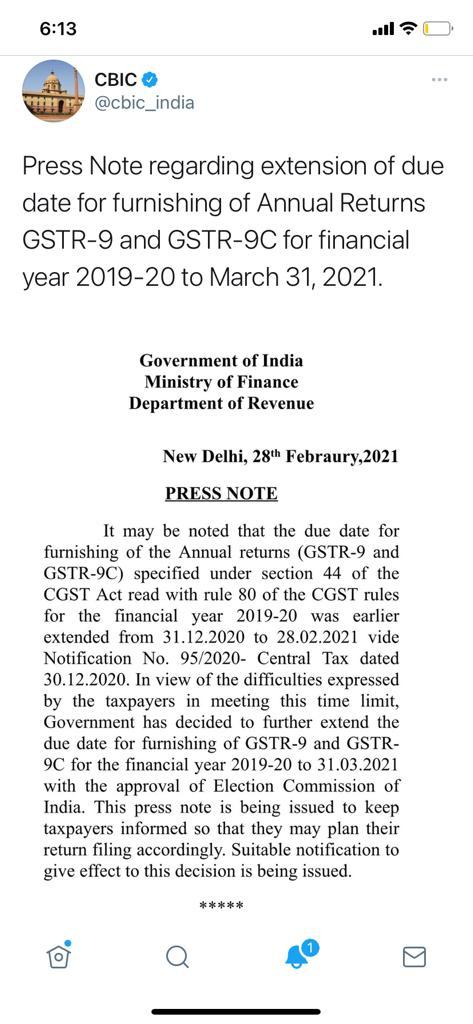

CBIC had extended, vide Press Note regarding extension of due date for furnishing of Annual Returns GSTR-9 and GSTR-9C for financial year 2019-20 to March 31, 2021.

This is the second extension given by the government. The deadline was earlier extended from December 31,2020 to February 28.

The year 2021 has come up with the various changes in Goods and Service Tax (GST) Rules which will have a direct impact on the business registered under the GST regime and the businessmen who are planning to get themselves registered under GST.

Firstly, the CBIC has revised the extent of provisional Input Tax Credit (ITC) claims from 10% to 5%, with effect from 1 January 2021.

Firstly, the CBIC has revised the extent of provisional Input Tax Credit (ITC) claims from 10% to 5%, with effect from 1 January 2021. As per the sub-rule (4) inserted in rule 36 of the Central Goods and Service Tax Rules, 2017, a taxpayer filing GSTR-3B can claim ITC only to the extent of 5% of the eligible credit available in GSTR-2A. The amount of eligible credit is arrived upon those invoices or debit notes, the details of which have been uploaded by the suppliers in the GSTR-2A only. The new percentage applies from 1 January 2021 onwards. The ITC claim was earlier restricted to 10% between 1 January 2020 and 31 December 2020 whereas it was 20% for the period from 9 October 2019 till 31 December 2019.

Secondly, the CBIC has amended the Rule 21, which is in respect of the suspension or cancellation of GST Registration. The amendment inserted the additional situation wherein the registration of a person can be suspended if he avails input tax credit in violation of the provisions of section 16 of the Act or the rules; or furnishes the details of outward supplies in FORM GSTR-1 for one or more tax periods which is in excess of the outward supplies declared by him in GSTR 3B for the said tax periods, or violates the provision of rule 86B.

Thirdly, the Board inserted Rule 86B wherein all the registered persons have to pay 1% cash liability so as to curb tax evasion by way of fake invoicing. The Rule 86B is applicable to only those registered persons whose value of taxable supply, other than exempt supply and export, in a month exceeds Rs 50 lakh that means those whose annual turnover is more than 6 crore.

For example, if a dealer has made a sale of Rs 1 crore of the goods whose tax rate is 12% and if he is discharging his tax liability more than 99% though ITC, then he has to pay only Rs.12,000 under this rule. On the other hand, a composition dealer would have paid Rs.1 lakh in cash with this volume of sale.

Fourthly, the CBIC has amended Rule 8 and 9 which pertained to New GST Registration, which provides for the biometric verification i.e. Aadhaar authentication and taking photographs or taking biometric information, photograph and verification of such other KYC documents for the applications for new registration.

However, in the case of those opting not to use Aadhaar, GST registration would be given only after physical verification of the business premise, which could take upto 21 days and in case a notice is issued, even more time.

Fifthly, the Board has amended Rule 59, not to permit the taxpayer to file GSTR 1 if the taxpayers have not furnished the return in FORM GSTR-3B for the preceding two months (for a taxpayer filing monthly returns); he has not furnished the return in FORM GSTR-3B for preceding tax period (for a taxpayer filing quarterly returns) and he is required to discharge the tax liability of at least 1% by cash (see the discussion on Rule 86B) and he has not furnished the return in FORM GSTR-3B for preceding tax period instead of two months.

