How to read the CIN of a company:

How to read the CIN of a company:

You would have come across some long alphanumeric numbers of companies called CIN.

The CIN (Corporate Identification Number) of a company is given as unique code of alphanumeric characters, which, every company that is incorporated in India is given as unique code at the time of its incorporation and this is the Corporate Identification Number (CIN) of that company. This code is given irrespective of whether the company is a private company, public company or listed company or One Person Company.

What CIN represents:

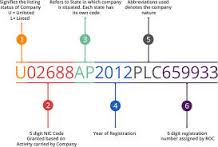

CIN is an alphanumeric 21 digit code given to companies. It stores vital information to represent a company. For example, a CIN would read something like this: U72300MH2014PTC097368. The CIN Number given in the above example is divided into 6 parts. Each part contains information about the Company:

- First Digit represents the listing status – A Company may be either listed or unlisted. First Digit of the CIN indicates the Listing status of the company. If the company is listed, it will be mentioned “L”, if the company is unlisted, it will be mentioned “U” as the first digit of the CIN.

- Next Five Digits represents the Industry Code – Depending on the business line the company belongs to, the Company selects an industry in which it operates. Accordingly, a relevant industry code is allotted to the company.

- Next Two Digits represents the State Code – These digits represent the State in which the registered office of the company is situated. This helps us know which Registrar or ROC is applicable with respect to the company.

For Example: If the company has been registered in Tamil Nadu in the above example “TN” and in case a company is situated in the state of Maharashtra, the Code would be “MH”. In case, the company shifts its registered office to some other place later, the CIN would change due to change in the State Code.

- Next Four Digits represents the year of incorporation of the Company – These digits represents the year in which the company was incorporated. By looking at the CIN of the company, one can tell that the year in which the company was incorporated.

- Next Three Digits represents the type of the company – These three digits identify the type of the company. A company may be any of the following:

– Public Limited Company (PLC)

– Private Limited Company (PTC)

– Government of India Company, Centre (GOI)

– One person Company (OPC)

– Company of State Government (SGC)

– Section 8 Company – Not for Profit (NPL)

- Last Six Digits – These last 6 digits represent the ROC Registration Number of the company. They are unique numbers given to every company at the time of incorporation by the ROC in which they are registering. This number depends on the ROC in which the company is registering and also the Industry to which has been associated with.

This is what the 21 digit CIN Code comprises of. Next time, you see CIN of a company, there would be many things that you should be able to read easily.

You can look for CIN of the companies in a corporate directory. CIN is also mentioned on the letter head of the company.

Would a Company’s CIN ever change?

Yes. CIN is the number with which we identify a company. Typically CIN is to remain with the company for a lifetime but in, few cases, the CIN of the company could change:

* Change in State where registered office of the company is situated

* The listing status of the company changes

* The industry of the company changes

* The company becomes public limited from private limited or vice versa

The government is looking to further simplify income tax return forms to help taxpayers fill them without seeking help from experts and the revenue department has set up a committee in this regard.

The government is looking to further simplify income tax return forms to help taxpayers fill them without seeking help from experts and the revenue department has set up a committee in this regard.