Chartered Accountants in Practice/Firms of Chartered Accountants to register themselves on GeM (Government e- marketplace) Portal

The Institute of Chartered Accountants of India ( ICAI ) has permitted the Chartered Accountants ( CA ) in Practice, Firms of Chartered Accountants are permitted to register on GeM Portal for rendering professional services.

The ICAI has said that, The Institute has been receiving queries as to whether Chartered Accountants in Practice/Firms of Chartered Accountants can register themselves on GeM Portal as registration on the Portal is a pre-requirement for providing professional services to the Government departments/ organisations.

The ICAI has clarified that, the Chartered Accountants in Practice / Firms of Chartered Accountants are permitted to register on GeM Portal for rendering professional services.

The information being published on the portal should be in compliance with the provisions of Code of Ethics.

The ICAI also said that, the Guidelines on Tenders dt. 7th April, 2016 issued by the Institute will be applicable to tender floated through GeM Portal also without any change.

The Guidelines are appearing as Appendix -J of Volume-II of Code of Ethics, and may be accessed on the website of the Institute at the link below:

This provides an opportunity to the ICAI members to expand their professional horizons and to foster working relations between the two accounting institutes. The Institute of Chartered Accountants of India (ICAI) and Chartered Accountants Australia and New Zealand (CA ANZ) will have an opportunity to play the leadership role in addressing new challenges facing the profession in a globalized environment.

The Cabinet, chaired by Prime Minister Shri Narendra Modi, has approved a fresh Memorandum of Understanding (MoU) between the Institute of Chartered Accountants of India (ICAI) and Chartered Accountants Australia and New Zealand (CA ANZ).

Impact:

The MOU intends to develop mutually beneficial relationship in the best interest of members, students and their organizations and is expected to provide an opportunity to the ICAI members to expand their professional horizons and to foster working relations between the two accounting institutes. The two accountancy institutes will have an opportunity to play the leadership role in addressing new challenges facing the profession in a globalized environment.

Benefits:

The engagement between the two Institutes is expected to result in greater employment opportunities for Indian Chartered Accountants and also greater remittances back to India.

Details:

The Memorandum of Understanding (MoU) between the Institute of Chartered Accountants of India (ICAI) & Chartered Accountants Australia and New Zealand (CA ANZ) would mutually recognize the qualification and admit the Members in good standing by prescribing a bridging mechanism between the two Institutes. The ICAI and CA ANZ aim to establish a mutual co-operation framework for the advancement of accounting knowledge, professional and intellectual development, advancement of the interests of their respective members and contribute positively to the development of the accounting profession in Australia, New Zealand and India.

Implementation strategy and Targets:

The MoU provides for mutual recognition of qualification of members of other body, who have achieved membership by completing the Examination, professional program and practical experience membership requirements of the two parties.

Background:

The Institute of Chartered Accountants of India (ICAI) is a statutory body established by an Act of Parliament of India, The Chartered Accountants Act, 1949′, to regulate the profession of Chartered Accountancy in India. Chartered Accountants Australia and New Zealand (CA ANZ), emerged from the merger of the Institute of Chartered Accountants in Australia and the New Zealand Institute of Chartered Accountants in October 2014.

The RBI notified Rotation Policy instead of Cooling Period for Bank Branch Audit for CAs.

The Reserve Bank of India (RBI) notified the change in norms on eligibility, empanelment, the appointment of Statutory Branch Auditors in Public Sector Banks from years 2020-21 onwards.

The RBI notified Rotation Policy instead of Cooling Period for Bank Branch Audit for CAs. In other words, the concept of compulsory rest for two years for audit firms located in the specified centres, after completion of four years of continuous branch audit, followed till Financial Year 2019-20 has been done away with.

Instead, the branch auditors across all the centres of the country, on completion of four years of continuous branch audit, will be subjected to the policy of rotation i.e. they may be considered for appointment as SBAs of any other PSB.

However, the audit firms will not be eligible to be re-appointed as SBAs, in the same bank where they completed their audit assignment prior to rest/rotation, at least for one cycle of four years.

The RBI further notified the change on norms for selection of branches of Public Sector Banks (PSBs) for Statutory Audit.

Firstly, statutory branch audit of PSBs should be carried out so as to cover 90% of all funded and 90% of all non-funded credit exposures of a bank.

The selection of branches for statutory audit shall include a representative cross section of rural/semi-urban/urban and metropolitan branches, predominantly including branches which are not subjected to concurrent audit.

CPUs/LPUs/and other centralised hubs, by whatever nomenclature called, would be included for branch audit every year.

The selection of branches shall be finalised by each PSB with the consent of their Statutory Central Auditor/s. Secondly, in respect of those branches, which are subject to concurrent audit by chartered accountants and not selected for branch audit, LFARs and other certifications done by concurrent auditors will be submitted to the Managing Director & CEO of the bank.

The banks in turn will consolidate/compile all such LFARs and other certifications submitted by the Concurrent Auditors and submit to Statutory Central Auditor/s as an internal document of the bank.

The RBI notified the change in the procedure for appointment of Statutory Branch Auditors.

