Keeping minimum change and with the view to minimise compliance burden, The Central Board of Direct Taxation (CBDT) has notified new income tax return forms — ITR-1 to ITR-7, for the Assessment Year 2021-22, the ministry of finance said in a statement on April 1.

In this new ITR form for AY 2021-22, the taxpayers will now have dedicated space in each of the ITR forms — Sahaj (ITR-1), Form ITR-2, Form ITR-3, Form ITR-4 (Sugam), Form ITR-5, Form ITR-6, Form ITR-7 and Form ITR-V to describe their investments, CBDT said.

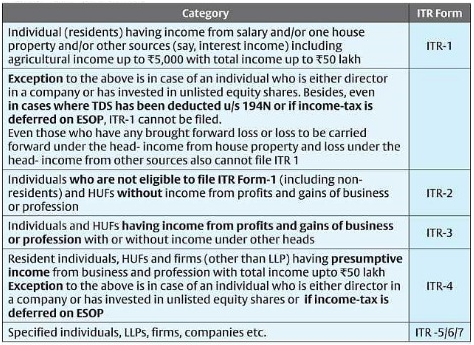

ITR Form 1 (Sahaj) and ITR Form 4 (Sugam) are simpler Forms that cater to a large number of small and medium taxpayers. Sahaj can be filed by an individual having income up to Rs 50 lakh and who receives income from salary, one house property / other sources (interest etc).

Similarly, Sugam can be filed by individuals, Hindu Undivided Families (HUFs) and firms (other than Limited Liability Partnerships (LLPs) having total income up to Rs 50 lakh and income from business and profession computed under the presumptive taxation provisions.

Individuals and HUFs not having income from business or profession (and not eligible for filing Sahaj) can file ITR-2, while those having income from business or profession can file ITR Form 3.

Persons other than individual, HUF and companies i.e. partnership firm, LLP etc can file ITR Form 5. Companies can file ITR Form 6. Trusts, political parties, charitable institutions etc claiming exempt income under the Act can file ITR-7.

There is no change in the manner of filing of ITR forms as compared to last year, the CBDT said.

Key points :

♦ ITR-1 cannot be filed in case tax has been deducted u/s 194N

As per, Section 194N – TDS 194N is required to be deducted if amount of cash withdrawn exceeds –

- Exceeds Rs 20 lakhs in case of non-filers of return

- Rs 1 crore in all other cases

from banking company or co-operative bank or post-office from one or more accounts maintained by taxpayer.

If tax has been deducted u/s 194N, a person can file –

- ITR 2

- ITR 3

- ITR 4

♦ TDS deducted u/s 194N cannot be carried forward to subsequent years.

It means Credit for tax deducted u/s 194N can be taken in previous year relevant to Assessment year in which tax has been deducted.

♦ Option has been given to Individual or HUF as per Section 115BAC.

From A.Y 2021-22 option is available to Individual & HUF whether to opt New Scheme or not. This option for lower tax regime, by foregoing certain exemptions and deductions, is given to Assessees to select new scheme-Section 115BAC and are required to file Form-10IE before filing the return u/s 139(1).

♦ Change in Schedule 112A-LTCG from sale of equity share or unit of equity oriented fund on which STT is paid.

Sale price per share/unit now added in Schedule 112A, which was not earlier provided.

♦ Dividend also taxable from A.Y 2021-22- As we know Dividend Income taxable from A.Y 2021-22 in hands of Assessee from A.Y 2021-22 so we are required to give quarterly break-up of Dividend received in order to get relief from interest levied u/s 234C.

♦ Changes in Section 44AB- The threshold limit to get books of account audited increased from Rs 1 crore to 10 crores, if the following conditions are satisfied-

- His aggregate of all receipts in cash during the previous year does not exceeds 5 % of such receipts.

- His aggregate of all payments in cash during the previous year does not exceeds 5 % of such payments