The reduced TDS and TCS rate will be for specific payments such as payment for a contract, professional fees, interest, rent etc.

In order to provide more funds at the disposal of the taxpayers, the rates of Tax Deduction at Source (TDS) for non-salaried specified payments made to residents and rates of Tax Collection at Source (TCS) for the specified receipts has been be reduced by 25% of the existing rates.

The Finance Minister Nirmala Sitharaman said that, Payment for the contract, professional fees, interest, rent, dividend, commission, brokerage, etc. shall be eligible for this reduced rate of Tax Deduction at Source.

This reduction shall be applicable for the remaining part of the FY 2020-21 i.e. from tomorrow 14th May 2020 to 31st March, 2021.

The Finance Minister also said that, It will help to Rs 50,000 crores liquidity through TDS/TCS rate reduction.

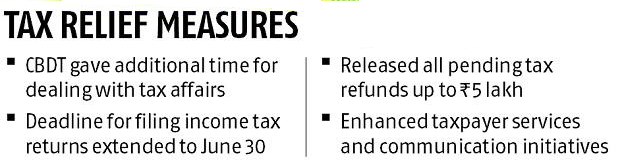

She also said that the income tax department has already cleared Rs 18,000 crore worth of refunds where the quantum due was up to Rs 5 lakh and instructed that all pending refunds to charitable trusts and non-corporate business and professions will be issued immediately.

TDS rate was not deducted on salaries, after considering various eligible deductions such as 80C of the salaried person. This had been done to ensure that the salaried individual did not bear the burden of paying higher taxes at the year end.

Move comes after a group of IRS created panic and tax policy uncertainty.

After rejecting “ill-conceived” suggestions by a group of Indian Revenue Services (IRS) officers, the Central Board of Direct Taxes (CBDT) directed officials not to keep any communication with assessees or issue scrutiny notices to them without the board’s approval.

According to it, any such notice would have an “adverse effect” on the assessees amid the coronavirus (Covid-19) pandemic.

These directives are part of the interim action plan for the first quarter (April-June) prepared by the direct tax board. It highlights certain areas which need immediate attention and preparedness until normalcy returns.

The move comes at a time when the tax department faced widespread criticism on a report prepared by a group of IRS officers. It had created panic and tax policy uncertainty at a time when India is already going through a difficult economic situation.

“Identification and preparedness regarding the issuance of notice under Section 148, which deals with income escaping and return filing in all eligible cases, should be done by June 30. However, these notices are to be issued only after getting fresh communication from the board in this regard,” said the CBDT note.

It added that due to the unprecedented situation arising out of Covid-19-induced social distancing and lockdown this year, a relatively short interim action plan has been issued.

Considering the current situation, we have been putting a slew of tax relief measures to mitigate the impact on business and even on household.

Any such communication may put pressure on the taxpayers and create unnecessary panic. A new system had already been put in place to make officials accountable for their communication with assessees.

However, during the lockdown, even such communication would not go without the board consent, said a CBDT official. Other than keeping no communication with assessees, the tax officials have been asked to centralise cases where searches took place in the financial year 2019-202.

This is because once lockdown is lifted, the officials would work on disposing them on merit.

Moreover, the CBDT asked officials to be prepared for tax demands in cases of international taxation, tax deduction at source and exemption-related charges.

The board wants the department to examine all pending demands, according to permanent account number (PAN) and assessment years.

It also removed demands which are creating duplication and are lying in the system. Besides, officials were asked to reconcile brought-forward cases, especially on TDS, based on the information available on the Traces portal for TDS units. The interim action plan also instructed officials to dispose of all applications concerning granting registration to charitable trusts received upto March 31.

Meanwhile, the direct tax board told its officials to upload manual orders on the systems, especially those under Section 263. It deals with appeals where the principal commissioner or commissioner may call for and examine the record of any proceeding. He or she may consider an order passed by the assessing officer to be erroneous, if it is prejudicial to the interests of the revenue.

Earlier, such registrations/approvals were granted without any specific expiry period unless specifically withdrawn by concerned tax authority. Under the new law introduced by Finance Act 2020 and effective from June 1, 2020, all such registrations/ approvals would now be issued with an expiry period of 5 years.