Firstly, the list of eligible auditors/audit firms will be prepared by the Institute of Chartered Accountants of India (ICAI) as per the norms prescribed by RBI.

Secondly, the list will be subjected to scrutiny by RBI for identifying the continuing and rested firms and excluding audit firms who have been denied audit.

Thirdly, RBI will, thereafter, forward the final list of all eligible auditors/audit firms to PSBs for selection of the required number of branch auditors/audit firms.

Banks will be required to clearly advise the selected audit firms that each audit firm can take up audit assignments (branch audit) in one PSB only. The audit firm should give its consent in writing for consideration of appointment in the bank concerned for the particular year and the subsequent continuing years.

Fourthly, the consent given by an audit firm is irrevocable and no request from audit firms for changing the bank, after giving its consent will be entertained.

Fifthly, after the selection of branch auditors, PSBs will be required to recommend the names of both continuing and selected branch auditors to RBI for seeking its prior approval before their actual appointment, as per statutory requirement.

The RBI while elaboration on the change in general guidelines applicable to appointment of Statutory Branch Auditors stated that SBAs will have a maximum tenure of four years in a particular bank.

The appointment of SBAs will be made on an annual basis, subject to their fulfilling the eligibility norms prescribed by RBI from time to time, and also subject to their suitability.

“While allotting branches, banks are required to select auditors/audit firms which are in close proximity to their offices/branches. Banks are also required to have a suitable mix of various categories of auditors / audit firms while selecting the branch auditors keeping in view the size of the branches to be audited.

Banks are advised to allot branches, to the extent possible, to the audit firms taking into consideration their category and audit experience in such a way that specialised and larger branches are audited by bigger/experienced audit firms,” the RBI said.

The audit firms retiring as Statutory Central Auditors from a PSB shall not be eligible to be appointed as SBAs of the same PSB during the prescribed cooling period for SCAs from that particular PSB.

The RBI notified change in the eligibility norms for the empanelment of audit firms to be appointed as Statutory Branch Auditors in PSBs.

The Institute of Chartered Accountants of India, in its gazette notification had made the generation of UDIN from the ICAI website mandatory for every kind of certificate/tax audit report and other attests made by their members as required by various regulators. This was introduced to curb fake certifications by non-CAs misrepresenting themselves as Chartered Accountants

The income tax department will validate with the Institute of Chartered Accountants of India (ICAI) the unique document identification number (UDIN) of chartered accountants when they upload tax audit reports, the finance ministry said on Thursday.

To curb fake certifications by non-CAs misrepresenting themselves as chartered accountants, the ICAI in 2019 made generation of UDIN from the ICAI website mandatory for every kind of certificate and tax audit report and other attests made by their members as required by various regulators.

The ministry said that in line with the ongoing initiatives of the income tax department for integrating with other government agencies and bodies, income-tax e-filing portal has completed its integration with the ICAI portal for validation of UDIN generated from the ICAI portal by the chartered accountants for documents certified/attested by them.

Income-tax e-filing portal had already factored mandatory quoting of UDIN with effect from April 27, 2020, for documents certified/attested in compliance with the Income Tax Act,1961 by a chartered accountant.

“With this system level integration, UDIN provided for the audit reports/certificates submitted by the chartered accountants in the e-filing portal shall be validated online with the ICAI,” the ministry added.

It said this will help in weeding out fake or incorrect tax audit reports not duly authenticated with the ICAI.

If a chartered accountant was not able to generate UDIN before submission of audit report or certificate, the e-filing portal permits such submission, subject to the CA updating the UDIN within 5 calendar days from the date of form submission in the income tax e-filing portal.

If the UDIN for the audit report/certificate is not updated within the 15 days, such audit report and certificate uploaded shall be treated as invalid submission, the ministry added.

The overall objective of the LFAR should be to identify and assess the gaps and vulnerable areas in the business operations, risk management, compliance and the efficacy of internal audit and provide an independent opinion on the same to the Board of the bank and provide their observations

The Reserve Bank on Saturday came up with revised long format audit report (LFAR) norms with a view to improving efficacy of internal audit and risk management systems.

The LFAR, which applies to statutory central auditors (SCA) and branch auditors of banks, has been updated keeping in view the large scale changes in the size, complexities, business model and risks in the banking operations, the RBI said.

The Chairman / Managing Director / Chief Executive Officer All Scheduled Commercial Banks (Excluding RRBs) All Local Area Banks All Small Finance Banks and All Payment Banks

Madam /Dear Sir,

Long Form Audit Report (LFAR) – Review

Please refer to RBI circular No. DBS.CO.PP.BC.11/11.01.005/2001-2002 dated April 17, 2002 on revision of Long Form Audit Report (LFAR).

2. Keeping in view the large scale changes in the size, complexities, business model and risks in the banking operations, a review of the LFAR formats, in consultation with the stakeholders, including the Institute of Chartered Accountants of India (ICAI), was undertaken and it has been decided to make the following changes.

3. The format of LFAR, as mentioned below, have been revised:

Annex I for Statutory Central Auditors (SCA)

Annex II for Branch Auditors

An Appendix as part of Annex II for the specialized branches and

Annex III on Large / Irregular / Critical accounts for branch auditors.

