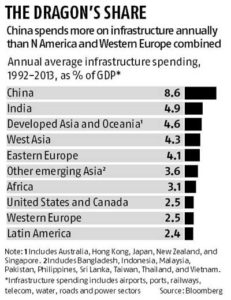

Despite a crying need for better infrastructure, investment in it has actually fallen in 10 major economies since the financial crisis, including the US, according to a new study by the McKinsey Global Institute. Meanwhile, China is still going gangbusters on roads, bridges, sewers, and everything else that makes a country run.

“China spends more on economic infrastructure annually than North America and Western Europe combined,” according to the report published Wednesday.

Economists around the world have been arguing that now is a great time to invest in infrastructure because interest rates are super-low and the global economy could use the spending jolt. “Is anyone proud of Kennedy airport?” Harvard University economist Lawrence Summers likes to ask.

The MGI report cites 10 countries where infrastructure spending fell as a share of gross domestic product from 2008 to 2013: the US, UK, Italy, Australia, South Korea, Brazil, India, Russia, Mexico, and Saudi Arabia. The study counts 11 economies, but that’s because it lists the European Union as a separate entity.

In contrast to the widespread declines, the institute says, infrastructure spending grew as a share of GDP in Japan, Germany, France, Canada, Turkey, South Africa and China. The chart from the MGI report shows China’s strength in infrastructure spending. Its bar is the highest. There’s such a thing as too much infrastructure spending, of course. At current rates of investment, China, Japan, and Australia are likely to exceed their needs between now and 2030, the McKinsey & Co-affiliated think tank says. To fund more public infrastructure, the report favours raising user charges such as highway tolls, among other measures.

To encourage more private investment in infrastructure, MGI argues for increasing “regulatory certainty” and giving investors “the ability to charge prices that produce an acceptable risk-adjusted return.”

India has jumped 13 positions from last year to rank second among 30 developing countries this year on ease of doing business, according to a study topped by China.

According to 2016 Global Retail Development Index (GRDI), which ranks top 30 developing countries for retail investment worldwide, a pick-up in GDP growth and better clarity regarding FDI regulations have helped India achieve a second ranking.

Debashish Mukherjee, a partner with A T Kearney and co-head of the Consumer Industries & Retail Products Practice for India and Southeast Asia, said,

India’s strong ranking reflects foreigner retailers increased optimism in its retail market and its vast growth potential. India has relaxed several key Foreign Direct Investment (FDI) regulations in single-brand retail and this has paved the way for multinational firms to enter the market, Mukherjee said.

India’s retail sector has expanded at a compound annual growth rate of 8.8 percent between 2013 and 2015, with annual sales crossing the $1 trillion mark, according to A T Kearney, a London-based business consultancy.

India has also become the world’s fastest growing economy. That, coupled with a large population base and the easing of FDI regulations in the sector, has made it an even more attractive market, it said in the ranking.

We expect to see e-commerce to propel India’s growth and make it a more attractive proposition. However, there are some challenges as well. India remains a challenging and complex market for foreign retailers, where understanding dynamics at the state level is important. Infrastructure bottlenecks including labour laws, complex regulations, high labour attrition rates, and limited high-quality retail space remain areas of concerns for retailers, Mukherjee said.

The country’s retail sector has also benefited from the rapid growth in e-commerce. India is the world’s second largest Internet market and the increasing Internet and smartphone penetration is contributing to the expansion of e-commerce.

As Indian consumers become more comfortable with shopping online, venture capital and private equity firms have boosted investment in the sector, providing further momentum, the report said.

TOKYO: Japanese conglomerate SoftBank and a number of investors here have shown keen interest in investing in India’s “infrastructure growth story”, Finance Minister Arun Jaitley said today as he kicked off his 6-day visit to Japan aimed at attracting investments from Asia’s second biggest economy.

After a meeting with Jaitley, SoftBank Group CEO Masayoshi Son said he is also interested in Internet companies as well as solar energy sector, where he has already announced $20 billion investment through a joint venture.

“There are people who want to participate in infrastructure growth story. For example, at the SoftBank meeting we just had, they are looking at one of the biggest investments in solar power already,” Jaitley said after meeting Son.

“There are people who want to participate in infrastructure growth story. For example, at the SoftBank meeting we just had, they are looking at one of the biggest investments in solar power already,” Jaitley said after meeting Son.

In June last year, SoftBank announced that the group was forming a joint venture with Bharti Enterprises and Taiwan’s Foxconn Technology Group to invest about $20 billion in renewable energy in India. The JV would aim to generate 20 gigawatts of electricity.

