Prime Minister Narendra Modi announced several tax measures on the eve of India’s Independence Day last week honouring the honest tax-paying citizen.

You will now have to file your income-tax (IT) return or pay higher percentage of tax deduction at source if you make certain spends in a year.

If you spend Rs 20,000 a year as hotel expenses, property tax or even a health insurance premium, then your transactions would be reported. Similarly, if your annual rent exceeds Rs 40,000, life insurance premium is at least Rs 50,000 or electricity bills of Rs 1 lakh or more during a financial year, then you would be answerable to the taxman either via notices or through mandatory filing of returns.

The motive of the move is to check whether your spending is in line with the income you actually disclose in your return.

The Government has been shunting all doors to not only reduce the number of all cash transactions, but also increase the number of returns filed. The new move to collect spending data is another tool in the armoury to curb tax evasion.

Are transactions tracked currently?

The existing income tax rules mandate financial institutions such as banks, mutual fund houses, share registrar and transfer agents,sub-registrars to report high value transactions exceeding a specified limit during a financial year to the Income Tax Department.

So, a bank has to report details of every account holder who makes cash deposits of more than Rs 10 lakh in a year in a savings account or makes a payment of more than Rs 2 lakh from his credit card in a year. Similarly, asset management companies are required to report details of all the investors who invest more than Rs 2 lakh in a single mutual fund scheme. Now not only your investments and financial transactions, but also your specific spends will be tracked.

Do I have to inform the government of all my spends?

No. You do not have to go out of your way to inform the government or anyone, unless asked for in the tax return forms. Your purchases and expenses beyond a threshold will be mentioned in the returns of the hotel, electronic goods seller, artist, school, ceramic supplier or the Registrar in the case of property purchase, apart from banks, mutual fund houses, life and general insurance companies.

The details mapped to you would be reflected in your individual tax statement or Form 26AS. This form would be available on your income-tax website login.

The moment your spends in any of the high-spend categories mentioned, exceed the respective threshold limits, your Form 26AS would capture it. In other words, you have to file your tax returns.

Non-filing of ITR may have severe consequences for a person, who is otherwise required to file an ITR. Apart from attracting interest, late fee and penalty, wilful non-filing of ITR may also attract criminal prosecution.

The new move has been part of the government’s move to widen the tax net and get more and more people to file their income tax returns. A total of about 55 lakh or 80 per cent of the total returns are filed by people having an income of up to Rs 5 lakh, as per the Central Board of Direct Tax’s numbers as of July 31, 2020.

Only 5,066 individuals, who have an income above Rs 1 crore file returns, accounting for 0.73 per cent of the total individual tax returns.

Taxpayers would not need to mention their high-value transactions in their income tax returns, said officials in the know of the matter, but added that broadening the scope of reporting financial transactions by third parties had become vital since taxation was moving towards a faceless approach.

It’s clarified that only third parties would report high-value transactions to the income tax department as per the Income Tax Act. The information would be used to identify people who are not paying up due taxes, and not for examining affairs of honest taxpayers.

“The information will be used to identify those who are either not filing the returns or the income disclosed in the returns are not proportionate to the pattern of expenditure reported in the statement of financial transactions (SFTs),” the official said.

Data analytics and artificial intelligence will be used for this, instead of manual intervention.

Terming the method as most ‘non-intrusive’, the official said it would be used for identifying those who spend big money on business class air travel, foreign travel and expensive hotels or send their children to expensive schools, but do not pay taxes, claiming their income to be under Rs 2.5 lakh a year.

Prime Minister Narendra Modi flagged this very issue on Thursday, and asked people to pay their fair share of taxes, given that the country’s tax base was relatively small.

“Only 1.5 crore people pay taxes in a country of 130 crores,” he pointed out while launching a taxpayer’s charter and faceless assessment, aimed at improving transparency in tax administration.

“No doubt, the third-party reporting of high-value transactions made by such non-filers would allow the department to nudge such persons to file their returns and pay their due tax,” the official said.

Faceless e-assessment will have no human interface and it’s purpose will be to eliminate instances of “undesirable practices” on the part of tax officials.

The Central Board of Direct Taxes (CBDT) on Thursday revised the ‘E-assessment Scheme, 2019’ notified on September 12, 2019. The Government notified that now, the e-Assessment scheme shall be called Faceless Assessment.

