Deactivation of DIN for non-compliance of KYC by company Directors has since been marked as ‘Deactivated due to non-filing of DIR-3 KYC’.

The Ministry of Corporate Affairs website (“MCA”), MCA has stated that the DINs which have not complied with the requirement of filing DIR-3 KYC have been marked as ‘Deactivated due to non-filing of DIR-3 KYC’.

The last date for filing DIR-3 KYC for the financial year 2018-19 has expired on 14th October 2019.

The process of deactivating the non-compliant DINs was in progress and has since been completed by MCA. The form DIR-3 KYC and web service DIR-3 KYC were not available for filing during the pendency of this activity.

Filing of DIR-3 KYC and DIR-3 KYC WEB can be made after completion of the scheduled activity, as above when the form & service are re-deployed on the portal after payment of applicable fees.

The DINs which have not complied with the requirement of filing DIR-3 KYC has since been marked as ‘Deactivated due to non-filing of DIR-3 KYC’.

Such DINs are not allowed to be used for filing any e-forms on the MCA21 portal.

In case the present status of your DIN is ‘Deactivated due to non-filing of DIR-3 KYC’, you are required to file ‘KYC’ using e-form DIR-3 KYC or DIR-3-KYC-WEB service as applicable with prescribed fee of INR 5000 to re-activate your de-activated DIN.

The revised FAQs related to DIR-3 KYC have been updated, giving detailed guidelines as below:

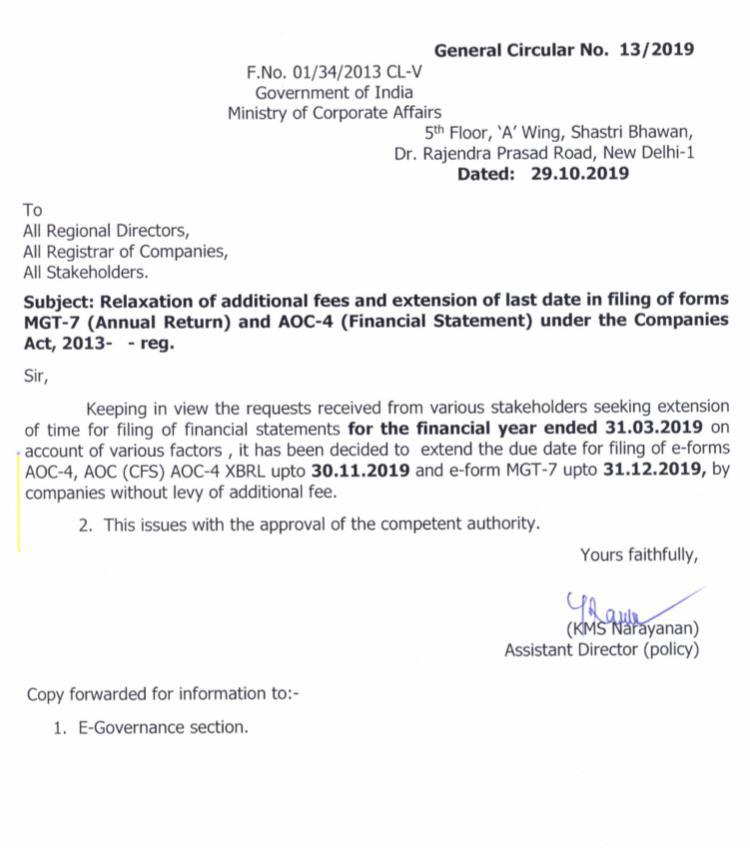

MCA extends due date for filing of AOC 4 and MGT 7 (Financial Statements & Annual Return)

MCA has notified that the due date for filing of financial statements and annual return in e-forms AOC 4, AOC (CFS) and AOC-4 XBRL upto 30 Nov. 2019 and e-form MGT 7 up to 31 Dec. 2019 by companies without levy of additional fee, in view of the practical difficulties faced by various stakeholders and the requests from various professional bodies and businesses, as under:

The due dates for filing Financial Statements – AOC-4, was 30 Oct,2019 and for the Annual Returns – MGT-7 was 30 Nov,2019. Both these are now relaxed by additional 1 more month for filing with Ministry of Corporate Affairs, without levy of additional fee.

The government, in creating disciplinary mechanisms, could consider bringing in disclosure norms for auditors with respect to non-audit services and fees charged by them

The Ministry of Corporate Affairs is planning to amend the Chartered Accountants Act to build disciplinary mechanisms for removing possible conflicts of interest between audit firms and companies they audit.

The government is also looking at ways to address the gaps in the law with respect to network entities of which audit firms are part.

“We need to strengthen the Chartered Accountants Act. Many entities need to be brought within the regulatory remit to create accountability and transparency,” a senior government official told Business Standard.

The government, in creating disciplinary mechanisms, could consider bringing in disclosure norms for auditor with respect to non-audit services and fees charged by them

Due Date for DIR-3 KYC is now extended to 14th October 2019 from 30th September 2019

As per Ministry of Corporate Affairs, if any person has been allotted “Director Identification Number” and the status of such DIN appears to be Approved then such Director needs to file a form to update DIR-3 KYC details in the system. Disqualified directors are also required to file form DIR-3 KYC.

For the financial year ending on 31 st March 2019, the individual shall submit e-form DIR-3 KYC or web form DIR-3 KYC-WEB, as the case may be, on or before the 14th October 2019 (extended from 30 September, 2019).

As per the said notification:

eForm DIR-3 KYC is to be filed by an individual who holds DIN and is filing his KYC details for the first time or by the DIN holder who has already filed his KYC once in eform DIR-3 KYC but wants to update his details.

