Move to weed out the assessees from GST net will ensure effective tax base

The Central Board of Indirect Taxes and Customs (CBIC) has initiated a process to weed out approximately 12 lakh Goods and Services Tax (GST) assessees who have fallen off the tax map.

“The CBIC has communicated to field officers to take the process further. Now, field officers will issue show-cause notices, which is just a formality but a requirement under the law, and then complete the process for deregistration,” a Finance Ministry official told BusinessLine.

Currently, there are over 1 crore registered assessees on the GST Nework (GSTN), but the number of those who file returns is much less.

Under GST rules, any entity registered under the previous Sales Tax–VAT (Value-Added Tax), Central Excise Duty of Service Tax regulations was required to be enrolled under the GST and get provisional certificates.

However, if the turnover of the entity is less than the GST threshold and he/she is not willing to go for voluntary registrations, such assessees had the option to get the provisional registration cancelled and move out of the GST net. However, many assessees fail to complete the process, and so they continued to be a part of the GST-assessee base.

GST was implemented from July 1 last year. In the very first year, the number of registered assessees increased by 72.5 per cent to 1.14 crore. Of these, 66.17 lakh were existing taxpayers, that is, those registered under previous VAT/Sales Tax, Central Excise or Service Tax regime; the remaining were new ones. The Government believes that the new assessees came into the net as a result of demonetisation, which resulted in the formalisation of the economy, prompting more and more people to get registered.

During the pre-GST regime, States had different slabs for registration under VAT/ST, which was as low as ₹1 lakh and could go up to ₹10 lakh: the thresholds for Service Tax and Central Excise were ₹10 lakh and ₹1.5 crore, respectively. Now the universal threshold is ₹20 lakh (or ₹10 lakh in some States), which means there will be fewer people paying tax and filing returns.

Another Finance Ministry official said that while a wider tax base is good, there is also a need to ensure an ‘effective’ tax base; the latest initiative will help achieve that. This kind of a tax base will serve two purposes: it will lighten the burden on the GSTN, and it will give a real picture of the indirect tax regime.

Filing of Income Tax Returns registers an upsurge of 71% up to 31st August,2018

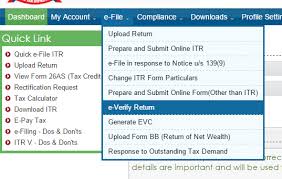

There has been a marked improvement in the number of Income Tax Returns (ITRs) filed during FY 2018 (upto 31/08/2018, the extended due date of filing) compared to the corresponding period in the preceding year.

The total number of ITRs e-filed upto 31/08/2018 was 5.42 crore as against 3.17 crore upto 31/08/2017, marking an increase of 70.86%.

Almost 34.95 lakh returns were uploaded on 31/08/2018 itself, being the last date of the extended due date of filing of ITRs.

A remarkable increase is seen in the number of ITRs in 2 categories ie ITRs filed by salaried Individuals (ITR-1& 2) as also those availing the benefit of the Presumptive Taxation Scheme (ITR-4).

The total number of e-returns of salaried Individual taxpayers filed till 31/08/2018 increased to 3.37 crore from 2.19 crore returns filed during the corresponding period of 2017, registering an increase of 1.18 crore returns translating into a growth of almost 54%.

A commendable growth has been witnessed in the number of returns e-filed by persons availing the benefit of Presumptive Tax, with 1.17 crore returns having been filed upto 31st August, 2018 compared to 14.93 lakh returns upto 31st August, 2017 registering a massive increase of 681.69%.

The increase in the number of returns reveals a marked improvement in the level of voluntary compliance of taxpayers which can be attributed to several factors, including the impact of demonetisation, enhanced persuasion & education of taxpayers as also the impending provision of late fee which would be effective on late filing of returns.

This is indicative of an India moving steadily towards a more tax compliant society & reflects the impact of continuous leveraging of technology to improve taxpayer service delivery.

