filing detailed returns — GSTR1, GSTR2 and GSTR3 — but businesses need to pay the tax with GSTR-3B filing. However, the slow pace at which even the interim returns are being filed is vexing the government — a TV channel reported that finance minister Arun Jaitley has asked the Central Board of Excise and Customs to submit daily reports of GST filings. With the GSTR1 for outward supplies for the month of July can now be filed until October 10 and GSTR2 for inward supplies by October 31, the government is now putting in place an interim arrangement for refund of taxes to exporters, as waiting for these funds for longer periods could hit the liquidity of thousands of exporters. Pandey said that some assessees were still filing return for July along with August. For July, there were nearly 60 lakh eligible taxpayers and this number must have moved up for August and new registrants are being added.

Pandey said the GSTN portal could handle the sudden rush in filings in the last two to three days, which displayed its robustness. He said GSTN accepted up to 85,000 returns per hour on Wednesday, as nearly 14 lakh assessees filed the interim summarised return on that day. While the government is keeping its fingers crossed on the GST revenue, analysts expect it to cut rates — at least for the goods that fall under 28% slab — given the robustness of collections. The government is closely examining the huge transitional credit claims of Rs 65,000 crore by the industry — these can be availed of by the industry against its supplies in the next six months. Sanjay Garg, partner, indirect tax, KPMG in India, said: “Expansion in the tax base at the outset due to the applicability of GST on transactions not taxed before would likely shrink after the industry avails the credit generated by payment of tax on such newly-taxable transactions. The GST collections might decline. It is apparent that fingers would remain crossed at least for next two quarters of (FY18).” Earlier this month, the GST Council had constituted a group of ministers (GoM) under Bihar deputy chief minister Sushil Modi, to resolve issues faced by businesses while filing returns and paying taxes on GSTN portal. The GoM met earlier this week, and assured taxpayers that most technical glitches in GSTN would be resolved by October-end.

Recommendations made by the GST Council in the 21st meeting at Hyderabad on 9th September, 2017

Press Information Bureau

Government of India

Ministry of Finance

09-September-2017 20:19 IST

The GST Council, in its 21st meeting held at Hyderabad on 9th September 2017, has recommended the following measures to facilitate taxpayers:

a) In view of the difficulties being faced by taxpayers in filing returns, the following revised schedule has been approved:

Sl. No.

Details / Return

Tax Period

Revised due date

1

GSTR-1

July, 2017

10-Oct-17

For registered persons with aggregate turnover of more than Rs. 100 crores, the due date shall be 3rd October 2017

2

GSTR-2

July, 2017

31-Oct-17

3

GSTR-3

July, 2017

10-Nov-17

4

GSTR-4

July-September, 2017

18-Oct-17 (no change)

Table-4 under GSTR-4 not to be filled for the quarter July-September 2017. Requirement of filing GSTR-4A for this quarter is dispensed with.

5

GSTR-6

July, 2017

13-Oct-17

Due dates for filing of the above mentioned returns for subsequent periods shall be notified at a later date.

b) GSTR-3B will continue to be filed for the months of August to December, 2017.

c) A registered person (whether migrated or new registrant), who could not opt for composition scheme, shall be given the option to avail composition till 30th September 2017 and such registered person shall be permitted to avail the benefit of composition scheme with effect from 1st October, 2017.

d) Presently, any person making inter-state taxable supplies is not eligible for threshold exemption of Rs. 20 lacs (Rs. 10 lacs in special category states except J & K) and is liable for registration. It has been decided to allow an exemption from registration to persons making inter-State taxable supplies of handicraft goods upto aggregate turnover of Rs. 20 lacs as long as the person has a Permanent Account Number (PAN) and the goods move under the cover of an e-way bill, irrespective of the value of the consignment.

e) Presently, a job worker making inter-State taxable supply of job work service is not eligible for threshold exemption of Rs. 20 lacs (Rs. 10 lacs in special category states except J & K) and is liable for registration. It has been decided to exempt those job workers from obtaining registration who are making inter-State taxable supply of job work service to a registered person as long as the goods move under the cover of an e-way bill, irrespective of the value of the consignment. This exemption will not be available to job work in relation to jewellery, goldsmiths’ and silversmiths’ wares as covered under Chapter 71 which do not require e-way bill.

f) FORM GST TRAN-1 can be revised once.

g) The due date for submission of FORM GST TRAN-1 has been extended by one month i.e. 31st October, 2017.

h) The registration for persons liable to deduct tax at source (TDS) and collect tax at source (TCS) will commence from 18th September 2017. However, the date from which TDS and TCS will be deducted or collected will be notified by the Council later.

The GST Council has decided to set up a committee consisting of officers from both the Centre and the States under the chairmanship of the Revenue Secretary to examine the issues related to exports.

The GST Council has also decided to constitute a Group of Ministers to monitor and resolve the IT challenges faced during GST implementation.

Aadhaar has now been made mandatory for so many things, including availing the benefits of various social and government schemes.

