The government extended the date for filing income tax returns for companies by one month to November 30.

Income Tax Department has extended the deadline for ITR filing for certain categories of taxpayers. This has brought great relief to the taxpayers/institutions falling in these categories and they have also been saved from paying heavy penalties due to delay.

According to the Income Tax Department, till September 5, about 6.98 crore individual taxpayers have filed ITR.

The Income Tax Department has extended the deadline for filing income tax returns for charitable trusts, religious institutions and professional bodies by one month to November 30. The Income Tax Department said in a statement that the due date for filing income tax return in Form ITR-7 for the assessment year 2023-24, which is 31 October 2023, has been extended to 30 November 2023.

Also, the due date for submission of audit report for 2022-23 by any fund, trust, institution or any university or educational institution or medical institution in Form 10B/10BB has been extended by one month to 31 October 2023. Earlier the last date for submission of audit report was 30 September.

ITR-7 is filed by institutions involved in charitable and religious activities, research institutes, professional bodies, political parties and electoral trusts also file tax returns through ITR-7.

The Finance Ministry said in a statement on Monday, the deadline for filing income tax return in Form ITR-7 for the assessment year 2023-24 has been extended from October 31, 2023 to November 30, 2023.

In the current financial year, till mid-September, net direct tax collection has increased by 23.51% to Rs 8.65 lakh crore. The Finance Ministry said that there has been a huge increase in direct tax collection due to more advance tax payment by the companies. During this period, advance tax payment has increased by 21%.

According to the data, net tax collection has been 47.45% of the budget estimate of Rs 18.23 lakh crore for the current financial year. In the last financial year 2022-23, direct tax collection was Rs 16.61 lakh crore.

AIS shows both reported value and the value after considering taxpayer feedback under each section (i.e. TDS, SFT, Other information).

The Income Tax Department has announced the roll-out of a new statement namely Annual Information Statement (AIS) which would provide you with almost all details about your financial transactions during the year. So far, the Income Tax Department has been issuing Form 26AS to provide information related to taxable income and tax deducted at source (TDS), which will now be replaced with the Annual Information Statement (AIS). The new AIS statement will provide comprehensive information of the taxpayer and will be significantly useful while preparing the tax return. The information will be provided in AIS after removing duplicate information and taxpayers can download such information in PDF, JSON, CSV formats.

A taxpayer can submit online feedback if the information is erroneous or refers to another person/year, or is duplicate. The list of Top 50 Transactions to be reported in the New Annual Information Statement are mentioned below.

1.Salary

Employer submits detailed breakup of salary, perquisites, profits in lieu of salary etc paid to the employee in Annexure II of the TDS statement (24Q) of the last quarter. This information is also provided by the employer to the employee (taxpayer) in Part B (Annexure) of Form 16. AIS displays all the financial transactions such as, salary income, dividend income, interest income from saving/fixed deposits, sale and purchase of securities, etc. With the help of all such financial information, it would be easy for a taxpayer to report the correct information in the income tax return

Rent Received

Tenants responsible for paying rent are liable to deduct tax at source on payment of rent. Deductor reports details of amount paid/credited, date of payment, details of Tax deduction made etc. in Form 26Q. This information is provided by the deductor to the deductee (taxpayer) in Form 16A. Tenant (Individual/HUF) paying a rent of more than 50,000 is liable to deduct tax while making payment to the landlord. Tenant reports details of rent paid amount paid/credited, property details, date of payment and tax deduction details etc. pertaining to rent paid in Form26QC.

Dividends

Dividend paid/declared by all companies (reporting entity) is reported under Statement of Financial Transactions (SFT). Company paying/distributing dividend is liable to deduct TDS from the amount paid subject to the threshold applicable in the act and report through form 26Q (quarterly statement). This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Interest from savings bank

Interest paid/credited/accrued on saving account is reported under Statement of Financial Transactions (SFT).

