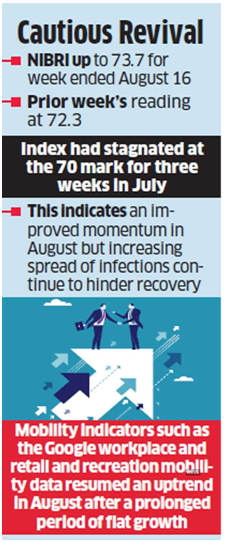

The Nomura India Business Resumption Index inched up to 73.7 for the week ending August 16, over the previous week’s reading of 72.3. This came after the NIBRI, a weekly tracker of the pace at which economic activity normalises, stagnated at the 70-mark for three weeks through July.

The economy sustained an increasing pace of recovery through August so far after a prolonged period of plateauing trends in July, according to a Nomura note on Monday.

The Nomura India Business Resumption Index (NIBRI) inched up to 73.7 for the week ending August 16, over the previous week’s reading of 72.3.

This came after the NIBRI, a weekly tracker of the pace at which economic activity normalises, stagnated at the 70 mark for three weeks through July.

While this indicated an improved momentum in August over the moderation in July, the rising spread of infections continued to hinder recovery.

“Nevertheless, the recovery is uneven, and the risk of reversal in momentum from a second wave of COVID-19 cases joining a ‘rolling wave’ in traditional safer states (in the south and the east) remains high,” the note said.

Mobility indicators such as the Google workplace and retail and recreation mobility data resumed an uptrend in August after a prolonged period of flat growth, Nomura said.

However, this was still materially below pre-pandemic levels, it added.

There was a steady pick up in the labour participation rate 42.2% as against 40.6% in the previous week.

On the other hand, the unemployment rate showed a steady uptrend rising to 9.1% compared to the 8.2% recorded last week, which grew from 7.2% reported the week before that.

The deterioration was spread both over rural and urban areas, the note said.

Power demand also showed a steady trend albeit in the opposite direction with a steep weekly contraction of 6.4% over the 0.8% contraction of the week earlier, it said.

The reserves are hitting the psychological threshold also because benign current account deficits over the last few quarters had allowed RBI to use less of the reserves to finance it.

India’s foreign exchange reserves have climbed tantalizingly close to the $400-billion mark on September 1 on the back of strong foreign portfolio investments into the Indian market, especially the debt segment

The reserves are hitting the psychological threshold also because benign current account deficits over the last few quarters had allowed RBI to use less of the reserves to finance it.

To be sure, the latest $100 billion addition to the reserves has taken close to 10s years. The $300 billion mark was reached in February 2008, while the previous $100 billion was accumulated in a span of just eleven months.

While the rupee remains strong against the dollar at levels of 64 having appreciated 6% so far in 2017, few would have anticipated this strength, especially after the free fall of the currency in mid-2013 when it slipped all the way to 68.85 against the greenback (the forex reserves had plunged by more than $17 billion during this period).

The other critical period for the reserves and currency was in 2008, during the financial crisis when the currency lost almost 25% of its value between May and November. In this period, the reserves fell by a little over $70 billion to $245.8 billion.

Currently, the reserves take care of approximately 12 months of imports; in the past the reserves have typically covered seven to eight months of imports. Interestingly, India has seen the third-highest reserves accretion globally after Switzerland and China, so far in 2017.

According to Indranil Sengupta, chief economist at Bank of India Merrill Lynch, RBI has been intervening fairly aggressively in the forex market and might continue to do so if the dollar weakens but perhaps less so if the greenback was to strengthen.

After a brief overnight pause, the rupee was again caught in a downward spiral and slipped by 12 paise to 64.12 against the US dollar on Thursday on fresh demand for the American currency from banks and importers amid persistent foreign capital outflows. Foreign portfolio investors sold shares worth a net Rs 827 crore on the day.

