CBDT confirms News of Income Tax Return filing due date extension in Social Media is Fake

CBDT – extension in due date for non-tax audit cases is fake and there are no such plans to extend this deadline beyond 31st July, 2018

CIRCULAR No.4/2018

F.No.370889/25/2018 Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes

New Delhi, Dated 21st July, 2018

Order under section 139(1) of the Income-tax Act, 1961 (‘the Act’)

This Circular is issued in pursuant to 139(1) of the Tax Act, 1961 is to clarify that rumorsspreading across in media regarding extension in due date for non-tax audit is fake and no such plans to extend this deadline beyond 31st July, 2018. The department already received over 1 crore returns filed electronically.

As per Section 234F of the Income Tax Act, from 1st April 2018, the penalty for late filing income tax return would be as

(a) five thousand rupees, if the return is furnished on or the 31st day of December of the assessment year;

(b) ten thousand rupees in any other case:

Provided further that if the total income of the person not exceed five lakh rupees, the fee payable under this section shall not exceed one thousand rupees. Therefore, the assessees are hereby asked to file their ITRs before the due date to avoid the penalty.

(Sanyam Suresh Joshi)

DCIT, CBDT

Copy to:

1. PS to FM/OSD to FM/PS to MoS(F)/OSD to MoS(F)

2. PS to Secretary (Revenue)

3. Chairman, CBDT

4. All Members, CBDT

5. All Pr. DGsIT/Pr. CCsIT

6. All Joint Secretaries/CsIT, CBDT

7. Directors/Deputy Secretaries/Under Secretaries of CBDT

8. DIT (RSP&PR)/Systems, New Delhi

9. The C&AG of India (30 copies)

10. The JS & Legal Adviser, Ministry of Law & Justice, New Delhi

11. The Institute of Chartered Accountants of India

12. All Chambers of Commerce

13. CIT (M&TP), Official Spokesperson of CBDT

14. O/o Pr. DGIT (Systems) for uploading on official website

SEBI has proposed giving the board of directors of the company the authority to take appropriate action after conducting an investigation against the individual or firm that violates any regulations or submits a false certificate or report.

India’s capital market regulator has proposed amendments to tighten laws governing auditors and other third-party individuals hired by listed companies for auditing financial results, among other things.

The Kotak Committee, formed to come up with proposals for improving corporate governance, last year recommended that the Securities and Exchange Board of India (SEBI) should have clear powers to act against auditors and other third-party individuals or firms with statutory duties under the securities law.

Auditing lapses have caused several frauds to go unnoticed for years and the capital market regulator has had no direct control on the auditing firms.

SEBI has proposed giving the board of directors of the company the authority to take appropriate action after conducting an investigation against the individual or firm that violates any regulations or submits a false certificate or report.

The proposed changes come months after Punjab National Bank, India’s second largest state-run lender, stunned markets after uncovering a $2 billion loan fraud that had gone undetected for years.

Merchant bankers, credit rating agencies, custodians, among others, are registered and regulated by SEBI but chartered accountants, company secretaries, valuers and monitoring agencies do not come under any direct regulators.

The amendments would mean auditors must ensure certificates or reports issued by them are true in all material respects and they must exercise all due care, skill and diligence with respect to all processes involved in issuance of the report or certificate.

The auditors would be responsible to report in writing to the audit committee of the listed company or the compliance officer on any violation of the securities law they noticed.

In January, SEBI barred Price Waterhouse from auditing listed companies in India for two years after an investigation into a nearly decade-old accounting fraud case in a software services company that became India’s biggest corporate scandal.

SEBI has sought feedback and comments on the draft regulations over the next 30 days.

ICAI have launched Unique Document Identification Number (UDIN) facility which is a unique number, which will be generated by the system for every document certified/ attested by a Chartered Accountant and registered with the UDIN portal available at https://udin.icai.org/ with effect from 1st July 2018.

It has been noticed that financial statements and documents were being certified/attested by third persons, in lieu of Chartered Accountants. As these statements are being relied upon by the authorities as true statements and certificates, UDIN can be generated by a practicing CA by registering his/her documents/ certificates on UDIN Portal for verification.

A practicing Chartered Accountant can generate a UDIN for certificate/ document attested by him either in individual capacity or as a partner.

At present, this facility is recommendatory. But ICAI is mulling to make the same compulsory in near future, so as to curb the menace of fake or forged documents.

No change is possible in the data already registered by a Chartered Accountant in the online system. Therefore, members are requested to thoroughly check the details in preview option before submission of their application.