Interest from deposit

Bank/deductor at the time paying/crediting interest on deposits is liable to deduct tax from deposit holder paid subject to the threshold applicable in the act. This information is reported by the Bank/deductor in form 26Q (quarterly statement). This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Interest from others

Interest paid/credited/accrued on others (other than savings account, term deposit, recurring deposit) is reported under Statement of Financial Transactions (SFT). Bank/deductor at the time paying/crediting other interest (interest on securities) is liable to deduct tax from deposit holder paid subject to the threshold applicable in the act. This information is reported by the Bank/deductor in form 26Q (quarterly statement). This information is provided by the deductor to the deductee (taxpayer) in Form 16A

Interest from income tax refund

Interest received on Income Tax Refund in the financial year is liable to be taxed as Income from other sources.

Rent on plant & machinery

Tenant paying rent is liable to deduct tax at applicable rate as per the Act from rent paid. Details of rent on Plant & Machinery is reported by the deductor in TDS form 26Q. Tenant furnishes the details of rent paid on quarterly basis. This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Winnings from lottery or crossword puzzle

Payer is liable to deduct tax at applicable rate as per act from winnings from lottery or crossword puzzle etc. Information about winnings is reported by payer in TDS form 26Q. Information is reported on quarterly basis. Income is taxable at special rate. This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Winnings from horse race

Payer is liable to deduct tax at applicable rate as per act from winnings from Horse race. Information about winnings is reported by payer in TDS form 26Q. Information is reported on quarterly basis and is chargeable to tax at special rate. This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Receipt of accumulated balance of PF from employer u/s 111

Employer/recognised provided fund reports information about accumulated balance due to an employee in form 26Q. Information is reported on quarterly basis and is chargeable to tax at special rate. This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Interest from infrastructure debt fund

Information relating to interest paid is reported by payer in form 27Q. Information is reported on quarterly basis and is chargeable to tax at special rate. This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Interest from specified company by a non-resident u/s 115A(1)(a)(iiaa)

Information relating to interest paid is reported by payer in form 27Q. Information is reported on quarterly basis and is chargeable to tax at special rate. This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Interest on bonds and government securities

Information relating to interest paid is reported by payer in form 27Q. Information is reported on quarterly basis and is chargeable to tax at special rate. This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Income in respect of units of non-resident u/s 115A(1)(a)(iiab)

Information about income in respect of units of Non Resident is reported by payer in form 27Q. Information is reported on quarterly basis and is chargeable to tax at special rate. This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Income and long-term capital gain from units by an offshore fund u/s 115AB(1)(b)

Information about income and long-term capital gain from units payable to an off shore fund is reported by payer in form 27Q. Information is reported on quarterly basis and is chargeable to tax at special rate. This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Income and long-term capital gain from foreign currency bonds or shares of Indian companies u/s 115AC

Information about income and long-term capital gain from foreign currency bonds or shares of Indian companies is reported by payer in form 27Q. Information is reported on quarterly basis and is chargeable to tax at special rate. This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Income of foreign institutional investors from securities u/s 115AD(1)(i)

Information about income of foreign institutional investors from securities is reported by payer in form 27Q. Information is reported on quarterly basis and is chargeable to tax at special rate. This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Insurance commission

Information about insurance commission received is reported by the payer in Form 26Q on a quarterly basis. This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Receipts from life insurance policy

Receipts from life insurance policy are exempt under section 10(10D) subject to conditions specified therein. If such conditions are not met, the receipts become taxable and tax is also deducted u/s 194DA. The information is reported by the payer in Form 26Q on a quarterly basis. This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Withdrawal of deposits under national savings scheme

Withdrawals from NSS are taxable. Tax is also deducted on such withdrawals and reported in Form 26Q by the payer on a quarterly basis. This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Receipt of commission etc. on sale of lottery tickets

Commission on lottery business is subject to tax deduction under section 194G. The payer reports such information in Form 26Q on a quarterly basis. This information is provided by the deductor to the deductee (taxpayer) in Form 16A

Income from investment in securitization trust

Income from investment made in securitization trust is subject to tax deduction. The payer reports such information in Form 27Q on a quarterly basis. This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Income on account of repurchase of units by MF/UTI

Receipt of income on account of repurchase of units by MF/UTI is subject to tax deduction under section 194F. The payer reports such information in Form 26Q on a quarterly basis. This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Interest or dividend or other sums payable to government

