Summary of Direct and Indirect Tax Proposals: Budget 2024-25

Summary of the direct and indirect tax proposals made in the Budget 2024-25 (Finance Bill 2024) presented by Smt Nirmala Sitharaman, Union Minister of Finance and Corporate Affairs:

Highlights of the Direct Tax Proposals of Finance Bill, 2024

No changes in Tax Rates

No changes have been proposed to the existing rates of direct and indirect taxes. The existing rates of income tax, gst, import duties, etc. have been retained.

To provide continuity, some tax benefits and exemptions have been extended by 1 year until 31st March 2025. These include:

Tax benefits for startups;

Tax exemptions on certain income for International Financial Services Centers (IFSCs); and

Tax exemptions on investments made by sovereign wealth funds and pension funds.

The Interim Budget 2024 maintains the status quo on tax rates and extends certain tax breaks by a year to provide stability and continuity in taxation. No new changes or reforms have been introduced to the tax structure or rates.

Withdrawal of Outstanding direct tax demands

The FM has announced to withdraw the outstanding demands of income tax. Here is a summary of the key points regarding the withdrawal of outstanding direct tax demands announced in the Interim Budget 2024:

i) In line with the government’s vision to improve ease of living and doing business, outstanding petty direct tax demands up to Rs 25,000 dating back to 1962 will be withdrawn for the period up to FY 2009.

ii) Similarly, outstanding demands up to Rs 10,000 will be withdrawn for the FY 2010-11 to 2014-15.

iii) These are non-verified, non-reconciled or disputed demands that continue to remain on the books, causing anxiety for taxpayers.

Withdrawing these demands will help provide relief to honest taxpayers and enable refunds for subsequent years.

This is expected to benefit about 1 crore taxpayers who have such outstanding demands.

The move aims to improve tax payer services and reduce harassment of taxpayers over small disputed sums dating back decades.

In short, the Interim Budget 2024 has announced the withdrawal of old, petty direct tax demands up to Rs 25,000 till FY 2009-10 and Rs 10,000 between FY 2010-11 to 2014-15 to provide relief to taxpayers.

Highlights of the Indirect Tax Proposals of Finance Bill 2024

The FM has proposed in Budget 2024 to retain the same tax rates in respect of GST, import duty, etc.indirect taxes as are applicable at present, i.e. existing GST and import duty rates shall continue in FY 2024-25 as well.