Information filled in can be edited/ modified any number of times before the submission. But once it is submitted, it cannot be edited.

The UDIN once generated can be withdrawn or cancelled with narration. Hence if any user search for this UDIN, appropriate narration indicated by Member with the date of revoke will be displayed for reference.

As part of updating its registry, MCA would be conducting KYC of all Directors of all companies annually through a new eform viz. DIR-3 KYC to be notified and deployed shortly.

Accordingly, every Director who has been allotted DIN on or before 31st March, 2018 and whose DIN is in ‘Approved’ status, would be mandatorily required to file form DIR-3 KYC on or before 31st August,2018.

While filing the form,the Unique Personal Mobile Number and Personal Email ID would have to be mandatorily indicated and would be duly verified by One Time Password(OTP).

The form should be filed by every Director using his own DSC and should be duly certified by a practicing professional (CA/CS/CMA).

Filing of DIR-3 KYC would be mandatory for Disqualified Directors also.

After expiry of the due date by which the KYC form is to be filed,the MCA21 system will mark all approved DINs (allotted on or before 31st March 2018) against which DIR-3 KYC form has not been filed as ‘Deactivated’ with reason as ‘Non-filing of DIR-3 KYC’.

After the due date filing of DIR-3 KYC in respect of such deactivated DINs shall be allowed upon payment of a specified fee only, without prejudice to any other action that may be taken.

The Securities and Exchange Board of India (Sebi) on Thursday eased several rules relating to Initial Public Offers (IPO), rights issues, buybacks and takeovers. The regulator’s board approved these changes as also those relating tenures of managing directors of market intermediaries. The capital markets watchdog reduced the time for announcing the price band of initial […]The Securities and Exchange Board of India (Sebi) on Thursday eased several rules relating to Initial Public Offers (IPO), rights issues, buybacks and takeovers.

The regulator’s board approved these changes as also those relating tenures of managing directors of market intermediaries. The capital markets watchdog reduced the time for announcing the price band of initial public offers (IPO) from five working days before the opening of the issue to two working days. This will give companies more time to fix the price band.

Companies now need to provide investors with financial disclosures — for public issues and rights issues — for only three years. Currently, information is provided in the offer documents for five years. Also, companies need to provide only consolidated audited financial disclosures in the IPO offer document; audited standalone financials of the issuer and subsidiaries must be disclosed on the company website.

Following a board meeting on Thursday, the capital markets regulator tweaked the buyback norms. The buyback period has been defined as the time between the board resolution or the date of declaration of results for a special resolution authorizing the buyback of shares and the day on which the shares are paid.

Also, Sebi has amended the takeover rules. It has given companies additional time to revise the open offer price upwards till one working day before the start the tendering period.

The Sebi board also approved some recommendations of R Gandhi committee on regulations relating to market infrastructure institutions (MIIs). For rights issues the threshold for submission of the draft letter of offer to Sebi has been increased to Rs.10 crore as against the earlier prescribed Rs 50 lakh. The regular also tweaked the rules relating to the underwriting of all non-SME public issues. If 90% of the fresh issue of share is subscribed, the underwriting will be restricted to that portion only. Accordingly, the requirement to underwrite 100% of the issue without regard to the minimum subscription requirements has been deleted.

Sebi also reduced minimum anchor investor size to Rs 2 crore from the existing Rs 10 crore, for SME issuances. This will allow companies to attract more anchor investors for an issue.

The board has permitted eligible domestic and foreign entities to hold up to 15% shareholding in case of Depository and Clearing Corporation. Moreover, multilateral and bilateral financial institutions, as notified by the government, have also been recommended to hold up to 15% in an MII. Moreover, Sebi has decided to limit the tenure of managing directors of an MII for a for a maximum of two terms of up to 5 years each or up to 65 years of age, whichever is earlier. The requirement would also apply to incumbent MDs of MIIs.

The regulator is also looking into the issues regarding IPO ICICI Securities in ICIC AMC bought the large stake.The regulator had sought details of a significant investment made by ICICI Prudential Mutual Fund in the IPO of ICICI Securities. “Yes we are looking into that, and we have sought some information from them, and we are yet to get their replies,” Tyagi said.

Last week, the Parliament cleared a bill to further amend the Companies Act.

The financial statements and annual returns of all company must be filed on time with the ROC / MCA each year. As per Companies Act, 2013, non-filing of annual return is an offence, consequences of which affect the directors, as well as the company.