Now, the National e-Assessment Centre shall intimate the assessee for the conduct of faceless assessment in case wherein notice has been issued by AO.

The Board has also extended its scope to cover best judgment assessments.

E-Assessment was a roadway towards a paperless, faceless assessment stripping away at bureaucratic layers. E-Assessment was earlier tried and tested by the Income-tax Department, before going forth with the E-Assessment Scheme, 2019.

The Board notified that in the notification dated September 12, 2019, in the opening portion, for the word “E-assessment”, the words “Faceless Assessment” shall be substituted. The Board notified the procedure for the faceless assessment wherein the National e-Assessment Centre shall serve a notice on the assessee under sub-section (2) of section 143, specifying the issues for selection of his case for assessment.

Promoting a transparent and fair tax regime, Prime Minister Narendra Modi unveiled ‘taxpayers’ charter’, enshrining rights of assesses in a statute under the Income tax law. With the launch of ‘Transparent Taxation — Honoring the Honest’ platform, Modi also unveiled faceless appeal and expanded the scope of faceless assessment, eliminating physical interface between taxpayers and tax authority.

Step wise process for Faceless Assessment, scope extended to cover best judgement assessment:

Introduction

The Central Board of Direct Taxes (CBDT) has revised the ‘E-assessment Scheme, 2019’ notified on September 12, 2019. Now, e-assessment scheme shall be called Faceless Assessment.

The National e-Assessment Centre shall intimate the assessee for conduct of faceless assessment in case wherein notice has been issued by AO. The Board has also extended its scope to cover best judgment assessments.

What was the E-assessment Scheme, 2019?

Finance Minister Nirmala Sitharaman had announced the e-assessment scheme in her Budget speech on July 5, 2019, which was subsequently inaugurated on October 7, 2019.

This was aimed at moving to faceless scrutiny and elimination of human interface in assessment proceedings. The scheme was set to bring in a “paradigm shift” in taxation by eliminating human interface in the income tax assessment system.

The Ministry of Finance vide Central Board of Direct Taxes (CBDT) notification No 61 & 62 dated 12th September 2019 has respectively notified the E- assessment Scheme 2019 & gave directions for its implementation.

E-assessment Scheme, 2019 to be now called as “Faceless Assessment”

Step wise process for Faceless Assessment

By the Notification issued by CBDT on 13th August, 2020, “E-assessment” will be now called as “Faceless Assessment”. Faceless assessment shall be made as per the following procedure:-

Step 1 – Issue of Notice on Assessee

National e-Assessment Centre shall serve a notice on the assessee under section 143(2), specifying the issues for selection of his case for assessment

Assessee may, within 15 days from the date of receipt of notice, file his response to the National e-assessment Centre

Step 2 – Case to be assigned to Assessment Unit

1.National e-assessment Centre shall assign the case selected for the purposes of e-assessment to a specific assessment unit in any one Regional e-assessment Centre through an automated allocation system

2. Where a case is assigned to the assessment unit, it may make a request to the National e-assessment Centre for:-

a. obtaining such further information, documents or evidence from the assesse or any other person

b. conducting of certain enquiry or verification by verification unit

c. seeking technical assistance from the technical unit

3. Where a request for obtaining further information, documents or evidence from the assessee or any other person has been made, the National e-assessment Centre shall issue appropriate notice or requisition to the assessee or any other person for obtaining the information, documents or evidence requisitioned by the assessment unit

4. Where a request for conducting of certain enquiry or verification by the verification unit has been made, the request shall be assigned by the National e-assessment Centre to a verification unit through an automated allocation system

5. Where a request for seeking technical assistance from the technical unit has been made, the request shall be assigned by the National e-assessment Centre to a technical unit in any one Regional e-assessment Centre through an automated allocation system

6. The assessment unit shall, after taking into account all the relevant material available on the record, make in writing, a draft assessment order either accepting the returned income of the assessee or modifying the returned income of the assessee, and send a copy of such order to the National e-assessment Centre with details of the penalty proceedings to be initiated therein, if any.

