The overall objective of the LFAR should be to identify and assess the gaps and vulnerable areas in the business operations, risk management, compliance and the efficacy of internal audit and provide an independent opinion on the same to the Board of the bank and provide their observations

The Reserve Bank on Saturday came up with revised long format audit report (LFAR) norms with a view to improving efficacy of internal audit and risk management systems.

The LFAR, which applies to statutory central auditors (SCA) and branch auditors of banks, has been updated keeping in view the large scale changes in the size, complexities, business model and risks in the banking operations, the RBI said.

The Chairman / Managing Director / Chief Executive Officer All Scheduled Commercial Banks (Excluding RRBs) All Local Area Banks All Small Finance Banks and All Payment Banks

Madam /Dear Sir,

Long Form Audit Report (LFAR) – Review

Please refer to RBI circular No. DBS.CO.PP.BC.11/11.01.005/2001-2002 dated April 17, 2002 on revision of Long Form Audit Report (LFAR).

2. Keeping in view the large scale changes in the size, complexities, business model and risks in the banking operations, a review of the LFAR formats, in consultation with the stakeholders, including the Institute of Chartered Accountants of India (ICAI), was undertaken and it has been decided to make the following changes.

3. The format of LFAR, as mentioned below, have been revised:

Annex I for Statutory Central Auditors (SCA)

Annex II for Branch Auditors

An Appendix as part of Annex II for the specialized branches and

Annex III on Large / Irregular / Critical accounts for branch auditors.

The revised formats are enclosed.

4. The revised LFAR formats are required to be put into operation for the period covering FY 2020-21 and onwards. The mandate and scope of the audit will be as per this format and if the SCA feels the need of any material additions, etc., this may be done by giving specific justification by the SCA and with the prior intimation of the bank’s Audit Committee of Board (ACB).

5. Regarding other operational issues relating to submission of LFAR, we further advise as under:

Timely receipt of LFARs from the auditors should be ensured;

The LFAR on the bank, after due examination, should be placed before the ACB / Local Advisory Board of the bank indicating the action taken/proposed to be taken for rectification of the irregularities, if any, mentioned therein; and

A copy each of the LFAR (i.e. for the bank / all Indian Offices of foreign bank as a whole) and the relative agenda note, together with the Board’s views or directions, should be forwarded to the concerned Senior Supervisory Manager (SSM) in the Department of Supervision, Reserve Bank of India within 60 days of submission of the LFAR by the statutory auditors.

6. The LFAR format and other instructions issued vide RBI circular No. DBS.CO.PP.BC.11/11.01.005/2001-2002 dated April 17, 2002 stand repealed.

Due to the widespread of COVID-19 and social distancing norms and consequential restrictions linked thereto, MCA has received several representations to allow companies to hold their Annual General Meeting for the financial year ended on 31st March, 2020 beyond the statutory period provided in section 96 of the Companies Act, 2013.

The matter was examined and MCA clarified vide General Circular No. 20/2020, dated 05.05.2020 regarding holding of AGM through video conferencing (VC) or other audiovisual means (OAVM), the companies which were unable to hold their AGM were advised to prefer applications for extension of AGM at a suitable point of time before the concerned Registrar of Companies under Section 96 of the Act.

MCA, in this regard, vide General Circular no. 28/2020 dated 17th August,2020 has issued clarification on extension of Annual General Meeting for the financial year ended as at 31.03.2020.

Provisions of holding Annual General Meeting (AGM) as per Companies Act, 2013.

According to section 96 of the Companies Act, 2013, companies are to hold their Annual General Meeting (AGM) within a period of 6 months from the date of closing of the financial year and companies which are to hold their first AGM shall be held within a period of 9 months from the date of closing of the financial year of that company.

The Ministry once again reiterated that the companies which are unable to hold their AGM for the financial year ended on March 31, 2020, despite availing the relaxations provided in MCA General Circular No. 20/2020 ought to file their applications in E-Form GNL-1 for seeking an extension of time in holding of AGM for the financial year ended on March 31, 2020, with the concerned Registrar of Companies on or before 29th September, 2020.

Also the Ministry has directed Registrars of Companies to consider all such applications (Filed in E-Form GNL-1) liberally in view of the hardships faced by the stakeholders and to grant an extension for the period as applied for (up to three months i.e. 31st December) in such applications.

Procedure to file Application seeking extension of time for holding Annual General Meeting:

1.