Sixthly, the CBIC has amended Rule 138(10) which related to E-way Bill wherein the available travel time has been enhanced to 200 Kms. For example, goods dispatched to the destination located at a distance of 550 kms have taken place on February 1, 2021. As per the existing rule, the validity of the E-way bill generated would have expired on February 7, 2021, i.e. one day for 100km starting from the midnight of the generation of the E-way bill. However, as per the amendment, the e-way bill will expire on February 4, 2021, and hence the goods must reach the destination within the time frame.

To handle the menace of fake firms and circular trading entities, GST officials have cancelled 1,63,042 registrations in the month of October and November this year due to non-filing of GSTR-3B returns for more than six months

The Government has canceled the Goods and Service Tax (GST) registration of 163,000 business entities who have not filed monthly tax returns (GSTR-3B) for the last six months or more.

Furthermore, the department would persuade 25,000 taxpayers, who have not filed returns for October that was due by November 24, to comply with tax return deadlines.

“All these business entities, who had not filed their GSTR-3B returns for more than six months, were first issued the cancellation notices and then their registrations were cancelled as per standard operating procedure,” one of the officials said.

The Tax officers have been directed to follow up personally with these defaulting taxpayers so that their GSTR-3B returns due for the month are filed by November 30.

The push for better compliance comes on the heels of the tax department’s nationwide drive against fake invoice scams. It is suspected that fraudsters often register firms under GST but remain mostly dormant on compliance while using the status to claim invalid input tax credit (ITC).

As per the sources, in the Ahmedabad zone 11,048 GST registrations have been cancelled. In the Chennai zone, 19,586 suo motu cancellations have been done so far in respect of GST taxpayers who have failed to file returns for more than six months.

The officials said that the tax authority is also scanning newly registered entities that have not provided correct details at the time of registration.

Out of 720 deemed registrations granted between August 21 and November 16 this year, where Aadhaar authentication was not done, 55 deemed registrations have been identified for the discrepancy and the process of cancellation was initiated in these cases.

The government has cancelled Goods and Services Tax (GST) registration of over 163,000 business entities due to non-filing of tax returns for more than six months to curb the menace of fly-by-night operators who create bogus firms and fraudulently avail input tax credit (ITC) worth thousands of crores.

The Government has canceled the Goods and Service Tax (GST) registration of 163,000 business entities who have not filed monthly tax returns (GSTR-3B) for the last six months or more.

Furthermore, the department would persuade 25,000 taxpayers, who have not filed returns for October that was due by November 24, to comply with tax return deadlines.

“All these business entities, who had not filed their GSTR-3B returns for more than six months, were first issued the cancellation notices and then their registrations were cancelled as per standard operating procedure,” one of the officials said.

The Tax officers have been directed to follow up personally with these defaulting taxpayers so that their GSTR-3B returns due for the month are filed by November 30.

The push for better compliance comes on the heels of the tax department’s nationwide drive against fake invoice scams.

It is suspected that fraudsters often register firms under GST but remain mostly dormant on compliance while using the status to claim invalid input tax credit (ITC). As per the sources, in the Ahmedabad zone 11,048 GST registrations have been cancelled.

In the Chennai zone, 19,586 suo motu cancellations have been done so far in respect of GST taxpayers who have failed to file returns for more than six months.

The officials said that the tax authority is also scanning newly registered entities that have not provided correct details at the time of registration.

Out of 720 deemed registrations granted between August 21 and November 16 this year, where Aadhaar authentication was not done, 55 deemed registrations have been identified for the discrepancy and the process of cancellation was initiated in these cases.

Furthermore, the department would persuade 25,000 taxpayers, who have not filed returns for October that was due by November 24, to comply with tax return deadlines.

Taxpayers can make GST payments through challan every month either by self-assessment of monthly liability or 35 per cent of net cash liability of previous filed GSTR-3B of the quarter. Quarterly GSTR-1 and GSTR-3B can also be filed through an SMS.

The government has launched the Quarterly Return Filing and Monthly Payment of Taxes (QRMP) scheme in a bid to ease the return filing experience of the Goods and Services Tax (GST) taxpayers. The scheme will come into effect from January 1, 2021, it will impact 9.4 million taxpayers, who constitute 92% of the total tax base of GST and have an annual aggregate turnover (AATO) of up to Rs 5 crore.

