“There is a need to create a regulator or authority for data business, which provides centralized regulation for all non-personal data exchanges,” the government-appointed panel said in the report. Such a regulator would be armed with legal powers to request data, supervise data sharing requests and settle disputes“.

A formal Memorandum of Understanding (MoU) was signed today between the Central Board of Direct Taxes (CBDT) and the Securities and Exchange Board of India (SEBI) for data exchange between the two organizations.

The MoU was signed by Smt. Anu J. Singh, Pr. DGIT (Systems), CBDT, and Smt. MadhabiPuri Buch, Whole Time Member, SEBI in the presence of senior officers from both the organizations via video conference.

The MoU will facilitate the sharing of data and information between SEBI and CBDT on an automatic and regular basis.

In addition to regular exchange of data, CBDT and SEBI will also exchange with each other, on request and suo moto basis, any information available in their respective databases, for the purpose of carrying out scrutiny, inspection, investigation and prosecution,” SEBI said in a statement.

In addition to regular exchange of data, SEBI and CBDT will also exchange with each other, on request and Suo moto basis, any information available in their respective databases, for the purpose of carrying out their functions under various laws.

The MoU comes into force from the date it was signed and is an ongoing initiative of CBDT and SEBI, who are already collaborating through various existing mechanisms.

A Data Exchange Steering Group has also been constituted for the initiative, which will meet periodically to review the data exchange status and take steps to further improve the effectiveness of the data-sharing mechanism.

The MoU marks the beginning of a new era of cooperation and synergy between SEBI and CBDT.

In the past, SEBI has cracked on several entities who had manipulated the stock prices of listed companies. The regulator had observed in the penny stock scam that promoters and market operators were using the stock exchange platform to evade taxes and launder black money.

The Government has also extended PAN-Aadhaar linking deadline.

In view of the challenges faced by taxpayers in meeting the statutory and regulatory compliance requirements across sectors due to the outbreak of Novel Corona Virus (COVID-19), the Government brought the Taxation and Other Laws (Relaxation of Certain Provisions) Ordinance, 2020 [the Ordinance] on 31st March, 2020 which, inter alia, extended various time limits.

In order to provide further relief to the taxpayers for making various compliances, the Government has issued a Notification on 24th June, 2020, the salient features of which are as under:

I. The time for filing of original as well as revised income-tax returns for the FY 2018-19 (AY 2019- 20) has been extended to 31st July, 2020.

II. Due date for income tax return for the FY 2019-20 (AY 2020-21) has been extended to 30th November, 2020. Hence, the returns of income which are required to be filed by 31st July, 2020 and 31st October, 2020 can be filed upto 30th November, 2020. Consequently, the date for furnishing tax audit report has also been extended to 31st October, 2020.

III. In order to provide relief to small and middle-class taxpayers, the date for payment of self-assessment tax in the case of a taxpayer whose self-assessment tax liability is upto Rs. 1 lakh has also been extended to 30th November, 2020. However, it is clarified that there will be no extension of date for the payment of self-assessment tax for the taxpayers having self-assessment tax liability exceeding Rs. 1 lakh. In this case, the whole of the self-assessment tax shall be payable by the due dates specified in the Income-tax Act, 1961 (IT Act) and delayed payment would attract interest under section 234A of the IT Act.

IV. The date for making various investment / payment for claiming deduction under Chapter-VIA-B of the IT Act which includes section 80C (LIC, PPF, NSC etc.), 80D (Mediclaim), 80G (Donations) etc. has also been further extended to 31st July, 2020. Hence the investment / payment can be made upto 31st July, 2020 for claiming the deduction under these sections for FY 2019-20.

V. The date for making investment / construction/ purchase for claiming roll over benefit / deduction in respect of capital gains under sections 54 to 54GB of the IT Act has also been further extended to 30th September, 2020. Therefore, the investment / construction/ purchase made up to 30th September, 2020 shall be eligible for claiming deduction from capital gains.

VI. The date for commencement of operation for the SEZ units for claiming deduction under section 10AA of the IT Act has also been further extended to 30th September, 2020 for the units which received necessary approval by 31st March, 2020. VII.

VII. The furnishing of the TDS/ TCS statements and issuance of TDS/ TCS certificates being the prerequisite for enabling the taxpayers to prepare their return of income for FY 2019-20, the date for furnishing of TDS/ TCS statements and issuance of TDS/ TCS certificates pertaining to the FY 2019-20 has been extended to 31st July, 2020 and 15th August, 2020 respectively.

VIII. The date for passing of order or issuance of notice by the authorities and various compliances under various Direct Taxes & Benami Law which are required to be passed/ issued/ made by 31st December, 2020 has been extended to 31st March, 2021. Consequently, the date for linking of Aadhaar with PAN would also be extended to 31st March, 2021.