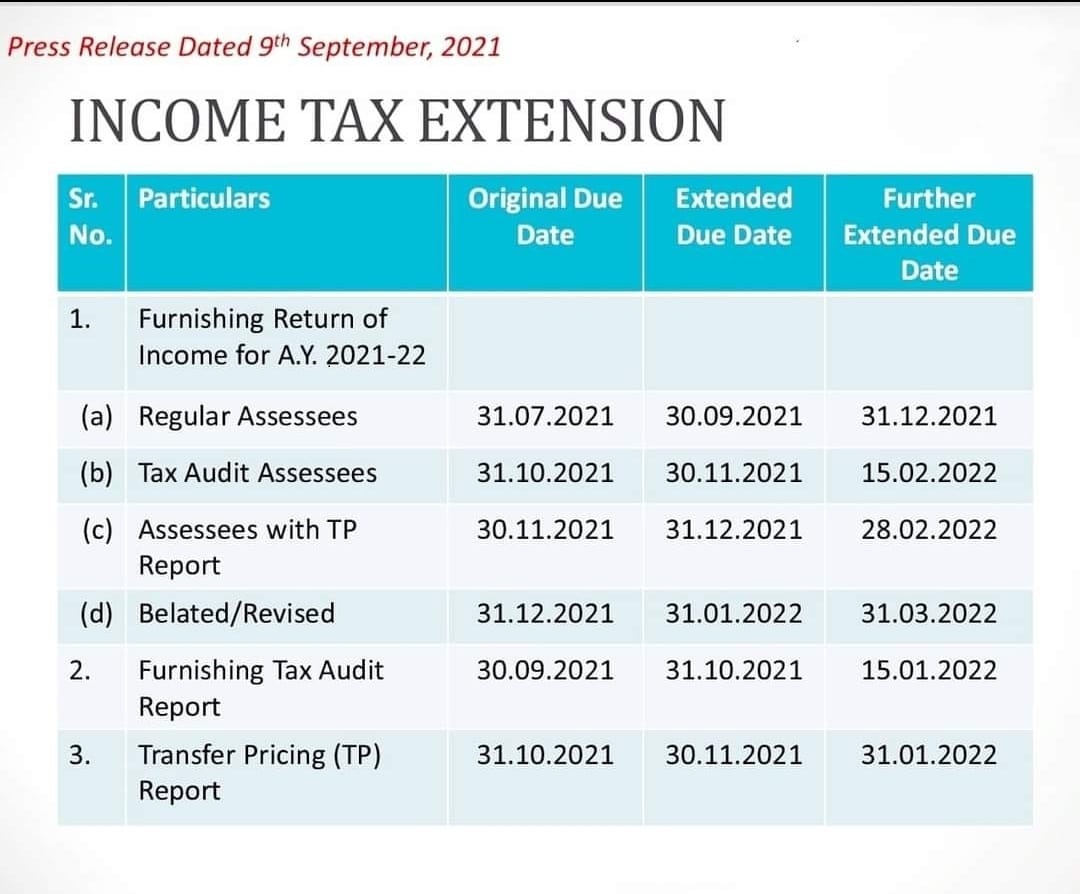

• This is the second time this financial year the government has extended the deadline of filing ITR for individuals whose accounts are not required to be audited. • The ITR filing deadline has been extended due to the many technical issues related to the government’s newly launched tax filing portal. • The deadline of filing belated/revised ITR has been extended by two months to March 31, 2022.

The government on Thursday extended the deadline to file income tax return (ITR) for FY 2020-21 by 3 months to December 31, 2021 from September 30, 2021. The extension of the deadline is for those individuals whose accounts are not required to be audited and who usually file their income tax return using ITR-1 or ITR-4 forms, as applicable.

In a statement, the Finance Ministry said that the decision has been on consideration of difficulties reported by the taxpayers and other stakeholders in filing of Income Tax Returns and various reports of audit for the Assessment Year 2021-22 under the Income Tax Act, 1961.

The income tax return (ITR) filing deadline for FY 2020-21 for individuals has already been extended, from the normal deadline of July 31, 2021. However, the new income tax e-filing portal has been marred by glitches and other problems from inception. Finance minister Nirmala Sitharaman has given Infosys, the company which set up the new income tax portal, time till September 15, 2021 to fix all the problems.

Last year too, the government has extended the due date of filing ITR for individuals four times – first from July 31 to November 30, 2020, then to December 31, 2020, and finally to January 10, 2021.

“On consideration of difficulties reported by the taxpayers in filing of Income Tax Returns(ITRs) & Audit reports for AY 2021-22 under the ITAct, 1961, CBDT further extends the due dates for filing of ITRs & Audit reports for AY 21-22. Circular No.17/2021 dated 09.09.2021 issued,” I-T Department tweeted on Thursday.

The due date of furnishing of report of audit under any provision of the Act for the previous year 2020-21, has been extended to January 15, 2022.

The due date of furnishing report from an accountant by persons entering into international transaction or specified domestic transaction under section 92E of the Act for the previous year 2020-21, is now January 31, 2022.

Again, the IT Department has decided to extend the due date of furnishing of Return of Income for the AY 2021-22, to February 15, 2022, among several other extensions.

The due date of furnishing of Return of Income for the Assessment Year 2021-22, which was December 31, 2021 has also been extended to February 28, 2022.

The due date of furnishing of belated or revised return of Income for the AY 2021-22 has been further extended to March 31, 2022.