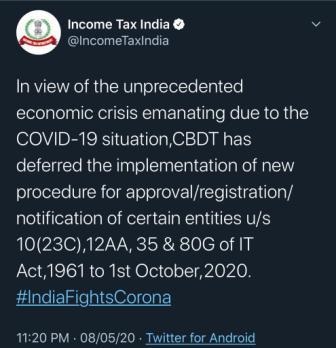

In a relief to religious trusts, educational institutions and other charitable institutions, the income tax department on Friday deferred by 4 months till October 1 the requirement of registration of these entities.

In a relief to religious trusts, educational institutions and other charitable institutions, the income tax department on Friday deferred by 4 months till October 1 the requirement of registration of these entities.

“In view of the unprecedented humanitarian and economic crisis, the CBDT has decided that the implementation of new procedure for approval/ registration/notification of certain entities shall be deferred to 1st October, 2020,” an official statement said.

Finance

Act 2020 prescribed substantial changes in law pertaining to

registration/approval of trusts and charitable institutions, whose

income are exempt under section 10(23C), Section 11 or for the purpose

of Section 80-G of the Act for tax deductible donations.

Earlier,

such registrations/approvals were granted without any specific expiry

period unless specifically withdrawn by concerned tax authority.

Under

the new law introduced by Finance Act 2020 and effective from June 1,

2020, all such registrations/ approvals would now be issued with an

expiry period of 5 years.

Further, all trusts/charitable institutions already having approval or registration were also supposed to file applications for renewal of there registration/approval within 3 months of new law coming into force, i.e. August 31, 2020.

Nangia

Andersen Consulting Shailesh Kumar said “in light of COVID-19 outbreak

and consequent lockdown, giving relief to the taxpayers, this timeline

has been deferred by 4 months. Thus, new law which was supposed to come

in effect from 01 June 2020 would now come in effect from 01st October

2020.

“All

existing trusts/ charitable institutions would now need to file

applications for renewal of their registrations/ approvals by December

31, 2020 instead of earlier August 31, 2020,” he added.

The

statement said various representations were received to the finance

ministry expressing concerns over the implementation of new procedure

from June 1, 2020 due to outbreak of coronavirus (COVID-19) and

consequent lockdown and there have been a number of requests to defer

the applicability of new procedure.

“This is a welcome move and provides expected relief in light of genuine hardships created by COVID-19. The entities benefited by this circular would be religious trusts, hospitals, educational institutions or other public charitable institutions created for welfare of public and allows exemption from income tax on account of their activities and charitable purpose,” Kumar added.

Consulting

firm AKM Global Tax Partner Amit Maheshwari said, “This is a welcome

clarification as in the absence of this extension, it was extremely

difficult to comply with these procedures. Several representations had

been made on this matter and this is indeed a welcome move.”

• An employee can change the option of tax structure at the time of filing the ITR • TDS will get adjusted accordingly

The Central Board of Direct Tax (CBDT) recently came out with a circular, offering clarifications for tax-paying employees on how they can migrate to the new concessional tax regime, which was announced in this year’s Union Budget.

The lower income tax rates under the new regime came to effect from April 1, 2020. However, there were many concerns raised on how employees can choose to opt between the old and regime.

In an April 13 release, the CBDT said employees, who do not have any income from a business, can opt for the new concessional tax slabs or the old regime by intimating the deductor (employer) through a declaration form.

The declaration will also help employers determine whether to deduct TDS as per the old regime or the new concessional rates.

Employees have an option to choose between the new tax regime and the old one. Experts have already said that each employee/taxpayer may opt for any of the two, based on investments.

Coming to the new slabs under the concessional tax regime, those earning Rs 2.5 lakh will have to pay no tax while people earning Rs 2.5-5 lakh will have to pay 5 per cent tax.

Individuals in the income bracket of Rs 7.5-10 lakh will pay 15 per cent tax. People earning over Rs 10-12.5 lakh will be taxed at 20 per cent and those earning Rs 12.5-15 lakh will pay 25 per cent taxes. Finally, people earning above Rs 15 lakh will pay 30 per cent tax under the concessional tax regime.

To sum up the clarifications: 1) Employees, who do not have any income from a business, can choose to inform their employer through a declaration if they want to opt for the new tax regime for deducting tax at source on TDS from salaries.

However, employees who do not submit any declaration to the employer will continue to be charged under the old regime as earlier.

2) The IT department also clarified that an employee can change the tax structure at the time of filing income tax and that the amount of TDS will be adjusted accordingly.