Chairman /Director of the company shall call for a meeting of Board of Director for which a notice must be send at least 7 days before holding of Meeting of Board.

2.

Convene a Board Meeting on the specified date.

3.

Pass a resolution for extension of time limit for holding annual general meeting specifying the due reason for extension of AGM.

4.

File an application to Registrar of Companies in E-Form No. GNL-1. (Reason for not holding AGM, along with other necessary information to be provided)

5.

Attach the Certified true copy of the Board Resolution in E-Form-GNL-1.

6.

The registrar will examine the application on the specific grounds and grant an extension.

Obtain the Certificate of Grant of extension in holding Annual General Meeting of theCompany.

Convening of Annual General Meeting in extended period:

Once the extension is granted, the company may convene the Annual General Meeting of the Company within the period as allowed by the Registrar of Companies.

The Income Tax department on Friday said it has issued refunds worth Rs 88,652 crore to over 24 lakh taxpayers so far this fiscal.

This include personal income tax (PIT) refunds amounting to Rs 28,180 crore issued to over 23.05 lakh taxpayers and corporate tax refunds amounting to Rs 60,472 crore to over 1.58 lakh taxpayers during this period.

“CBDT has, so far, issued refunds of over Rs 88,652 crore to more than 24.64 lakh taxpayers from 1st April, 2020 onwards.

Income tax refunds of Rs 28,180 crore have been issued in 23,05,726 cases & corporate tax refunds of Rs 60,472 crore have been issued in 1,58,280 cases,” the Income Tax department tweeted.

The Central Board of Direct Taxes (CBDT) is the apex decision-making body in direct tax matters, administers personal income tax and corporate tax.

The government has emphasized on providing tax related services to taxpayers without any hassles during COVID-19 pandemic and to that end has been clearing up pending tax refunds.

Prime Minister Narendra Modi announced several tax measures on the eve of India’s Independence Day last week honouring the honest tax-paying citizen.

You will now have to file your income-tax (IT) return or pay higher percentage of tax deduction at source if you make certain spends in a year.

If you spend Rs 20,000 a year as hotel expenses, property tax or even a health insurance premium, then your transactions would be reported. Similarly, if your annual rent exceeds Rs 40,000, life insurance premium is at least Rs 50,000 or electricity bills of Rs 1 lakh or more during a financial year, then you would be answerable to the taxman either via notices or through mandatory filing of returns.

The motive of the move is to check whether your spending is in line with the income you actually disclose in your return.

The Government has been shunting all doors to not only reduce the number of all cash transactions, but also increase the number of returns filed. The new move to collect spending data is another tool in the armoury to curb tax evasion.

Are transactions tracked currently?

The existing income tax rules mandate financial institutions such as banks, mutual fund houses, share registrar and transfer agents,sub-registrars to report high value transactions exceeding a specified limit during a financial year to the Income Tax Department.

So, a bank has to report details of every account holder who makes cash deposits of more than Rs 10 lakh in a year in a savings account or makes a payment of more than Rs 2 lakh from his credit card in a year. Similarly, asset management companies are required to report details of all the investors who invest more than Rs 2 lakh in a single mutual fund scheme. Now not only your investments and financial transactions, but also your specific spends will be tracked.

Do I have to inform the government of all my spends?

No. You do not have to go out of your way to inform the government or anyone, unless asked for in the tax return forms. Your purchases and expenses beyond a threshold will be mentioned in the returns of the hotel, electronic goods seller, artist, school, ceramic supplier or the Registrar in the case of property purchase, apart from banks, mutual fund houses, life and general insurance companies.

The details mapped to you would be reflected in your individual tax statement or Form 26AS. This form would be available on your income-tax website login.

The moment your spends in any of the high-spend categories mentioned, exceed the respective threshold limits, your Form 26AS would capture it. In other words, you have to file your tax returns.

Non-filing of ITR may have severe consequences for a person, who is otherwise required to file an ITR. Apart from attracting interest, late fee and penalty, wilful non-filing of ITR may also attract criminal prosecution.

The new move has been part of the government’s move to widen the tax net and get more and more people to file their income tax returns. A total of about 55 lakh or 80 per cent of the total returns are filed by people having an income of up to Rs 5 lakh, as per the Central Board of Direct Tax’s numbers as of July 31, 2020.

Only 5,066 individuals, who have an income above Rs 1 crore file returns, accounting for 0.73 per cent of the total individual tax returns.