With the introduction of the QRMP scheme, sources say, small taxpayers would need to file only eight returns – four each GSTR-3B and GSTR-1 – instead of the existing requirement of 16 returns in a financial year, of which 12 are GSTR-3B. The new scheme would also significantly reduce taxpayers’ professional expenses on return filing as they would have to file just half the number of returns as against the current requirement of 16. Also, the QRMP scheme would be available on the common GST portal with the facility to opt-in and opt-out, and opt-in again, as per a taxpayer’s wishes.

The scheme would bring in the concept of providing input tax credit (ITC) only on the reported invoices, thus putting a curb on the menace of fake invoice frauds. Additionally, the QRMP scheme is also likely to have the optional feature of Invoice Filing Facility (IFF) to mitigate the business-related hardships of the small and medium taxpayers. Under the IFF, taxpayers who opt to file their returns quarterly would be able to upload and file such invoices even in the first and second month of the quarter for which there is a demand from the recipients.

The taxpayers won’t need to upload and file all the invoices of the month. Only those invoices, which are required to be filed in IFF as per the recipients’ demands, are to be uploaded. The remaining invoices of the first and second months can be uploaded in the quarterly GSTR-1 return.

The QRMP scheme is based on the existing return system with suitable modifications in a bid to give much-needed flexibility to the small and medium enterprises with regards to GST compliance. It was approved in principle by the GST Council in its 42nd meeting on October 5, 2020.

In a statement, the Department of Revenue (DoR) reiterated that there will be no extra compliance burden on the taxpayers for GST turnover displayed in the Form 26AS, which is an annual consolidated tax statement that can be accessed from the income-tax website by taxpayers using their Permanent Account Number (PAN).

Prime Minister Narendra Modi launched GST into operation on the 1 st of July, 2017. GST was publicised as ‘one nation, one tax’ by the government, aimed to provide a simplified, single tax regime. GST is a dual levy where the Central Government levies and collects Central GST (CGST) and the State levies and collects State GST (SGST) on intra-state supply of goods or services. Centre also levies and collects Integrated GST (IGST) on inter-state supply of goods or services. The GST Portal is a website where all the compliance activities of GST can be done before and after GST login. Activities such as the GST registration return filing, payment of taxes, application for refund, etc. can be done on the GST Portal.

GSTN, recently launched many new features on GSTN portal. One of its features is that GSTN portal is now showing aggregate annual turnover for previous financial year after logging in to the portal.

The GST turnover is being shown in 26AS just for the information of the taxpayer. DoR acknowledged that there may be some differences in GSTR-3Bs filed and the GST shown in the Form 26AS but it can’t happen that a person shows turnover of crores of rupees in GST and doesn’t pay a single rupee of income tax.

The DoR said that the notified Income Tax Return for the current AY 2020-21 already requires reporting of GST outward supplies in the Schedule GST.

Therefore, the information displayed in Form 26AS would provide ease of compliance to the taxpayers in filling Schedule GST.

The revenue department has noticed that many unscrupulous persons are trying to avail or pass on input tax credit fraudulently by generating fake invoices and has already formulated a strategy for identifying these fake invoice generators which inter alia takes into account the income tax profiles of the suspected fake invoice generators.

These persons in most of the cases never file their income tax returns or disclose very meagre taxable income in the income tax return.

The suspected fake invoice generators are being identified for serious action under GST and other laws including suspension of their GST registration based on the fact that whether their income tax payment commensurate with the expected profit margin on turnover reported by them in the GST returns, the DoR said.

What “aggregate turnover” means?

“Aggregate turnover” is the aggregate value of all taxable supplies, exports of goods or/and services or both, exempt supplies and interstate supplies of persons having the same PAN, to be computed on all India basis. However, such taxable supplies do not include the value of inward supplies on which GST is being paid under reverse charge basis. The aggregate turnover also excludes Central tax, State tax, Union territory tax, Integrated tax and cess.

Basically, sum of the following shall be considered as an aggregate turnover:

Value of all taxable supplies of goods and services

Value of all Inter-state supplies

Value of all exempt supplies of goods and services

Value of all export of goods or services or both

However, the following items would be excluded from Turnover:

Inward supplies on which taxes are paid under reverse charge

Taxes and cesses under GST

Interstate supply of services

Transactions which are neither supply of goods or service.

Supplies provided outside India or received outside India

Extrapolation of Turnover at GSTIN level (for those who have not filed all the returns as per their eligibility or liability)

GSTIN-wise GSTR-3B turnover for FY 2019-2020 has been extrapolated by the formula: >> Total turnover declared as per all GSTR-3B filed / No. of GSTR-3B filed) X No. of GSTR-3B eligible or liable to be filed

GSTIN-wise CMP-08 outward supply has been extrapolated by the formula: >> Total outward supply declared as per all CMP-08 filed / No. of CMP-08 filed) X No. of CMP- 08 eligible or liable to be filed

Added both the values of S. No. (a) and S. No. (b).