“They have made considerable headway and have identified location. It will probably be one of the largest investment in those areas,” Jaitley said.

The Japanese telecom and Internet giant has made a string of tech investments in India, amounting to $2 billion in the past two year. SoftBank is looking at accelerating the pace of investments in the future.

“India has a great future… We are interested in investing for Internet companies, also for solar energy. We would make a strong commitment,” Son said.

He had previously said that India’s market is poised for massive growth, making it an important destination for investors.

SoftBank’s investments in the past two years include $627 million in online-retailing marketplace Snapdeal and leading a $210 million funding round in taxi-hailing app Ola Cabs.

It paid $200 million for a 35 per cent stake in InMobi, an Indian mobile-advertising network, starting in 2011.

SoftBank also has a JV with Bharti Group, Bharti SoftBank, the investments of which include the mobile application Hike Messenger. Its other investments include real-estate website Housing.com, hotel-booking app Oyo Rooms and Grofers.

Son had previously predicted that India’s e-commerce industry would become a $500 billion business in the next 10 years.

SoftBank, which owns one of Japan’s biggest mobile carriers and a controlling stake in US-based Sprint Corp, has been moving quickly to expand its Internet and media holdings.

As the largest shareholder in Alibaba Group Holding Ltd, the Chinese e-commerce company, SoftBank has ample resources to deploy for acquisitions.

Renewable energy projects have received Rs 86,000 crore investment, most of it from private sector, in the last three years with Madhya Pradesh at top garnering Rs 14,313.80 crore.

“Most of the investment in renewable energy came from private sector. Total estimated investment in renewable energy power projects during the last three years is around Rs 86,000 crore,” New and Renewable Energy Minister Piyush Goyal said in a written reply to Lok Sabha today.

According to the statement, around 15,400 million units has been generated through solar power projects during the last three years.

Madhya Pradesh remained at the top, recording maximum investment in clean energy projects at Rs 14,313.80. It was followed by Maharashtra at Rs 13,743.01 crore, Rajasthan at Rs 11,632.96 crore, Karnataka at Rs 9,586.31 crore, Andhra Pradesh at Rs 9,539.12 crore, Tamil Nadu at Rs 8,961.28 crore and Gujarat at Rs 6,646.35 crore.

The minister also stated that Pondicherry, Laskhwadeep, Dadar & Nagar Haveli, Sikkim, Manipur, Meghalaya and Goa received no investment at all for renewable energy projects in last three years.

According to a separate reply to the House, as on March 31, 2016, a cumulative capacity of 42.76 GW has been installed from various renewable energy sources, which include 26.78 GW from Wind, 6.76 GW from solar, 4.27 from small hydro power and 4.95 GW from bio power.

In another reply to the House, the Maharashtra will require the maximum solar power generation capacity of 13,270 MW by 2021-22 as per tentative renewable purchase obligation (RPO) requirement estimated by the ministry.

The ministry has estimated 1,02,021 MW solar power generation capacity to be installed in the entire country by 2021-22.

After Maharashtra, Uttar Pradesh’s solar power generation capacity by 2021-22 as per RPO requirement would be the second highest at 12,124 MW followed by Gujarat at 9,796 MW, Tamil Nadu at 9,398 MW and Rajasthan 6,953 MW.

Under RPO, states are mandated by power regulators to have certain proportion of renewable energy capacity in their total power mix to promote clean and green sources like solar and wind.

The minister in another reply to the House stated that the new pithead thermal power plants have the lowest tariff of Rs 3.75 per unit in the first year of operation compared Rs 4.5 per unit for solar, Rs 4.6 for hydro, Rs 4.94 for atomic power and Rs 5.49 for non-pithed thermal plants.

However, the levellised tariff for hydro power plants is the lowest at Rs 4 per units compared Rs 4.5 for solar, Rs 5 for atomic power, Rs 4.57 for pithead based thermal power and Rs 7.57 per unit for non-pithead based thermal power plant.

France will help India develop Chandigarh, Nagpur and Puducherry as smart cities. Agence Française de Developpement (French Development Agency) signed memoranda of understanding with the government of Union territory of Chandigarh, and government of Union territory of Puducherry and the Maharashtra government here on Sunday in the presence of French President Francois Hollande and Prime Minister Narendra Modi.

Chandigarh, designed by the French architect Le Corbusier half a century ago as a model city, is spread across 114 sq km and the urban infrastructure and green belt of the city provide it a distinguished status among India’s planned cities.

On January 26, Modi is set to announce the official list of 20 smart cities to be developed in the first phase.

A delegation of 26 CEOs from France travelled to Chandigarh with Hollande and had discussions on CEO forums to explore partnerships in renewable energy, defence, information technology and aerospace.

