Summary of Direct and Indirect Tax Proposals: Budget 2024-25

Summary of the direct and indirect tax proposals made in the Budget 2024-25 (Finance Bill 2024) presented by Smt Nirmala Sitharaman, Union Minister of Finance and Corporate Affairs:

Highlights of the Direct Tax Proposals of Finance Bill, 2024

No changes in Tax Rates

No changes have been proposed to the existing rates of direct and indirect taxes. The existing rates of income tax, gst, import duties, etc. have been retained.

To provide continuity, some tax benefits and exemptions have been extended by 1 year until 31st March 2025. These include:

Tax benefits for startups;

Tax exemptions on certain income for International Financial Services Centers (IFSCs); and

Tax exemptions on investments made by sovereign wealth funds and pension funds.

The Interim Budget 2024 maintains the status quo on tax rates and extends certain tax breaks by a year to provide stability and continuity in taxation. No new changes or reforms have been introduced to the tax structure or rates.

Withdrawal of Outstanding direct tax demands

The FM has announced to withdraw the outstanding demands of income tax. Here is a summary of the key points regarding the withdrawal of outstanding direct tax demands announced in the Interim Budget 2024:

i) In line with the government’s vision to improve ease of living and doing business, outstanding petty direct tax demands up to Rs 25,000 dating back to 1962 will be withdrawn for the period up to FY 2009.

ii) Similarly, outstanding demands up to Rs 10,000 will be withdrawn for the FY 2010-11 to 2014-15.

iii) These are non-verified, non-reconciled or disputed demands that continue to remain on the books, causing anxiety for taxpayers.

Withdrawing these demands will help provide relief to honest taxpayers and enable refunds for subsequent years.

This is expected to benefit about 1 crore taxpayers who have such outstanding demands.

The move aims to improve tax payer services and reduce harassment of taxpayers over small disputed sums dating back decades.

In short, the Interim Budget 2024 has announced the withdrawal of old, petty direct tax demands up to Rs 25,000 till FY 2009-10 and Rs 10,000 between FY 2010-11 to 2014-15 to provide relief to taxpayers.

Highlights of the Indirect Tax Proposals of Finance Bill 2024

The FM has proposed in Budget 2024 to retain the same tax rates in respect of GST, import duty, etc.indirect taxes as are applicable at present, i.e. existing GST and import duty rates shall continue in FY 2024-25 as well.

With 2.75 crore refunds already processed, the I-T department has asked taxpayers to respond to outstanding tax demands promptly.

The Income Tax Department has urged taxpayers to address any outstanding tax demands for previous years in order to facilitate faster clearance of refunds for the 2022-23 fiscal year. This is a taxpayer-friendly measure, as it gives taxpayers an opportunity to clarify the status of any outstanding demands and ensure that they receive their refunds as quickly as possible.

The Income Tax Department on September 23, 2023, called upon taxpayers to promptly respond to intimation of outstanding tax demands, adding that it will help in faster processing of income tax returns (ITR) and quicker issuance of refunds.

For the Assessment Year 2023-24, a total of 7.09 crore returns have been filed. Of these, 6.96 crore ITRs have been verified, 6.46 crore returns have been processed, and 2.75 crore refund returns have already been issued as per the latest data from the I-T department.

The Income Tax Department is making every effort to complete the processing of ITRs and issuance of refunds expeditiously, it said in a social media post on X. However, a significant hurdle in achieving this goal is that there are previous outstanding tax demands.

What are pending tax demands?

After you file your returns, the Income Tax Department inspects the tax declarations and if there are any mismatches with your actual tax liability, it issues an “outstanding tax demand” notice.

Section 245(1) of the Income-tax Act, 1961, necessitates offering taxpayers an opportunity to provide their input before adjusting the refund against any existing demand. Taxpayers are required to agree, disagree, or clarify the status of the demand.