MCA extends due date of DIR -3KYC / E-KYC of Directors

In order to update the Directors database of The Ministry of Corporate Affairs(MCA), MCA has requested all Directors holding a DIN to complete DIN KYC before 15th September 2018.

To complete DIN KYC, the Director would be required to file a form known as DIR-3 KYC or DIN e-KYC.

The notification issued by Ministry of Corporate Affairs has been reproduced below:

Government of India MINISTRY OF CORPORATE AFFAIRS

Notification

New Delhi, dated 21st August 2018

G.S.R. …… (E).-In exercise of the powers conferred by sections 396,398,399, 403 and 404 read with sub-sections (1) and (2) of section ‘1-69 of the Companies Act, 2013 (18 of 2013), the Central Government hereby makes the following rules further to amend the Companies (Registration Offices and Fees) Rules, 2014, namely:-

(1) These rules may be called the Companies (Registration Offices and Fees) Fourth Amendment Rules, 2018.

(2) They shall come into force from the date of their publication in the Official Gazette.

In the Companies (Registration Offices and Fees) Rules, 2014, in the Annexure, under the head VII, for note below Fee for filing e-form DIR-3 KYC, the following note shall be substituted, namely:-

“for the current financial (2018-2019), no fee shall be chargeable till

the 15th September 2018 and fee of Rs.5000 shall be payable on or after the 16th September 2018”.

[F. No. 01/16/2013 CL-V (Pt-I)]

Sd/-

K.V.R MURTY, JOINT SECRETARY

Purpose of E-form DIR-3 KYC

The main purpose of e-form DIR-3 KYC is to collect the latest information about the directors of all companies. The information to be provided while completing eKYC procedures include Aadhar, PAN, Passport number, address, phone and email. The information submitted must be authenticated by completing one-time-password (OTP) verification and by signing with Digital Signature of Director and a practising Chartered Accountant.

Applicability

All directors having a DIN as on 31st March of 2018 must file e-form DIR-3 KYC on or before 15th September of 2018. For all Directors who obtained DIN after 31st March, 2018, DIR e-KYC must be filed next year.

Documents Required

The following are the documents required to file E-form DIR-3 KYC:

PAN Card for identity proof

Aadhar Card for address proof

Recent passport size photographs

Personal Mobile Number and E-mail ID of director for OTP Verification

Digital Signature Certificate of the director (DSC) that must be registered on MCA Portal

Passport (if the person holds a foreign citizenship)

Certifying Authority

The E-form DIR-3 KYC has to be duly certified by the Practicing Chartered Accountant (PCA), Practicing Company Secretary (PCS) or Practicing Cost Accountant.

Penalties

If the DIN holders do not file DIR-3, the MCA will mark them as deactivated. If the DIN holder files e-form DIR-3 KYC after 31st August 2018, a fee of Rs. 5,000 will be charged.

Time Limit

All directors to whom DIN has been allocated as of March 2018, the e-form DIR-3 KYC has to be filed by September 15, 2018. Originally, the MCA had provided a due date of 31st August which was subsequently changed to 15th September.

The Central Government has notified that the Form GSTR 3B for each month from July 2018 to March 2019 required to be filed by 20th of next month.

A Notification issued by the Central Board of Indirect Taxes and Customs (CBIC) has said that “the return in FORM GSTR-3B of the said rules for each of the months from July, 2018 to March, 2019 shall be furnished electronically through the common portal, on or before the twentieth day of the month succeeding such month.

“Every registered person furnishing the return in FORM GSTR-3B of the said rules shall, subject to the provisions of section 49 of the said Act, discharge his liability towards tax, interest, penalty, fees or any other amount payable under the said Act by debiting the electronic cash ledger or electronic credit ledger, as the case may be, not later than the last date, as specified in the first paragraph, on which he is required to furnish the said return,” the Notification said.

GSTR-3B is a monthly return. All regular taxpayers need to file this return till June 2018. Taxpayers can file their return on GST Portal. Taxpayers have to file this return by 20th of the subsequent month.