Step 3 – Draft Assessment Order

1.National e-assessment Centre shall examine the draft assessment order in accordance with the risk management strategy specified by the Board, including by way of an automated examination tool, whereupon it may decide to:-

a. finalise the assessment as per the draft assessment order and serve a copy of such order and notice for initiating penalty proceedings, if any, to the assessee, alongwith the demand notice, specifying the sum payable by, or refund of any amount due to, the assessee on the basis of such assessment, or

b. provide an opportunity to the assessee, in case a modification is proposed, by serving a notice calling upon him to show cause as to why the assessment should not be completed as per the draft assessment order, or

c. assign the draft assessment order to a review unit in any one Regional e-assessment Centre, through an automated allocation system, for conducting review of such order;

2. Review unit shall conduct review of the draft assessment order, referred to it by the National e-assessment Centre whereupon it may decide to:-

a. agree with the draft assessment order and intimate the National e-assessment Centre about such agreement; or

b. suggest such modification, as it may deem fit, to the draft assessment order and send its suggestions to the National e-assessment Centre;

3. National e-assessment Centre shall, upon receiving concurrence of the review unit, follow the procedure laid down in sub point (a) or (b) of point (1), as the case may be

4. National e-assessment Centre shall, upon receiving modification suggestions from the review unit, communicate the same to the Assessment unit

5. Assessment unit shall, after considering the modifications suggested by the Review unit, send the final draft assessment order to the National e-assessment Centre

6. The National e-assessment Centre shall, upon receiving final draft assessment order, follow the procedure laid down in sub point (a) or (b) of point (1),as the case may be

7. The assessee may, in a case where show-cause notice has been served upon him, furnish his response to the National e-assessment Centre on or before the date and time specified in the notice

8. The National e-assessment Centre shall,-

a. in a case where no response to the show-cause notice is received, finalise the assessment as per the draft assessment order; or

b. in any other case, send the response received from the assessee to the assessment unit;

9. The assessment unit shall, after taking into account the response furnished by the assessee, make a revised draft assessment order and send it to the National e-assessment Centre

Step 4 – Final Order and Completion of Assessment

The National e-assessment Centre shall, upon receiving the revised draft assessment order:-

a. in case no modification prejudicial to the interest of the assessee is proposed with reference to the draft assessment order, finalise the assessment or

b. in case a modification prejudicial to the interest of the assessee is proposed with reference to the draft assessment order, provide an opportunity to the assessee

c. the response furnished by the assessee shall be dealt with as per the procedure laid down in point 7, 8, 9 of Step 3

2. The National e-assessment Centre shall, after completion of assessment, transfer all the electronic records of the case to the Assessing Officer having jurisdiction over such case for:

a. imposition of penalty

b. collection and recovery of demand

c. rectification of mistake;

d. giving effect to appellate orders

e. submission of remand report, or any other report to be furnished, or any representation to be made, or any record to be produced before the Commissioner (Appeals), Appellate Tribunal or Courts, as the case may be

f. proposal seeking sanction for launch of prosecution and filing of complaint before the Court;

3. National e-assessment Centre may at any stage of the assessment, if considered necessary, transfer the case to the Assessing Officer having jurisdiction over such case.

Faceless assessment facility was extended to the entire country on 13th August, 2020, ending territorial jurisdiction and individual discretion, where an officer was the whole and sole to the assessee. Scrutiny will be allotted on a random basis. Assessment of a taxpayer in Delhi could well be carried by an officer sitting in Pune. It will put an end to needless litigation. Best Judgements Assessments under Section 144 will be also now covered under Faceless Assessment.

What is the meaning of Best Judgement Assessment?

The Best Judgment Assessment is a procedure under the Income Tax Act to comply with the principles of natural justice. Vide Section 144 of the Income Tax Act, 1961 the Assessing Officer is under an obligation to make an assessment of the total income or less to the best of his judgment in the following cases:

If the person fails to file a return required under section 139(1) and he has not filed a revised return.

If any person fails to comply with all the terms and conditions stipulated under a notice under section 142 or fails to comply with the directions requiring him to get his accounts audited in terms of section 142(2A).

If any person, after having filed a return fails to comply with all the terms of a notice under section 143(2) requiring his presence or production of evidence and documents; or

If the Assessing officer is not satisfied about the correctness and the completion of the accounts of the assessee if no method of accounting has been regularly employed by the assessee.

While Faceless Assessment and Taxpayers Charter came in force already, Faceless Appeal will be available from September 25, 2020. Under the Faceless Appeals system introduced by the government, appeals will be randomly allotted to any officer across the country and the identity of the officer deciding the appeal will remain unknown. The decisions will be team-based.

