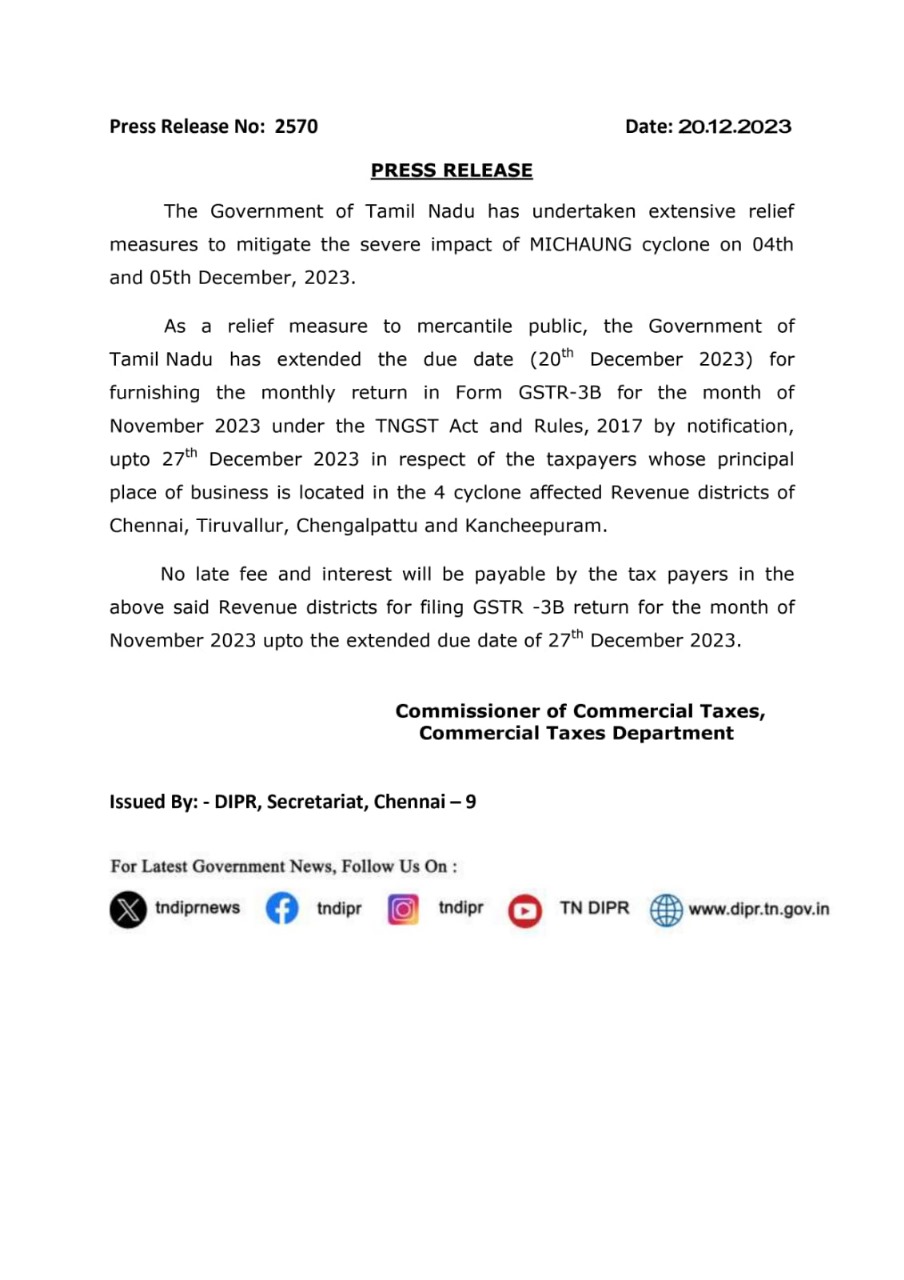

In response to the devastation caused by the MICHAUNG cyclone in early December 2023, the deadline for monthly GST returns has been extended, in respect of the taxpayers whose principal place of business is located in the four cyclone-affected districts of Chennai, Tiruvallur, Chengalpattu and Kancheepuram, as per release from Commercial Taxes Department.