Missing the ITR filing deadline would have had penal consequences. A late filing fee of Rs 5,000 would be levied if the ITR is filed by an individual after the expiry of the deadline.

Do keep in mind that government has also extended the deadline of filing belated ITR by one month from new deadline of December 31, 2021, to January 31, 2022. If the ITR is not filed by January 31, 2022, then the individual will not be able to file ITR for FY 2020-21, unless a notice is issued by the income tax department.

A late filing fee of Rs 5,000 along with penal interest at the rate of 1 per cent per month will be levied on the non-payment of tax dues in this case.

The initiative would play a catalytic role in contributing to the growth of the identified companies and would also have downstream benefits such as growth and diversification of India’s exports, impetus to brand India, and employment generation.

Union finance minister Nirmala Sitharaman on Saturday launched the Ubharte Sitaare Fund (USF) for export-oriented small and mid-sized companies and startups in Lucknow. Sitharaman had announced the fund in her Budget speech in 2020 in the backdrop of constraints faced by small and mid-sized companies in realising their export ambitions, stating that micro, small and medium enterprises (MSMEs) were important to keep the “wheels of the economy moving”.

The fund, jointly sponsored by Exim Bank and SIDBI, has a size of Rs 250 crore with a green shoe option of Rs 250 crore. The fund will invest by way of equity, and equity-like products, in export-oriented units, both in the manufacturing and services sectors.

Stating that the ambitious programme was to support the champion sectors, she said some developed countries like Germany have already tried this by identifying, supporting and hand-holding the champion sectors and giving them necessary technology and fund infusion. Ubharte Sitaare largely follows the same principal, she said, adding that induction of tech will itself bring a big difference to the small and medium units.

“A project that was tailormade for MSMEs to identify champions among them and also support them now also gets the additional benefit of UP’s one-district-one-product (OPOD) programme. UP has already completed the identification process of every product in every district, and also the champions in the state. So UP justifies the launch of Ubharte Sitaare programme,” she said, adding that this will help Sidbi to extend the credit and technology facility and boost capacity to go to the market to raise funds.

The FM highlighted the efforts taken by the government to provide a boost to the MSME sector in the country, including the launch of the production-linked incentive scheme and noted that the USF would make investments in export-oriented small and mid-sized companies by way of equity and equity-like products, and thereby help script a new paradigm of growth in exports. The initiative would play a catalytic role in contributing to the growth of the identified companies and would also have downstream benefits such as growth and diversification of India’s exports, impetus to brand India, and employment generation.

Harsha Bangari, deputy managing director, India Exim Bank, said India Exim Bank has developed a robust pipeline of over 100 potential proposals and supported several companies across a diverse range of sectors. SIDBI chairman & managing director Sivasubramanian Ramann highlighted several initiatives that have been taken in the recent past for the benefit of MSMEs in the country, more so in the state of Uttar Pradesh. Meanwhile, in another event, Punjab National Bank MD & CEO SS Mallikarjuna Rao handed over a loan sanction letter of Rs 5,100 crore for implementation of the Ganga Expressway project to the Uttar Pradesh Expressways Industrial Development Authority (UPEIDA).

The 594 km-long, eight-lane expressway project from Meerut to Prayagraj will cost nearly Rs 36,000 crore and will pass through 12 districts in UP. The amount of Rs 5,100 crore, under the securitisation process will be repaid to the bank within a period of 15 years from the toll to be received on the Agra-Lucknow Expressway. During this period of loan repayment, the expressway would continue to be owned and operated by UPEIDA.

Income tax return filing due date: ITR FOR COMPANIES:- Deadline for filing income tax return for 2019-20 by companies extended by 15 days to Feb 15, 2021and for individuals by 10 days to Jan 10, 2021

In a major development, Income Tax department has extended the deadline for ITR filings. The deadline for filing income tax return for 2019-20 by companies extended by 15 days to Feb 15, 2021. Further, the deadline for filing income tax returns by individuals extended by 10 days to January 10, 2021. Also, the last date to declare under Vivad se Vishwas Scheme extended to 31st January 2021, it was expiring on December 31st.