CBDT extended the last date to August 31 to file income tax return

The Central Board of Direct Taxes (CBDT) has extended the due date for filing of Income Tax Returns (ITR) to 31st August, 2018. Earlier, the due date for filing of ITR for Assessment Year 2018-19 was July 31, 2018.

As the due date has been coming closer, the Board had received several requests from the tax practitioners body and the Institute of Chartered Accountants of India (ICAI) requesting a due date extension due to several reasons.

CBDT stated in a circular issued today, “The due date for filing of Income Tax Returns for Assessment Year 2018-19 is 31.07.2018 for certain categories of taxpayers. Upon consideration of the matter, the Central Board of Direct Taxes (CBDT) extends the ‘due date’ for filing of Income Tax Returns from 31st July, 2018 to 31st August, 2018 in respect of the said categories of taxpayers.

Generally, the income tax department extends the deadline by only a few days, but this year the deadline has been extended by full one month.

Kuldip Kumar, partner and leader, personal tax, PwC India, said, “Although due date extended.. those who have taxes to pay should pay before July 31 to save additional one month interest under section 234B.”

So, now if you don’t file ITR by the end of July then it won’t be treated as a belated return, as the new deadline is August 31, 2018. But if you miss the deadline of August 31, then according to the Income Tax Act, for returns pertaining to any financial year the last date for late return would be the end of the relevant assessment year. For example: For Financial Year 2017-18 (AY 2018-19), the last date would be 31 March 2019, and it would be your last opportunity to file the return.

From the current Assessment Year onwards, non-filing of ITR before due date will invite late fee of Rs. 1,000/5,000/10,000 as the case may be, under section 234F of the Income Tax Act.

The Board had notified the new Income Tax Return forms for the assessment year 2018-19 on April 5. The income Tax department has launched all the income tax forms for e-filing after more than a month of them being notified.

Further, due to GST and the over burden of compliance procedure, the tax practitioners were unable to finish their IT works. It is in this background, the people urged the Board to extend due date.

India’s GDP amounted to $2.597 trillion at the end of last year, against $2.582 trillion for France

India has become the world’s sixth-biggest economy, pushing France into seventh place, according to updated World Bank figures for 2017. India’s gross domestic product (GDP) amounted to $2.597 trillion at the end of last year, against $2.582 trillion for France. India’s economy rebounded strongly from July 2017, after several quarters of slowdown blamed on economic policies pursued by Prime Minister Narendra Modi’s government.

India, with around 1.34 billion inhabitants, is poised to become the world’s most populous nation, whereas the French population stands at 67 million. This means that India’s per capita GDP continues to amount to just a fraction of that of France which is still roughly 20 times higher, according to World Bank figures.

Manufacturing and consumer spending were the main drivers of the Indian economy last year, after a slowdown blamed on the demonetisation of large banknotes that Modi imposed at the end of 2016, as well as a chaotic implementation of a new harmonised goods and service tax regime.

India has doubled its GDP within a decade and is expected to power ahead as a key economic engine in Asia, even as China slows down.

According to the International Monetary Fund, India is projected to generate growth of 7.4% this year and 7.8% in 2019, boosted by household spending and a tax reform. This compares to the world’s expected average growth of 3.9%.

The London-based Centre for Economics and Business Research, a consultancy, said at the end of last year that India would overtake both Britain and France this year in terms of GDP, and had a good chance to become the world’s third-biggest economy by 2032.

At the end of 2017, Britain was still the world’s fifth-biggest economy with a GDP of $2.622 trillion. The US is the world’s top economy, followed by China, Japan and Germany.

Ahead of China, India to remain fastest growing economy in FY19 & FY20

India will continue to be the fastest growing major economy, ahead of China, with 7.3% growth rate in 2018-19 and 7.6% in 2019-20, the Asian Development Bank (ADB) said on Thursday.

The growth in India will be driven by increased public spending, higher capacity utilisation rate and uptick in private investment, said the ADB supplement to the Asian Development Outlook (ADO).