Web service DIR-3-KYC-WEB is to be used by the DIN holder who has submitted DIR-3 KYC eform in the previous financial year and no update is required in his details.

Due Date for above is now extended to 14th October 2019 from 30th September 2019.

What happens if eForm DIR-3 KYC is not filed within the specified due date?

As per MCA notification Dated 25th Jully 2019, If a Director, fails to file eform DIR-3 KYC before the expiry of the due date, then MCA21 system will mark his/her DIN as ‘De-activated’ with reason as ‘Non-filing of DIR-3 KYC’.

However, the de-activated DIN shall be re-activated only after eform DIR-3 KYC is filed along with payment of Rs. 5000.

In order to avoid any delay which would result in payment of Rs. 5000, the Directors are advised to file the same before the due date.

A government-appointed panel on regulating auditors and the networks had suggested that the fee from non-audit services should not be more than 50% of the audit fee.

India is considering tougher rules for audit firms, including a cap on the number of listed companies they can examine, according to a person with knowledge of the matter, as the government seeks to tighten oversight after a recent spate of governance lapses.

In India, 70% of the about 1,800 companies that trade on the National Stock Exchange are audited by firms affiliated to EY, Deloitte & Touche, KPMG and PWC, according to Delhi-based Prime Database. Current rules stipulate that individual auditors can examine accounts of up to 20 companies, though there is no limit on number of audits for the company.

The Big Four in India operate through a network of local chartered accountants firms. One way for them is to partner as a member of a local firm. They can also allow their brand name to be used by sub-licensee of a member local firm. The ministry hasn’t decided if the cap on audits will be at the group level or on each member firm, the person said.

The government is planning to expand the list of services which can’t be offered by statutory auditors under the Companies Act. Currently, statutory auditors can’t offer nine services, directly or indirectly, including internal audit, investment banking, and actuarial services. There is no restriction on providing services such as taxation or restructuring and valuation.

One option is to tweak the present cap on fees that can be generated through offering non-audit services, the person said. This cap, fixed in 2002, says fees from non-audit work can’t be more than the aggregate statutory audit fees. A spokeswoman for the corporate affairs ministry declined to comment.

A government-appointed panel on regulating auditors and the networks had suggested that the fee from non-audit services should not be more than 50% of the audit fee.

Deloitte Ban

Governance lapses and negligence has loaded the nation’s banks with one of the world’s worst piles of bad debt. In some cases, allegations of fund diversion have surfaced, while the founders of some shadow banks have faced accusations of accepting kickbacks in exchange for loans.

The corporate affairs ministry earlier this month sought a ban on Deloitte Haskins & Sells and BSR & Co. for their role as auditors to IL&FS Financial Services, a part of the IL&FS Group that was seized by the government last year after a string of debt defaults.

Deloitte in an emailed statement said it’s fully compliant with Indian audit standards, while BSR said it would defend its position in accordance with the law.

Meanwhile, the banking regulator forbid EY affiliate S. R. Batliboi & Co. from taking on bank audits for a year and, in 2018, the markets watchdog banned the local unit of PricewaterhouseCoopers LLP for two years in relations to work from a decade earlier.

Clarification on Auditor’s Certificate on Return of Deposits pursuant to Rule 16 of the Companies (Acceptance of Deposits) Rules, 2014

This has reference to Rule 16 of the Companies (Acceptance of Deposits) Rules, 2014 and further amendments.

In this regard, the Ministry of Corporate Affairs vide its letter no. File No: P-01/08/2013- CL-V Vol. VI dated June 24, 2019 has clarified on the matter as under:

The Auditor’s Certificate is mandatory only in case of return of deposits.

For filing particulars of transactions not considered as deposits information contained therein as on 31st March of that year need not be from the duly audited Financial Statement.

Only in case of Return of Deposit information contained therein as on 31st March of that year should be from duly audited financial statement of the company.

Also in order to provide guidance to members, the Auditing and Assurance Standards Board of ICAI has issued Illustrative Auditor’s Certificate on Return of Deposits, which is available on the below cited link:

With a spate of corporate irregularities coming to the fore, the Centre has decided to make disclosure norms more stringent. Corporate India is now required to submit details of transactions involving the receipt of money or loans taken by them, which are otherwise not considered deposits.

Every company other than Government company to which these rules apply, shall on or before the 29th day of June, of every year, file with the Registrar, a return in Form DPT–3 along with the fee as provided in Companies (Registration Offices and Fees) Rules, 2014 and furnish the information contained therein as on the 31st day of March of that year duly audited by the auditor of the company.

Form DPT–3 shall be used for filing return of deposit or particulars of transaction not considered as a deposit or both by every company other than Government company.

Due Date of the Form DPT-3 – Return of Deposits: Every company shall on or before the 30th day of June, of every year, file a return of deposit with the Registrar and furnish the information contained therein as on the 31st day of March of that year duly audited by the auditor of the company.

Due Date of the Form DPT-3 (ONE TIME): Form DPT-3 one time Due Date – all companies would be required to file Form DPT-3 one-time on or before the 29th June 2019

DPT-3 Due Date (EVERY YEAR): Form DPT-3 every year on or before 30th June of the preceding year.

Auditor of Company prepare the financial statements which include the following (Audited Copy)

Balance sheet,

Profit and loss account

Income and expenditure account

Cash flow statement

Statement of changes in equity

Due Date: 29th May 2019

Penalty On the defaulting company A fine of minimum Rs. 1 crore or twice the amount of deposit so accepted, whichever is lower, which may extend to Rs.10 crores; and

Every Officer who is in default: Imprisonment up to seven years and with a fine of not less than Rs. 25 lakh which may extend to Rs. 2 crores.