Taxpayers who have outstanding demands from previous years will receive notifications from the department. So it has requested the taxpayers to respond to such intimations to enable “cleaning up/reconciliation” of pending demands and facilitate timely issue of refunds. It will not only aid in resolving pending demands but also expedite the timely issuance of refunds.

How to Respond to Outstanding Tax Demands?

In its official website, the Income Tax Department shows how one can respond to outstanding demands. Here are the steps to follow:

To begin the process, taxpayers should visit the official Income Tax Department’s e-filing portal at https://www.incometax.gov.in/iec/foportal/.

Under the ‘e-File’ menu, taxpayers should locate and click on the ‘Response to Outstanding Demand’ option.

In the subsequent screen, taxpayers will find a list of response options. They can select from the following choices:

a) Demand is correct

b) Demand is partially correct

c) Disagree with demand

d) Demand is not correct but agree for adjustment

Submit Your Response: Depending on the chosen response, taxpayers should follow the instructions provided on the portal. If the taxpayer selects ‘Demand is correct,’ they should click on the ‘Submit’ button to confirm their choice and complete the response submission process.

However, if the ‘Demand is correct’ option is confirmed, taxpayers will not have the option to disagree with the demand later and any refund owed will be adjusted against the outstanding demand. Taxpayers also have the option to pay the demand directly by clicking the link under the ‘Pay Tax’ option.

This scheme aims to grant a condonation of delay to LLPs for filing of Form-3, Form-4, and Form-11 from September 1, 2023 to September 30, 2023.

The Ministry of Corporate Affairs (MCA) has notified the Limited Liability Partnership (LLP) Amnesty Scheme. The ministry vide circular number No. 8/2023 issued on 23rd August 2023 condoning the delay in filing of Form-3, Form-4 and Form-11 under Section 67 of Limited Liability Partnership (LLP) Act, 2008 read with Section 460 of Companies Act, 2013.

These forms shall be available for filing from 01.09.2023 onwards till 30.11.2023 (both dates inclusive). Also, the LLPs availing the scheme shall not be liable for any action for delayed filing of the Form-3, Form-4 and Form-11.

Based on the representations received by the government that certain LLPs are finding difficulties in filing Form- 3 (LLP Agreement and changes therein), Form- 4 (Notice of appointment, cessation, change in name/ address/designation of a designated partner or partner and consent to become a partner/ designated partner) and Form- 11 (Annual Return of LLP) for various reasons including due to mismatch in the master data in electronic registry of the Ministry.

Due to this, the records/data in the electronic registry are also not being updated. Thus, to address these issues, the government has decided to grant one-time relaxation in additional fees to those LLPs who could not file the Form 3, 4 and 11 within the due date and provide an opportunity to update their filings and details in master data for future compliances.

The following are highlights of Amnesty Scheme:

The Form-3 and Form-4 would be processed under Straight Through Process (STP) mode for all purposes except for change in business activities.

The stakeholders are advised to file these forms in sequential manner i.e., the filing for old events date may be filed first and so on so as to update the master data in proper manner.

At the time of filing these forms, the pre-filled data as per existing master data of the LLP shall be provided in each of above mentioned forms but the same shall have the facility to edit. The onus of filing correct data would be on the stakeholders.

In case of misrepresentation, the Designated Partner and the professional certifying the form may be liable for adverse action as per provisions of the law.

The filing of Form-3 and Form-4 without additional fee shall be applicable for the event dates 01.01.2021 and onwards.

For events dated prior to 01.01.2021, these forms can be filed with 02 times and 04 times of normal filing fees as additional fee for small LLPs and Other than small LLPs respectively.

The filing of Form-II without additional fee shall be applicable for the financial year 2021-22 onwards.

Form-II for previous years (prior to financial year 2021-22) can be filed with 02 times and 04 times of normal filing fee as additional fee for small LLPs and Other than small LLPs respectively.

