The World Bank’s ease of doing business report showed that eight reforms were key in helping businesses in 2016/17. India is also among the 10 economies to have improved the most, alongside El Salvador, Malawi, Nigeria and Thailand.

Doing business in India became much easier over the past one year because of a raft of policy reforms, an annual World Bank index showed on Tuesday, in what is possibly a shot in the arm for Prime Minister Narendra Modi’s efforts to win big-ticket investments.

For the first time, India jumped 30 places to break into the top 100 in the ease of doing business rankings for the year to June 2017. The 190-country index is an influential barometer of competitiveness among countries that likely also helps businesses make investment decisions.

India’s impressive performance was largely due to reforms in taxation, insolvency laws and access to credit, part of measures Prime Minister Modi’s government has pushed to boost investment and jobs that would help absorb a million people who join the workforce every month.

“India’s performance is not based on efforts of just one year but consistent efforts made over the last three years to continuously improve the regulatory environment of doing business,” Annette Dixon, vice president South Asia, told a press conference.

“It is the result of a number of reforms that the government has undertaken that India is becoming a preferred destination to do business.”

India saw improvements in six of 10 indicators, including on winning construction permits, enforcing contracts, paying taxes and resolving insolvency. It, however, slipped when it came to starting a business, getting an electricity connection, cross-border trade and registering property.

Underlining how reforms had helped India improve its overall ranking, the World Bank said the establishment of debt recovery tribunals reduced non-performing loans by 28% and lowered interest rates on larger loans, suggesting that faster processing of debt recovery cases cut the cost of credit.

India was also among the 10 economies to have improved the most, alongside El Salvador, Malawi, Nigeria and Thailand.

The Global Competitiveness Index (GCI) is prepared on the basis of country-level data covering 12 categories or pillars of competitiveness.

India has been ranked as the 40th most competitive economy — slipping one place from last year’s ranking — on the World Economic Forum’s global competitiveness index, which is topped by Switzerland.

On the list of 137 economies, Switzerland is followed by the US and Singapore in second and third places, respectively.

In the latest Global Competitiveness Report released today, India has slipped from the 39th position to 40th while neighbouring China is ranked at 27th.

“India stabilises this year after its big leap forward of the previous two years,” the report said, adding that the score has improved across most pillars of competitiveness. These include infrastructure (66th rank), higher education and training (75) and technological readiness (107), reflecting recent public investments in these areas, it added.

According to the report, India’s performance also improved in ICT (information and communications technologies) indicators, particularly Internet bandwidth per user, mobile phone and broadband subscriptions, and Internet access in schools.

However, the WEF said the private sector still considers corruption to be the most problematic factor for doing business in India.

“A big concern for India is the disconnect between its innovative strength (29) and its technological readiness (up 3 to 107): as long as this gap remains large, India will not be able to fully leverage its technological strengths across the wider economy,” it noted.

Among the BRICS, China and Russia (38) are placed above India.South Africa and Brazil are placed at 61st and 80th spots, respectively.

In South Asia, India has garnered the highest ranking, followed by Bhutan (85th rank), Sri Lanka (85), Nepal (88), Bangladesh (99) and Pakistan (115).

“Improving ICT infrastructure and use remain among the biggest challenges for the region: in the past decade, technological readiness stagnated the most in South Asia,” WEF said.

Other countries in the top 10 are the Netherlands (4th rank), Germany (5), Hong Kong SAR (6), Sweden (7), United Kingdom (8), Japan (9) and Finland (10).

The Global Competitiveness Index (GCI) is prepared on the basis of country-level data covering 12 categories or pillars of competitiveness.

Institutions, infrastructure, macroeconomic environment, health and primary education, higher education and training, goods market efficiency, labour market efficiency, financial market development, technological readiness, market size, business sophistication and innovation are the 12 pillars.

According to WEF’s Executive Opinion Survey 2017, corruption is the most problematic factor for doing business in India.