Taxpayers would not need to mention their high-value transactions in their income tax returns, said officials in the know of the matter, but added that broadening the scope of reporting financial transactions by third parties had become vital since taxation was moving towards a faceless approach.

It’s clarified that only third parties would report high-value transactions to the income tax department as per the Income Tax Act. The information would be used to identify people who are not paying up due taxes, and not for examining affairs of honest taxpayers.

“The information will be used to identify those who are either not filing the returns or the income disclosed in the returns are not proportionate to the pattern of expenditure reported in the statement of financial transactions (SFTs),” the official said.

Data analytics and artificial intelligence will be used for this, instead of manual intervention.

Terming the method as most ‘non-intrusive’, the official said it would be used for identifying those who spend big money on business class air travel, foreign travel and expensive hotels or send their children to expensive schools, but do not pay taxes, claiming their income to be under Rs 2.5 lakh a year.

Prime Minister Narendra Modi flagged this very issue on Thursday, and asked people to pay their fair share of taxes, given that the country’s tax base was relatively small.

“Only 1.5 crore people pay taxes in a country of 130 crores,” he pointed out while launching a taxpayer’s charter and faceless assessment, aimed at improving transparency in tax administration.

“No doubt, the third-party reporting of high-value transactions made by such non-filers would allow the department to nudge such persons to file their returns and pay their due tax,” the official said.

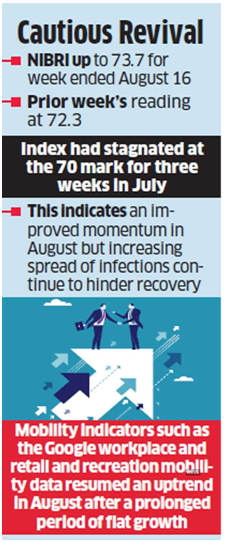

The Nomura India Business Resumption Index inched up to 73.7 for the week ending August 16, over the previous week’s reading of 72.3. This came after the NIBRI, a weekly tracker of the pace at which economic activity normalises, stagnated at the 70-mark for three weeks through July.

The economy sustained an increasing pace of recovery through August so far after a prolonged period of plateauing trends in July, according to a Nomura note on Monday.

The Nomura India Business Resumption Index (NIBRI) inched up to 73.7 for the week ending August 16, over the previous week’s reading of 72.3.

This came after the NIBRI, a weekly tracker of the pace at which economic activity normalises, stagnated at the 70 mark for three weeks through July.

While this indicated an improved momentum in August over the moderation in July, the rising spread of infections continued to hinder recovery.

“Nevertheless, the recovery is uneven, and the risk of reversal in momentum from a second wave of COVID-19 cases joining a ‘rolling wave’ in traditional safer states (in the south and the east) remains high,” the note said.

Mobility indicators such as the Google workplace and retail and recreation mobility data resumed an uptrend in August after a prolonged period of flat growth, Nomura said.

However, this was still materially below pre-pandemic levels, it added.

There was a steady pick up in the labour participation rate 42.2% as against 40.6% in the previous week.

On the other hand, the unemployment rate showed a steady uptrend rising to 9.1% compared to the 8.2% recorded last week, which grew from 7.2% reported the week before that.

The deterioration was spread both over rural and urban areas, the note said.

Power demand also showed a steady trend albeit in the opposite direction with a steep weekly contraction of 6.4% over the 0.8% contraction of the week earlier, it said.

Faceless e-assessment will have no human interface and it’s purpose will be to eliminate instances of “undesirable practices” on the part of tax officials.

The Central Board of Direct Taxes (CBDT) on Thursday revised the ‘E-assessment Scheme, 2019’ notified on September 12, 2019. The Government notified that now, the e-Assessment scheme shall be called Faceless Assessment.

Now, the National e-Assessment Centre shall intimate the assessee for the conduct of faceless assessment in case wherein notice has been issued by AO.

The Board has also extended its scope to cover best judgment assessments.

E-Assessment was a roadway towards a paperless, faceless assessment stripping away at bureaucratic layers. E-Assessment was earlier tried and tested by the Income-tax Department, before going forth with the E-Assessment Scheme, 2019.

The Board notified that in the notification dated September 12, 2019, in the opening portion, for the word “E-assessment”, the words “Faceless Assessment” shall be substituted. The Board notified the procedure for the faceless assessment wherein the National e-Assessment Centre shall serve a notice on the assessee under sub-section (2) of section 143, specifying the issues for selection of his case for assessment.

