RBI is also likely to question the auditor on whether the SBI proposal would have any ‘material impact’ on the existing accounts of Yes Bank

The Reserve Bank of India will check if troubled lender Yes Bank’s auditor had raised any alarm in the past year. The apex bank has been in touch with the auditor and will look into whether they had specifically issued any warning in the past 12 months.

According to a report in The Economic Times, RBI has been in touch with auditor BSR & Co and wants to know if it had raised any red flag relating to the health of Yes Bank or any other issue. The auditor is part of KPMG India. The central bank is also likely to question the auditor on whether the SBI proposal would have any ‘material impact’ on the existing accounts of Yes Bank.

On Friday, the RBI announced a reconstruction scheme for the bank. It said that SBI that has expressed interest to invest in the troubled bank would do so to the extent of holding 49 per cent shareholding. The apex bank said that SBI’s investment in Yes Bank would not impact the employees and their current terms of employment.

BSR and Co was appointed as Yes Bank’s auditor after RBI banned SR Batliboi & Co for a year. The RBI had stated that the firm that was part of EY was banned due to “lapses identified in a statutory audit assignment carried out by the firm”.

RBI put restrictions on Yes Bank on March 6, allowing its customers to withdraw only Rs 50,000 for a month. The apex bank relaxed the guidelines subsequently. On Tuesday, the bank permitted its credit card customers to pay their credit card dues and loan obligations from other bank accounts. It allowed NEFT payments to clear loan EMIs and make credit card payments. The bank had, before that, allowed customers to withdraw money from ATMs of other banks.

A government-appointed panel on regulating auditors and the networks had suggested that the fee from non-audit services should not be more than 50% of the audit fee.

India is considering tougher rules for audit firms, including a cap on the number of listed companies they can examine, according to a person with knowledge of the matter, as the government seeks to tighten oversight after a recent spate of governance lapses.

In India, 70% of the about 1,800 companies that trade on the National Stock Exchange are audited by firms affiliated to EY, Deloitte & Touche, KPMG and PWC, according to Delhi-based Prime Database. Current rules stipulate that individual auditors can examine accounts of up to 20 companies, though there is no limit on number of audits for the company.

The Big Four in India operate through a network of local chartered accountants firms. One way for them is to partner as a member of a local firm. They can also allow their brand name to be used by sub-licensee of a member local firm. The ministry hasn’t decided if the cap on audits will be at the group level or on each member firm, the person said.

The government is planning to expand the list of services which can’t be offered by statutory auditors under the Companies Act. Currently, statutory auditors can’t offer nine services, directly or indirectly, including internal audit, investment banking, and actuarial services. There is no restriction on providing services such as taxation or restructuring and valuation.

One option is to tweak the present cap on fees that can be generated through offering non-audit services, the person said. This cap, fixed in 2002, says fees from non-audit work can’t be more than the aggregate statutory audit fees. A spokeswoman for the corporate affairs ministry declined to comment.

A government-appointed panel on regulating auditors and the networks had suggested that the fee from non-audit services should not be more than 50% of the audit fee.

Deloitte Ban

Governance lapses and negligence has loaded the nation’s banks with one of the world’s worst piles of bad debt. In some cases, allegations of fund diversion have surfaced, while the founders of some shadow banks have faced accusations of accepting kickbacks in exchange for loans.

The corporate affairs ministry earlier this month sought a ban on Deloitte Haskins & Sells and BSR & Co. for their role as auditors to IL&FS Financial Services, a part of the IL&FS Group that was seized by the government last year after a string of debt defaults.

Deloitte in an emailed statement said it’s fully compliant with Indian audit standards, while BSR said it would defend its position in accordance with the law.

Meanwhile, the banking regulator forbid EY affiliate S. R. Batliboi & Co. from taking on bank audits for a year and, in 2018, the markets watchdog banned the local unit of PricewaterhouseCoopers LLP for two years in relations to work from a decade earlier.

Move in response to falling GST revenue collections

The GST Council may move the sales and purchase invoice matching system to the back end. It will do so to keep tabs on missing transactions and check over-claim of input tax credits in the goods and services tax (GST).