The second biggest bottleneck is ‘access to financing’, followed by ‘tax rates’, ‘inadequate supply of infrastructure’, ‘poor work ethics in national labour force’ and ‘inadequately educated work force’, among others.

The survey findings are mentioned in the report.

“Countries preparing for the Fourth Industrial Revolution and simultaneously strengthening their political, economic and social systems will be the winners in the competitive race of the future,” WEF founder and Executive Chairman Klaus Schwab said.

Jim Kim said Japan, Europe and the US along with India were growing and there was a levelling-out in developing countries.

India has been growing “pretty robustly”, World Bank President Jim Yong Kim has said as he predicted a strong global growth this year.

Speaking at the Bloomberg Global Business Forum meeting here on Wednesday, Kim also called for more cooperation among the multilateral system, private sector and the governments to take advantage of the current win-win situation.

“That dormant capital will earn a higher return, where developing countries will have access to much more capital for the infrastructure needs, even for investing in health and education, investing in resilience to climate change and other factors,” Kim said.

He said Japan, Europe and the US along with India were growing and there was a levelling-out in developing countries.

“A country like India is growing, has been growing pretty robustly. We think, Japan is growing. Europe is growing in a much more healthy way. The United States continues to grow. There is a levelling-out in developing countries,” he said, adding that the growth will be more robust this year.

In June, the World Bank predicted a 7.2 per cent growth rate for India this year against 6.8 per cent growth in 2016. India remains the fastest growing major economy in the world, the World Bank officials had said.

“It used to be that commodity importers were doing much better than commodity exporters. But that’s levelling out. So the growth is relatively more evenly distributed,” Kim said.

He said in terms of indebtedness, the bank was watching very carefully the debt-to-GDP ratios of every single country.

“In Africa, the debt-to-GDP ratios are still very manageable…We would not be moving toward providing more financing for countries if we thought there was a real problem with over indebtedness in the countries. Because we follow this very closely, along with the IMF,” he said.

“We think that there are tremendous opportunities for investment. But sometimes, purely based on perception, investors in sovereign wealth funds – I’ve heard them say, Africa is risky. Right, as if Africa was a single country.

Africa’s not a single country and the risk profiles from country to country have enormous differences,” he said.

The pact in the area of disaster risk management, entered into between the Ministry of Home Affairs and the Cabinet Office of the Government of Japan, aims to cooperate and collaborate in the field of disaster risk reduction, an official statement said

India and Japan on Wednesday signed 15 deals in key areas, including civil aviation, trade, science and technology, and skill development.

The pact in the area of disaster risk management, entered into between the Ministry of Home Affairs and the Cabinet Office of the Government of Japan, aims to cooperate and collaborate in the field of disaster risk reduction, an official statement said.

It said the understanding in the field of skill development looks to further strengthen bilateral relations and cooperation in the field of Japanese language education in India.

The one titled ‘India-Japan Investment Promotion Road Map’ envisages enhanced Japanese investments in India while the ‘Japan-India special programme for Make In India’ is on bilateral cooperation towards infrastructure development in the Mandal Bechraj-Khoraj region in Gujarat.

There was exchange of RoD (Record of Discussions) on civil aviation under which Indian and Japanese carriers can now mount unlimited number of flights to selected cities in both countries.

There was an agreement to establish a joint exchange programme to identify and foster talented young scientists from both countries to collaborate in the field of theoretical biology.

The MoU (Memorandum of Understanding) between the Department of Biotechnology and Japan’s National Institute of Advanced Science & Technology (AIST) seeks to promote research collaboration between these institutions in the field of life sciences and biotech, the statement said.

The India Japan Act East Forum, among the agreements signed, seeks to enhance connectivity and promote developmental projects in India’s North Eastern region in an efficient and effective manner, it said.

