Bad debts at Indian lenders, especially state-run banks, have climbed to a 15-year high and may increase further, a central bank study showed.

Bad debts at Indian lenders, especially state-run banks, have climbed to a 15-year high and may increase further, a central bank study showed. Under the baseline scenario in a “macro stress test,” the industry’s gross bad-loan ratio may increase to 10.2 percent by March 2018 after climbing to 9.6 percent in March 2017, the highest since 2002, according to the Reserve Bank of India’s Financial Stability Report released Friday. Stressed assets, including soured debt and restructured loans, eased slightly to 12 percent in March 2017 from 12.3 percent in September 2016.

Weakness in the Indian banking system is a threat to growth in Asia’s third-largest economy and may stall Prime Minister Narendra Modi’s plan to revive credit growth from near a two-decade low. The soured loans have contributed to a $191 billion pile of zombie debt that’s cast the future of some lenders in doubt and curbed investment by businesses. “The RBI and the government are proactively taking steps to resolve NPA challenges in the banking sector,” Deputy Governor NS Vishwanathan said in a foreword to the report. “We have also activated prompt corrective action to stem the slide in the banking system.”

State-run lenders under performed their peers in the private sector, the report showed, which measures risks to the banking system by tracking factors such as profitability, asset quality and liquidity. Last month, the government gave new powers to the RBI in an effort to clean up the country’s bad-debt mess, which has left banks struggling with billions of rupees in nonperforming loans. The government amended the Banking Regulation Act to enable the RBI to order lenders to initiate insolvency proceedings against defaulters and to create committees to advise banks on recovering their loans.

The RBI in June ordered the banks to use the insolvency courts to find a solution for 12 of the debtors, though it didn’t name the institutions on its list. Earlier in the decade, many Indian steel and construction companies borrowed to fund expansion at a time when the economy was expanding at 9 percent to 10 percent a year. Loans turned sour as that growth slowed, weakening demand for steel used in construction projects.

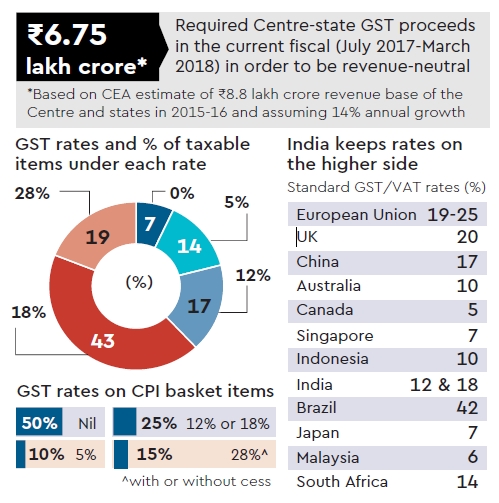

India embraced the goods and services tax (GST) on the intervening night of Friday-Saturday, in a move that marked the culmination of the country’s long and chequered journey toward a uniform, all-encompassing, pan-India indirect tax system.

India embraced the goods and services tax (GST) on the intervening night of Friday-Saturday, in a move that marked the culmination of the country’s long and chequered journey toward a uniform, all-encompassing, pan-India indirect tax system. The GST would militate against and cut out the cascade of multiple taxes which jack up product prices. The official launch of the tax preceded a grand ceremony in the central hall of Parliament attended by the president and prime minister, along with members of both Houses and the GST Council. Some Opposition parties including the Congress, Trinamool Congress and Left did not attend the ceremony, citing protests against GST by small and medium-scale entrepreneurs, traders, weavers and informal-sector workers.

Although the design of the new destination-based tax on consumption with its multiple rates, sub-optimal coverage and complicated rules is unmistakably inferior to an “ideal GST”, even independent tax experts welcomed the launch, calling it a transformational move. However, trenchant critics would say the imperfect GST has merely enabled cross-utilisation of credit between the central and state VAT chains and is, therefore, akin to the 2004 Cenvat rules that allowed such cross-credit facility between central excise and service tax.