Very Important update for Charitable Trusts and Exempt Institution registered under section 80G, 12A or section 12AA : New – Fresh Registration Required : Last Date 31.12.2020

All Charitable trusts and exempt institution which are already registered under section 80G, 12A or section 12AA of Income Tax Act, 1961 will now be required to obtain FRESH REGISTRATION by December 31, 2020.

Provisions of registration under section 80G, 12AA or section 12A will be redundant from 31st December, 2020 and a new section 12AB will come into force with effect from 01st January 2021.

All the existing registered trusts under the erstwhile section 80G, 12A or section 12AA would move to new provision section 12AB.

The new section 12AB proposes to change the registration process by prescribing the time frame for processing the application and validity of such a registration certificate so granted under the new section 12AB.

An order granting registration or approval shall be passed within 3 months of the application. Such registration or approval shall be valid for 5 years.

Similarly, charitable trusts and exempt institutions which already have Section 80G certificate will now be required to reapply for registration or approval by December 31, 2020.

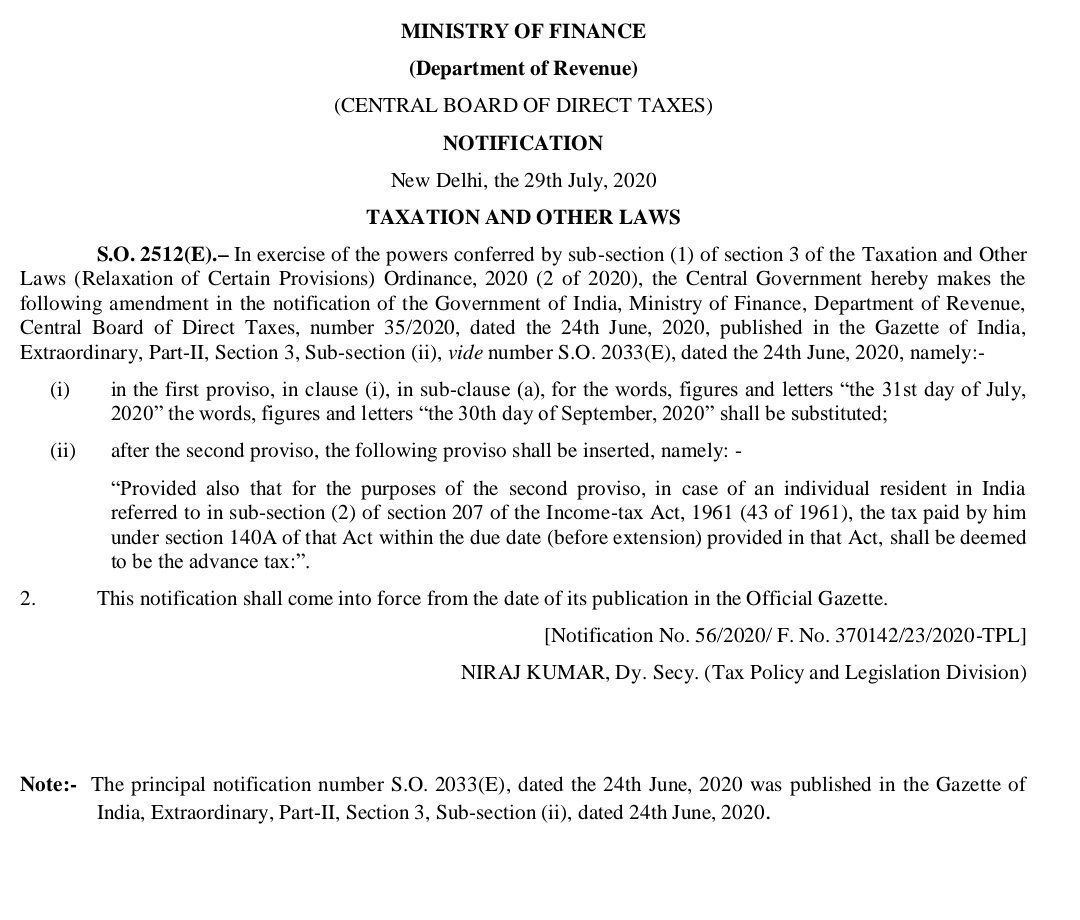

The Central Board of Direct Taxes (CBDT) on Wednesday (July 29) extended the deadline for filing income tax returns for 2018-19 fiscal till September 30 due to corona virus COVID-19 pandemic.