The CBIC vide Notification No. 55/2023 – Central Tax dated December 20, 2023, extends the deadline for filing FORM GSTR-3B for November 2023 until December 27, 2023.

This extension applies to registered individuals with their principal place of business in specific districts of Tamil Nadu (Chennai, Tiruvallur, Chengalpattu, Kancheepuram), as recommended by the Council under section 39(1) and rule 61(1)(i) of the Central Goods and Services Tax Rules, 2017 (“the CGST Rules”).

GST collection in October crosses ₹1.3 lakh crore, second highest ever

The gross GST revenue collected in the month of October 2021 exceeded ₹1.3 lakh crore. The GST revenues for October is the second highest ever since introduction of GST, second only to that in April 2021, which related to year-end revenues. The revenues for the month of October 2021 are 24% higher than the GST revenues in the same month last year.

The gross GST revenue collected in the month of October 2021 exceeded ₹1.3 lakh crore. The GST revenues for October is the second highest ever since introduction of GST, second only to that in April 2021, which related to year-end revenues. The revenues for the month of October 2021 are 24% higher than the GST revenues in the same month last year.

“This is very much in line with the trend in economic recovery. This is also evident from the trend in the e-way bills generated every month since the second wave. The revenues would have still been higher if the sales of cars and other products had not been affected on account of disruption in supply of semi-conductors,” the government said in a statement.

The government settled ₹27,310 crore to CGST and ₹22,394 crore to SGST from IGST as regular settlement. The total revenue of Centre and the States after regular settlements in the month of October 2021 is ₹51,171 crore for CGST and ₹52,815 crore for the SGST.

During the month, revenues from import of goods was 39% higher and the revenues from domestic transaction (including import of services) are 19% higher than the revenues from these sources during the same month last year.

Indian stock market benchmark Sensex was up over 600 points in noon trade. A private survey released earlier in the day showed India’s manufacturing sector activities gained further strength in October as companies scaled up production and stepped up input purchasing in anticipation of further improvements in demand.

The seasonally adjusted IHS Markit India Manufacturing Purchasing Managers’ Index (PMI) rose from 53.7 in September to 55.9 in October, pointing to the strongest improvement in overall operating conditions since February.

Robust gains in new work aided production growth in October as output and new orders expanded at fastest rates in seven months, while business optimism hit a six-month high, the survey said.

The Ministry of Corporate Affairs (MCA), considering requests to waive additional fee for late filing of statutory forms which fall due between 1 April and end of May owing to the COVID-19 restrictions and disruption, has granted extra time without additional fee for filing statutory forms till the end of July, 2021

The ministry of corporate affairs (MCA) has offered relaxation in certain compliance requirements for businesses, including a longer interval between two board meetings in view of the hardships during the second wave of the pandemic.

Companies are normally required to hold a minimum of four board meetings in a year with the interval between them not exceeding 120 days. This has now been relaxed by 60 days so that the interval could go up to 180 days, the ministry said in a notification issued on Monday.

The ministry also said in a separate notification that it has received several requests to waive the additional fee for late filing of statutory forms which fall due between 1 April and end of May in view of the covid-19 restrictions and disruption.

The ministry said these requests have been examined and taking into account the difficulties due to resurgence of coronavirus infections, extra time without additional fee has been granted till the end of July for filing statutory forms. In the case of filing forms to report creation or modification of a charge (lien or claim) on the assets of a company under various circumstances, the ministry has issued another notification granting relief. Accordingly, in cases where due date had expired before 1 April, extra time has been granted till end of May.

The finance ministry has already given relief for various compliance requirements related to income tax and goods and services tax (GST), besides exempting basic customs duty and agriculture cess on various medical supplies used in the prevention and treatment of coronavirus disease. The pandemic has taken a heavy toll on lives with over 222,000 deaths.