These forms shall be available for filing from 01.09.2023 onwards till 30.11.2023 (both dates inclusive). The LLPs availing the scheme shall not be liable for any action for delayed filing of the Form-3, Form-4 and Form-11.

The Ministry of Corporate Affairs (MCA) is all set to launch the Second Set of Company Forms on the MCA21 V3 portal, in January 2023, comprising of total 56 forms.

The first lot will consist of 10 forms to be released on January 9, 2023, and the second lot will consist of 46 forms to be released on January 23, 2023.

In order to simplify the process of integrating these forms into ( web based filing) the MCA21 V3 portal, the Ministry of Corporate Affairs has requested stakeholders to take note of the following points:

(1) For 10 forms scheduled for rollout from January 7, 2023, at 12:00 a.m. to January 8, 2023, at 11:59 p.m., company e-Filings on the V2 portal will be disabled for the specified forms that are scheduled to be released on January 9, 2023.

(2) For 46 forms scheduled for rollout on January 23, 2023, company e-Filings on the V2 portal will be disabled from January 7, 2023, at 12:00 a.m. to January 22, 2023, at 11:59 p.m.

(3) All stakeholders are advised to ensure that there are no SRNs in “pending payment” or “resubmission” status.

(4) Offline payments in V2 for the above 56 forms using the “Pay Later” option would be discontinued on December 28, 2022, at 12:00 AM. The stakeholders are required to pay for these forms in V2 online (via credit/debit card or net banking).

(5) Due to the upcoming release of 56 company forms, the V3 portal will be unavailable from January 7 at 12:00 AM to January 8 at 11:59 PM for the roll-out of 10 company forms, and from January 21 to 22, 2023, for the roll-out of 46 company forms.

(6) The V2 Portal for company filing will continue to be available for all forms except the 56 mentioned above.

LIST OF 10 COMPANY FORMS TO BE ROLLED OUT ON 09 Jan 2023

Sl. No.

Form Number

Form Name

1

SPICe+ PART A

Application for reservation of name for new company incorporation

2

RUN

Application for change of name of existing company

3

SPIce+ PART B

Integrated Company Incorporation Application

4

AGILE PRO S

Application for Goods and services tax Identification number , employees state Insurance corporation registration pLus Employees provident fund organisation registration, Profession tax Registration, Opening of bank account and Shops and Establishment Registration

5

e-AOA[INC-34]

Articles of Association

6

e-MOA[INC-13]

Memorandum of Association

7

e-MOA[INC-31]

Articles of Association

8

e-MOA[INC-33]

Memorandum of Association

9

INC-9

Declaration by Subscribers and First Directors

10

URC-1

Application by a company for registration under section 366

LIST OF 46 COMPANY FORMS TO BE ROLLED OUT ON 23rd Jan 2023

Sl. No.

Form Number

Form Name

1

DIR-12

Particulars of appointment of directors and the key managerial personnel and the changes among them

2

DIR-11

Notice of resignation of a director to the Registrar

3

DIR-3

Application for allotment of Director Identification Number

4

DIR-3C

Intimation of Director Identification Number by the company to the Registrar DIN services

5

DIR-5

Application for surrender of Director Identification Number

6

DIR-6

Intimation of change in particulars of Director to be given to the Central Government

7

INC-12

Application for grant of License to an existing company under section 8

8

INC-18

Application to Regional Director for conversion of section 8 company into any other kind of company

Sl. No.