“The deductor shall compute his total income, and make TDS thereon in accordance with the provisions of section IISBAC of the Act. If such intimation is not made by the employee, the employer shall make TDS without considering the provision of section 11SBAC of the Act,” the CBDT notification said.

3) Another important clarification by the tax department was related to TDS. Once employees make their intention clear to opt for the concessional rates, it will remain the same for TDS purpose for the year without any scope of modification.

“It is also clarified that the intimation so made to the deductor (employee) shall be only for the purposes of TDS during the previous year and cannot be modified during that year,” it said.

“However, the intimation would not amount to exercising an option in terms of sub-section (5) of section 115BAC of the Act and the person shall be required to do so along with the return to be furnished under sub-section (1) of section 139 of the Act for that previous year. Thus, option at the time of filing of return of income under sub-section (1) of Section 139 of the Act could be different from the intimation made by such employee to the employer for that previous year.”

Infosys Nilekani gave GST Network presentation to Council.

Council ask Infosys to improve GST Network by July.

Filing to be mandatory for taxpayers over Rs 5cr of annual

turnover

Decides to extend deadline for filing of GSTR9 & GSTR9C

for FY18-19 till June 30, 2020,

GST Council to continue with 3B till September & defer the new return system.

Council defers the proposal on taxability of economic surplus of brand owners of alcohol for human consumption,

Reassures states towards payment of compensation dues,

Where Cancellation have been cancelled till March 14,

application for cancellation of revocation can be filed till March 31, 2020.

GSTR-1 to be made compulsory only for making B2B supplies,

exports & amendments

B2C & non-filers of GSTR-3B to be exempted from filing

GSTR-1

Before 10th for turnover greater than Rs 1.5 cr

Before 13th for turnover lesser than Rs 1.5 cr

GSTR-2A to be generated on 14th of every month

Council approves “Know your Supplier” Scheme

Major Reliefs:

Interest for delay in GST payment will now be charged on next cash liability under Section 50, to be applicable from July 2017

GST on mobile phones and specified parts was increased from 12% to 18%. This decision was taken to avoid difficulties due to the inverted duty structure.

All types of matches have been rationalised to a single GST rate of 12%. Till now, the handmade ones were taxed at 5% and the rest was taxed at 18%.

GST on Maintenance, Repair and Overhaul (MRO) service in respect to aircraft was reduced from 18% to 5% with full ITC.

All these rate changes will come into effect from 01 April 2020.

A new scheme called ‘Know your Supplier’ has been introduced so that the taxpayers are informed about the basic details of the suppliers with whom they transact or propose to conduct business.

Supplier can upload the Tax Invoices on real time basis in Anx-1.

Recipient can view his purchase Invoices on near real time basis.

Recipient can also view whether supplier has filed his return or not.

Supplier has to upload the Tax Invoices latest by 10th of Next Month.

However, recipient can claim ITC on missing invoices also subject to certain conditions.

In case, Invoice uploaded by the supplier in Anx-1, but RET-1 is not filed, uploading of invoices in Anx-1 will be treated as self-admitted liability and recovery proceedings will be initiated against the supplier, except in certain specified situations where recipient will be liable to pay.

Recipient has to pay the amount of ITC availed on missing invoices after specified period. (Missing invoices means, invoices not uploaded in Anx-1)

To find out missing invoices, Offline IT Tool will be provided for matching invoices in Anx-2 with invoices in the accounting system of recipient.

Payment of tax shall be discharged full at the time of filing of RET-1 or SAHAJ or SUGAM itself.

In case of Quarterly returns, tax shall be paid on monthly basis.

Recipient can do the following actions on the invoices appearing in Anx-2 (auto drafted Purchase Invoice):

Accept also called as locking

Reject (eg. Invoice not related to the recipient)

Pending

If no action is taken on a particular invoice, it will be deemed by the system as accepted and ITC will be available against these invoices.

Once invoice is accepted by the recipient, i.e., locked by the recipient, supplier cannot amend those invoices.

Locked Invoice should be unlocked by the recipient only, for making any amendment by the supplier.

Supplier will be able to issue Debit Note or Credit Note on locked invoices also. If credit/debit note is issued against any pending invoice, then system will club the credit/debit note with pending invoice.

Second set of 15 features (16-30 points) as PART-II:-

Missing invoices shall be reported in RET-1 of the current month.