Deadline for filing income tax return for 2019-20 by companies extended by 15 days to Feb 15, 2021 & deadline for filing income tax returns by individuals extended by 10 days to Jan 10, 2021

Taking to Twitter, Income Tax Department said, “In view of the continued challenges faced by taxpayers in meeting statutory compliances due to outbreak of COVID-19, the Govt further extends the dates for various compliances. Press release on extension of time limits issued today:”

Earlier, direct tax professionals had sought extension for tax audit report, income tax returns for audit cases and time limit for AGMs in the wake of the ongoing pandemic scenario. The Direct Taxes Professionals Association (DTPA) had urged Finance Minister Nirmala Sitharaman for extension of date of furnishing of tax audit report under section 44AB to February 28 and the due date of filing of income tax returns of assessment year 2020-21 in audit cases to March, 31, 2021.

Meanwhile, the IT department on Wednesday said more than 4.54 crore tax returns for 2019-20 fiscal have been filed till December 29. In the comparable period last year, 4.77 crore income tax returns were filed. At the close of deadline for filing ITRs without payment of late fees for fiscal 2018-19 (assessment year (AY) 2019-20), over 5.65 crore returns were filed by taxpayers.

In a tweet on Wednesday, the Income Tax department nudged taxpayers to file their ITRs by the due date. “More than 4.54 crore Income Tax Returns for AY 2020-21 have already been filed till 29th of December, 2020,” the I-T department said.

The data released by the tax department showed that over 2.52 crore ITR-1 have been filed till December 29, 2020, lower than the 2.77 crore filed till August 29, 2019.

Over 1 crore ITR-4 have been filed till December 29 as compared to 99.50 lakh filed till August 29, 2019. An analysis of the data showed that individuals filing tax return for fiscal 2019-20 have slowed so far in the current year, while filings by businesses and trusts have increased.

Returns in ITR-1 Sahaj can be filed by an ordinarily resident individual whose total income does not exceed Rs 50 lakh, while form ITR-4 Sugam is meant for resident individuals, Hindu Undivided Families (HUFs) and firms (other than LLP) having a total income of up to Rs 50 lakh and having presumptive income from business and profession.

Over 33.93 lakh ITR-2 (filed by people having income from residential property) were filed till December 29.

During last year, the due date for filing ITR by individuals who do not need to get their accounts audited was August 31. However, the date has been extended till December 31 this year on account of the COVID-19 pandemic.

ITR-5 (filed by LLP and Association of Persons) filings till December 29, 2020 jumped to 7.09 lakh from 4.14 lakh filed till August 29, 2019. ITR-6 (filed by businesses) filings skyrocketed to over 3.46 lakh till December 29, 2020 as compared to 21,962 filed till August 29, 2019.

ITR-7 (filed by persons having income derived from property held under trust) filings also jumped to over 1.04 lakh till December 29, 2020 as compared to 41,963 till August 29 last year.

Earlier, for the FY 2019-20, the government had also extended the date for making various investment/ payment for claiming deduction under Chapter-VIA-B of the IT Act which includes section 80C (LIC, PPF, NSC etc.), 80D (Mediclaim), 80G (Donations) to 31st July, 2020. Now the investment/ payment can be made upto 31st July, 2020 for claiming the deduction under these sections for FY 2019-20. In the income tax forms, Schedule DI enables taxpayers to claim exemptions on investments they made during the extended period, until June 30, 2020.

Under normal circumstances, the last date to take income tax benefits is till March 31 of the financial year. The government had also extended the last date for the issuance of Form 16 by employers to their employees. In fact, the extension has been given for all TDS ( tax deducted at source) certificates, including Form 16. The CBDT has already notified the Income Tax Return Forms for the assessment year (AY) 2020-21 and are available for e-Filing by downloading either excel or Java utility.