Form Number

Form Name

9

INC-20

Intimation to Registrar of revocation of license issued under section 8

10

INC-20A

Declaration for commencement of business

11

INC-22

Notice of situation or change of situation of registered office

12

INC-23

Application to the Regional Director for approval to shift the Registered Office from one State to another state or from jurisdiction of one Registrar to another Registrar within the State

13

INC-24

Application for approval of Central Government for change of name

14

INC-27

Conversion of public company into private company or private company into public company or Conversion of Unlimited Liability Company into Limited Liability Company

15

INC-28

Notice of Order of the Court or any other competent authority

16

INC-4

One Person Company – Change in Member/ Nominee

17

INC-6

One Person Company – Conversion form

18

MGT-14

Filing of Resolutions and agreements to the Registrar under section 117

19

MR-1

Return of appointment of managing director or whole time director or manager

20

MR-2

Form of application to the Central Government for approval of appointment or reappointment and remuneration or increase in remuneration or waiver for excess or over payment to managing director or whole time director or manager and commission or remuneration to directors

21

NDH-4

Form for filing application for declaration as Nidhi Company or updation of status by Nidhis.

22

PAS-3

Return of Allotment

Sl. No.

Form Number

Form Name

23

SH-7

Notice to Registrar of any alteration of share capital

24

SH-11

Return in respect of buy-back of securities

25

SH-8

Letter of Offer

26

SH-9

Declaration of Solvency

27

NDH-1

Return of Statutory Compliances

28

NDH-2

Application for extension of time

29

NDH-3

Return of Nidhi Company for the half year ended

30

GNL-3

Particulars of person(s) charged for the purpose of sub-clause (iii) or (iv) of clause 60 of section 2

31

PAS-6

Reconciliation of Share Capital Audit Report (Half-yearly)

32

MGT-3

Notice of situation or change of situation or discontinuation of situation, of place where foreign register shall be kept

33

PAS-2

Information Memorandum

34

DIR-9

Report by the company to Registrar for disqualification of Directors

35

DIR-10

Application for removal of Disqualification of Directors

36

AOC-5

Notice of address at which books of account are maintained

37

FC-1

Information to be filed by foreign company

38

FC-2

Return of alteration in the documents filed for registration by foreign company

39

FC-3

Annual accounts along with the list of all principal places of business in India established by foreign company

40

FC-4

Annual Return of a Foreign company

41

GNL-2

Form for submission of documents with the Registrar

42

GNL-4

Addendum to form

43

MSC-1

Application to ROC for obtaining the status of dormant company

44

MSC-3

Return of dormant companies

45

MSC-4

Application for seeking status of active company

46

RD-1

Form for filing application to Regional Director

Stakeholders are advised by MCA to plan accordingly.

MCA has further revised/ increased the ‘paid-up capital’ and ‘turnover’ thresholds applicable in the case of ‘small companies’ under the Companies Act, 2013, to reduce compliance burden for more number of companies to be treated as ‘small companies’, as part of ‘ease of doing business’ initiative.

Earlier, the definition of “small companies” under the Companies Act, 2013 was revised by increasing these thresholds, i.e. paid up capital threshold was increased from not exceeding Rs 50 lakh to Rs 2 crore and turnover threshold was increased from not exceeding Rs 2 crore to Rs 20 crore.

These thresholds, now have been further revised/ increased to amend the definition of small companies, so that more number of companies can be treated as ‘small companies’, eventually to reduce their compliance burden. Now the paid up capital threshold has been increased from not exceeding Rs 2 crore to Rs 4 core and turnover threshold has been increased from not exceeding Rs 20 crore to Rs 40 crore, which effectively means that number of small companies will increase substantially.

In the recent past, MCA has taken several initiatives/ measures in the direction of ease of doing business for corporates, like decriminalization of various provisions of the Companies Act, 2013/ LLP Act, 2008, extending fast track mergers to start ups, incentivizing incorporation of One Person Companies (OPCs) etc.

Lakhs of small companies significantly contribute to the growth of Indian economy and generation of employment. Therefore, Government is making continuous efforts by such initiatives/ measures which create a more conducive business environment for law-abiding small companies, by reducing their compliance burden so that they can focus more on their core business.