Meanwhile, India’s CAD, which stood at 0.7% in the fourth quarter of last fiscal is expected to widen sharply to 3% in Q1FY18 due to a sharp deterioration in the merchandise trade deficit. According to Sonal Varma, chief economist at Nomura, the low commodity prices in the last two years have resulted in the CAD narrowing to about 1% of GDP. “With commodity prices marginally higher and a cyclical recovery expected in coming quarters, we expect the current account deficit to widen to a steady state of around 1.5-2.0% of GDP (for FY18),” Varma said.

Currently, as the central bank continues to shore up the reserves, it appears to be depending more on forward purchases than the spot market. This is due to the abundant liquidity in the system which prevents excessive action in the spot market.

MV Srinivasan, vice-president, Mecklai Financial Services believes the RBI is attempting to prevent any appreciation of the rupee beyond 63.80 levels. “The central bank is trying to rein in the excess liquidity in the system through OMO sales and dollar purchases in the spot will counter these measures,” he says.

Srinivasan believes that if the US Federal Reserve begins to reduce its balance sheet size, there could be forex outflows following which the RBI might intervene to stabilise the markets. Net portfolio inflows to the India’s bond and stock markets have been to the tune of $26.7 billion so far in 2017.

A Universal Robots employee demonstrates how a model of their industrial robot arms works in Singapore March 3, 2017.

Foreign precision engineering firms are investing more in Singapore, drawn by strong semiconductor demand and government incentives aimed at re-tooling an economy short of skilled labor.

The city-state is running programs worth billions of dollars to support productivity, automation and research, attracting global chipmakers including U.S.-based Micron Technology Inc and Germany’s Infineon Technologies.

This investment rush into electronics helped the technology sector log 57 percent output growth on average in October-February from a year ago, and kept Singapore from recession late last year.

“I’ve lived in Europe, I’ve lived in Japan, I’ve spent a lot of time in Taiwan and other countries. From a proactive standpoint, Singapore is about as good as it gets,” said Wayne Allan, vice president of global manufacturing at Micron, adding the Singapore government’s long-term vision was key to Micron expanding its investment.

Taking advantage of government grants, Micron is investing $4 billion to make more flash-memory chips in Singapore. It increased output by a third in the second half of last year and expects similar growth in the first half of this year.

Linear Technology Corp, a maker of analog integrated circuits, has opened a third chip testing facility in Singapore, and will produce 90 percent of its global test equipment in the city-state.

All this has created something of a virtuous circle in the semiconductor supply chain, with chip testing equipment supplier Applied Materials reporting record shipments to Singapore last year, said its regional chief, Russell Tham.

It’s unclear how much of this revival in Singapore’s $40 billion chip industry is due to a so-called ultra-super-cycle in the global memory chip sector, and Singapore remains a smaller player than South Korea and Taiwan.

“It is vulnerable to a pull-back,” said Nomura economist Brian Tan. “If there’s a turnaround in the semiconductor industry … it becomes a lot more apparent that the underlying growth momentum is not great.”

MOVING UP

However, there are real signs that the targeted government incentives are helping firms move up the value chain.

One of the larger programs is the Productivity and Innovation Credit, where Singapore has budgeted S$3.6 billion ($2.6 billion) for 2016-18. Another S$400 million automation support package is aimed at small firms, and a S$500 million Future of Manufacturing plan encourages testing new technologies.

The Ministry of Trade and Industry says it encourages manufacturers to “embrace disruptive technologies” such as robotics. “These measures will help ensure the manufacturing sector in Singapore remains globally competitive,” it said, attributing the strong semiconductors performance partly to demand from China’s smartphone market and improved global semiconductor demand.

For Feinmetall Singapore, whose products are used for testing semiconductor wafers, grants covered about two thirds of the $100,000 cost of a needle-bending machine it needed to help overcome an island-wide labor shortage.

“If we use the same methods as before … I don’t think we can expect any growth,” said Sam Chee Wah, the company’s general manager, noting Feinmetall Singapore struggled to retain some workers for much longer than a year, even after nine months of training.

GlobalFoundries Singapore, a wafer maker, has spent $50 million on 77 robots, each able to perform the tasks of 3-4 workers. This has helped the company move up the value chain into parts for self-driving cars and security-related chips for credit cards and mobile payments, says general manager KC Ang.