The Direct Tax Vivad se Vishwas Act, 2020 was enacted on March 17, 2020 to settle direct tax disputes locked up in various appellate forums.

The Ministry of Finance has extended the deadline for making a declaration under Vivad Se Vishwas Scheme till 31′ January, 2021 from 31st December, 2020.

The Ministry of Finance has extended the deadline for making a declaration under Vivad Se Vishwas Scheme till 31′ January, 2021 from 31st December, 2020.

The date for the passing of order or issuance of notice by the authorities under the Direct Taxes & Benami Acts which are required to be passed/ issued/ made by 30th March 2021 has also been extended to 31st March 2021.

The Vivad se Vishwas scheme was announced by Union Finance Minister Nirmala Sitharaman during her budget speech on February 1, 2020.

Given below are all the aspects you have to know about this amnesty scheme: Under this scheme, taxpayers whose tax demands are locked in dispute in multiple forums, can pay due to taxes by March 31, 2020, and get a complete waiver of interest and penalty.

If a taxpayer is not able to pay within the deadline, he gets a further time till June 30, but in that case, he would have to pay 10% more on the tax.

Faceless e-assessment will have no human interface and it’s purpose will be to eliminate instances of “undesirable practices” on the part of tax officials.

The Central Board of Direct Taxes (CBDT) on Thursday revised the ‘E-assessment Scheme, 2019’ notified on September 12, 2019. The Government notified that now, the e-Assessment scheme shall be called Faceless Assessment.

Now, the National e-Assessment Centre shall intimate the assessee for the conduct of faceless assessment in case wherein notice has been issued by AO.

The Board has also extended its scope to cover best judgment assessments.

E-Assessment was a roadway towards a paperless, faceless assessment stripping away at bureaucratic layers. E-Assessment was earlier tried and tested by the Income-tax Department, before going forth with the E-Assessment Scheme, 2019.

The Board notified that in the notification dated September 12, 2019, in the opening portion, for the word “E-assessment”, the words “Faceless Assessment” shall be substituted. The Board notified the procedure for the faceless assessment wherein the National e-Assessment Centre shall serve a notice on the assessee under sub-section (2) of section 143, specifying the issues for selection of his case for assessment.

Promoting a transparent and fair tax regime, Prime Minister Narendra Modi unveiled ‘taxpayers’ charter’, enshrining rights of assesses in a statute under the Income tax law. With the launch of ‘Transparent Taxation — Honoring the Honest’ platform, Modi also unveiled faceless appeal and expanded the scope of faceless assessment, eliminating physical interface between taxpayers and tax authority.

Step wise process for Faceless Assessment, scope extended to cover best judgement assessment:

Introduction

The Central Board of Direct Taxes (CBDT) has revised the ‘E-assessment Scheme, 2019’ notified on September 12, 2019. Now, e-assessment scheme shall be called Faceless Assessment.

The National e-Assessment Centre shall intimate the assessee for conduct of faceless assessment in case wherein notice has been issued by AO. The Board has also extended its scope to cover best judgment assessments.

What was the E-assessment Scheme, 2019?

Finance Minister Nirmala Sitharaman had announced the e-assessment scheme in her Budget speech on July 5, 2019, which was subsequently inaugurated on October 7, 2019.

This was aimed at moving to faceless scrutiny and elimination of human interface in assessment proceedings. The scheme was set to bring in a “paradigm shift” in taxation by eliminating human interface in the income tax assessment system.

The Ministry of Finance vide Central Board of Direct Taxes (CBDT) notification No 61 & 62 dated 12th September 2019 has respectively notified the E- assessment Scheme 2019 & gave directions for its implementation.