IX. The reduced rate of interest of 9% for delayed payments of taxes, levies etc. specified in the Ordinance shall not be applicable for the payments made after 30th June, 2020. The Finance Minister has already announced extension of date for making payment without additional amount under the “Vivad Se Vishwas” Scheme to 31st December 2020, necessary legislative amendments for which shall be moved in due course of time. The said Notification has extended the date for the completion or compliance of the actions which are required to be completed under the Scheme by 30th December, 2020 to 31st December, 2020. Therefore, the date of furnishing of declaration, passing of order etc under the Scheme stand extended to 31st December, 2020

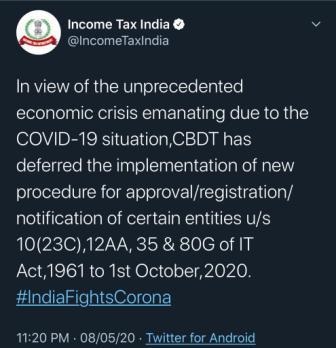

Deferment of the implementation of new procedure for approval/ registration/ notification of certain entities u/s 10(23C), 12AA, 35 and 80G of the IT Act has already been announced vide Press Release dated 8th May, 2020 from 1st June, 2020 to 1st October, 2020. It is clarified that the old procedure i.e. pre-amended procedure shall continue to apply during the period from 1st June, 2020 to 30th September, 2020. Necessary legislative amendments in this regard shall be moved in due course of time.

The Finance Minister has already announced reduced rate of TDS for specified non-salaried payments to residents and specified TCS rates by 25% for the period from 14th May, 2020 to 31st March, 2021. The announcement was also followed by the Press Release dated 13th May, 2020. The necessary legislative amendments in this regard shall be moved in due course of time

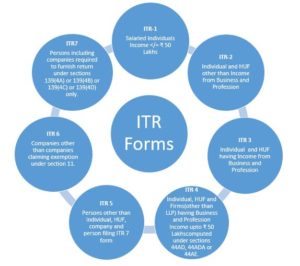

The Central Board of Direct Taxes (CBDT) has notified new Income-tax Return (ITR) forms applicable for the Assessment Year 2020-21.

CBDT notified Income Tax Return forms of FY 2020-21

G.S.R. 338(E).— In exercise of the powers conferred by section 139 read with section 295 of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes has made the rules to amend the Income-tax Rules, 1962.

The principal rules were published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (ii) vide notification number S.O. 969(E), dated the 26th March, 1962 and last amended by the Income-tax (11th Amendment) Rules, 2020, vide notification number G.S.R. 329 (E) dated 28.5.2020.

In essence, the following are the key changes:

House ownership: Individual taxpayers who are joint owners of house property cannot file ITR 1 or ITR4.

Passport: One needs to disclose the Passport number if held by the taxpayer. This is to be furnished both in ITR 1-Sahaj and ITR 4-Sugam. Hopefully, it will be made mandatory in other ITR Forms as and when they are notified.

Cash deposit: For those filing ITR 4-Sugam, it has been made compulsory to declare the amount deposited as cash in a bank account, if such amount exceeds Rs 1 crore during the FY.

Foreign travel: If you have spent more than Rs 2 lakh on travelling abroad during the FY, you need to disclose the actual amount spent.

Electricity consumption: If your electricity bills have been more than Rs 1 lakh in aggregate during the FY, you need to disclose the actual amount.

Investment details: Details of investment qualifying for deduction under chapter VIA with bifurcation of details of investment made during the period from April 1, 2020 to June 30, 2020.

A new schedule ‘Schedule DI’ has been inserted to claim benefit of investment/ deposit/payments made between 01-04-2020 to 30-06-2020 for the previous year 2019-20.

The amendment, aims at controlling tax evasion, and bring glassiness Form 26AS, which is now being replaced with a new Annual Information Statement (AIS) i.e Form 26AIS.

The Central Board of Direct Taxes (CBDT) on Thursday notified Income Tax (11th Amendment) Rules, 2020.

In exercise of the powers conferred by section 285BB read with section 295 of the Income-tax Act, 1961 (43 of 1961), the Central Board of Direct Taxes hereby makes the following rules further to amend the Income-tax Rules, 1962, namely:-

In Income Tax Rules, 1962 Rule 114-I relating to Annual Information shall be inserted which is, “the Principal Director General of Income Tax (System) or the Director-General of Income Tax (Systems) or any person authorized by him shall, under Section 285BB of the Income-Tax Act, 1961, upload in the registered account of the assessee an annual information statement in Form No. 26AS containing the information specified in the column (2) of the table below, which is in his possession within three months from the end of the month in which the information is received by him.”

The notification consists of a table that contains the nature of information which includes information relating to a tax deduction or collected at source; specified financial transaction; payment of taxes; demand and refund; pending proceedings; and completed proceedings:

Sl. No.