Modi said French companies can exploit India’s trained and affordable manpower to expand their manufacturing operations in the country. The French president committed annual investment to the tune of €1 billion to strengthen business relations with India.

An agreement between Airbus and Mahindra was also inked under Indo-French cooperation to manufacture helicopters within the Make in India initiative.

French companies will also collaborate with public sector firm Engineering Projects India to provide integrated railways solutions. The railway stations of Ambala and Ludhiana will also be redeveloped with French partnership.

The French delegation evinced interest in the areas of renewable energy, infrastructure, transport, defence, and water treatment.

The possibility of their investing, either directly in projects or through the National Investment and Infrastructure Fund (NIIF) that we have created, were both discussed,” he told reporters at the Indian High Commission in London.

Amid fears of the global economy edging close to recession, India and UK have agreed to open up trade and markets to support growth, carry out structural reforms and address issues related to cross-border tax evasion.

After talks between India’s Finance Minister Arun Jaitley and UK Chancellor of the Exchequer George Osborne, the two nation’s agreed to boost economic ties particularly in areas of infrastructure and financial services and renewed pledge for autonomical exchange of tax information from 2017.

“From the Indian point of view, we were extremely interested in having the British investors look at infrastructure investments in India for which various possibilities were discussed,” Jaitley said after the talks.

India, he said, is “extremely keen that large British companies, particularly involved in infrastructure financing, start investing in Indian infrastructure”.

The two nations will work together for developing an India-UK partnership fund under the umbrella of National Investment and Infrastructure Fund (NIIF) recently created in India.

“This fund will seek to increase flows of private sector capital and expertise alongside multilateral support into Indian infrastructure,” a joint statement issued after talks said.

The world’s fifth largest economy will work on development of smart cities in India. New Delhi is also looking at London for issuance of rupee-denominated bonds to get UK investors to fund its infrastructure projects.

“The possibility of their investing, either directly in projects or through the National Investment and Infrastructure Fund (NIIF) that we have created, were both discussed,” Jaitely told reporters at the Indian High Commission here.

With the IMF warning of global economy being close to recession with 3.4 per cent growth this year, the two sides said they “remain concerned that global growth is falling short of expectations and that the risks to the global outlook have increased”.

“In this regard we stand ready to take the necessary steps to open up trade and markets to support growth and jobs, and agree on the importance of structural reforms and pursuing credible fiscal policies,” the joint statement said.

The joint statement talked about advancement of cooperation in a range of sectors including infrastructure financing, addressing issues of cross-border tax evasion/ avoidance besides opening up of the Indian legal sector to foreign lawyers.

“The UK and India share a common commitment to address cross-border tax evasion and avoidance. Both sides have committed to the Common Reporting Standards (CRS) on Automatic Exchange of Tax Information and will begin exchange in 2017,” the statement said.

“We call on other countries to meet the commitments they have made and to implement the new standard on time,” it said.

During the talks, which included senior representatives from Finance Ministries, Central Banks and key regulators of both countries, the two leaders discussed ways to strengthen the Indo-UK existing economic partnership in order to further boost trade and investment, and to build on the success of Prime Minister, Narendra Modi’s recent summit with his British counterpart David Cameron in the UK.

“Given the fact that even in a somewhat difficult global scenario, India is managing a reasonable growth rate, this is one of the better options that investors have and that kind of a sentiment gets really echoed in the meetings with the investors that we had. Of course, the investors are also keenly watching which way our reform process in India goes,” Jaitley said.

The two nations agreed to work together on building commercial and regualtor-to-regulator links that can underpin further fintech growth in both countries.

“The UK and India agreed to renew the existing mandate of the India-UK Financial Partnership, and building on the re-establishment of the CEO Forum,” the statement said, adding that potential areas of interest for the India-UK Financial Partnership could be reinsurance, international use of the rupee, role of financial technology, financial inclusion, investor protection and green finance.

“The global economy is facing serious challenges and therefore the estimates of global growth also have been repeatedly lowered. Compared to how various countries across the world have been doing, India’s growth rate despite these challenges is probably the highest in the world among major economies,” Jaitley said, in reference to his meetings with investors at Goldman Sachs and London Stock Exchange.

As a follow up on Prime Minister Modi’s announcement during his UK visit last November on the listing of Rupee bonds in London, the minister said, “the UK is very keen for these to be listed in London and broadly the economic and financial dialogue was carried further”.

During the dialogue, the two sides recognised that as the leading financial centre in the world and in the view of successful issuance of Masala bonds issued by the International Finance Cooperation last year, London will be an attractive location for issuance of rupee-denominated bonds.