E-assessment Scheme, 2019 to be now called as “Faceless Assessment”

Step wise process for Faceless Assessment

By the Notification issued by CBDT on 13th August, 2020, “E-assessment” will be now called as “Faceless Assessment”. Faceless assessment shall be made as per the following procedure:-

Step 1 – Issue of Notice on Assessee

National e-Assessment Centre shall serve a notice on the assessee under section 143(2), specifying the issues for selection of his case for assessment

Assessee may, within 15 days from the date of receipt of notice, file his response to the National e-assessment Centre

Step 2 – Case to be assigned to Assessment Unit

1.National e-assessment Centre shall assign the case selected for the purposes of e-assessment to a specific assessment unit in any one Regional e-assessment Centre through an automated allocation system

2. Where a case is assigned to the assessment unit, it may make a request to the National e-assessment Centre for:-

a. obtaining such further information, documents or evidence from the assesse or any other person

b. conducting of certain enquiry or verification by verification unit

c. seeking technical assistance from the technical unit

3. Where a request for obtaining further information, documents or evidence from the assessee or any other person has been made, the National e-assessment Centre shall issue appropriate notice or requisition to the assessee or any other person for obtaining the information, documents or evidence requisitioned by the assessment unit

4. Where a request for conducting of certain enquiry or verification by the verification unit has been made, the request shall be assigned by the National e-assessment Centre to a verification unit through an automated allocation system

5. Where a request for seeking technical assistance from the technical unit has been made, the request shall be assigned by the National e-assessment Centre to a technical unit in any one Regional e-assessment Centre through an automated allocation system

6. The assessment unit shall, after taking into account all the relevant material available on the record, make in writing, a draft assessment order either accepting the returned income of the assessee or modifying the returned income of the assessee, and send a copy of such order to the National e-assessment Centre with details of the penalty proceedings to be initiated therein, if any.

Step 3 – Draft Assessment Order

1.National e-assessment Centre shall examine the draft assessment order in accordance with the risk management strategy specified by the Board, including by way of an automated examination tool, whereupon it may decide to:-

a. finalise the assessment as per the draft assessment order and serve a copy of such order and notice for initiating penalty proceedings, if any, to the assessee, alongwith the demand notice, specifying the sum payable by, or refund of any amount due to, the assessee on the basis of such assessment, or

b. provide an opportunity to the assessee, in case a modification is proposed, by serving a notice calling upon him to show cause as to why the assessment should not be completed as per the draft assessment order, or

c. assign the draft assessment order to a review unit in any one Regional e-assessment Centre, through an automated allocation system, for conducting review of such order;

2. Review unit shall conduct review of the draft assessment order, referred to it by the National e-assessment Centre whereupon it may decide to:-

a. agree with the draft assessment order and intimate the National e-assessment Centre about such agreement; or

b. suggest such modification, as it may deem fit, to the draft assessment order and send its suggestions to the National e-assessment Centre;

3. National e-assessment Centre shall, upon receiving concurrence of the review unit, follow the procedure laid down in sub point (a) or (b) of point (1), as the case may be

4. National e-assessment Centre shall, upon receiving modification suggestions from the review unit, communicate the same to the Assessment unit

5. Assessment unit shall, after considering the modifications suggested by the Review unit, send the final draft assessment order to the National e-assessment Centre

6. The National e-assessment Centre shall, upon receiving final draft assessment order, follow the procedure laid down in sub point (a) or (b) of point (1),as the case may be

7. The assessee may, in a case where show-cause notice has been served upon him, furnish his response to the National e-assessment Centre on or before the date and time specified in the notice

8. The National e-assessment Centre shall,-

a. in a case where no response to the show-cause notice is received, finalise the assessment as per the draft assessment order; or

b. in any other case, send the response received from the assessee to the assessment unit;

9. The assessment unit shall, after taking into account the response furnished by the assessee, make a revised draft assessment order and send it to the National e-assessment Centre

Step 4 – Final Order and Completion of Assessment

The National e-assessment Centre shall, upon receiving the revised draft assessment order:-

a. in case no modification prejudicial to the interest of the assessee is proposed with reference to the draft assessment order, finalise the assessment or

b. in case a modification prejudicial to the interest of the assessee is proposed with reference to the draft assessment order, provide an opportunity to the assessee

c. the response furnished by the assessee shall be dealt with as per the procedure laid down in point 7, 8, 9 of Step 3