But these critics might have taken too dim a view; GST is a momentous event for thee reasons: One, it puts in place a federal, rules-bound indirect tax system that would curtail the scope of rate differentials for the same products among states (one-product-one-tax) ; two, it could potentially slash India’s high logistics costs by speeding up movement of goods across state borders and even within states and thereby make the country’s goods and services more competitive; and three, thanks to the availability of seamless input tax credits, GST would discourage tax evasion and expand the revenue base for the government without hurting the businesses or the consumers. The GST will subsume excise duty and state VAT (along with the corresponding taxes on imports), service tax, octroi, entry tax, purchase tax, central sales tax, and entertainment tax, but not the basic Customs duty which is the tariff on imports.

Earlier, the GST Council, which met for an hour, decided to reduce the tax rate on fertilisers from 12% proposed earlier to 5%, a move that would nullify the chances of prices of these key farm inputs rising under GST. The gap between the current tax incidence on fertilisers and the 12% rate had created a practical difficulty in recovering the differential from fertiliser stocks lying with manufacturers and dealers as MRPs are printed on them. Also, the ministry of finance tweeted, the rate for “exclusive parts of tractors” have been reduced to 18% from 28%.

NITI Aayog member Bibek Debroy on Friday rebutted the claim that GST would produce 1.5% increase in GDP. “For an imperfect GST, I have no idea what is the figure. This particular figure (1.5%) was for ideal GST,” he said. Chief economic adviser Arvind Subramanian had told FE earlier that even though “we have not got as much base expansion and as much reduction in complexities as we would have liked”, there was still a huge reduction in complexities. “I expect a 10% expansion in the (tax) base due to just invoice-matching,” he had said.

While the government has iterated that the GST would not stoke inflation — GST will be zero on 50% of consumer price index basket and 5% on another 10% — former finance minister P Chidambaram said that the new tax could be inflationary in the short run. However, Subramanian said that with with actual tax incidence to be substantially lower under GST due to input tax credit, a downward bias on prices was to be expected. Firms disposing of stocks could also have a dampening effect on prices in the short run, he added.

Even as the industry is keeping its fingers crossed, the government has assured them that the anti-profiteering provision built into the relevant GST laws to prevent companies from not passing on the tax benefit under GST to consumers would be sparingly used. “I sincerely hope that we don’t have to really use the anti-profiteering mechanism,” Jaitley had said on Thursday. Chidambaram, however, sharply criticised the mechanism, saying it was wrong to assume that “the element of taxes decide at what price I sell my goods”. Since tax is only one of the things that make up costs, he said, if tax falls, it does not mean there should be a corresponding reduction in prices.

Even though 68 lakh businesses have already been issued provisional IDs by GSTN, the IT backbone for the new system, and the deadline for first filing of returns have been postponed to August 20 — invoice-wise returns can be filed as late as the first week of September — concern over the transition pains remained. Arun Kumar, chairman and CEO at KPMG in India, said: “The focus should now be on making the transition seamless and effective. Making compliance cost-effective, particularly for smaller businesses, is extremely important. The potential benefits of this landmark-reform will become real when the benefits of rationalised taxation accrue to consumers and business benefits from cost-efficiencies in logistics and streamlined processes.”

According to Shyamal Mukherjee, chairman, PwC India, “We are confident (that GST) will boost investors’ confidence in India, incentivise manufacturing and fuel the growth of the economy.” When asked about the quantum of extra growth due to GST by a TV channel earlier in the day, the chief economic adviser, however, merely said GST’s effect on the economy would be “positive”. “The medium-term impact of GST on macroeconomic indicators is expected to be extremely positive. Inflation will be reduced as cascading of taxes will be eliminated,” CII director general Chandrajit Banerjee said, adding that exports would emerge as more competitive in global markets, while FDI was likely to be encouraged.

The government has made quoting the Aadhaar number a must at the time of applying for a permanent account number, or PAN, card.