There were four agreements in the field of sports, including one to facilitate and deepen international education cooperation and exchanges between both Sports Authority of India and Nippon Sport Science University, Japan.

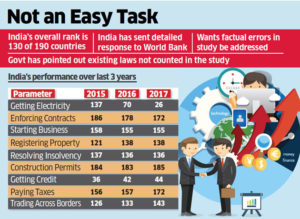

The government expects a double-digit improvement in India’s rank in the global index on ease of doing business, likely to be announced by the World Bank next month.

A senior official told ET that the World Bank had shared its feedback, stating that it had accepted many of the reforms claimed by the government. Last year, India’s rank had improved by just one spot to 130 among 190 countries.

“The World Bank has acknowledged around 20 reforms among many more mentioned by us in response to their study … The overall ranking will depend on how other countries have performed, but we should come close to the 100 mark,” the official said.

The World Bank had recently finished gathering feedback from users for its Doing Business Report. The cut-off date for implementing reforms for the study was June 1. Reforms implemented thereafter will not be counted for this year’s ranking.

Reforms such as GST have not been taken into account as the impact is yet to be felt by users. But India is expecting these to reflect in next year’s report and significantly boost the country’s position.

India had showed one of its poorest performances on the parameter of ‘Paying Taxes’ last time, ranking 172 among the countries surveyed for the report. That, along with an equally lower position in ‘Enforcing Contracts’, landed India at the 130th spot, falling behind countries such as Mexico (38), Russia (51) and Pakistan (138). The ranking considers business environment in Delhi and Mumbai.

Over the past few months, the government has taken up concerns about not getting due credit for its reform drive with the World Bank. While responding to the survey this year, the government flagged such issues citing examples of reforms undertaken for enforcing contracts, starting business and issuing construction permits, among other things.

The government also cited provisions in the existing legal framework that deal effectively with the issue of enforcing contracts.

ET View: Push legal reforms

The way ahead is to push reforms. India fares poorly, for example, in enforcing contracts. We need judicial reforms to drastically reduce legal delays. So, even if states improve lower courts, disputes could end up in the higher judiciary and the reform lies with the Centre. The Department of Justice should drive the reforms. The need is also to enhance transparency in funding of political parties. It will weed out corruption that will automatically improve ease of doing business.

Gujarat is followed by Delhi, Andhra Pradesh, Haryana, Telangana, Tamil Nadu, Kerala, Maharashtra, Karnataka and Madhya Pradesh.

Gujarat has retained the top position in the list of 21 states and UTs with most investment potential, according to a report by economic think-tank NCAER.

Gujarat is followed by Delhi, Andhra Pradesh, Haryana, Telangana, Tamil Nadu, Kerala, Maharashtra, Karnataka and Madhya Pradesh.

The ranking of 20 states and one Union Territory of Delhi was based on six pillars — labour, infrastructure, economic climate, governance and political stability, perceptions and land — and 51 sub-indicators.

While Gujarat topped in economic climate and perceptions, Delhi ranked one in infrastructure. While Tamil Nadu topped the chart in labour issues, Madhya Pradesh ranked one in land pillar.

The National Council of Applied Economic Research (NCAER) State Investment Potential Index (N-SIPI 2017) report ranks states on their competitiveness in business and their investment climate.

Compared to 2016, Gujarat and Delhi again top the list of states, while Haryana and Telangana have moved rapidly up the ranks to finish among the top five, it said.

NCAER Director-General Shekhar Shah said: “Investment opportunities are expanding in India in all sectors. The GST will weave India’s states together in ways that has not been possible before”.

Further the report said that although Bihar, Uttar Pradesh and West Bengal are ranked among the least favourable states for investment, they rank higher under individual pillars.

Indira Iyer, the team leader for the 2017 N-SIPI, stated that as per the report, “corruption” continues to be the number one constraint faced by businesses.

However, she said, the 2017 N-SIPI reports a decline in the percentage of respondents citing corruption as a constraint to conducting business from 79 per cent in 2016 to 57 per cent in 2017.

