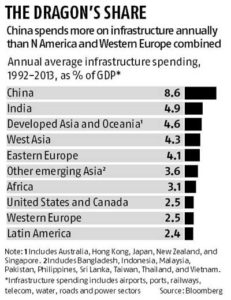

Despite a crying need for better infrastructure, investment in it has actually fallen in 10 major economies since the financial crisis, including the US, according to a new study by the McKinsey Global Institute. Meanwhile, China is still going gangbusters on roads, bridges, sewers, and everything else that makes a country run.

“China spends more on economic infrastructure annually than North America and Western Europe combined,” according to the report published Wednesday.

Economists around the world have been arguing that now is a great time to invest in infrastructure because interest rates are super-low and the global economy could use the spending jolt. “Is anyone proud of Kennedy airport?” Harvard University economist Lawrence Summers likes to ask.

The MGI report cites 10 countries where infrastructure spending fell as a share of gross domestic product from 2008 to 2013: the US, UK, Italy, Australia, South Korea, Brazil, India, Russia, Mexico, and Saudi Arabia. The study counts 11 economies, but that’s because it lists the European Union as a separate entity.

In contrast to the widespread declines, the institute says, infrastructure spending grew as a share of GDP in Japan, Germany, France, Canada, Turkey, South Africa and China. The chart from the MGI report shows China’s strength in infrastructure spending. Its bar is the highest. There’s such a thing as too much infrastructure spending, of course. At current rates of investment, China, Japan, and Australia are likely to exceed their needs between now and 2030, the McKinsey & Co-affiliated think tank says. To fund more public infrastructure, the report favours raising user charges such as highway tolls, among other measures.

To encourage more private investment in infrastructure, MGI argues for increasing “regulatory certainty” and giving investors “the ability to charge prices that produce an acceptable risk-adjusted return.”

The possibility of their investing, either directly in projects or through the National Investment and Infrastructure Fund (NIIF) that we have created, were both discussed,” he told reporters at the Indian High Commission in London.

Amid fears of the global economy edging close to recession, India and UK have agreed to open up trade and markets to support growth, carry out structural reforms and address issues related to cross-border tax evasion.

After talks between India’s Finance Minister Arun Jaitley and UK Chancellor of the Exchequer George Osborne, the two nation’s agreed to boost economic ties particularly in areas of infrastructure and financial services and renewed pledge for autonomical exchange of tax information from 2017.

“From the Indian point of view, we were extremely interested in having the British investors look at infrastructure investments in India for which various possibilities were discussed,” Jaitley said after the talks.

India, he said, is “extremely keen that large British companies, particularly involved in infrastructure financing, start investing in Indian infrastructure”.

The two nations will work together for developing an India-UK partnership fund under the umbrella of National Investment and Infrastructure Fund (NIIF) recently created in India.

“This fund will seek to increase flows of private sector capital and expertise alongside multilateral support into Indian infrastructure,” a joint statement issued after talks said.

The world’s fifth largest economy will work on development of smart cities in India. New Delhi is also looking at London for issuance of rupee-denominated bonds to get UK investors to fund its infrastructure projects.

“The possibility of their investing, either directly in projects or through the National Investment and Infrastructure Fund (NIIF) that we have created, were both discussed,” Jaitely told reporters at the Indian High Commission here.

With the IMF warning of global economy being close to recession with 3.4 per cent growth this year, the two sides said they “remain concerned that global growth is falling short of expectations and that the risks to the global outlook have increased”.

“In this regard we stand ready to take the necessary steps to open up trade and markets to support growth and jobs, and agree on the importance of structural reforms and pursuing credible fiscal policies,” the joint statement said.

The joint statement talked about advancement of cooperation in a range of sectors including infrastructure financing, addressing issues of cross-border tax evasion/ avoidance besides opening up of the Indian legal sector to foreign lawyers.

“The UK and India share a common commitment to address cross-border tax evasion and avoidance. Both sides have committed to the Common Reporting Standards (CRS) on Automatic Exchange of Tax Information and will begin exchange in 2017,” the statement said.

“We call on other countries to meet the commitments they have made and to implement the new standard on time,” it said.

During the talks, which included senior representatives from Finance Ministries, Central Banks and key regulators of both countries, the two leaders discussed ways to strengthen the Indo-UK existing economic partnership in order to further boost trade and investment, and to build on the success of Prime Minister, Narendra Modi’s recent summit with his British counterpart David Cameron in the UK.

“Given the fact that even in a somewhat difficult global scenario, India is managing a reasonable growth rate, this is one of the better options that investors have and that kind of a sentiment gets really echoed in the meetings with the investors that we had. Of course, the investors are also keenly watching which way our reform process in India goes,” Jaitley said.

The two nations agreed to work together on building commercial and regualtor-to-regulator links that can underpin further fintech growth in both countries.

“The UK and India agreed to renew the existing mandate of the India-UK Financial Partnership, and building on the re-establishment of the CEO Forum,” the statement said, adding that potential areas of interest for the India-UK Financial Partnership could be reinsurance, international use of the rupee, role of financial technology, financial inclusion, investor protection and green finance.