It may be noted that small companies are eligible for certain benefits/ relaxations, in the form of reduced compliance burden, some of which are listed hereunder:

i) No need to prepare cash flow statement by small companies, forming part of financial statement,

ii) Advantage of preparing and filing an Abridged Annual Return,

iii) Mandatory rotation of auditor not required,

iv) An Auditor of a small company is not required to report on the adequacy of the internal financial controls and its operating effectiveness in the auditor’s report,

v) Holding of only two board meetings in a year,

vi) Annual Return of the company can be signed by the company secretary, or where there is no company secretary, by a director of the company,

vii) Lesser penalties for small companies, etc.

In view of the fact that ‘paid up capital’ and turnover’ thresholds applicable for ‘small companies’ under the Companies Act, 2013 have been further revised/ increased, this will allow more number of companies to enjoy relaxation from certain compliance burdens.

The Double Tax Avoidance Agreement (DTAA) is essentially a bilateral agreement entered into between two countries. The basic objective is to promote and foster economic trade and investment between two Countries by avoiding double taxation.

WHAT IS DOUBLE TAXATION OF INCOME?

When the same income is taxed more than once, due to levying of tax by two or more jurisdictions, on the same income asset or financial transaction, this results in double taxation. This may happen, when an assessee – an Individual or a company, is taxed more than once for the same income in India, either on the basis of place of residence or on the basis of source of accrual, which leads to double taxation.

Countries have started entering into Double Taxation Avoidance Agreements (DTAA) with other countries to resolve double taxation issue so as to ease out the tax burden of their taxpayers. This relief for taxes paid in foreign country is given to taxpayer while taxing the same income in the India, which is termed as Foreign Tax Credit (FTC).

B. HOW DOUBLE TAXATION AVOIDANCE AGREEMENT (DTAA) WORKS?

In any country, the tax is levied based on 1) Source Rule and 2) the Residence Rule.

The source rule holds that income is to be taxed in the country in which it originates irrespective of whether the income accrues to a resident or a non-resident whereas the residence rule stipulates that the power to tax should rest with the country in which the taxpayer resides.

If both rules apply simultaneously to a business entity and it were to suffer tax at both ends, the cost of operating on an international business would become prohibitive and would deter the process of globalization. It is from this point of view that Double Taxation Avoidance Agreements (DTAA) have become significant.

Where the Central Government has entered into an agreement with the Government of any country outside India or specified territory outside India, for granting relief of tax, or as the case may be, avoidance of double taxation, then, in relation to the assessee to whom such agreement applies, the provisions of this Act shall apply to the extent they are more beneficial to that assessee.

Impact of Double Taxation Avoidance Agreement:

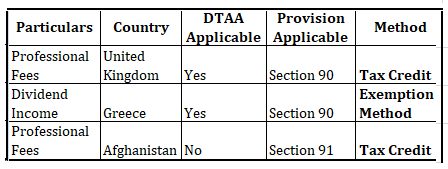

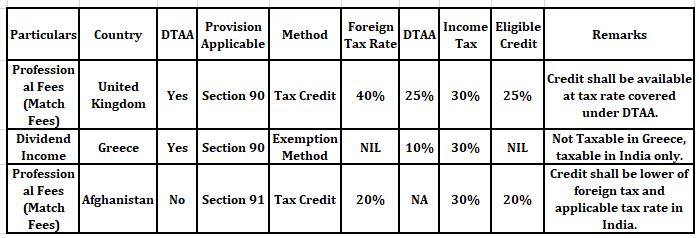

1. WHERE DTAA EXISTS (SECTION 90):

There are two methods of granting relief under Double Taxation Avoidance Agreement.

Exemption method – A particular income is taxed in one of the both countries and exempted in the other

Example- For the Income from Dividend, Interest, royalty and fees for technical services Source Rule is applicable in treaty with Greece, Libyan and United Arab Republic. So for citizen of these 3 countries if the dividend, interest, royalty or fees for technical services is arising in India, then it will be solely taxable in India only and for a resident if such income is arising in any of these 3 countries then the income will solely be taxed in these 3 countries and it will not at all be taxable in India.