Individuals having permanent account number (PAN) will have to link it to their existing Aadhaar number from 1 July, a Finance Ministry notification said on Wednesday.

Amending income tax rules, the government has made quoting the 12-digit identification number or Aadhaar enrolment ID compulsory while applying for PAN, which is mandatory for filing tax returns, opening of bank accounts and financial transactions beyond a threshold.

Every person who has been allotted PAN as on the 1st day of July shall intimate his Aadhaar number to the tax authorities, the notification from revenue department said.

Biometrics identification enabled by Aadhaar proves the identity of the PAN holder and helps tax authorities to crack cases of multiple PANs held by the same person with the idea of tax evasion. As many as 20.7 million taxpayers have already linked their Aadhaar with PAN. There are over 250 million PAN card holders in the country while Aadhaar has been issued to 1.15 billion people.

The rule will come into force from 1 July, the revenue department said while amending Rule-114 of the Income Tax Act, which deals in application for allotment of PAN.

Earlier this month, the tax department had clarified that the relief granted by the Supreme Court regarding non-cancellation of PAN for not linking Aadhaar with it was applicable only in cases of people who do not have Aadhaar and do not wish to obtain it for the time being. Their PAN cards will not be treated as invalid. For tax filing, Aadhaar is mandatory from 1 July.

“The notification does not specify the form and manner in which Aadhaar should be intimated, neither the timelines for such intimation have been set out,” said Sonu Iyer, tax partner and people advisory services leader, EY.

“Individuals having a PAN but no Aadhaar application number who would be filing an income tax return post June 30, 2017 will need to apply for Aadhaar in order to be able to file the income tax return. Individuals who are not required to file an income tax return but who have a PAN and are eligible to obtain Aadhaar (whether they have one or not) as on July 1, 2017 should wait for further notification which will specify the date and manner in which the two identification numbers shall be linked,” added Iyer.

Aadhaar-linked PAN enables taxpayers to verify their returns through a one-time password sent to their phone numbers at the time of filing returns. This makes return filing easier as there is no need for an e-filer to send a signed physical copy of the return to the department, completing the legal formality of filing. Aadhaar and the password performs the verification function of an assessee’s signature in a physical copy of the return that pledges the information furnished to be true.

For decades, Sugal & Damani Group focused on lotteries before it entered the online bill payment business with Payworld.

Now, it has become a GST service provider (GSP), an entity that will help businesses register, upload electronic invoices and file on the technology platform, and plans to leverage its network.

Pune-based Vayana Network has been working with small and medium enterprises (SMEs) to arrange funds and has no experience of taxation, but it too has become a GSP and is eyeing business from companies, their vendors as well as standalone SMEs.

Besides GSPs, GST has given birth to another set of entities called ‘application service providers’ or ASPs that will use sales and purchase data from taxpayers and convert it into GST returns for filing online.GST is spawning a $2 billion-3 billion (Rs 13,000 crore-20,000 crore) industry comprising software service providers, ASPs and GSPs, chartered accountants and consulting firms as the entire industry is undergoing business process re-engineering.

SAP and Oracle, the big daddies of the ERP business, may mop up revenues of at least $1 billion (Rs 6,500 crore) over the next two years, industry players say.

Homegrown Tally Solutions, which has close to 11 lakh users of its accounting software, has already got around six lakh subscriptions from businesses, which entitles them to free upgrades and access to all information.

While the cost of software varies between Rs 18,000 and Rs 54,000, each annual subscription fetches the company Rs 3,600 (for a single user) to Rs 10,800 (multiple users).

With 10,000 melas planned in the next one month, the company is out to garner as much business as possible while helping businesses tackle GST, said Tally Systems executive director Tejas Goenka.

Even a smaller player like the newly set up Ginesys is eyeing a turnover of around Rs 100 crore in three years, said co-founder Ashish Mittal. Then, there are the likes of ClearTax, which was set up to file income tax returns. Sensing a huge business opportunity it has expanded into the GST arena with its software and tie-ups with around 10,000 chartered accountants, said ClearTax founder CEO Archit Gupta.