The revised formats are enclosed.

4. The revised LFAR formats are required to be put into operation for the period covering FY 2020-21 and onwards. The mandate and scope of the audit will be as per this format and if the SCA feels the need of any material additions, etc., this may be done by giving specific justification by the SCA and with the prior intimation of the bank’s Audit Committee of Board (ACB).

5. Regarding other operational issues relating to submission of LFAR, we further advise as under:

Timely receipt of LFARs from the auditors should be ensured;

The LFAR on the bank, after due examination, should be placed before the ACB / Local Advisory Board of the bank indicating the action taken/proposed to be taken for rectification of the irregularities, if any, mentioned therein; and

A copy each of the LFAR (i.e. for the bank / all Indian Offices of foreign bank as a whole) and the relative agenda note, together with the Board’s views or directions, should be forwarded to the concerned Senior Supervisory Manager (SSM) in the Department of Supervision, Reserve Bank of India within 60 days of submission of the LFAR by the statutory auditors.

6. The LFAR format and other instructions issued vide RBI circular No. DBS.CO.PP.BC.11/11.01.005/2001-2002 dated April 17, 2002 stand repealed.

Institute of Chartered Accountants of India enable generation of UDIN (Unique Document Identification Number) for certification by its members

A provision for generating UDIN in bulk for Certificates has been incorporated in UDIN Portal.

Using this facility now the members will be able to generate UDIN in bulk (uptil 300 UDINs) for various types of Certificates in one go. It can be done through uploading of excel file.

Process for bulk UDIN

Step-wise complete process for generating bulk UDINs is as under:

i) After login, from the Menu bar, click on Bulk UDIN for Certificates. Minimum 3 certificates and Maximum 300 certificates can be generated using this procedure.

ii) Download template file from Download Template button and open in Excel. Please note that the .xlsx file can be opened in Excel 2007 and later versions.

iii) Select Certificate type from drop down.

iv) Input dates in the format as per your system/computer (generally it is in mm/dd/yyyy or as 10 June 2020). Excel will format dates automatically in required format i.e dd-mm-yyyy. Do not use copy paste in this cell.

v) Fill in all the parameters and values.

vi) Save the file.

vii) Click on the upload file on the Certificate Form on UDIN Portal.

viii) Select the file just saved now.

ix) Portal will populate the data in the Form. Verify the data so populated.

x) If correct, Send and Verify OTP and Submit.

xi) Alternatively, the option of filling the details of Type of Certificates, Dates and key fields etc. is available on the form itself.

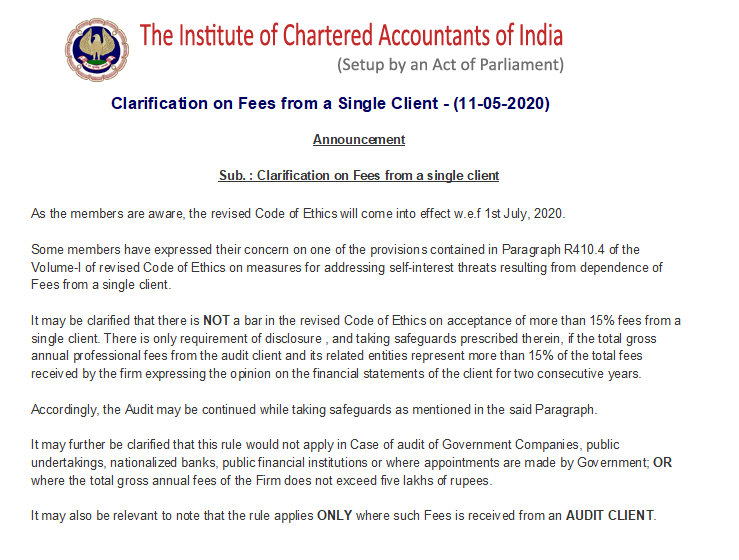

The Institute of Chartered Accountants of India ( ICAI ) has clarified that there is NOT a bar in the revised Code of Ethics on acceptance of more than 15% fees from a single client.

The ICAI has said that some members have expressed their concern on one of the provisions contained in Paragraph R410.4 of the Volume-I of revised Code of Ethics on measures for addressing self-interest threats resulting from the dependence of Fees from a single client.

The ICAI clarified that there is NOT a bar in the revised Code of Ethics on acceptance of more than 15% fees from a single client. There is the only requirement of disclosure, and taking safeguards prescribed therein, if the total gross annual professional fees from the audit client and its related entities represent more than 15% of the total fees received by the firm expressing the opinion on the financial statements of the client for two consecutive years.

Accordingly, the Audit may be continued while taking safeguards as mentioned in the said Paragraph. The ICAI further clarified that this rule would not apply in case of audit of Government Companies, public undertakings, nationalized banks, public financial institutions, or where appointments are made by Government; OR where the total gross annual fees of the Firm does not exceed five lakhs of rupees.

It may also be relevant to note that the rule applies ONLY where such Fees are received from an AUDIT CLIENT.