Income from interest or dividend or other sums payable is not subject to tax deduction. The payer reports such information in Form 26Q on a quarterly basis. This information is provided by the deductor to the deductee (taxpayer) in Form 16A

Payment to non-resident sportsmen or sports association u/s 115BBA

Information pertaining to amount paid to non-resident sportsmen or sports association is reported by deductor in form 27Q. This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Sale of land or building

Sales consideration of immovable property transferred is reported under Statement of Financial Transactions (SFT). The information will be shown in AIS of all sellers to enable submission of feedback. Sale of immovable property is also reported in Form 61 where PAN is not furnished by the transacting party. PAN is populated based on aadhaar and other attributes of the person. Information related to receipts under specified agreement is reported by person making payment for specified agreement entered into. This information is provided by the deductor to the deductee (taxpayer) in Form 16A.

Receipts from transfer of immovable property

Information related to receipts from transfer of immovable property is reported by buyer of property in Form 26QB. This information is provided by the deductor to the deductee (taxpayer) in Form 16B.

Sale of vehicle

Sale of motor vehicle is reported in Form 61 where PAN is not furnished by the transacting party. PAN is populated based on aadhaar and other attributes of the person.

Sale of securities and units of mutual fund

In the SFT reporting of depository transactions, the estimated sale consideration for the debit transaction is determined on the best possible available price of the asset with the depository (e.g. end of day price). The taxpayer will be able to modify the sales consideration and other related information before filing the return. In the SFT reporting of depository transactions, the estimated sale consideration for the debit transaction is determined on the best possible available price of the asset with the depository (e.g. end of day price). The taxpayer will be able to modify the sales consideration and other related information before filing the return.

Off market debit transactions

In the SFT reporting of depository transactions, the depository reports details of off market debit transactions. The value of transaction is computed on the basis of end of day price of the security. In case, the consideration is available, the same is also shown.

Off market credit transactions

In the SFT reporting of depository transactions, the depository reports details of off market credit transactions. The value of transaction is computed on the basis of end of day price

Business receipts

Information pertaining to amount paid to contractor is reported by contractee in form 26Q. This information is provided by the deductor to the deductee (taxpayer) in Form 16A. Information pertaining to amount paid to the service provider is reported by recipient of services in form 26Q. This information is provided by the deductor to the deductee (taxpayer) in Form 16A

Business expenses

Information pertaining to purchase of alcoholic liquor is reported by tax collector in TCS form 27EQ (quarterly statement). This information is provided by the collector to the taxpayer in Form 27D.

Rent payments

Information is reported by person making payment in form 26QC. This information is provided by the deductor to the taxpayer in Form 16C

Miscellaneous payments

Information is reported by person making payment in form 26QD. This information is provided by the deductor to the taxpayer in Form 16D. Purchase of bank drafts or pay orders may be reported in Form 61 if PAN is not furnished by the transacting party. PAN is populated based on aadhaar and other attributes of the person

Cash deposits

Information pertaining to cash deposits in an account other than current account is reported by reporting entity in form 61A. The information will be shown in AIS of all account holders to enable submission of feedback. Information pertaining to cash deposits in current account is reported by reporting entity in form 61A. The information will be shown in AIS of all account holders to enable submission of feedback.

Cash withdrawals

Information pertaining to Cash withdrawals from current account is reported by reporting entity in form 61A. The information will be shown in AIS of all account holders to enable submission of feedback. Sometimes, cash withdrawals from accounts other than current account are reported by the Reporting Entity in SFT-004. The information will be shown in AIS of all account holders to enable submission of feedback. Information pertaining to Cash withdrawals is reported by reporting entity through TDS statement 26Q. This information is provided by the deductor to the taxpayer in Form 16A.

Cash payments

Information pertaining to Cash payments for goods and services is reported by reporting entity in form 61A. Information pertaining to Purchase of bank drafts or pay orders or banker’s cheque in cash is reported by reporting entity in form 61A. Information pertaining to Purchase of prepaid instruments in cash is reported by reporting entity in form 61A.