Not surprisingly, companies have hired big time to meet the required demand. SAP and its partners have around 500-600 people working on implementing ERP solutions, business filing, supply chain and the app for filing returns, said Neeraj Athalye, who leads the firm’s GST adoption drive. Cleartax has hired around 400 in the last one year or so.The big four accounting firms too have ramped up. Deloitte’s indirect tax team has around 250 new recruits, while PwC has expanded its pool of CAs and systems executives by 200-250. While the billing for large companies runs into crores, including consulting services, the smaller companies are banking on volumes with some charging a fee of as low as Rs 100-200 a month for filing returns.

The loan is aimed at making Indian youth more employable through reskilling

The World Bank has cleared a USD 250-million loan for making Indian youth more employable through reskilling, in a move that is seen to aid the Skill India Mission.

The multi-lateral lender is keen to support the Indian government in its efforts to better equip the young workforce with employable skills. It said the support will help the youth contribute to India’s economic growth and prosperity.

“The USD 250-million Skill India Mission Operation (SIMO), approved by the World Bank board of executive directors, will increase the market relevance of short-term skill development programmes (3-12 months or up to 600 hours) at the national and state level,” the Bank said in a statement.

Under the programme, adults in 15-59 years of age, underemployed or unemployed, will get the skill training.

It will also include the 1.2 crore youngsters in the age group of 15-29 years who are entering the labour market every year.

The programme has a mandate to provide placement and entrepreneurship opportunities to women and increase their exposure to skill training.

The Washington-headquartered World Bank’s SIMO is a six-year programme in support of the Indian government’s National Policy for Skill Development and Entrepreneurship (2017-23).

SIMO will be implemented through the National Skill Development Mission and will specifically target labour market entrants.

According to an official skill gap analysis, India will require an additional 109 million skilled workers in 24 key sectors by 2022.

“This programme will support the government’s vision of investing in the human capital of India’s youth, enable greater off-farm employment and increase women’s participation in the labour market,” World Bank Country Director to India Junaid Ahmad said.

India continues to be on its path of structural reforms and a higher-skilled labour force can potentially serve as a catalyst in transforming it into a competitive middle income country, Ahmad said.

As per the Bank’s estimate, skill development capacity of the system would increase by the end of the programme so that at least 8.8 million youth with relevant training have an improved employment opportunity to raise their earnings.

The programme will benefit approximately 15,000 trainers and 3,000 assessors, it added.

Opened for first time for new assessees, tax practitioners

With barely five days left for the roll-out of the goods and services tax (GST), the GST Network (GSTN), a company that provides information technology systems for the GST, reopened registration for assessees on Sunday.

That was for new assessees not enrolled in the existing tax system — central excise duty, service tax and state-level value added tax — and for tax practitioners such as chartered accountants. Existing assessees which did not apply earlier can also enrol. The system also opened for those to be registered as tax deducted at source (TDS) or tax collected at source (TCS).

So far as smoothness of registration is concerned, Archit Gupta, chief executive officer (CEO) of Cleartax, that helps assessees register on GSTN, said, “We have an online service for fresh registrations and have received applications form small & medium businesses. So far, we haven’t faced any issues in the registration process for our customers.”

As many as 6.56 million registrations have already been made on the GSTN, which is 81 per cent of the existing 8.01 million registrations.

The new assessees, as well as existing ones, will be given a month’s time to register on the GSTN from Sunday.

Earlier, GSTN was opened in phases since November 16 for existing tax assessees. The GSTN had stopped registrations in between, as it was to transfer data to its own data centre from an earlier hired data centre. The GST portal has already opened two windows for enrolments — first between November 8 and April 30 and then from June 1 to June 15. This is the third window to allow all taxpayers enough time to migrate to the new regime.