The Central Board of Direct Taxes (CBDT) on Wednesday (July 29) extended the deadline for filing income tax returns for 2018-19 fiscal till September 30 due to coronavirus COVID-19 pandemic.

“In view of the constraints due to the Covid pandemic & to further ease compliances for taxpayers, CBDT extends the due date for filing of Income Tax Returns for FY 2018-19 (AY 2019-20) from 31st July, 2020 to 30th September, 2020,” the Income Tax Department said in a tweet.

It is to be noted that this is the third extension given by the Centre to taxpayers to file both original and revised tax returns for 2018-19 fiscal.

In March, the Centre had extended the due date from March 31 to June 30 due to corona virus COVID-19 pandemic. Later in June, the date was again extended by a month till July 31.

If an individual fails to file the belated ITR, if due, by the deadline (i.e., September 30, 2020), then he/she will not be able to file the income tax return for the financial year 2018-19.

The CBDT has said that an individual can also file a revised ITR for FY2018-19 within this deadline.

The Central Board of Direct Taxes (CBDT) has issued refunds worth Rs 71,229 crore in more than 21.24 lakh cases upto 11th July, 2020, to help taxpayers with liquidity during COVID-19 pandemic, since the Government’s decision of 8th April, 2020 to issue pending income tax refunds at the earliest.

Income tax refunds amounting to Rs. 24,603 crore have been issued in 19.79 lakh cases to taxpayers and corporate tax refunds amounting to Rs. 46,626 crore in 1.45 lakh cases have been issued to taxpayers during COVID-19.

It is stated that the government has laid great emphasis on providing tax related services to the taxpayers without any hassles and is aware that during these difficult times of COVID-19 pandemic, many of the taxpayers are waiting to see that their tax demands and refunds reach finality as quickly as possible.

It is further emphasized that all the refund related cleaning up of the tax demands are being taken up on priority and is likely to be completed by 31st August, 2020.

Also, all applications for rectifications and for giving effect to appeal orders are to be uploaded on the ITBA.

It has been decided to do all the work of rectification and appeal effect on ITBA only.

It is reiterated that taxpayers, for quick processing of their refunds, should provide immediate response to the emails of I-T Department.

A quick response from the taxpayer in this regard would facilitate the I-T Department to process their refunds expeditiously.

Many taxpayers have submitted their responses electronically for rectification, appeal effects or tax credits. These are being attended to in a time bound manner.

All refunds have been issued online and directly into the bank accounts of the taxpayers.

-Through this one time relaxation scheme, ITR for FY 2014-15 to FY 2018-19 can be verified, on or before 30th September 2020. – All such verified ITRs shall be processed on or before 31st December 2020. – ITRs can be verified digitally through EVC or by sending duly signed a copy to CPC Bangalore.

The Central Board of Direct Taxes (CBDT) on Monday notified the one-time relaxation for verification of tax return for the Assessment Year 2015-16, 2016-17, 2017-18, 2018-19 and 2019-20, which are pending due to non-filing of ITR- V form and processing of such returns.

It has been brought to the notice of CBDT that a large number of electronically filed ITR still remains pending with the Income-Tax Department for want of receipt of a valid ITR-V Form at CPC, Bengaluru from the taxpayers concerned.

In law, consequences of non-filing the ITR-V within the time allowed is significant as such a return is/can be declared Non-est in law. Thereafter, all the consequences for non-filing a tax return, as specified in the Income-tax Act,1961 follow.

“The CBDT, in the exercise of powers under section 119 of the Act, in case of returns for Assessment Years 2015-16, 2016-17, 2017-18, 2018-19 and 2019-20 which were uploaded electronically by the taxpayer within the time allowed under section 139 of the Act and which have remained incomplete due to non-submission of ITR-V Form for verification, hereby permits verification of such returns either by sending a duly signed physical copy of ITR-V to CPC, Bengaluru through speed post or through EVC/OTP modes as listed in para 1 above.

Such verification process must be completed by 30.09.2020,” the circular said.