Outward foreign remittance/purchase of foreign currency

Information of outward foreign remittance is reported by authorised dealer in form 15CC. Information about Remittance under LRS for educational loan taken from financial institutions mentioned in section 80E (Third proviso to Section 206C(1G)) is reported by authorised dealer through TCS form 27EQ for specified foreign remittances made by remitter PAN.Information about Remittance under LRS for purpose other than for purchase of overseas tour package or for educational loan taken from financial institution (Section 206C(1G(a))) is reported by authorised dealer through TCS form 27EQ for specified foreign remittances made by remitter PAN.

Receipt of foreign remittance

Information relating to payment of royalty or fees for technical services etc., paid to non- residents is reported by deductor in form 27Q. This information is provided by the deductor to the deductee (taxpayer) in Form 16A. Information is reported by authorised dealer in form 15CC for foreign remittances made by remitter PAN. Information of receipt of foreign remittance by a remittee is reported by authorised dealer in form 15CC.

Foreign travel

Information is reported by deductor in TCS form 27EQ (quarterly statement). This information is provided by the collector to the taxpayer in Form 16D. Payment in connection with travel to any foreign country may be reported in Form 61 if the PAN is not furnished by the transacting party. PAN is populated based on aadhaar and other attributes of the person.

Purchase of immovable property

Information relating to immovable property is reported by the Property Registrar through SFT. The information will be shown in AIS of all buyers to enable submission of feedback. Buyer at the time of making payment towards purchase of property is liable to deduct tax from the amount paid to the seller subject to the threshold applicable. This information is reported in form 26QB. Seller of property reports the details of property buyer in schedule CG of ITR. Payment for purchase of immovable property may be reported in Form 61 if the PAN is not furnished by the transacting party. PAN is populated based on aadhaar and other attributes of the person.

Purchase of vehicle

Information is reported by deductor in TCS form 27EQ (quarterly statement). This information is provided by the collector to the taxpayer in Form 16D. Payment for purchase of motor vehicle may be reported in Form 61 if the PAN is not furnished by the transacting party. PAN is populated based on aadhaar and other attributes of the person.

Purchase of time deposits

Information relating to Purchase of Time deposits is reported by reporting entity (such as the bank) in the Statement of Financial Transaction (SFT). Information pertaining to investment in Time deposit is reported in Form 61 where PAN is not furnished by the transacting party. PAN is populated based on aadhaar and other attributes of the person.

Purchase of securities and units of mutual funds

Information is reported by reporting entity in the Statement of Financial Transaction (SFT). Purchase of shares (including share application money). Information is reported by reporting entity in the Statement of Financial Transaction (SFT). Information is reported by reporting entity (such as mutual fund companies) in the Statement of Financial Transaction (SFT).

Credit/Debit card

Information pertaining to application for issuance of credit/debit card is reported in Form 61 where PAN is not furnished by the transacting party. PAN is populated based on aadhaar and other attributes of the person.

Balance in account

Details of bank account other than saving and time deposits opened during the year , as reported in Form 61. Bank account with balance exceeding 50,000 at the closing of Financial year, as reported in Form 61.

Income distributed by business trust

Information relating to income from units of a business trust is reported by payer in form 27Q. Information is reported on quarterly basis and is chargeable to tax at special rate.

Income distributed by investment fund

This information is reported by the deductor in Form 26Q on a quarterly basis

The Income Tax Department tracks more comprehensive information about assessees & this facilitates financial transactions from many income sources and expenditures to be captured, in more detail. This needs to be reconciled while filing ITR and proper records to be maintained by all for above list of items, as these are scrutinized by tax department.

ITR filing for AY 2023-24 starts. CBDT enables Excel Utilities for ITR-1, ITR-4

For the assessment year 2023-24, the Income Tax Department has released an offline Excel-based utility for filing ITR-1 Sahaj and ITR-4 Sugam. The utility is available for download from the official Income Tax Department website. Because the utility and forms may change from time to time, it is critical to check the official website for the most recent version/updates and instructions.

The Excel-based utility for filing ITR-1 Sahaj and ITR-4 Sugam for AY 2023-24 is available for download from the Income Tax Department’s website – Released on 25-Apr-2023 and updated on 05-May-2023. The utility – Excel & Java, facilitates to electronically file ITR-1 and ITR-4 forms.