2. The National e-assessment Centre shall, after completion of assessment, transfer all the electronic records of the case to the Assessing Officer having jurisdiction over such case for:

a. imposition of penalty

b. collection and recovery of demand

c. rectification of mistake;

d. giving effect to appellate orders

e. submission of remand report, or any other report to be furnished, or any representation to be made, or any record to be produced before the Commissioner (Appeals), Appellate Tribunal or Courts, as the case may be

f. proposal seeking sanction for launch of prosecution and filing of complaint before the Court;

3. National e-assessment Centre may at any stage of the assessment, if considered necessary, transfer the case to the Assessing Officer having jurisdiction over such case.

Faceless assessment facility was extended to the entire country on 13th August, 2020, ending territorial jurisdiction and individual discretion, where an officer was the whole and sole to the assessee. Scrutiny will be allotted on a random basis. Assessment of a taxpayer in Delhi could well be carried by an officer sitting in Pune. It will put an end to needless litigation. Best Judgements Assessments under Section 144 will be also now covered under Faceless Assessment.

What is the meaning of Best Judgement Assessment?

The Best Judgment Assessment is a procedure under the Income Tax Act to comply with the principles of natural justice. Vide Section 144 of the Income Tax Act, 1961 the Assessing Officer is under an obligation to make an assessment of the total income or less to the best of his judgment in the following cases:

If the person fails to file a return required under section 139(1) and he has not filed a revised return.

If any person fails to comply with all the terms and conditions stipulated under a notice under section 142 or fails to comply with the directions requiring him to get his accounts audited in terms of section 142(2A).

If any person, after having filed a return fails to comply with all the terms of a notice under section 143(2) requiring his presence or production of evidence and documents; or

If the Assessing officer is not satisfied about the correctness and the completion of the accounts of the assessee if no method of accounting has been regularly employed by the assessee.

While Faceless Assessment and Taxpayers Charter came in force already, Faceless Appeal will be available from September 25, 2020. Under the Faceless Appeals system introduced by the government, appeals will be randomly allotted to any officer across the country and the identity of the officer deciding the appeal will remain unknown. The decisions will be team-based.

In a major relief to companies, the Securities and Exchange Board of India (SEBI) today extended the deadline for submission of financial results for the quarter, half-year, and financial year ended 30 June 2020 to September 15. The SEBI circular said that it has received representations requesting an extension of time for submission of financial results for the quarter or half year-ended 30 June 2020, due to the shortened time gap between the extended deadline for submission of financial results for the period-ended 31 March 2020 and the quarter or half year-ended June 30, 2020.

Under Regulation 33 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 (‘LODR Regulations’), a listed entity is required to submit its quarterly, half-yearly, or annual financial results within 45 days or 60 days, as applicable, from the end of each quarter, half year, or financial year.

Accordingly, listed entities were required to submit the financial results for the quarter, half-year-ended 30 June 2020 on or before 14 August 2020.

Earlier, the regulatory body had also extended the timeline for submission of financial results by listed entities for the quarter, half-year, or financial year-ended 31 March 2020 to 31 July 2020, due to the impact of the coronavirus pandemic.

SEBI further said that today’s announcement shall come into force with immediate effect and advised all stock exchanges to bring the provisions of this circular to the notice of all listed entities.

It has asked the stock exchanges to bring the provisions of the circular to the notice of all listed entities and also disseminate on their websites.

Meanwhile, SEBI’s move to relax the deadlines is expected to give more time to companies already struggling with operations part amid the pandemic.

In-line with the efforts to provide relief to the sagging businesses, Finance Minister Nirmala Sitharaman earlier announced to decriminalise some offences under the Companies Act.

The SEBI has also introduced new norms to give more fund-raising flexibility to stressed firms.

The amendments can help promoters get financial investors on board without losing control of the company.