At present, assessees claim input credits themselves by filing summary input- output returns, and the tax authorities do not have any clue whether the claims are correct or not. The process of invoice matching was supposed to be done by the assessees, though it was deferred till March. However, slowing GST revenues have now prompted the government to design an alternative mechanism, under which tax officials will do the matching themselves.

“Instead of asking taxpayers to match invoices, we may do it ourselves at the back end. We may follow a risk-based approach; when the gross level of transactions does not match, we may match invoices,” an official said, adding the proposal was under consideration.

GSTR-1 (sales) and GSTR-2 (purchase) returns have to be matched with GSTR-3 to ensure that claims by taxpayers are correct. Both GSTR-2 and GSTR-3 returns have been postponed.

A committee, under GSTN Chairman Ajay Bhushan Pandey, is looking at ways of making the filing of the GSTR-2 and GSTR-3 forms business-friendly. The time period for filing the GSTR-2 and GSTR-3 forms for the months of July to March is also being worked out. The committee has recommended merging the GSTR-1, 2 and 3 forms as one option to simplify filing returns.

According to estimates, there is a 15-20 per cent GST revenue leakage at the moment.

GSTR-1 is used to file details of outward sales of a dealer. After submission, the details of purchases made by the dealer are automatically populated in the GSTR-2 form. The dealer is required to verify the details and submit the form. Finally, GSTR-3 calculates a taxpayer’s tax liability and the available input tax credit.

GST revenue collections touched their lowest in November at ~808 billion. According t0o the government’s estimates, if this trend continues, there could be a shortfall of ~250-300 billion in indirect tax collections this fiscal year. The government had attributed the slowing revenue to postponement of features of the GST such as matching of returns, electronic way bills and the reverse charge mechanism.

The revenue slowdown prompted the GST Council to call an urgent meeting on December 16 and advance the introduction of the electronicway bill for inter-state movements of goods to February 1 and for intra-state carriage from June 1.

“It is important that the concept of invoice matching continues as it is part of the basic design of the GST. If it is not done electronically, it will be needed at the time of assessment or audit, which will lead to more paperwork. The process can, however, be simplified,” said Pratik Jain, leader-indirect taxes, PwC India.

M S Mani, senior director-indirect taxes, Deloitte, said invoice matching provided taxpayers the ability to view transactions and take corrective steps on an ongoing basis. “While this may be cumbersome for small businesses, there are significant benefits for taxpayers and the government. However, the technology challenges will have to be overcome so that the matching happens seamlessly online in real time,” he said.

Bipin Sapra, partner— indirect taxes, EY, said, “In the absence of invoice level matching, the alternative is to match revenues and credits with GSTR1 but since the process will not be automated, it will be possible for a limited number of clients on the basis of risk assessment.”

Union minister for shipping Nitin Gadkari on Tuesday announced that the government has identified five major ports — Mumbai, Mormugao, Mangalore, Chennai and Cochin — to boost cruise tourism in India.

While the number of Indians who took a cruise in 2016-17 was 2 lakh, the number could go up to 40 lakh, according to a report prepared by consultants Bermelo & Ajamil jointly with Ernst & Young. Of this, 80% or 32 lakh passengers are expected to take cruises from the Mumbai port alone.

However, Gadkari added that the cruise tourism industry is facing challenges on many issues and that he would make a representation to the finance ministry to waive the goods and services tax (GST), levied at 5% currently on all cruise ships, as well as establish a zero income tax regime.

While the largest cruise line operator, Carnival PLC, is looking to increase the number of cruise liners in India, David Dingle, the company’s chairman told FE that the country must create a domestic cruising tax regime competitive with tax regimes elsewhere in the world.

“In principle, the cruise industry will not come to a part of the world where it has to pay GST on the ticket price and on the sales made on board. We will not bring our ships here in any significant numbers all the while that cruising attracts any GST,” he said. Moreover, Dingle added that international cruise companies have to have the right to repatriate their profits through double tax treaties.

Carnival PLC sold 181,000 cruises in India in 2016, registering a compounded annual growth rate of 31%.