The instructions, utilities, schemas and validation rules will be updated as and when there is a change after due approval from ITD (Income Tax Department)

General Instructions for Returns:

Select the Assessment Year

Download and extract the zip file containing the utilities to the folder and open the utility

System Requirements: Excel Utilities:

Macro enabled MS-Office Excel version 2007/2010/2013 on Microsoft Windows 7 / 8 /10 / 11 with .Net Framework (3.5 & above).

The instructions, utilities, schemas and validation rules will be updated as and when there is a change after due approval from ITD

Using the Excel Utility

When using the Excel utility, it is critical to use a compatible version of Excel that supports macros. Resident and Ordinarily Resident (ROR) individuals with a total income of up to Rs 50 lakh from salaries, one house property, and other sources are eligible for ITR-1 Sahaj. Individuals/HUFs/partnership firms (other than LLP) with a total income of less than Rs. 50 lakh can file the ITR-4 Sugam form.

Using Macros in Excel

It is necessary to enable macros in the Excel sheet before using the ITR utility. To enable macros in Excel, navigate to File > Options > Trust Centre > Trust Centre Settings > Macro Settings > Enable All Macro > Click ‘OK’. Only enable macros in Excel sheets from trusted sources. Some Excel utility worksheets may include a help.txt file that contains instructions on how to enable macros.

Common Technical Problems

Macro errors, login issues, XML validation errors, and offline utility issues are some of the most common technical issues encountered when using the ITR utility. If you encounter any technical difficulties while using the ITR utility, you can seek assistance from the Income Tax Department Helpdesk or Tax Professional.

ITR Utility Customer Service

If you require technical assistance with the ITR utility, please visit the Income Tax Department’s official website and check the FAQs section for offline ITR utility. The FAQs section answers frequently asked questions about the ITR utility and can assist in resolving some technical issues. You can also get help from the Income Tax Department by calling their toll-free number or emailing them.

Conclusion

Filing ITR-1 Sahaj and ITR-4 Sugam using the Income Tax Department’s Excel utility can help to simplify the tax filing process. You can effectively file your taxes by downloading the utility, enabling macros in Excel, and understanding the requirements for using the utility. If you run into any technical difficulties or require assistance, the Income Tax Department and tax professionals are here to help.

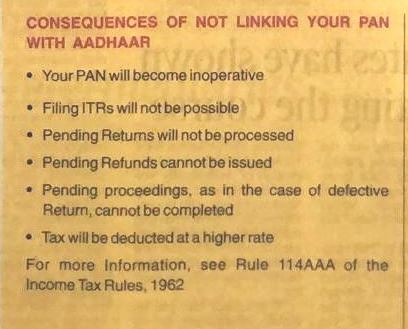

Linking Aadhar with PAN will allow your income tax returns to be processed. The PAN card of a person will become inoperative when it is not linked to an Aadhaar card.

It has become a mandatory process to link your PAN with Aadhaar. This is an important process because this will allow your income tax returns to be processed. Linking of your PAN with Aadhaar is also required if you are carrying out banking transactions for amount of Rs.50,000 and above.

In order to provide some more time to tax payers, Central Board of Direct Taxes (CBDT) has extended the date for linking the PAN and Aadhaar to June 30,2023.

* * * * * * * * * * *

Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes

New Delhi, 28th March, 2023

PRESS RELEASE

Last date for linking of PAN-Aadhaar extended

In order to provide some more time to the taxpayers, the date for linking PAN and Aadhaar has been extended to 30th June, 2023, whereby persons can intimate their Aadhaar to the prescribed authority for Aadhaar-PAN linking without facing repercussions. Notification to this effect is being issued separately.

Under the provisions of the Income-tax Act, 1961 (the ‘Act’) every person who has been allotted a PAN as on 1st July, 2017 and is eligible to obtain Aadhaar Number, is required to intimate his Aadhaar to the prescribed authority on or before 31st March, 2023, on payment of a prescribed fee. Failure to do so shall attract certain repercussions under the Act w. e.f. 1st April, 2023. The date for intimating Aadhaar to the prescribed authority for the purpose of linking PAN and Aadhaar has now been extended to 30th June, 2023.