“The global economy is facing serious challenges and therefore the estimates of global growth also have been repeatedly lowered. Compared to how various countries across the world have been doing, India’s growth rate despite these challenges is probably the highest in the world among major economies,” Jaitley said, in reference to his meetings with investors at Goldman Sachs and London Stock Exchange.

As a follow up on Prime Minister Modi’s announcement during his UK visit last November on the listing of Rupee bonds in London, the minister said, “the UK is very keen for these to be listed in London and broadly the economic and financial dialogue was carried further”.

During the dialogue, the two sides recognised that as the leading financial centre in the world and in the view of successful issuance of Masala bonds issued by the International Finance Cooperation last year, London will be an attractive location for issuance of rupee-denominated bonds.

“The bonds, which were first announced during the visit of Prime Minister Modi to the UK in November, illustrate the crucial role that the UK’s capital markets can play in an enhanced economic relations relationship with India, with UK investors providing financing for the transformation of India’s infrastructure and continued rapid economic growth,” the statement said.

India and the UK also agreed that the development of deeper markets in rupee-linked products, and the increasingly sophisticated relationship between the Indian and UK financial sectors, are important underlying factors in fostering an enduring economic and financial partnership.

Both sides agreed to continue working closely on the development of smart cities in India.

“We will continue to build on and further embed the existing Technical Assistance Partnerships that were announced during Prime Minister Modi’s recent visit to the UK, and to continue working together on research collaboration and other measures to support India’s 100 Smart Cities programme,” the statement said.

While noting the strength of the economic outlook for both countries, the two sides expressed concern that global growth is falling short of expectations and that the risks to the global outlook have increased.

“In this regard we stand ready to take the necessary steps to open up trade and markets to support growth and jobs, and agree on the importance of structural reforms and pursuing credible fiscal policies in order to raise living standards,” it said.

India and the UK also agreed to work together with the aim of developing an Indo-UK partnership fund under the umbrella of the NIIF. The fund will seek to increase flows of private sector capital and expertise alongside multilateral support into Indian infrastructure.

The working group to be established will report back within the course of 2016 on a proposed fund strategy and delivery approach, the statement said.

“As part of this, India and the UK also both recognise the importance of identifying the sector or sectors where there is greatest potential for developing sustainable project pipelines, and of developing a supportive institutional environment for investment and delivery,” it said.

A deadline for comments on the draft guidelines to determine the tax residency of a foreign company has been extended to January 9.

The government felt the need to determine a company’s place of effective management due to lack of detail in the Income Tax Act leading to the possibility of tax avoidance.

“Representations requesting for extension of the last day for submitting comments and suggestions, have been received and considered,” according to a government statement announcing the extension of the deadline for comments on the issue, earlier slated for January 2.

The Place of Effective Management (POEM) of a company, as the concept was called, was introduced in the Finance Act, 2015 to determine the tax residency of a foreign company.

The draft guidelines for what defines a company’s place of effective management, released on December 23, defines the POEM as “a place where key management and commercial decisions that are necessary for the conduct of the business of an entity as a whole are, in substance made.”

“Section 6(3) of the Income-tax Act, 1961, prior to its amendment by the Finance Act, 2015, provided that a company is said to be resident in India in any previous year, if it is an Indian company or if during that year, the control and management of its affairs is situated wholly in India. This allowed tax avoidance opportunities for companies to artificially escape the residential status under these provisions by shifting insignificant or isolated events related with control and management outside India,” according to draft guidelines issued by the Central Board of Direct Taxes.

“As per the amendment brought in by the Finance Act, 2015 a foreign company will be regarded as a tax resident of India, if its POEM in that year is in India,” according to a report by Deloitte and CII.

According to the Deloitte report, there is ambiguity around some of the provisions in the guidelines, such as the duration for which a company has India as a place of effective management. “A question may still arise that for a foreign company to be resident in India, is it necessary that the POEM should be situated in India throughout the financial year under consideration or mainly in India.

Similarly, the term “key management and commercial decisions” in the definition of POEM seems to be causing some confusion.

“Unlike, for instance, the UK, India does not define the term ‘key management and commercial decisions’ and therefore these are undefined and subjective.

In the UK, judicial precedents and tax rules lay emphasis on whether directors/officers taking major decisions are independent, are empowered to take these or whether such directors/officers are acting under the influence or direction of shareholders,” Mr.Alex Postma, Leader–Global and EMEIA International Tax Services, EY had said in a note.

Enterprises have become increasingly mobile and technology and connectivity are as important as never before in their global competence. This poses risks that a travelling executive may create significant unforeseen tax burdens in India,” Mr. Postma added in his note.

The finance ministry is streamlining safe harbour rules and advance agreements, two mechanisms to determine the price of services rendered by a multinational to its subsidiary in India.

Safe harbour rules – directives on margins the tax authorities should accept for the transfer price declared by an assessee – have drawn a tepid response since they were introduced a couple of years ago. There is also a huge backlog in advance pricing agreements (APAs), an ahead-of-time understanding between a taxpayer and the tax authority on an appropriate transfer pricing methodology.