System will calculate the interest automatically. Once the tax and interest is paid, the missing invoice will be clubbed with the monthly return to which it relates.

For amendments, separate Return Form is available.

Maximum 2 amendments return can be filed for any one month.

“NIL” Return can be filed by “SMS”.

Negative liability if any shall be carried forward to next month regular return.

Higher late fee for amendment return if change in liability is more than 10%

Shipping Bill details also should be entered in Anx-1 by the exporters.

If the shipping bill details are not available by the time of filing the return, the same can be entered later on also.

The export data then will be transmitted to ICEGATE portal for cross verification purposes.

Until the facility is ready to pull the data from ICEGATE portal, importers can avail ITC on imports and supplies from SEZ on self-declaration basis.

New concept of suspension of registration will be introduced. From the date of suspension till the date of cancellation, tax payer need not file returns and invoice uploading also will not be allowed.

HSN should be reported at 4 digit level in monthly return.

The tables in the return will be opened based on the profile of the tax payer.

For all return obligations offline utility tools are made available to make filing process as easy as possible.

In the union budget 2020, the following section 115BAC shall be inserted in the Income Tax Act, with effect from the 1st day of April, 2021, with new income tax slabs and lower rates. These income tax rates are optional and are available to those who are willing to forego some exemptions and some deductions.

Direct Taxes

1. Tax rate reduced for new companies to 22% and for manufacturing companies 15%

2. New simplified personal tax regime for Individual tax payers. The revised slab can be availed if they do not claim deductions and certain exemptions.

For income :

Upto 5,00,000 nil

Rs 5,00,000 -7,50,000: 10%

Rs 7,50,000 – 10,00,000 : 15%

Rs10,00,000 – Rs 12,50,000 20%

Rs 12,50,000- Rs 15,00,000 : 25%

More than Rs 15,00,000 : 30%

3. Companies not required to deduct dividend distribution tax and will be taxed only in the hands of the recipient. Parent company to be allowed deduction of dividend received subsidiary

4. Concessional tax rate of 15% extended to power generation companies

5. Investment made in Infrastructure and other specified sectors

6. Tax rate of 194LC at 5% for interest payment to non resident in respect of money borrowed or bond issued upto June 30,2023 and for 194LD at 5% for interest on borrowing from foreign institutional or qualified investor and municipal bonds

7. Interest payment on bonds listed on exchange by ILFS – 4%

8. Option to Cooperative societies to pay tax at 22% with no exemption or deduction. Exempt from alternative minimum tax

9. Affordable housing tax breaks extended by one year. Additional 1.5 lakhs tax benefit on interest paid on affordable housing loans to March 2021

10. Turnover threshold for tax audit raised to Rs 5 crore from Rs 1 crore

11. 100% tax concession to sovereign wealth funds on investment in infra projects

12. Income from Charitable institutions fully exempt from taxation. Donation to such institution allowed as deduction.

13. Registration of charity institutions to be made completely electronic, donations made to be pre-filled in IT return form to claim exemptions for donations easily.

14. Faceless appeals against tax orders on lines of faceless assessments

15. For tax payers who have appeals pending only disputed tax is to be paid by tax payer and no interest or penalty if the same is paid within March 31,2020. Post March 31,2020 certain amount levied uptill June 30,2020

16. Startup ESOP taxes deferred by 5 years Other Areas

1. New scheme to provide subordinate debt to MSME

2. Decriminalise some norm violations in Companies Act

3. Increase the bank deposit insurance from Rs 1 lakh to Rs 5 lakh

4. New system for instant allotment of PAN

5. A new scheme NIRVIK to be launched this year itself for exporters

6. A debt ETF consisting of government securities will be launched.

7. For NBFCs and HFCs, liqduity constraints will be addressed.

8. FPI Limit in corporate bonds will be raised to 15% from 9%.

9. LIC to be listed at stock exchanges

Two important changes in Income tax (TDS/TCS)

— TCS to be collected by seller whose turnover exceeds Rs. 10 cr. In previous year from each buyer on amount exceeding 50 lacs @0.1% for sale of goods.

-TDS rate u/s 194J for technical payment changed from 10% to 2% to avoid litigations in respect of 194J Vs 194C

First 15 features (1-15 points) as PART-I:-

First 15 features (1-15 points) as PART-I:- In the union budget 2020, the following section

In the union budget 2020, the following section