Singapore now has about 400 robots per 10,000 workers, the world’s second-highest density after South Korea. Most robots are used in electronics, according to the International Federation of Robots.

And further developments are in the pipeline.

AUTOS, IOT

At its Singapore manufacturing hub, Infineon is developing productivity tools such as robotics and automated guided vehicles which it hopes to deploy to other production sites. Dutch chipmaker NXP Semiconductors is also developing vehicle-to-everything technology, enabling vehicles to communicate with each other and roadside infrastructure.

Instead of trying to compete with high-volume producers such as China or Malaysia, Singapore has shifted to higher-end products, said Jagadish C.V., head of Systems on Silicon Manufacturing, another firm making semiconductor wafers.

“So you do the products which others can’t do so easily,” he said, adding his firm had shifted most of its output to specialized products, such as chips used in smartphones.

CK Tan, President of the Singapore Semiconductor Industry Association, noted the global chip industry is automating faster than other sectors because of cost pressure, a need to eliminate or reduce error, and have a consistent process control.

“In Singapore, it’s even more important for us to … look at how to speed up or increase the level of automation because of the lack of skilled resources,” he said. “The industry has recognized it has to move upscale. The government incentives play a part to allow the manufacturing side to be relevant, to be at least cost competitive.”

The Ministry of Trade and Industry said first-quarter growth in manufacturing – up 6.6 percent year-on-year, while overall GDP was up 2.5 percent – was due mainly to output expansion in electronics and precision engineering.

Integrated circuits were Singapore’s biggest export product among non-oil domestic exports in January-March, topping S$6 billion ($4.29 billion), according to trade agency IE Singapore.

Offshore units of Nomura, Standard Chartered and Bank of America Merrill Lynch bought about Rs 3,000 crore of the Rs 3,500 crore on offer. (Photo: Reuters)

Three banks snapped up almost 90 percent of bonds sold by Indian states to foreigners, and turned them into derivatives, raising the prospect of more volatility in one of Asia’s best performing debt markets.

Several market participants involved in the sale said offshore units of Nomura, Standard Chartered (STAN.L) and Bank of America Merrill Lynch (BAC.N) bought about 30 billion rupees ($451 million) of the 35 billion rupees on offer in October, the first window for foreigners to buy in.

Much of that debt was then sold for a hefty fee as derivatives known as total return swaps to offshore clients keen for the bonds’ higher yields, compared with India’s already popular sovereign debt, and with similar guarantees.

In contrast, traditional buyers of the illiquid bonds are state banks, who hold the debt to maturity.

When contacted by Reuters, the three banks declined to comment.

India has been one of the most resilient emerging markets, with foreign buyers taking up about $9.7 billion of debt this calendar year, nearly exhausting available limits on sovereign debt purchases.

Those purchases have helped domestic debt return 7.8 percent so far this year, the highest in Asia, according to HSBC.

Given that appetite and a need to expand its investor base, India let foreigners buy state bonds and also relaxed the investment ceiling in government bonds by around 56 billion rupees in September: the first step in a gradual opening.

“The main objective of (Reserve Bank of India) in opening these limits is to attract diverse and new sets of investors to the Indian bond market,” said a senior foreign bank treasury official based in Mumbai.

“But if eventually the FII (offshore) units of the foreign banks in India get to corner the limits, elbowing out the long term investors, then that leaves open a big risk of these trades unwinding and disrupting the Indian debt market.”

India’s central bank has sought to discourage “bond tourists”, favouring what it calls “real” investors, who would not flit in and out of the market.

Although currency and market risks have been passed on to other buyers, a sharp sell-off could see these investors re-selling the derivatives back to the banks and forcing them to swap the debt or sell at a discount.

But with foreigners owning only 4 percent of Indian government debt versus 47 percent in Indonesia, for example – the impact of even a significant sell-off would likely be muted.

“We are less concerned as the liquidity in IGBs is one of the highest in the region, and foreign positioning remains a very low component of the outstanding market,” said Rohit Arora, interest rate strategist at Barclays in Singapore, referring to Indian government bonds.

The next window for foreigners to buy state government debt is on Jan. 1.