The central government has not favoured a lockdown of the country during the second wave, but several states had to impose curbs on movement and assembly of people to break the chain of infections. India has so far vaccinated over 15 crore people, or roughly 12% of the population. The second wave is expected to slow India’s economic recovery from an expected 7.7% contraction in FY21.

The GST revenues during April 2021 are the highest since the introduction of GST even surpassing collections in the last month

The gross GST revenue collected in the month of April is at a record high of Rs. 1,41,384 crore of which CGST is Rs. 27,837 crore, SGST is Rs. 35,621, IGST is ₹68,481 crore (including Rs. 29,599 crore collected on import of goods) and Cess is Rs. 9,445 crore (including Rs. 981 crore collected on import of goods).

“Despite the second wave of COVID-19 pandemic affecting several parts of the country, Indian businesses have once again shown remarkable resilience by not only complying with the return filing requirements but also paying their GST dues in a timely manner during the month,” according to a statement by Ministry of Finance.

The GST revenues during April 2021 are the highest since the introduction of GST even surpassing collections in the last month (March’2021). In line with the trend of recovery in the GST revenues over past six months, the revenues for the month of April 2021 are 14% higher than the GST revenues in the last month of March’2021.

During the month, the revenues from domestic transaction (including import of services) are 21% higher than the revenues from these sources during the last month.

GST revenues have not only crossed the Rs. 1 lakh crore mark during successively for the last seven months but have also shown a steady increase. These are clear indicators of sustained economic recovery during this period.

Closer monitoring against fake-billing, deep data analytics using data from multiple sources including GST, Income-tax and Customs IT systems and effective tax administration have also contributed to the steady increase in tax revenue. Quarterly return and monthly payment scheme has been successfully implemented bringing relief to the small taxpayers as they now file only one return every three months.

Providing IT support to taxpayers in the form of pre-filled GSTR 2A and 3B returns and ramped up System capacity have also eased the return filing process.

During this month the government has settled Rs. 29,185 crore to CGST and Rs. 22,756 crore to SGST from IGST as regular settlement.

The total revenue of Centre and the States after regular and ad-hoc settlements in the month of April’ 2021 is Rs. 57,022 crore for CGST and Rs. 58,377 crore for the SGST.

The government has cancelled Goods and Services Tax (GST) registration of over 163,000 business entities due to non-filing of tax returns for more than six months to curb the menace of fly-by-night operators who create bogus firms and fraudulently avail input tax credit (ITC) worth thousands of crores.

The Government has canceled the Goods and Service Tax (GST) registration of 163,000 business entities who have not filed monthly tax returns (GSTR-3B) for the last six months or more.

Furthermore, the department would persuade 25,000 taxpayers, who have not filed returns for October that was due by November 24, to comply with tax return deadlines.

“All these business entities, who had not filed their GSTR-3B returns for more than six months, were first issued the cancellation notices and then their registrations were cancelled as per standard operating procedure,” one of the officials said.

The Tax officers have been directed to follow up personally with these defaulting taxpayers so that their GSTR-3B returns due for the month are filed by November 30.

The push for better compliance comes on the heels of the tax department’s nationwide drive against fake invoice scams.

It is suspected that fraudsters often register firms under GST but remain mostly dormant on compliance while using the status to claim invalid input tax credit (ITC). As per the sources, in the Ahmedabad zone 11,048 GST registrations have been cancelled.

In the Chennai zone, 19,586 suo motu cancellations have been done so far in respect of GST taxpayers who have failed to file returns for more than six months.

The officials said that the tax authority is also scanning newly registered entities that have not provided correct details at the time of registration.

Out of 720 deemed registrations granted between August 21 and November 16 this year, where Aadhaar authentication was not done, 55 deemed registrations have been identified for the discrepancy and the process of cancellation was initiated in these cases.

Furthermore, the department would persuade 25,000 taxpayers, who have not filed returns for October that was due by November 24, to comply with tax return deadlines.

Taxpayers can make GST payments through challan every month either by self-assessment of monthly liability or 35 per cent of net cash liability of previous filed GSTR-3B of the quarter. Quarterly GSTR-1 and GSTR-3B can also be filed through an SMS.