Promoting a transparent and fair tax regime, Prime Minister Narendra Modi unveiled ‘taxpayers’ charter’, enshrining rights of assesses in a statute under the Income tax law. With the launch of ‘Transparent Taxation — Honoring the Honest’ platform, Modi also unveiled faceless appeal and expanded the scope of faceless assessment, eliminating physical interface between taxpayers and tax authority.

Step wise process for Faceless Assessment, scope extended to cover best judgement assessment:

Introduction

The Central Board of Direct Taxes (CBDT) has revised the ‘E-assessment Scheme, 2019’ notified on September 12, 2019. Now, e-assessment scheme shall be called Faceless Assessment.

The National e-Assessment Centre shall intimate the assessee for conduct of faceless assessment in case wherein notice has been issued by AO. The Board has also extended its scope to cover best judgment assessments.

What was the E-assessment Scheme, 2019?

Finance Minister Nirmala Sitharaman had announced the e-assessment scheme in her Budget speech on July 5, 2019, which was subsequently inaugurated on October 7, 2019.

This was aimed at moving to faceless scrutiny and elimination of human interface in assessment proceedings. The scheme was set to bring in a “paradigm shift” in taxation by eliminating human interface in the income tax assessment system.

The Ministry of Finance vide Central Board of Direct Taxes (CBDT) notification No 61 & 62 dated 12th September 2019 has respectively notified the E- assessment Scheme 2019 & gave directions for its implementation.

E-assessment Scheme, 2019 to be now called as “Faceless Assessment”

Step wise process for Faceless Assessment

By the Notification issued by CBDT on 13th August, 2020, “E-assessment” will be now called as “Faceless Assessment”. Faceless assessment shall be made as per the following procedure:-

Step 1 – Issue of Notice on Assessee

National e-Assessment Centre shall serve a notice on the assessee under section 143(2), specifying the issues for selection of his case for assessment

Assessee may, within 15 days from the date of receipt of notice, file his response to the National e-assessment Centre

Step 2 – Case to be assigned to Assessment Unit

1.National e-assessment Centre shall assign the case selected for the purposes of e-assessment to a specific assessment unit in any one Regional e-assessment Centre through an automated allocation system

2. Where a case is assigned to the assessment unit, it may make a request to the National e-assessment Centre for:-

a. obtaining such further information, documents or evidence from the assesse or any other person

b. conducting of certain enquiry or verification by verification unit

c. seeking technical assistance from the technical unit

3. Where a request for obtaining further information, documents or evidence from the assessee or any other person has been made, the National e-assessment Centre shall issue appropriate notice or requisition to the assessee or any other person for obtaining the information, documents or evidence requisitioned by the assessment unit

4. Where a request for conducting of certain enquiry or verification by the verification unit has been made, the request shall be assigned by the National e-assessment Centre to a verification unit through an automated allocation system

5. Where a request for seeking technical assistance from the technical unit has been made, the request shall be assigned by the National e-assessment Centre to a technical unit in any one Regional e-assessment Centre through an automated allocation system

6. The assessment unit shall, after taking into account all the relevant material available on the record, make in writing, a draft assessment order either accepting the returned income of the assessee or modifying the returned income of the assessee, and send a copy of such order to the National e-assessment Centre with details of the penalty proceedings to be initiated therein, if any.

Step 3 – Draft Assessment Order

1.National e-assessment Centre shall examine the draft assessment order in accordance with the risk management strategy specified by the Board, including by way of an automated examination tool, whereupon it may decide to:-

a. finalise the assessment as per the draft assessment order and serve a copy of such order and notice for initiating penalty proceedings, if any, to the assessee, alongwith the demand notice, specifying the sum payable by, or refund of any amount due to, the assessee on the basis of such assessment, or

b. provide an opportunity to the assessee, in case a modification is proposed, by serving a notice calling upon him to show cause as to why the assessment should not be completed as per the draft assessment order, or

c. assign the draft assessment order to a review unit in any one Regional e-assessment Centre, through an automated allocation system, for conducting review of such order;

2. Review unit shall conduct review of the draft assessment order, referred to it by the National e-assessment Centre whereupon it may decide to:-

a. agree with the draft assessment order and intimate the National e-assessment Centre about such agreement; or

b. suggest such modification, as it may deem fit, to the draft assessment order and send its suggestions to the National e-assessment Centre;

3. National e-assessment Centre shall, upon receiving concurrence of the review unit, follow the procedure laid down in sub point (a) or (b) of point (1), as the case may be