ALIGNING INDIAN TAXATION WITH BEST PRACTICES

Safe harbour rules

Government looking at lowering safe harbour margins to make it attractive for companies to opt for it

Government to make safe harbour definition unambiguous bringing in more clarity

Advance Pricing Agreement

With close to 550 cases pending, government looking at expediting clearances through:

Sector-specific approach to cases

Increasing manpower and filling up vacancies

The move would simplify the tax regime, reduce litigation and help improve the business environment, a finance ministry official said.

The steps will involve lowering the margins in safe harbour rules and definitions will be reworked to remove ambiguities. India announced the safe harbour rules in 2013, but the high margins of up to 25 per cent on total operational profits have made it unattractive for companies to use them.

“We are addressing issues related to transfer pricing to align it with best practices. We are revising the safe harbour rules that will include revisiting the definition and revising the margins, considered high by companies,” said a tax official.

Information technology (IT) and information technology-enabled services (ITeS) companies with transactions of up to Rs 500 crore have a safe harbour operating margin of 20 per cent and those with transactions above Rs 500 crore have a margin of 22 per cent. Knowledge process outsourcing companies have a safe harbour operating margin of 25 per cent.

Experts argue there is ambiguity in the definition of IT, ITeS and knowledge process outsourcing companies with a lot of overlap. Moreover, the margins decided in tribunals or in advance pricing agreements turn out much lower, ranging between 15 and 18 per cent.

“The definitions under the safe harbour rules are fuzzy and sometimes overlap, creating confusion over what rate should apply and which company will fall under which sector. We are expecting clarity on the definition,” said Rahul Garg, leader, direct tax, PwC.

Manisha Gupta, partner, Deloitte Haskins & Sells, said the safe harbour margins were high. “The government agrees to far lower rates at tribunals and in advance pricing agreements,” she said.

The lowering of safe harbour rates will ease the advance pricing agreement backlog. The government introduced the advance pricing scheme in 2012 and there are over 500 applications pending.

“We are considering sector-wise handling of cases by officers to expedite decisions,” the tax official said. “We have already made a request for an increase in manpower to clear the backlog. We expect a decision soon,” he added.

India has the highest incidence of transfer pricing litigation worldwide. The number of cases scrutinised has quadrupled from 1,061 in 2005-06 to 4,290 in 2014-15.

Among measures recently introduced, the government said an officer would be assigned not more than 50 important and complex transfer pricing cases. Officers typically audit more than 70 cases at a time.

Besides, the tax department has incorporated range and multi-year data in transfer pricing calculations to bring Indian laws in line with international practices. Earlier, single-year data and the arithmetic mean were used to arrive at transfer pricing.

Earlier this year, the finance ministry allowed rollback advance pricing agreements so that multinational companies could settle taxes for previous years as well.

“The burden on tribunals, high courts, Supreme Court and even on the APA team can be substantially reduced if the Indian government revamps the safe harbour rules (that is, devising calibrated and more reasonable margins for the sector consistent with the margins finally arrived at post-tribunal orders/MAP/APA and providing clarifications on what constitutes software development activities, KPO, contract R&D,” said a Deloitte & Taxsutra report on transfer pricing.

Approximately over 40 per cent of APA applications are from the IT/ITeS sector. Up to September 2015, more than 575 APA applications have been filed with the APA authorities. Fourteen of these APAs have been concluded, of which 12 are unilateral and two bilateral (with Japan and the UK).

Despite a crying need for better infrastructure, investment in it has actually fallen in 10 major economies since the financial crisis, including the US, according to a new study by the McKinsey Global Institute. Meanwhile, China is still going gangbusters on roads, bridges, sewers, and everything else that makes a country run.

Despite a crying need for better infrastructure, investment in it has actually fallen in 10 major economies since the financial crisis, including the US, according to a new study by the McKinsey Global Institute. Meanwhile, China is still going gangbusters on roads, bridges, sewers, and everything else that makes a country run. In contrast to the widespread declines, the institute says, infrastructure spending grew as a share of GDP in Japan, Germany, France, Canada, Turkey, South Africa and China. The chart from the MGI report shows China’s strength in infrastructure spending. Its bar is the highest. There’s such a thing as too much infrastructure spending, of course. At current rates of investment, China, Japan, and Australia are likely to exceed their needs between now and 2030, the McKinsey & Co-affiliated think tank says. To fund more public infrastructure, the report favours raising user charges such as highway tolls, among other measures.

In contrast to the widespread declines, the institute says, infrastructure spending grew as a share of GDP in Japan, Germany, France, Canada, Turkey, South Africa and China. The chart from the MGI report shows China’s strength in infrastructure spending. Its bar is the highest. There’s such a thing as too much infrastructure spending, of course. At current rates of investment, China, Japan, and Australia are likely to exceed their needs between now and 2030, the McKinsey & Co-affiliated think tank says. To fund more public infrastructure, the report favours raising user charges such as highway tolls, among other measures.