If you thought that filing an income tax return or opening a bank account are the only few things which require Aadhaar cards now, then think again. The fact is Aadhaar has now been made mandatory for so many things, including availing the benefits of various social and government schemes. While for some schemes it has already been made compulsory, for some others it will be made mandatory soon. Here we are taking a look at 10 such things:

Income Tax Return: If you have an Aadhaar card, then you are required to link your Aadhaar number to your PAN card for filing your income tax return. Although the deadline for linking one’s Aadhaar number has now been extended to December 31, 2017, however your income tax returns will not be processed by the Income Tax Department unless you link your Aadhaar number to your PAN card. Having an Aadhaar card also makes e-verification of income tax return quick and easy.

Opening of Bank Account: Possessing an Aadhaar card has now been made mandatory for opening a bank account. You are also required to link your Aadhaar number to your existing bank account. The government has laid a deadline of 31st December 2017 for this activity. Also, it is pretty easy to open a bank account using the Aadhaar card. Since the Aadhar card can be used as a proof of identity as well as a proof of address, it reduces the number of documents that are required for opening a bank account.

Banking transactions of Rs 50,000 or above: It is now necessary to submit your Aadhaar number in banking transactions of Rs 50,000 or above. As per a gazette notification of the Ministry of Finance, dated 1st June 2017, Aadhaar will now be sought for all transactions for an amount Rs 50,000 or above.

Mutual Fund Accounts: It has also been made mandatory to link one’s Aadhaar number to one’s mutual fund account, if one invests in mutual funds. The government has set the deadline of December 31, 2017, for doing this. If one fails to do this by this time, then one’s MF account will become inactive.

Digital Locker: The government has introduced an online locker system to store personal documents on the government server. An account in DigiLocker can now be opened only if a person has an Aadhaar card.

Student Scholarship: In order to receive government scholarship, students have to link their Aadhaar number to their bank accounts.

Provident Fund: One can apply for the Employee Provident Fund (EPF) withdrawal online only if the Aadhaar number is linked with one’s EPF account.

Monthly Pension: Just like EPF, it is mandatory to quote one’s Aadhaar number to receive pension. This rule has been levied to make sure that there are no fraudulent pensions given out. However, this rule is state-specific.

E-KYC for mobile number: The Telecom Ministry has issued an order to the telecom companies to e-verify every user’s phone number using their Aadhaar card.

Gas subsidy: Pratyaksh Hanstantrit Labh (PAHAL) scheme, also know as Direct Benefit Transfer for LPG (DBTL), involves linking of one’s Aadhaar number to the gas connection in order to receive a subsidy on LPG directly to one’s bank account.

In a major clampdown against black money, the government on Tuesday directed freezing bank accounts of more than 2.09 lakh companies whose names have been struck off from the records and said action would be taken against more such firms.

Banks have also been asked to step up their vigil against those companies that are non-compliant with various regulations and not carrying out business activities for long, a senior finance ministry official said as authorities continue their crackdown against shell entities The official said banks have been directed to freeze the bank accounts of these deregistered companies.

While warning that action would be taken against erring firms, the official said the efforts would help in enhancing corporate governance standards as well as clean up the system that otherwise is prone to be misused.

The names of over 2.09 lakh firms have been struck off from register of companies for failing to comply with regulatory requirements

“The names of 2,09,032 companies have been struck off from the register of companies under Section 248 (5) of the Act. The existing directors and authorised signatories of such struck-off companies will now become ex-directors or ex- authorised signatories,” an official release said

Section 248 of the Companies Act – which is implemented by the corporate affairs ministry – provides powers to strike off names of companies from the register on various grounds including for being inactive for long.

According to the official, since these companies had ceased to be legal entities, there was no reason having active bank accounts which could be prone to misuse.

Once these companies become compliant, banks would activate their accounts, the official added. “Furthering our war against #BlackMoney, banks have been advised to immediately restrict bank accounts of struck-off companies,” Minister of State for Corporate Affairs P P Chaudhary said in a tweet.

The official said a detailed analysis has been initiated to check whether these deregistered companies were used as conduits for channelising unaccounted money into the system, especially during demonetisation.

Amid efforts against shell companies which are allegedly used as conduits for illicit fund flows and tax evasion, the government said the directors of deregistered firms would not be able to operate the bank accounts till these entities are legally restored

About the directors and signatories of the over 2.09 lakh firms, the government said they would not be able to operate bank accounts of such companies till these entities are legally restored. The restoration, as and when it happens, would be reflected in the official records by way of change in the status from ‘struck off’ to ‘active’. “Since such ‘struck off’ companies have ceased to exist, action has been initiated to restrict the operation of bank accounts of such companies,” the release said.

The Department of Financial Services, through the Indian Banks Association, has advised banks that they should take immediate steps to put restrictions on bank accounts of such struck-off companies. “In addition to such struck-off companies, banks have also been advised to go in for enhanced diligence while dealing with companies in general,” the release said.

A company even having an active status on the corporate affairs ministry website but defaulting in filing of its due financial statements or annual returns, among others, “should be seen with suspicion as, prima facie, the company is not complying with its mandatory statutory obligations”. In another tweet, Chaudhary said the ministry is committed “in attaining @narendramodi ji’s vision of eliminating black money”.