4. National e-assessment Centre shall, upon receiving modification suggestions from the review unit, communicate the same to the Assessment unit

5. Assessment unit shall, after considering the modifications suggested by the Review unit, send the final draft assessment order to the National e-assessment Centre

6. The National e-assessment Centre shall, upon receiving final draft assessment order, follow the procedure laid down in sub point (a) or (b) of point (1),as the case may be

7. The assessee may, in a case where show-cause notice has been served upon him, furnish his response to the National e-assessment Centre on or before the date and time specified in the notice

8. The National e-assessment Centre shall,-

a. in a case where no response to the show-cause notice is received, finalise the assessment as per the draft assessment order; or

b. in any other case, send the response received from the assessee to the assessment unit;

9. The assessment unit shall, after taking into account the response furnished by the assessee, make a revised draft assessment order and send it to the National e-assessment Centre

Step 4 – Final Order and Completion of Assessment

The National e-assessment Centre shall, upon receiving the revised draft assessment order:-

a. in case no modification prejudicial to the interest of the assessee is proposed with reference to the draft assessment order, finalise the assessment or

b. in case a modification prejudicial to the interest of the assessee is proposed with reference to the draft assessment order, provide an opportunity to the assessee

c. the response furnished by the assessee shall be dealt with as per the procedure laid down in point 7, 8, 9 of Step 3

2. The National e-assessment Centre shall, after completion of assessment, transfer all the electronic records of the case to the Assessing Officer having jurisdiction over such case for:

a. imposition of penalty

b. collection and recovery of demand

c. rectification of mistake;

d. giving effect to appellate orders

e. submission of remand report, or any other report to be furnished, or any representation to be made, or any record to be produced before the Commissioner (Appeals), Appellate Tribunal or Courts, as the case may be

f. proposal seeking sanction for launch of prosecution and filing of complaint before the Court;

3. National e-assessment Centre may at any stage of the assessment, if considered necessary, transfer the case to the Assessing Officer having jurisdiction over such case.

Faceless assessment facility was extended to the entire country on 13th August, 2020, ending territorial jurisdiction and individual discretion, where an officer was the whole and sole to the assessee. Scrutiny will be allotted on a random basis. Assessment of a taxpayer in Delhi could well be carried by an officer sitting in Pune. It will put an end to needless litigation. Best Judgements Assessments under Section 144 will be also now covered under Faceless Assessment.

What is the meaning of Best Judgement Assessment?

The Best Judgment Assessment is a procedure under the Income Tax Act to comply with the principles of natural justice. Vide Section 144 of the Income Tax Act, 1961 the Assessing Officer is under an obligation to make an assessment of the total income or less to the best of his judgment in the following cases:

If the person fails to file a return required under section 139(1) and he has not filed a revised return.

If any person fails to comply with all the terms and conditions stipulated under a notice under section 142 or fails to comply with the directions requiring him to get his accounts audited in terms of section 142(2A).

If any person, after having filed a return fails to comply with all the terms of a notice under section 143(2) requiring his presence or production of evidence and documents; or

If the Assessing officer is not satisfied about the correctness and the completion of the accounts of the assessee if no method of accounting has been regularly employed by the assessee.

While Faceless Assessment and Taxpayers Charter came in force already, Faceless Appeal will be available from September 25, 2020. Under the Faceless Appeals system introduced by the government, appeals will be randomly allotted to any officer across the country and the identity of the officer deciding the appeal will remain unknown. The decisions will be team-based.

Very Important update for Charitable Trusts and Exempt Institution registered under section 80G, 12A or section 12AA : New – Fresh Registration Required : Last Date 31.12.2020

All Charitable trusts and exempt institution which are already registered under section 80G, 12A or section 12AA of Income Tax Act, 1961 will now be required to obtain FRESH REGISTRATION by December 31, 2020.

Provisions of registration under section 80G, 12AA or section 12A will be redundant from 31st December, 2020 and a new section 12AB will come into force with effect from 01st January 2021.

All the existing registered trusts under the erstwhile section 80G, 12A or section 12AA would move to new provision section 12AB.

The new section 12AB proposes to change the registration process by prescribing the time frame for processing the application and validity of such a registration certificate so granted under the new section 12AB.

An order granting registration or approval shall be passed within 3 months of the application. Such registration or approval shall be valid for 5 years.

Similarly, charitable trusts and exempt institutions which already have Section 80G certificate will now be required to reapply for registration or approval by December 31, 2020.