Tax Credit method- The income is taxed in both the countries as per the treaty and the country of residence will allow the tax credit / reduction for the tax charged in the country of Origin.

Example- Mr. A (an Indian resident) has received salary from a US company for job in US. Since Mr. A is a resident so his global Income will be taxable in India. In this case, source country is US (since the service has been rendered in US) and resident country is India. So at the time of computation of tax liability of Mr. A, the tax paid in US will be allowed as set off against his total tax liability but limited to the tax payable on such foreign income at Indian tax rates.

Therefore DTAA determines which method to be used first and, if the income is taxable only in one country then exemption method shall be used, but if the same is taxable in both countries then tax credit method comes into play.

In case where Bilateral agreement has been entered under section 90 of the Income Tax Act, 1961 with a foreign country then the assessee has an option either to be taxed as per the Double Taxation Avoidance Agreement (hereinafter referred as “DTAA”) or as per the normal provisions of Income Tax Act 1961, whichever is more beneficial to assessee.

Example- As per DTAA between India and Germany, tax on Interest is specified @ 10% whereas under Income Tax Act 1961, it depends on slab rates for individuals & HUF and flat rates (generally 30%) for other kind of assessees (like firm, company etc). Hence, one can follow DTAA and pay tax @ 10% only.

2. WHERE DTAA DOES NOT EXIST (SECTION 91):

i. If any person who is resident in India in any previous year, in respect of income which arose outside India (and which is not deemed to accrue or arise in India), and paid in any country with which there is no agreement under section 90 for the relief or avoidance of double taxation, then he shall be entitled to the deduction from the tax payable in India,

ii. Deduction shall be lower of:

Tax calculated on such double taxed income at the Indian rates.

Tax calculated on such double taxed income at the rate of tax of the said country

Example :Suppose Indian Sportsman, resident of India who earns foreign income in form of match fees being professional and dividend income as his other foreign income from the below mentioned countries, then in such case following provisions and method shall govern his taxability:

Therefore, both Tax Credit method u/s 90 and Section 91 deals with Foreign Tax Credit, but still having DTAA is beneficial because assessee is taxed at rate beneficial to him, which is not so in case of NO DTAA.

C. HOW CREDIT OF FOREIGN TAX IS AVAILED IN INDIA?

Rule 128 governs the credit of taxes paid on income earned in foreign country. An assessee shall be eligible to claim credit of foreign tax paid if he complies with provisions stated under Rule 128 of the Income Tax Rules which are discussed as follows:

1. Analysis of Rule 128 introduced under Indian Income Tax Rules

Applicability of the rules

The rules came into force with effect from 1.4.2017 applicable only for resident assessee for the amount of foreign taxes paid by him in a foreign country. The credit is available only if income corresponding to the taxes is offered for tax or assessed to tax in India during the year in which the credit is claimed.

In the cases where the income for which the foreign taxes paid or deducted is offered to taxes for more than one year, the credit will be given across the years in the same proportion to which the income is offered to tax in India during the year in which credit is claimed.

2. Foreign Tax Credit Defined under sub-rule 2:

i. FTC in case of DTAA countries: Taxes that are covered under the said agreement.

ii. FTC in case of other countries (No DTAA): Tax payable under the law in force in that country in the nature of income-tax referred in Section 91.

The LOWER OF tax payable under the act on such income or the foreign tax paid is eligible as FTC. However, while considering the foreign tax paid, it cannot exceed the amount arrived as per DTAA with that country.

3. Utilization of Foreign Tax Credit:

FTC is eligible for adjustment against the tax, surcharge and cess payable under the IT Act. FTC cannot be adjusted against interest, fee or penalty payable under the IT Act. FTC is not available in case foreign tax or part thereof is disputed by the assessee in any manner.