For those taxpayers who have filed all the returns as per their respective eligibilities, value of S. No. (c) will be the actual turnover)

Aggregation of extrapolated turnover at PAN level or Annual Aggregate Turnover Resultant values as per S.No. (c) above are aggregated or rolled up at PAN level to arrive at the Annual Aggregate Turnover.

What is the relevance of knowing aggregate turnover?

The aggregate turnover is a crucial parameter for determining the following aspects:

Determining whether registration is required or not-

Aggregate Turnover is relevant for a person to determine threshold limit to obtain registration under GST.

Threshold turnover limit for exclusively supply of goods = Rs 40 lakh (Rs 20 lakh in case of supplies effected from special category states)

Threshold turnover limit for supply of Services or (goods and services both): Rs 20 lakh (Rs 10 lakh in case of supplies effected from special category states)

Determine the limit of composition levy – Threshold limit to opt for composition scheme: Rs 1.5 crore in a financial year (Rs 75 lakh in case of supplies effected from special category states).

To determine a “Taxable person” – Section 2 of CGST Act defines the “taxable person” as a person who has obtained registration or is liable to register as per section 22 and 24 of CGST Act. Here the Section 22 provides a liability to register when the tax payer’s turnover exceeds the limit as determined in certain cases. This is again based on aggregate turnover.

Calculation of Late fee –

Under section 33 any registered taxable person person who fails to file the return u/s 30 i.e Annual return shall be liable to pay late fees of Rs. 100 for every day when such failure continues subject to a maximum of an amount of 0.25% of his aggregate turnover.

This can escalate the amount of late fee because aggregate turnover will include all supplies except reverse charge.

To determine whether Audit is required –

Registered persons with an aggregate turnover exceeding the prescribed GST audit limit of Rs 2 Crore during a financial year are liable for GST Audit. The turnover limit of Rs 2 Crore is same for the registered tax persons across all States and UTs. Thus, no separate turnover limit is defined for Special Category States for GST Audit.

Therefore, it is advised to carry on the computation of aggregate turnover accurately as the same will be used at a number of places which will in turn determine the tax liability of a person.

The govt has given a suitable extension for annual compliance under GST laws as well as income tax laws due to disruptions caused by coronavirus.

The government on Saturday said due dates for filing income tax returns and tax audit reports for FY20 for various classes of tax payers have been extended to give more time for tax payers to comply.

The government also, on advice from the federal tax body, the Goods and Services Tax (GST) Council, extended the due date for filing annual return for FY19 from 31 October to 31 December, finance ministry said.

For filing income tax returns for FY20, individuals who are not required to conduct a tax audit report will now get time till 31 December. The original due date of 31 July was earlier extended to 30 November.

Tax payers who are required to file their tax audit reports—professionals with gross receipts more than ₹50 lakh and those running businesses with sales up to ₹1 crore—have also got extra time. They can now file their tax returns by 31 January. The earlier deadline, after one extension, was 30 November.

Assessees who enter into international transactions or specified domestic transactions and are required to file tax audit reports, have also been given extra time to file their FY20 tax returns. As per Saturday’s announcement, they can file their tax returns for FY20 by end of January.

“Consequently, the date for furnishing of various audit reports under the Income Tax Act including tax audit report and report in respect of international or specified domestic transaction has also been extended to 31 December, 2020,” said the finance ministry statement.

The ministry also gave extra time for small tax payers to pay their self- assessment tax. This facility is available only to those with self-assessment tax liability up to ₹1 lakh. Accordingly, those who are liable to get tax audit done, can pay self assessment tax by end of January and others can pay by end of December. Finance ministry said it will notify these changes.

The government also said it has been receiving requests for more time to file GST annual return and the reconciliation statement for FY19. Accordingly the due date for the same has been extended from 31 October to 31 December, said the ministry.

Filing annual return (form GSTR-9/GSTR-9A) for FY19 is optional for taxpayers who had sales below ₹2 crore. Filing of reconciliation statement in form 9C is optional for the taxpayers with sales up to ₹5 crore, said the ministry.

CBIC had extended, vide Press Note regarding extension of due date for furnishing of Annual Returns GSTR-9 and GSTR-9C for financial year 2019-20 to March 31, 2021.

CBIC had extended, vide Press Note regarding extension of due date for furnishing of Annual Returns GSTR-9 and GSTR-9C for financial year 2019-20 to March 31, 2021.