The government has launched the Quarterly Return Filing and Monthly Payment of Taxes (QRMP) scheme in a bid to ease the return filing experience of the Goods and Services Tax (GST) taxpayers. The scheme will come into effect from January 1, 2021, it will impact 9.4 million taxpayers, who constitute 92% of the total tax base of GST and have an annual aggregate turnover (AATO) of up to Rs 5 crore.

With the introduction of the QRMP scheme, sources say, small taxpayers would need to file only eight returns – four each GSTR-3B and GSTR-1 – instead of the existing requirement of 16 returns in a financial year, of which 12 are GSTR-3B. The new scheme would also significantly reduce taxpayers’ professional expenses on return filing as they would have to file just half the number of returns as against the current requirement of 16. Also, the QRMP scheme would be available on the common GST portal with the facility to opt-in and opt-out, and opt-in again, as per a taxpayer’s wishes.

The scheme would bring in the concept of providing input tax credit (ITC) only on the reported invoices, thus putting a curb on the menace of fake invoice frauds. Additionally, the QRMP scheme is also likely to have the optional feature of Invoice Filing Facility (IFF) to mitigate the business-related hardships of the small and medium taxpayers. Under the IFF, taxpayers who opt to file their returns quarterly would be able to upload and file such invoices even in the first and second month of the quarter for which there is a demand from the recipients.

The taxpayers won’t need to upload and file all the invoices of the month. Only those invoices, which are required to be filed in IFF as per the recipients’ demands, are to be uploaded. The remaining invoices of the first and second months can be uploaded in the quarterly GSTR-1 return.

The QRMP scheme is based on the existing return system with suitable modifications in a bid to give much-needed flexibility to the small and medium enterprises with regards to GST compliance. It was approved in principle by the GST Council in its 42nd meeting on October 5, 2020.

In a statement, the Department of Revenue (DoR) reiterated that there will be no extra compliance burden on the taxpayers for GST turnover displayed in the Form 26AS, which is an annual consolidated tax statement that can be accessed from the income-tax website by taxpayers using their Permanent Account Number (PAN).

Prime Minister Narendra Modi launched GST into operation on the 1 st of July, 2017. GST was publicised as ‘one nation, one tax’ by the government, aimed to provide a simplified, single tax regime. GST is a dual levy where the Central Government levies and collects Central GST (CGST) and the State levies and collects State GST (SGST) on intra-state supply of goods or services. Centre also levies and collects Integrated GST (IGST) on inter-state supply of goods or services. The GST Portal is a website where all the compliance activities of GST can be done before and after GST login. Activities such as the GST registration return filing, payment of taxes, application for refund, etc. can be done on the GST Portal.

GSTN, recently launched many new features on GSTN portal. One of its features is that GSTN portal is now showing aggregate annual turnover for previous financial year after logging in to the portal.

The GST turnover is being shown in 26AS just for the information of the taxpayer. DoR acknowledged that there may be some differences in GSTR-3Bs filed and the GST shown in the Form 26AS but it can’t happen that a person shows turnover of crores of rupees in GST and doesn’t pay a single rupee of income tax.

The DoR said that the notified Income Tax Return for the current AY 2020-21 already requires reporting of GST outward supplies in the Schedule GST.

Therefore, the information displayed in Form 26AS would provide ease of compliance to the taxpayers in filling Schedule GST.

The revenue department has noticed that many unscrupulous persons are trying to avail or pass on input tax credit fraudulently by generating fake invoices and has already formulated a strategy for identifying these fake invoice generators which inter alia takes into account the income tax profiles of the suspected fake invoice generators.

These persons in most of the cases never file their income tax returns or disclose very meagre taxable income in the income tax return.

The suspected fake invoice generators are being identified for serious action under GST and other laws including suspension of their GST registration based on the fact that whether their income tax payment commensurate with the expected profit margin on turnover reported by them in the GST returns, the DoR said.

What “aggregate turnover” means?