4. Exception & Conditions relating to Foreign Tax Credits:

Credit is allowed in the year in which the income is offered/assessed in India upon the assessee within six months from the end of the month in which dispute is finally settled and assessee furnishes:

Evidence of settlement of dispute

Evidence that the liability for payment of such foreign tax has been discharged and

Undertaking that no refund in respect of such amount is directly or indirectly been claimed. Further, credit for each source of income shall be calculated separately for a specific country and then aggregated. The rate of exchange to be taken for this purpose is TT buying rate on the last day of the month immediately preceding month in which the tax is paid or deducted.

5. Documents required under Foreign Tax Credit:

Furnish FORM 67 duly verified and certified by a Chartered Accountant on or before furnishing return of income u/s 139(1)

Furnishing following certificates or statement specifying:

Nature of income and,

Amount of Tax paid of which statement given by:

Tax authority of that country, or

Person responsible for deduction of such tax, or

Signed by the assessee:

In this case, it should be accompanied with – an acknowledgment of online payment or receipt or bank counterfoil for proof of payment of tax, if tax is paid by the assessee

In case of tax deduction, proof of such Tax deducted at source

D. JUDICIAL PRECEDENTS UNDER FOREIGN TAX CREDIT

1. WIPRO LIMITED F TS – 565 – HC – 2015 (KAR)

The judgment of WIPRO provides that merely because the taxpayer’s income is exempt from tax due to a limited tax holiday provided under the ITA, does not mean that foreign tax credit can be simply denied.

2. TATA SONS [2011] 43 SOT 27 (MUM AT)

Though DTAA with USA provides credit only the tax paid with the Federal Government, credit was extended to the Taxes paid to State taxes as well. It has considered the relief u/s 91 which was beneficial to the assessee than that of the DTAA.

3. VIJAY ELECTRICALS [2015] 54 COM 19 (HYD AT)

Tax credit is available even if the same is not deposited with the overseas Government in the year in which the income is taxable.

Taxpayers can make GST payments through challan every month either by self-assessment of monthly liability or 35 per cent of net cash liability of previous filed GSTR-3B of the quarter. Quarterly GSTR-1 and GSTR-3B can also be filed through an SMS.

The government has launched the Quarterly Return Filing and Monthly Payment of Taxes (QRMP) scheme in a bid to ease the return filing experience of the Goods and Services Tax (GST) taxpayers. The scheme will come into effect from January 1, 2021, it will impact 9.4 million taxpayers, who constitute 92% of the total tax base of GST and have an annual aggregate turnover (AATO) of up to Rs 5 crore.

With the introduction of the QRMP scheme, sources say, small taxpayers would need to file only eight returns – four each GSTR-3B and GSTR-1 – instead of the existing requirement of 16 returns in a financial year, of which 12 are GSTR-3B. The new scheme would also significantly reduce taxpayers’ professional expenses on return filing as they would have to file just half the number of returns as against the current requirement of 16. Also, the QRMP scheme would be available on the common GST portal with the facility to opt-in and opt-out, and opt-in again, as per a taxpayer’s wishes.

The scheme would bring in the concept of providing input tax credit (ITC) only on the reported invoices, thus putting a curb on the menace of fake invoice frauds. Additionally, the QRMP scheme is also likely to have the optional feature of Invoice Filing Facility (IFF) to mitigate the business-related hardships of the small and medium taxpayers. Under the IFF, taxpayers who opt to file their returns quarterly would be able to upload and file such invoices even in the first and second month of the quarter for which there is a demand from the recipients.

The taxpayers won’t need to upload and file all the invoices of the month. Only those invoices, which are required to be filed in IFF as per the recipients’ demands, are to be uploaded. The remaining invoices of the first and second months can be uploaded in the quarterly GSTR-1 return.

The QRMP scheme is based on the existing return system with suitable modifications in a bid to give much-needed flexibility to the small and medium enterprises with regards to GST compliance. It was approved in principle by the GST Council in its 42nd meeting on October 5, 2020.