It has become a mandatory process to link your PAN with Aadhaar. This is an important process because this will allow your income tax returns to be processed. Linking of your PAN with Aadhaar is also required if you are carrying out banking transactions for amount of Rs.50,000 and above.

In order to provide some more time to tax payers, Central Board of Direct Taxes (CBDT) has extended the date for linking the PAN and Aadhaar to June 30,2023.

* * * * * * * * * * *

Government of India

Ministry of Finance

Department of Revenue Central Board of Direct Taxes

New Delhi, 28th March, 2023

PRESS RELEASE

Last date for linking of PAN-Aadhaar extended

In order to provide some more time to the taxpayers, the date for linking PAN and Aadhaar has been extended to 30th June, 2023, whereby persons can intimate their Aadhaar to the prescribed authority for Aadhaar-PAN linking without facing repercussions. Notification to this effect is being issued separately.

Under the provisions of the Income-tax Act, 1961 (the ‘Act’) every person who has been allotted a PAN as on 1st July, 2017 and is eligible to obtain Aadhaar Number, is required to intimate his Aadhaar to the prescribed authority on or before 31st March, 2023, on payment of a prescribed fee. Failure to do so shall attract certain repercussions under the Act w. e.f. 1st April, 2023. The date for intimating Aadhaar to the prescribed authority for the purpose of linking PAN and Aadhaar has now been extended to 30th June, 2023.

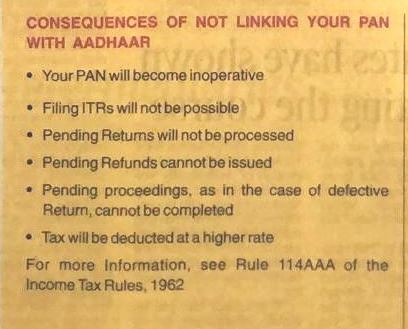

From 1st July, 2023, the PAN of taxpayers who have failed to intimate their Aadhaar, as required, shall become inoperative and the consequences during the period that PAN remains inoperative will be as follows:

(i) no refund shall be made against such PANS;

(ii) interest shall not be payable on such refund for the period during which PAN remains inoperative; and

(iii) TDS and TCS shall be deducted / collected at higher rate, as provided in the Act.

The PAN can be made operative again in 30 days, upon intimation of Aadhaar to the prescribed authority after payment of fee of Rs 1,000.

Those persons who have been exempted from PAN-Aadhaar linking will not be liable to the consequences mentioned above. This category includes those residing in specified States, a non-resident as per the Act, an individual who is not a citizen of India or individuals of the age of eighty years or more at any time during the previous year.

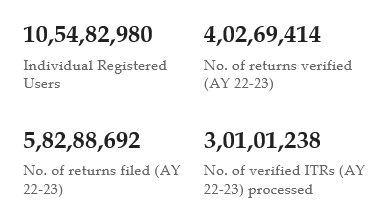

it is stated that more than 51 crore PANS have already been linked with Aadhaar till date.

PAN can be linked with Aadhaar by accessing the following link

https://eportal.incom et ax. goy ntiecifoservices/#/pre-login/b nk-aadhaar

(Surabhi Ahluwaiia)

Pr. Commissioner of Income Tax

(Media & Technical Policy) &

Official Spokesperson, CBDT