Current estimates are that over 120,000 Indians book a cruise each year with over 90% of them travelling to Singapore to board a cruise liner. To cater to this growing market, the Indian government wants to increase the number of cruise liners that come to India, eliminating the need for cruise seekers to fly abroad to board a ship.

The Indian coastline saw 150 cruise ship visits in 2016 and the government is aiming to increase this to about 955 in the next few years.

The government has made quoting the Aadhaar number a must at the time of applying for a permanent account number, or PAN, card.

Individuals having permanent account number (PAN) will have to link it to their existing Aadhaar number from 1 July, a Finance Ministry notification said on Wednesday.

Amending income tax rules, the government has made quoting the 12-digit identification number or Aadhaar enrolment ID compulsory while applying for PAN, which is mandatory for filing tax returns, opening of bank accounts and financial transactions beyond a threshold.

Every person who has been allotted PAN as on the 1st day of July shall intimate his Aadhaar number to the tax authorities, the notification from revenue department said.

Biometrics identification enabled by Aadhaar proves the identity of the PAN holder and helps tax authorities to crack cases of multiple PANs held by the same person with the idea of tax evasion. As many as 20.7 million taxpayers have already linked their Aadhaar with PAN. There are over 250 million PAN card holders in the country while Aadhaar has been issued to 1.15 billion people.

The rule will come into force from 1 July, the revenue department said while amending Rule-114 of the Income Tax Act, which deals in application for allotment of PAN.

Earlier this month, the tax department had clarified that the relief granted by the Supreme Court regarding non-cancellation of PAN for not linking Aadhaar with it was applicable only in cases of people who do not have Aadhaar and do not wish to obtain it for the time being. Their PAN cards will not be treated as invalid. For tax filing, Aadhaar is mandatory from 1 July.

“The notification does not specify the form and manner in which Aadhaar should be intimated, neither the timelines for such intimation have been set out,” said Sonu Iyer, tax partner and people advisory services leader, EY.

“Individuals having a PAN but no Aadhaar application number who would be filing an income tax return post June 30, 2017 will need to apply for Aadhaar in order to be able to file the income tax return. Individuals who are not required to file an income tax return but who have a PAN and are eligible to obtain Aadhaar (whether they have one or not) as on July 1, 2017 should wait for further notification which will specify the date and manner in which the two identification numbers shall be linked,” added Iyer.

Aadhaar-linked PAN enables taxpayers to verify their returns through a one-time password sent to their phone numbers at the time of filing returns. This makes return filing easier as there is no need for an e-filer to send a signed physical copy of the return to the department, completing the legal formality of filing. Aadhaar and the password performs the verification function of an assessee’s signature in a physical copy of the return that pledges the information furnished to be true.

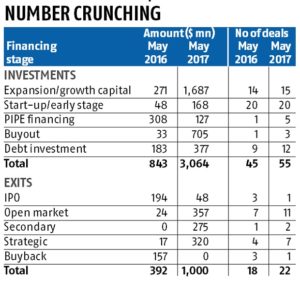

PE, Venture Capital flows up 155% in May to $ 3 billion; SoftBank – Paytm deal tops

Private equity and venture capital (PE/VC) investments have recorded the highest monthly investments in the past 10 years at $3.1 billion in May 2017. For the third consecutive month in a year, the investment flow crossed the $2-billion mark.

The financial services sector topped the table on account of the $1.4-billion investment by Softbank in Paytm. This deal accounted 46 per cent of aggregate deal value for the month.

According to Ernst & Young (EY) data, the month recorded a 264 per cent increase in terms of value and 23 per cent in volume over May 2016. PE/VCs have invested $3,064 million across 55 deal in May this year as against $843 million across 45 deals in May 2016.

There were five deals of more than $100 million aggregating to $2.3 billion, accounting for 75 per cent of the aggregate deal value in May 2017.

Another important deal during the month was the $500-million investment by Canada Pension Plan Investment Board (CPPIB) in Indospace (a real estate platform for industrial and logistics parks) for a majority stake, thus taking the investments by Canadian pension funds in 2017 close to $2 billion.

Mayank Rastogi, partner and leader for PE, EY said that Indian PE/VC market has significantly matured over time. Five to seven years ago, the classic growth capital was the only meaningful capital pool available with limitations such as investment horizon and return expectations, and could not have suited some specific situations.