($1 = 66.450 Indian rupees)

(Writing by Clara Ferreira Marques; Editing by Rafael Nam and Jacqueline Wong)

In the midst of foreign entities exiting the Indian mutual fund segment, Invesco, a large global player in asset management, has decided to show a long-term commitment here.

Religare on Wednesday informed the stock exchanges that Invesco Ltd had agreed to raise its stake in Religare Invesco Asset Management Company to 100 per cent, from the existing 49 per cent. It could, say company sources, be a Rs 500-550 crore deal, to be finalised after regulatory clearances.

“Invesco had a call option to increase their stake to 100 per cent by March 2016. Invesco decided to announce it ahead of the deadline, so that the regulatory clearance could be in place (by then),” said a company official.

MANAGING ASSETS

Foreign players exiting MF

Goldman Sachs sold to Reliance MF

Pinebridge sold to Kotak AMC

ING sold to Birla Sunlife MF

Morgan Stanley to HDFC MF

Daiwa sold to SBI MF

Fidelity sold to L&T Finance

Foreign players increasing MF India presence

Invesco agrees to increase stake to 100% in Religare Invesco fund house

Nippon agreed to increase stake to 49% in Reliance Mutual Fund

Schroders acquired 25% stake in Axis Mutual Fund

The reason for the sale by Religare was not disclosed to the stock exchanges. Sources indicated it could be due to the promoters wanting to monetise some assets to meet other financial obligations. Religare’s shares reacted negatively to the announcement, with a fall of nearly two per cent on Thursday morning.

This deal marks the bucking of a trend, with seven foreign entities quitting the fund management space in the past seven years. The latest was the buyout of Goldman Sachs’ Indian asset management business by Reliance MF. Reportedly, Nomura is also planning to end its joint venture with Life Insurance Corporation, in LIC Nomura MF. “We are excited about the long-term prospects of the important Indian market. By taking full ownership of this business, we will further deepen our presence in India and enhance our ability to meet client needs across the globe,” said Andrew Lo, head of Asia-Pacific for Invesco.

Globally, Invesco manages Rs 52.8 lakh crore. Outside of America, it is the largest fund manager in Britain and also has operations in other parts of Europe, Canada and Asia.

Religare Invesco MF managed Rs 21,593 crore of assets as of end-September. Invesco first invested in Religare in 2013 when the assets under management stood at Rs 14,000 crore. The global firm had bought stake from the promoters, Delhi-based brothers Malvinder and Shivinder Singh, for Rs 450 crore.

Invesco says it has decided to continue with the same management team, headed by Saurabh Nanavati as chief executive.

“We will look at introducing more products from Invesco’s global portfolio which will be suitable to the sensibilities of Indian customers,” said another company official.

India e-commerce story strong, to hit $35 bn by 2019: Nomura

Indian e-commerce sector’s growth looks strong and is expected to reach $35 billion by 2019, says a report.

“The growth of India e-commerce remains strong, tracking our expectations of reaching $35 billion by 2019,” Nomura said in a research report.

The report, however, noted that the focus needs to move towards the roadmap to profitability, where “some progress is visible but a lot is still in the works”.

It further said that there are areas where significant progress needs to be made and that include diversification of categories, less discounting, improved logistics and benign legislation like GST. On these fronts, there are “still works in progress and remain big areas of investment”, the report said.

According to Nomura, the festive sale season kicked off with a bang for Indian eCommerce players, but still is lower in comparison with China and the US.

In China, Alibaba during its ‘Singles Day’ on November 11, 2014 sold goods worth $9 billion, while in the US, during Cyber Monday (Monday after Thanksgiving) and Black Friday, sales of around $3 billion each were recorded in 2014.

In comparison, the quarterly expectations for India’s holiday sales are closer to $4 billion.

Typically the festive season (October to December) accounts for about 35-40 per cent of annual sales for the e-commerce firms.

According to Technopak, e-commerce in India recorded around $7 billion in annual sales in FY15, and is expected to generate about $10 billion in FY16, leading to sales expectations of around $4 billion for the e-commerce firms this festive season.