From 1st July, 2023, the PAN of taxpayers who have failed to intimate their Aadhaar, as required, shall become inoperative and the consequences during the period that PAN remains inoperative will be as follows:

(i) no refund shall be made against such PANS;

(ii) interest shall not be payable on such refund for the period during which PAN remains inoperative; and

(iii) TDS and TCS shall be deducted / collected at higher rate, as provided in the Act.

The PAN can be made operative again in 30 days, upon intimation of Aadhaar to the prescribed authority after payment of fee of Rs 1,000.

Those persons who have been exempted from PAN-Aadhaar linking will not be liable to the consequences mentioned above. This category includes those residing in specified States, a non-resident as per the Act, an individual who is not a citizen of India or individuals of the age of eighty years or more at any time during the previous year.

it is stated that more than 51 crore PANS have already been linked with Aadhaar till date.

Govt has declared March 31, 2023 as the deadline for linking PAN and Aadhaar. Failing to link will make PAN inactive.

It is mandatory to link Permanent Account Numbers (PAN) to Aadhaar by March 31, 2023.

The last date to link Permanent Account Number (PAN) to Aadhaar is nearing soon. According to the Central Board of Direct Taxes (CBDT), the apex body of the Income Tax department, it is mandatory to link Aadhaar to Permanent Account Numbers (PAN) by March 31 this year, failing which the PAN will become ‘inoperative’ on April 1. The previous deadline for linking was March 31, 2022, but the government extended it with a Rs. 1000 penalty fee.

PAN and Aadhaar are both unique identification cards that serve as proof of identity and are required for verification.

Benefits of linking PAN with Aadhaar

– Multiple PAN Cards: Linking of PAN and Aadhaar eliminates the possibility of an individual having more than one PAN Card, thereby reducing fraudulent activities.

– Prevent Tax Evasion: The Income Tax Department will be able to detect any form of tax evasion after PAN is linked with Aadhaar.

-Income Tax Returns: The process of filing income tax returns will become significantly simpler because individuals will no longer be required to provide proof that they have filed their income tax returns. Since Aadhaar holds all the information about an individual including biometric verification, the linking will initiate a faster return filing process.

– Linking your Aadhaar to PAN will prevent the tax return process from being cancelled and will also help in summarising one’s taxes attached to the Aadhaar for furture references.

Steps to link PAN with Aadhaar via web portal:

1. Visit the Income Tax e-filing official websites- eportal.incometax.gov.in or incometaxindiaefiling.gov.in

2. Register on the portal with your PAN as the user ID if not registered already.

3. Log into the portal.

4. A pop-up window will appear to link PAN with Aadhaar or go to ‘Profile Settings’ on the Menu bar and click on Link Aadhaar.

5. Relevant details like name, date of birth, and gender will already be mentioned as per the PAN card details.

6. Verify the details with Aadhaar. If the details match, enter the Aadhaar number and click on the link now button.

7. A message will pop up saying that the Aadhaar has been successfully linked to the PAN.

Other methods of linking PAN with Aadhaar:

1. People can also visit the following websites for the linking process- https://www.utiitsl.com/ and https://www.egov-nsdl.co.in/

2. Through SMS: Type the following message UIDPAN<12 digit Aadhaar><10 digit PAN>. The message can be sent to 567678 or 56161.

3. Visiting nearby PAN service centres: The linking process can also be done manually by visiting the nearby PAN service centre.

Unable to link ?

– You may be unable to link your PAN to Aadhaar in some cases. The most common reason for rejection is a mismatch between the information in your PAN and Aadhaar. Ideally, your demographic information (name, gender, and date of birth) should match in both the documents.

– If there is a minor mismatch between your Aadhaar Name and the actual data in Aadhaar, a One Time Password (Aadhaar OTP) will be sent to the mobile phone registered with Aadhaar. Ensure that PAN and Aadhaar have the same date of birth and gender.

– In a rare case where Aadhaar name is completely different from name in PAN, then the linking will fail and you will be prompted to change the name in either Aadhaar or in PAN database.

– However, once the corrections have been made, you will able to link the PAN and Aadhaar.