Hence, it is a must for every company to file with the MCA:

1. The annual return within 60 days of the Annual General Meeting and

2. The Financial Statement, within 30 days of the Annual General Meeting.

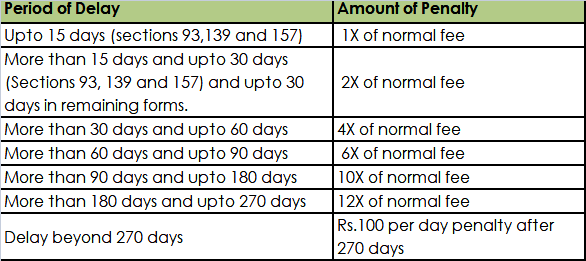

The various consequences and the penalties for not filing annual return of a company (Forms MGT-7 & AOC-4) are highlighted here.

A. Consequences – for Directors

The Directors of a company are responsible for ensuring the compliance of the company with all applicable rules and regulations. When a company defaults on compliance or dues payable, the Directors are held responsible for the default. The following are penal consequences for a Director of a company for default of non-filing of the Annual Return.

Director Disqualification

In case a company has not been filed its Annual Return for three continuous financial years, then every person who has been a director or is currently the director of the specific company could be disqualified under the Companies Act, 2013. If a Director is disqualified, his/her DIN would become inactive and the person would not be eligible to be appointed as a Director of any company for a period of five years from the date of disqualification. Further, disqualified Directors would not also be allowed to incorporate another company for a period of five years.

Fine & Imprisonment

A director of the company can be punished if the company has not been filed even after 270 days from the date when the company should have originally filed with additional penalty. Any Director who has defaulted in the filing of annual return of a company can also be penalized with an imprisonment of a term extended up to six months or with a fine of an amount not lesser than fifty thousand rupees and it might extend up to five lakh rupees, or with both imprisonment and fine. However, this provision provided under the Companies Act, 2013 is rarely used.

In addition, if any information filed by a Director or any other person in the annual return is false by any nature or if he/she failed to mention any fact or material that is true can be punished with imprisonment for a term which is not lesser than six months and which could extend up to 10 years. Further, he/she can also be liable for payment of a fine which is not lesser than the amount subject to the fraud involved and it may extend to an amount three times of the sum concerned with the fraud.

B. Consequences of Default – For Company

The following are some of the penal consequences for a company that has not filed its annual return:

Penalty

Normally, the Government fee for filing or registering any document under the Companies Act required or authorized to be filed with the Registrar is Rs.200. A private limited company would be required to file form MGT-7 and form AOC-4 each year and the government fee applicable if filed on time would be Rs.400. In case of delay in filing of annual return, the penalty as mentioned would be applicable:

The penalty for not filing a company’s annual return (Form MGT-7 and Form AOC-4) is increased to Rs.100 per day w.e.f.July 1, 2018.

Strike-Off

In case the company has not filed its Annual Return for the last two financial years continuously, then such companies would be termed as an “inactive company”. On such a classification, the bank account of the company could be frozen. Further, the Registrar could also issue a notice to the Company and initiate strike-off of the company from the MCA records.

In case you need any assistance to file annual return for your company, you can contact us at Director@Sunkrish.com

Taxpayer would be required to approach the concerned jurisdictional tax officer to get the password for the GST Identification Number (GSTIN) allotted to the business

The Finance Ministry on Thursday said that GST registrants can approach jurisdictional tax officer with valid documents to change the e-mail and mobile number recorded against their GST identification number (GSTIN).

The revenue department had received complaints from taxpayers that the intermediaries who were authorised by them to apply for registration on their behalf had used their own e-mail and mobile number during the process.

These intermediaries are not sharing the user details with the taxpayers.

“With a view to address this difficulty of the taxpayer, a functionality to update e-mail and mobile number of the authorised signatory is available in the GST system.

“The e-mail and mobile number can be updated by the concerned jurisdictional tax authority of the taxpayer,” the ministry said in a statement.

Taxpayer would be required to approach the concerned jurisdictional tax officer to get the password for the GSTIN allotted to the business. Taxpayers can check jurisdiction through ‘Search Taxpayer’ option available on GST portal.

Taxpayer would be required to provide valid documents to the tax officer as proof of his/her identity and to validate the business details related to his GSTIN. Following this, the officer would authenticate the activity and enter the new e-mail address and mobile number provided by the taxpayer.

After uploading of the documents, tax officer will reset the password for GSTIN in the system and username and temporary password reset will be communicated to the e-mail address as entered by the officer.

Taxpayer would then have to login on GST portal using the username and temporary password e-mailed to him. The username and password can now be changed by the taxpayer.