“The bonds, which were first announced during the visit of Prime Minister Modi to the UK in November, illustrate the crucial role that the UK’s capital markets can play in an enhanced economic relations relationship with India, with UK investors providing financing for the transformation of India’s infrastructure and continued rapid economic growth,” the statement said.

India and the UK also agreed that the development of deeper markets in rupee-linked products, and the increasingly sophisticated relationship between the Indian and UK financial sectors, are important underlying factors in fostering an enduring economic and financial partnership.

Both sides agreed to continue working closely on the development of smart cities in India.

“We will continue to build on and further embed the existing Technical Assistance Partnerships that were announced during Prime Minister Modi’s recent visit to the UK, and to continue working together on research collaboration and other measures to support India’s 100 Smart Cities programme,” the statement said.

While noting the strength of the economic outlook for both countries, the two sides expressed concern that global growth is falling short of expectations and that the risks to the global outlook have increased.

“In this regard we stand ready to take the necessary steps to open up trade and markets to support growth and jobs, and agree on the importance of structural reforms and pursuing credible fiscal policies in order to raise living standards,” it said.

India and the UK also agreed to work together with the aim of developing an Indo-UK partnership fund under the umbrella of the NIIF. The fund will seek to increase flows of private sector capital and expertise alongside multilateral support into Indian infrastructure.

The working group to be established will report back within the course of 2016 on a proposed fund strategy and delivery approach, the statement said.

“As part of this, India and the UK also both recognise the importance of identifying the sector or sectors where there is greatest potential for developing sustainable project pipelines, and of developing a supportive institutional environment for investment and delivery,” it said.

The smart cities planned by the government will use nearly 1.6 billion of connected things or Internet of Things (IoT) by 2016, an increase of 39% from 2015, Gartner said in a report.

IoT is the network of physical objects or “things” embedded with electronics, software, sensors, and network connectivity, which enables these objects to collect and exchange data.

“Smart commercial buildings will be the highest user of IoT until 2017, after which smart homes will take the lead with just over 1 billion connected things in 2018,” said Gartner’s Research vice president Bettina Tratz-Ryan.

Commercial real estate benefits greatly from IoT implementation as it creates a unified view of facilities management as well as advanced service operations through the collection of data and insights from a multitude of sensors.

“Especially in large sites, such as industrial zones, office parks, shopping malls, airports or seaports, IoT can help reduce the cost of energy, spatial management and building maintenance by up to 30%,” Tratz-Ryan said.

The business applications that are fuelling the growth of IoT in commercial buildings are handled through building information management systems that drive operations management, especially around energy efficiency and user-centric service environments, Gartner said.

“In 2016, commercial security cameras and webcams as well as indoor LEDs will drive total growth, representing 24% of the IoT market for smart cities,” she said.

Tratz-Ryan further said IoT deployment in commercial buildings will continue to grow at a rapid pace over the next few years, and is on pace to reach just over 1 billion in 2018.

“Incentives into the deployment of IoT in commercial real estate will fuel its development,” she added.

Despite a crying need for better infrastructure, investment in it has actually fallen in 10 major economies since the financial crisis, including the US, according to a new study by the McKinsey Global Institute. Meanwhile, China is still going gangbusters on roads, bridges, sewers, and everything else that makes a country run.

Despite a crying need for better infrastructure, investment in it has actually fallen in 10 major economies since the financial crisis, including the US, according to a new study by the McKinsey Global Institute. Meanwhile, China is still going gangbusters on roads, bridges, sewers, and everything else that makes a country run. In contrast to the widespread declines, the institute says, infrastructure spending grew as a share of GDP in Japan, Germany, France, Canada, Turkey, South Africa and China. The chart from the MGI report shows China’s strength in infrastructure spending. Its bar is the highest. There’s such a thing as too much infrastructure spending, of course. At current rates of investment, China, Japan, and Australia are likely to exceed their needs between now and 2030, the McKinsey & Co-affiliated think tank says. To fund more public infrastructure, the report favours raising user charges such as highway tolls, among other measures.

In contrast to the widespread declines, the institute says, infrastructure spending grew as a share of GDP in Japan, Germany, France, Canada, Turkey, South Africa and China. The chart from the MGI report shows China’s strength in infrastructure spending. Its bar is the highest. There’s such a thing as too much infrastructure spending, of course. At current rates of investment, China, Japan, and Australia are likely to exceed their needs between now and 2030, the McKinsey & Co-affiliated think tank says. To fund more public infrastructure, the report favours raising user charges such as highway tolls, among other measures.