However, the circular clarified that this relaxation shall not apply in those cases, where during the intervening period, the Income Tax Department has already taken recourse to any other measure as specified in the Act for ensuring filing of a tax return by the taxpayer concerned after declaring the return as Non-est.

“CBDT also relaxes the time-frame for issuing the intimation as provided in the second proviso to sub-section (1) of Section 143 of the Act and directs that such returns shall be processed by 31.12.2020 and intimation of processing of such returns shall be sent to the taxpayer concerned as per the laid down procedure.

In refund cases, while determining the interest, provision of section 244A (2) of the Act would apply,” the circular said.

The levy is applicable only for large cash withdrawals. The intent is to minimize cash transactions and expand digital payments to enlarge the ambit of organized transactions over time.

In order to tighten the noose on those who don’t file income tax returns (ITR) despite earning taxable income and discourage cash transactions, the Finance Act 2020 introduced higher TDS (Tax Deducted at Source) rates on cash withdrawals for those who do not file ITR. The rates are applicable from 1 July.

Those who haven’t filed ITR for the past three financial years will have to pay TDS at the rate of 2%, if the amount withdrawn from the bank is above ₹20 lakh but doesn’t exceed ₹1 crore in a financial year. If the amount withdrawn exceeds ₹1 crore, TDS will be deducted at the rate of 5% under Section 194N of the Income-tax Act, 1961, for those who do not file ITR.

However, if you withdraw cash above ₹1 crore in a FY, you will still have to pay TDS whether you file ITR or not. In July 2019, the government, through Section 194N, had first introduced TDS at the rate of 2% on cash withdrawals above ₹1 crore in a financial year. This continues to be applicable.

“It is important to note that TDS shall be required to be deducted only when the aggregate amount of cash withdrawal during the FY by an individual from one or more of his bank accounts exceeds ₹20 lakh or ₹1 crore, as the case may be,” said Parizad Sirwalla, partner and head, global mobility services, tax, KPMG in India.

Further, tax will be deducted only on the amount exceeding the said thresholds. “If the individual withdraws a sum of money on regular intervals, the bank or financial institution will have to deduct TDS from the amount once the total sum withdrawn exceeds the threshold in a FY,” said Sirwalla.

For example, if person A has filed his ITR and if he withdraws cash up to ₹1 crore, then no TDS will be applicable. In case person A withdraws cash, which is more than ₹1 crore, then only 2% TDS will be applicable. If person A has withdrawn ₹1.25 crore in two transaction of ₹75 lakh in and ₹50 lakh, the TDS liability will only be on the excess amount that is ₹25 lakh.

On the other hand, if person B has not filed his ITR for the last three financial years and if he withdraws cash between ₹20 lakh and ₹1 crore, then 2% TDS will be applicable. In case person B withdraws cash which is more than ₹1 crore, then 5% TDS will be applicable.

“In case, the individual does not furnish the PAN to the bank or financial institution, then a TDS at a higher rate of 20% will become applicable,” said Sirwalla.

TDS will be applicable on withdrawals from banks, co-operative banks and post offices. The limit will apply on all accounts in the same bank. So, if you have multiple accounts with the same bank, then TDS will be applicable once you breach the mandatory limit across all the accounts or in any one of the account with the same bank. But for accounts with different banks, the limit will apply separately.

Banks will need to keep track of cash withdrawals and once the limit is breached, they will need to deduct TDS.

“Banks are asking declaration from people to ensure they have filed a return in the past three years or in any one of the last three years. This is done by banks for easier tracking as they wouldn’t know if the person has filed ITR or not,” said Sandeep Sehgal, director, taxes and regulatory, AKM Global.

The purpose of slapping this TDS is to minimize cash transactions and push digital payments.

“The levy is applicable only for large cash withdrawals in excess of ₹20 lakh/100 lakh per annum, as the case may be. The intent is to minimize cash transactions and expand digital payments to enlarge the ambit of organized transactions over time. So if individuals need to avoid this TDS levy, they should ensure that their cash withdrawals are restricted to the bare minimum and that the bulk of their payments happen through banking or digital means,” said Divakar Vijayasarathy, founder and managing partner, DVS Advisors LLP.

Prime Minister Narendra Modi announced several tax measures on the eve of India’s Independence Day last week honouring the honest tax-paying citizen.

Prime Minister Narendra Modi announced several tax measures on the eve of India’s Independence Day last week honouring the honest tax-paying citizen.