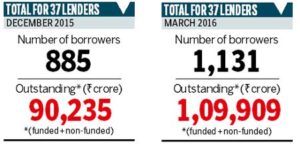

More than a thousand borrowers have outstandings that are substantially larger than the amounts sanctioned to them by banks, data sourced from Reserve Bank of India (RBI) shows. The total outstandings of 1,131 borrowers, at Rs 1,09,909 crore, were 150% more than the amount sanctioned, as on March 2016, data accessed by FE reveal. At the end of December 2015, the outstandings were Rs 90,235 crore.

More than a thousand borrowers have outstandings that are substantially larger than the amounts sanctioned to them by banks, data sourced from Reserve Bank of India (RBI) shows. The total outstandings of 1,131 borrowers, at Rs 1,09,909 crore, were 150% more than the amount sanctioned, as on March 2016, data accessed by FE reveal. At the end of December 2015, the outstandings were Rs 90,235 crore.

Bankers and ex-bankers that FE reached out to attributed the pile-up in outstandings to short-term requirements of borrowers that were met by banks to help them tide over a cash crunch. Overdue interest, they said, could be another cause for the high outstandings. One senior banker observed that there were occasions when the capacity of the borrower to repay the additional amount was not assessed properly. “At times, limits get exceeded without a proper assessment of the customer’s ability to service the loan,” he said.

A former executive director of a public sector bank said one reason for the actual outstanding exceeding the permitted limits was that lenders tended to sanction ad hoc non-funded letters of credit (LC) even before the limits were okayed by the consortium. “Sometimes ad hoc LCs are opened for amounts which are bigger than those agreed to by the consortium. Since consortiums take anywhere between six months and a year to sanction limits, the money is disbursed since business cannot wait,” he explained, adding that such loans serve as working capital.

A former chairman of a state-owned bank said if the customer was unable to service the loan, the interest piled up pushing up the outstanding amount. “If the interest hasn’t been paid for three or four years, the amounts can become large,” he pointed out.

An RBI document on the Central Repository of Information on Large Credits notes that if outstanding loans exceed 150% of the limit, a “warning message should be displayed to the user on generation of the instance document”.

Ashvin Parekh, managing partner, Ashvin Parekh Advisory Services, observed the main reason for the outstandings surpassing the sanctions was “temporary accommodation and loans against receivables”.

Parekh explained that at times borrowers approached banks for funds to be able to take delivery of imports. “The customer promises to pay back the amount from receivables so bankers do accommodate such requests,” he said.

Total non-performing assets (NPAs) of the banking system stood at Rs 5.8 lakh crore at the end of March 2016 and total provisions were Rs 1.43 lakh crore.

The central bank has been trying to help banks tackle bad loans by allowing them to convert debt into equity and more recently into convertible redeemable preference shares. However, banks have not been able to find buyers for any of the assets under strategic debt restructuring scheme.

FE had earlier reported that bank loans that aren’t NPAs just yet but could turn toxic amount to over Rs 6 lakh crore or close to 9% of total advances, citing RBI data. The total troubled loans of Rs 6,24,119 crore at the end of December 2015 were 9% higher than the Rs 5, 73,381 crore at the end of June 2015.

While Rs 3,06,180 crore worth of loans were classified in the SMA-1 category where repayments are overdue between 30 and 60 days, another Rs 3,17,939 crore was in the SMA-2 category where repayments are overdue between 60 and 90 days. These Special Mention Accounts follow a fiat from the RBI in 2014 asking banks to put in place a mechanism to red-flag troubled loan accounts early in the day so that these could be dealt with speedily. If the loan is not serviced after 90 days it must be classified as an NPA.