Navin Kumar, chairman of GSTN, said, “We started the migration of existing taxpayers in November and wanted to close the process by March. The government however asked us not to close it, as many were still to register. At that time, the number of people coming to the portal fell to a few thousands compared to 200,000 a day (now). But we halted the process briefly, hoping it would trigger more people to come and register when we reopen the window.” Interestingly, there was no law that required them to register as GSTs then; the Bills were passed later.

“In fact, I am surprised why they came. We asked the tax department to persuade them to come and migrate, so the entire credit goes to CBEC. About six million came in the first instance and then 600,000 more came in the 15 days after that,” he said.

There were 8.01 million registrations in the existing system. Kumar said he wondered why the 1.4 million didn’t come. He believed one factor could be the exemption threshold under VAT for most states is Rs 5 lakh, and is Rs 20 lakh under the GST. Those with a turnover below the threshold have to register if they want to claim input tax credit.

It is expected not all assessees would migrate to the GSTN portal as, businesses with turnover of up to Rs 5 lakh are currently exempt from VAT. But, if they are supplying to other businesses or if want to pass on credit, then they need to register their business.

The existing assessees were given provisional IDs if they registered with their email ID and mobile numbers. But, for the second stage and final registration, the businesses have to give details of its business, such as the shareholding pattern of business, main place of business, additional place of business, directors and bank account details etc.

Revenue Secretary Hasmukh Adhia had cautioned those with provisional IDs not to rush for registration on GSTN, as they had got one month more for registration.

The GST Council has given relaxation for filing of returns. The assessees can file detailed, invoice-based returns by September 5 for the month of July. Had this relaxation not been given, they would have to file these returns by August 10.

Similarly for August, these returns could be filed by September 20, a relaxation of 10 days.

Meanwhile, the GSTN released three sets of videos to reach out to assessees and help them register.

“To help the people register themselves to the new GST portal smoothly, we have released three videos just after the opening of the portal today (Sunday). The videos are an official guide for registration which will ensure a smooth roll out of the regime. The videos have been crafted to help all taxpayers including those who are not well versed with technology to complete their enrolments,” Kumar said.

This will bring down the incidence of taxation on business, which can be shared with consumers through lower prices.

Buying cleaning liquids for ‘Swachh Bharat’ as part of corporate social responsibility or taking a business associate out for lunch, companies will be able to set off all taxes paid on their consumption of goods and services when they clear their own GST liability.

The upcoming indirect tax reform seeks to revamp the entire credit process, allowing credit for any tax paid towards the furtherance of business barring a few items.

“Uninterrupted and seamless chain of input tax credit is one of the key features of GST, which will prevent cascading of taxes” .

This will bring down the incidence of taxation on business, which can be shared with consumers through lower prices.

Goods and services tax (GST), India’s most ambitious indirect tax reform, is set to roll out from July 1.

Tax charged by central and state governments would also be part of the same tax regime with credit available for tax paid at every stage for set off against GST liability.

“Any registered person can avail credit of tax paid on the inward supply of goods or services or both which is used or intended to be used in the course or furtherance of business,” the provision reads.

Under the current tax regime, if a retailer purchases a refrigerator to store perishable goods, he is not able to claim credit for tax paid on it. But under GST, he will be able to claim credit for tax paid on new refrigerator when he files his own taxes.

Similarly, credit could be claimed on tax paid on taking business associates out for lunch, or on goods or service used for corporate social responsibility. There are some exceptions, such as contribution towards employee provident fund and car lease, which are not covered under input tax credit.

“Under GST, input credit is available on all business expense except few that are specifically denied, such as employee benefits and construction,” said Pratik Jain, leader, indirect tax, at PwC.

“This is much more liberal than the current laws and would significantly increase the credit pool for the businesses,” he said.

“One would hope that authorities will interpret the law also liberally as this would need in change in mindset both for the industry as well as the government,” Jain said.

There is a pass through available for tax paid on a good or service consumed to ensure that tax is not levied on tax.