According to CBDT, if the linking is not done by March 31, 2023, the PAN cards of such users will become inactive from April 1, 2023.

“As per the Income Tax Act, 1961, the last date to link PAN with Aadhaar is 31.3.2023 for all PAN card holders, who do not fall in the exempted category.

If not linked with Aadhaar, PAN will become inactive,” tweeted the CBDT through the IT department’s handle, adding that such users won’t be able to use PAN starting April 1, 2023.

The Central Board of Direct Taxes (CBDT), the apex body of the Income Tax department, has urged Permanent Account Number (PAN) card holders who are yet to link their PAN with Aadhaar card, to do so by March 31 next year, or else the former will be deactivated.

Steps to link PAN card with Aadhaar card:

In the Income Tax portal, enter your PAN and Aadhaar number on the required fields and then click on ‘Validate’

If the message ‘PAN is already linked with the Aadhaar or with some other Aadhaar’ pops up on your screen, it means your Adhaar is already linked with PAN

If your PAN is not linked to your Aadhaar and you have paid a challan on the NSDL Portal

The fee payment for PAN-Aadhaar Linkage needs to be made through e-Pay Tax functionality available on e-filing Portal

If you have bank account in any of the designated banks in the tax portal, you can follow below mentioned steps:

Provide your PAN, Confirm PAN and Mobile number to receive OTP

Post OTP verification, you will be redirected to a page showing different payment tiles

Click Proceed on the Income Tax portal

Select AY and Type of Payment – as other Receipts (500) and Continue

Enter the amount as Rs. 1000 under ‘Others’ field in tax break-up and proceed with further steps

If you have other bank accounts (bank that is not designated for payment through e-Pay tax), please follow below steps:

Click on hyperlink ‘Click here to go to NSDL (Protean) tax payment page for other banks’ given below on e-Pay tax page to redirect to Protean (NSDL) portal

Click Proceed under Challan No./ITNS 280

Select (0021) Income Tax (Other than Companies) under Tax Applicable (Major Head)

Select (500) Other Receipts) under Type of Payment (Minor Head)

Provide other mandatory details and Proceed

You are required to wait 4-5 working days before submitting the linkage request if the payment details are not authenticated on the e-filing portal and if you have already paid the amount on the NSDL portal.

After the payment, the information will be validated by electronic filing

You will receive a pop-up notification stating that “Your payment details are verified” after confirming your PAN and Aadhaar.

Click the Link Aadhaar option, and then enter the 6-digit OTP received on your mobile phone number

After successfully submitting your request for an Aadhaar-PAN link, you may now check its status.

Here is how you can check PAN and Aadhaar linkage status

Enter your PAN and Aadhaar Number, and then click on the ‘View Link Aadhaar Status’ option.

Your PAN and Aadhaar linkage status will be displayed on the screen upon successful validation.

PAN Holders should note that they need to check the status again if the UIDAI is still processing their request to link PAN and Aadhaar for confirmation.

Providing a relaxation to the tax payer, the Central Board of Direct Taxes has extended the deadline for filing income tax return for the assessment year of 2022-23 till November 7, 2022. The decision was taken on Wednesday. It is to be noted that the last date to file ITR for FY23 was October 31.

The Central Board of Direct Taxes (CBDT) said in a notification that the ITR filing due date has been extended as it had last month extended the deadline for filing audit reports.

Providing a relaxation to the tax payer, the Central Board of Direct Taxes has extended the deadline for filing income tax return for the assessment year of 2022-23 till November 7, 2022. The decision was taken on Wednesday. It is to be noted that the last date to file ITR for FY23 was October 31.

CBDT extends the due date for furnishing Income Tax Return for AY 2022-23 to 7th November, 2022 for certain categories of assessees in consequence of extension of due dates for filing various reports of audit. Circular No. 20/2022 dated 26.10.2022 issued.

CBDT’s extension of due date for filing of Income Tax Return (ITR) for Assessment Year 2022-23 from 31/10/2022 to 07/11/2022 applies to the following assesses:

a) Companies

b) Persons subject to Tax Audit or Audit under any other law

c) Partner of Firm which is subject to Tax Audit

d) Other specified persons whose due date of filing the return of income is 31/10/2022.