There are a variety of capital pools available ranging from angel/VC to buyout funds, family offices, pensions and sovereigns, corporate funds, debt funds, sector-focused funds providing solutions that address specific needs. This is one of the key drivers for continuing buoyancy in the PE/VC investments in India despite slow growth capital investing.

Financial services ($1.6 billion across 11 deals) emerged as the most active sector on account of the Paytm-Softbank deal, the largest deal in the financial services sector till date. The real estate sector bagged four deals worth $709 million, followed by e-commerce sector’s six deals worth $211 million in terms of activity.

May 2017 recorded $1 billion in exits and was the second consecutive month with more than $1 billion in exits.

The strong buyout trend established over the past two years continued into 2017 with $2 billion invested across 18 deals till date.

Between January and May, there was a significant increase of over 60 per cent compared to 2016 and over 100 per cent compared to 2015, both, in terms of value and volume.

Debt deals recorded the biggest monthly volume since 2014 with $377 million recorded across 12 deals.

Given the buoyancy in the public markets, open market deals emerged as the preferred mode of exit, accounting for 36 per cent of exits by value and 50 per cent by volume, similar to the trend seen in the previous month.

Till date, open market exits have accounted for 49 per cent of the total value of exits in 2017 compared to 25 per cent for the whole of 2016. May 2017 recorded $90 million in fund raise, a decline of 82 per cent and 76 per cent as compared to May 2016 and April 2017 respectively. The plans for fund raise announced during the month stood at $908 million.

There was one PE-backed initial public offering (IPO) in May 2017 (S Chand, a publishing company, primarily in the education space), which saw Everstone exiting a 13.9 per cent stake for $48 million. Till May 2017, PE-backed IPO tally stands at four compared to eight during the same period in 2016.

Financial services emerged as the leading sector with exits worth $466 million across six deals followed by the healthcare sector with exits worth $260 million across three deals.

Under the new rules, the merger will also require prior approval of the Reserve Bank of India.

India will allow local companies to merge with overseas firms, easing rules to help home-grown businesses restructure their expanding global operations, and pave the deck for more listings of securities on capital markets abroad.

“Until now, only inbound mergers were permitted. With outbound mergers now permissible, there would be a lot of opportunities for Indian companies to acquire, restructure, or list on offshore exchanges as well,” said Mehul Shah, a partner at Khaitan and Co.

Until the federal notification by the corporate affairs ministry on April 13, India had permitted only inbound mergers. The merger would be in compliance with the Companies Act, 2013, and require prior approval of the Reserve Bank of India (RBI).

The notification also lists certain jurisdictions on the foreign companies, covering countries that comply with rules such as being members of the Financial Action Task Force (FATF) and whose central banks are members of the Bank for International Settlements (BIS).

Experts, however, believe that certain related laws must be amended before these rules take effect. “There would be need to have clarifications under tax laws. Exchange control regulations need to be re-looked and clarified to give effect to this notification. Also, an obligation is cast on RBI to provide approval for these mergers, as today, the RBI does not have mechanisms in place for this,” Shah added.

“Now exchange control regulations, securities laws, etc will need to be amended to facilitate a practical implementation of the amended law,” said Amit Maru, partner-transaction tax at EY.

The notification amends the Companies (Compromises, Arrangements and Amalgamations) Rules, 2016, notified in December 2016. Previously, mergers or demergers were governed by the Companies Act, 1956 before the notification of provisions of the Companies Act, 2013.

But, there were some gaps in the rules governing mergers. The latest notification seeks to fill these gaps. For instance, the law was earlier unclear on prior RBI approval even for inbound mergers, it is now clear that the nod is necessary.

“It might take some time for an Indian company to merge into a foreign company as it is not only one law but a host of laws which have to be amended before this becomes operational. For instance, income tax laws will have to be amended to give you a tax-neutral merger status because all mergers today are otherwise tax-neutral.” said Maru.The government had recently exempted firms, with Indian revenue of less than Rs 1,000 crore, from seeking the prior approval of the Competition Commission of India (CCI) while going in for a merger.