“Aggregate turnover” is the aggregate value of all taxable supplies, exports of goods or/and services or both, exempt supplies and interstate supplies of persons having the same PAN, to be computed on all India basis. However, such taxable supplies do not include the value of inward supplies on which GST is being paid under reverse charge basis. The aggregate turnover also excludes Central tax, State tax, Union territory tax, Integrated tax and cess.

Basically, sum of the following shall be considered as an aggregate turnover:

Value of all taxable supplies of goods and services

Value of all Inter-state supplies

Value of all exempt supplies of goods and services

Value of all export of goods or services or both

However, the following items would be excluded from Turnover:

Inward supplies on which taxes are paid under reverse charge

Taxes and cesses under GST

Interstate supply of services

Transactions which are neither supply of goods or service.

Supplies provided outside India or received outside India

Extrapolation of Turnover at GSTIN level (for those who have not filed all the returns as per their eligibility or liability)

GSTIN-wise GSTR-3B turnover for FY 2019-2020 has been extrapolated by the formula: >> Total turnover declared as per all GSTR-3B filed / No. of GSTR-3B filed) X No. of GSTR-3B eligible or liable to be filed

GSTIN-wise CMP-08 outward supply has been extrapolated by the formula: >> Total outward supply declared as per all CMP-08 filed / No. of CMP-08 filed) X No. of CMP- 08 eligible or liable to be filed

Added both the values of S. No. (a) and S. No. (b).

For those taxpayers who have filed all the returns as per their respective eligibilities, value of S. No. (c) will be the actual turnover)

Aggregation of extrapolated turnover at PAN level or Annual Aggregate Turnover Resultant values as per S.No. (c) above are aggregated or rolled up at PAN level to arrive at the Annual Aggregate Turnover.

What is the relevance of knowing aggregate turnover?

The aggregate turnover is a crucial parameter for determining the following aspects:

Determining whether registration is required or not-

Aggregate Turnover is relevant for a person to determine threshold limit to obtain registration under GST.

Threshold turnover limit for exclusively supply of goods = Rs 40 lakh (Rs 20 lakh in case of supplies effected from special category states)

Threshold turnover limit for supply of Services or (goods and services both): Rs 20 lakh (Rs 10 lakh in case of supplies effected from special category states)

Determine the limit of composition levy – Threshold limit to opt for composition scheme: Rs 1.5 crore in a financial year (Rs 75 lakh in case of supplies effected from special category states).

To determine a “Taxable person” – Section 2 of CGST Act defines the “taxable person” as a person who has obtained registration or is liable to register as per section 22 and 24 of CGST Act. Here the Section 22 provides a liability to register when the tax payer’s turnover exceeds the limit as determined in certain cases. This is again based on aggregate turnover.

Calculation of Late fee –

Under section 33 any registered taxable person person who fails to file the return u/s 30 i.e Annual return shall be liable to pay late fees of Rs. 100 for every day when such failure continues subject to a maximum of an amount of 0.25% of his aggregate turnover.

This can escalate the amount of late fee because aggregate turnover will include all supplies except reverse charge.

To determine whether Audit is required –

Registered persons with an aggregate turnover exceeding the prescribed GST audit limit of Rs 2 Crore during a financial year are liable for GST Audit. The turnover limit of Rs 2 Crore is same for the registered tax persons across all States and UTs. Thus, no separate turnover limit is defined for Special Category States for GST Audit.

Therefore, it is advised to carry on the computation of aggregate turnover accurately as the same will be used at a number of places which will in turn determine the tax liability of a person.

In response to the devastation caused by the MICHAUNG cyclone in early December 2023, the deadline for monthly GST returns has been extended, in respect of the taxpayers whose principal place of business is located in the four cyclone-affected districts of Chennai, Tiruvallur, Chengalpattu and Kancheepuram, as per release from Commercial Taxes Department.

In response to the devastation caused by the MICHAUNG cyclone in early December 2023, the deadline for monthly GST returns has been extended, in respect of the taxpayers whose principal place of business is located in the four cyclone-affected districts of Chennai, Tiruvallur, Chengalpattu and Kancheepuram, as per release from Commercial Taxes Department.