Getting approvals for starting a business is still the second-most pressing constraint faced by businesses in 2017 as was the case in 2016, she added.

Talking about this index, Department of Industrial Policy and Promotion (DIPP) Secretary Ramesh Abhishek said these reports are aiding states in improving the business climate and attracting investors.

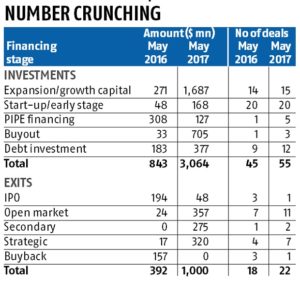

PE, Venture Capital flows up 155% in May to $ 3 billion; SoftBank – Paytm deal tops

Private equity and venture capital (PE/VC) investments have recorded the highest monthly investments in the past 10 years at $3.1 billion in May 2017. For the third consecutive month in a year, the investment flow crossed the $2-billion mark.

The financial services sector topped the table on account of the $1.4-billion investment by Softbank in Paytm. This deal accounted 46 per cent of aggregate deal value for the month.

According to Ernst & Young (EY) data, the month recorded a 264 per cent increase in terms of value and 23 per cent in volume over May 2016. PE/VCs have invested $3,064 million across 55 deal in May this year as against $843 million across 45 deals in May 2016.

There were five deals of more than $100 million aggregating to $2.3 billion, accounting for 75 per cent of the aggregate deal value in May 2017.

Another important deal during the month was the $500-million investment by Canada Pension Plan Investment Board (CPPIB) in Indospace (a real estate platform for industrial and logistics parks) for a majority stake, thus taking the investments by Canadian pension funds in 2017 close to $2 billion.

Mayank Rastogi, partner and leader for PE, EY said that Indian PE/VC market has significantly matured over time. Five to seven years ago, the classic growth capital was the only meaningful capital pool available with limitations such as investment horizon and return expectations, and could not have suited some specific situations.

There are a variety of capital pools available ranging from angel/VC to buyout funds, family offices, pensions and sovereigns, corporate funds, debt funds, sector-focused funds providing solutions that address specific needs. This is one of the key drivers for continuing buoyancy in the PE/VC investments in India despite slow growth capital investing.

Financial services ($1.6 billion across 11 deals) emerged as the most active sector on account of the Paytm-Softbank deal, the largest deal in the financial services sector till date. The real estate sector bagged four deals worth $709 million, followed by e-commerce sector’s six deals worth $211 million in terms of activity.

May 2017 recorded $1 billion in exits and was the second consecutive month with more than $1 billion in exits.

The strong buyout trend established over the past two years continued into 2017 with $2 billion invested across 18 deals till date.

Between January and May, there was a significant increase of over 60 per cent compared to 2016 and over 100 per cent compared to 2015, both, in terms of value and volume.

Debt deals recorded the biggest monthly volume since 2014 with $377 million recorded across 12 deals.

Given the buoyancy in the public markets, open market deals emerged as the preferred mode of exit, accounting for 36 per cent of exits by value and 50 per cent by volume, similar to the trend seen in the previous month.

Till date, open market exits have accounted for 49 per cent of the total value of exits in 2017 compared to 25 per cent for the whole of 2016. May 2017 recorded $90 million in fund raise, a decline of 82 per cent and 76 per cent as compared to May 2016 and April 2017 respectively. The plans for fund raise announced during the month stood at $908 million.

There was one PE-backed initial public offering (IPO) in May 2017 (S Chand, a publishing company, primarily in the education space), which saw Everstone exiting a 13.9 per cent stake for $48 million. Till May 2017, PE-backed IPO tally stands at four compared to eight during the same period in 2016.

Financial services emerged as the leading sector with exits worth $466 million across six deals followed by the healthcare sector with exits worth $260 million across three deals.