While retaining India’s growth rate for current fiscal and the next, ADO said economic growth in China would decelerate to 6.6% in 2018 and further to 6.4% in 2019. China’s growth rate was 6.9% in 2017.

On India, it said: “In sum, the GDP growth forecast for FY2018 (ending March 2019) is maintained at 7.3%. Growth in FY2019 is expected to rise to 7.6% as measures taken to strengthen the banking system bolster private investment and as benefits kick in from the goods and services tax. Any further increase in oil prices poses a downside risk to growth.”

The ADB said India was the dominant economy in the South Asia sub-region with its growth gaining momentum at 7.7% in the last quarter ended March of 2017-18, the highest rate of growth since first quarter of 2016-17.

This pushed full-year growth to 6.7% (2017-18), a tad higher than estimated in ADO 2018, largely driven by government spending for both consumption and public administration.

“In the first half of 2018-19, the growth rate is expected to benefit from a low base. Other key drivers of growth include an uptick in public consumption, which is typical before elections, and a recovery in exports following shortages of working capital related to a new goods and services tax,” said the ADO supplement.

In India, the private consumption is expected to grow at a healthy rate as disruption caused by demonetisation in 2016 fades. Capacity utilisation rates are at their highest in four years and should provide incentives to firms to invest.

Growth in Asia and the Pacific’s developing economies for 2018 and 2019 will remain solid as it continues apace across the region, despite rising tensions between the US and its trading partners.

“South Asia, meanwhile, continues to be the fastest growing sub-region, led by India, whose economy is on track to meet fiscal year 2018 projected growth of 7.3% and further accelerating to 7.6% in 2019, as measures taken to strengthen the banking system and tax reform boost investment,” it said further.

Developing Asia is largely on track to meet growth expectations as set out in April in Asian Development Outlook 2018 (ADO 2018), said the report. The regional gross domestic product (GDP) is forecast to expand by 6% in 2018 and 5.9% in 2019, the rate envisaged in April, ADO supplement said.

In April, ADO had said that India’s economic growth would rise to 7.3% this fiscal and further to 7.6% in the next financial year, retaining the fastest-growing Asian economy tag, on back of GST and banking reforms.

“Although rising trade tensions remain a concern for the region, protectionist trade measures implemented so far in 2018 have not significantly dented buoyant trade flows to and from developing Asia,” said ADB chief economist Yasuyuki Sawada. “Prudent macroeconomic and fiscal policy-making will help economies across the region prepare to respond to external shocks, ensuring that growth in the region remains robust,” he added.

ADO has also retained the combined growth forecast for the major industrial economies — the US, the Euro zone and Japan — as growth in the US and the Euro area remains robust.

In Japan, though, unanticipated contraction in the first quarter prompts slight revision of the 2018 growth forecast, it added.

However, ADB said that the rise in protectionist trade measures from the US and countermeasures from China and other countries “poses a clear downside risk to the outlook for developing Asia”.

The ADO supplement has factored in the tariffs imposed by July 15.

“The risk of further ratcheting up of protectionist measures could undermine consumer and business confidence and thus developing Asia’s growth prospects,” ADB said.

On price rise front, ADO has raised the South Asia inflation forecast to 5 per cent from 4.7 per cent, mainly to accommodate an increase in the forecast for India, but kept at 5.1 per cent for 2019.

“The upgrade in the 2018-19 inflation forecast for India from 4.6 per cent to 5 per cent responds to higher oil prices, significant depreciation of the Indian rupee in the past few months, and generous increases announced on 4 July in minimum support prices for summer crops,” the ADO said.

For developing Asia, it has revised down inflation projections from 2.9 per cent to 2.8 per cent in 2018 and from 2.9 per cent to 2.7 per cent in 2019 citing domestic factors to help contain inflationary pressures.

“As the US monetary policy normalises, central banks in the region act to spare their currencies’ sharp depreciation and to subdue inflation. Further, some governments have reintroduced subsidies to contain the effects of rising food and oil prices.”