Nature of information

(i)

Information relating to tax deducted or collected at source

(ii)

Information relating to specified financial transaction

(iii)

Information relating to payment of taxes

(iv)

Information relating to demand and refund

(v)

Information relating to pending proceedings

(vi)

Information relating to completed proceedings

(vii)

Any other information in relation to sub-rule (2) of rule 114-I

The amendment, aims at controlling tax evasion, and bring glassiness Form 26AS, which is now being replaced with a new Annual Information Statement (AIS) i.e Form 26AIS.

Further sub-clause (2) of Rule 114-I says, “the Board may also authorize the Principal Director General of Income-tax (System) or the Director-General of Income Tax (Systems) or any person authorized by him to upload the information received from any officer, authority or body performing any function under any law or the information received under an agreement referred to in Section 90 or Section 90A of the Income Tax Act, 1961 or the information received from any other person to the extent as it may deem fit in the interest of the revenue in the annual information statement referred to in sub-clause (1).”

Lastly, sub-clause (3) of Rule 114-I says, “the Principal Director General of Income-tax (System) or the Director-General of Income Tax (Systems) shall specify the procedures, formats, and standards for the purpose of uploading of annual information statement referred to in sub-clause (1).”

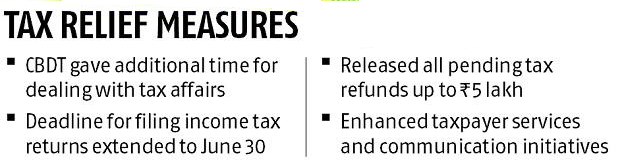

Income-tax refund of Rs 14,632 crore to 15,81,906 assesses and corporate tax refund amounting to Rs 11,610 crore to 1,02,392 assesses have been processed during this period, the CBDT said in a statement.

Income Tax Deptt. has issued refunds of Rs. 26,242 crores since 1st April 2020 to 16.84 lac individual/ corporate assessees. Further, the refund process has been geared up for necessary action to match the Aatma Nirbhar Bharat initiative (COVID-19) announced by PM/ FM recently.

CBDT Press Release dt. 22 May 2020

Central Board of Direct Taxes (CBDT) has issued tax refunds worth Rs. 26,242 crore to 16,84,298 assessees since 1st April, 2020 to 21st May, 2020.

Income Tax refunds amounting to Rs. 14,632 crore have been issued to 15,81,906 assessees and corporate tax refunds amounting to Rs. 11,610 crore have been issued to 1,02,392 assessees during this period.

It is stated that the refund process has been further expedited and refunds are being issued at a greater pace since the Union Finance Minister Smt. Nirmala Sitharaman’s announcement made in the Aatma Nirbhar Bharat Abhiyan last week. CBDT has released a sum of Rs. 2050.61 crore in the previous week ended on 16th May, i.e., between 9th to 16th May, 2020 to 37,531 income tax assessees and a sum of Rs. 867.62 crore to 2878 corporate tax assessees. During this week, i.e. between 17th to 21st May, 2020, yet another 1,22,764 income tax assessees were refunded Rs. 2672.97 crore and 33,774 corporate tax assessees including trusts, MSMEs, proprietorships, partnerships, etc. were issued refunds worth Rs. 6714.34 crore, taking the total amount refunded to Rs. 9387.31 crore in the case of 1,56,538 assessees.

Move comes after a group of IRS created panic and tax policy uncertainty.

After rejecting “ill-conceived” suggestions by a group of Indian Revenue Services (IRS) officers, the Central Board of Direct Taxes (CBDT) directed officials not to keep any communication with assessees or issue scrutiny notices to them without the board’s approval.

According to it, any such notice would have an “adverse effect” on the assessees amid the coronavirus (Covid-19) pandemic.

These directives are part of the interim action plan for the first quarter (April-June) prepared by the direct tax board. It highlights certain areas which need immediate attention and preparedness until normalcy returns.

The move comes at a time when the tax department faced widespread criticism on a report prepared by a group of IRS officers. It had created panic and tax policy uncertainty at a time when India is already going through a difficult economic situation.

“Identification and preparedness regarding the issuance of notice under Section 148, which deals with income escaping and return filing in all eligible cases, should be done by June 30. However, these notices are to be issued only after getting fresh communication from the board in this regard,” said the CBDT note.

It added that due to the unprecedented situation arising out of Covid-19-induced social distancing and lockdown this year, a relatively short interim action plan has been issued.

Considering the current situation, we have been putting a slew of tax relief measures to mitigate the impact on business and even on household.

Any such communication may put pressure on the taxpayers and create unnecessary panic. A new system had already been put in place to make officials accountable for their communication with assessees.

However, during the lockdown, even such communication would not go without the board consent, said a CBDT official. Other than keeping no communication with assessees, the tax officials have been asked to centralise cases where searches took place in the financial year 2019-202.

This is because once lockdown is lifted, the officials would work on disposing them on merit.

Moreover, the CBDT asked officials to be prepared for tax demands in cases of international taxation, tax deduction at source and exemption-related charges.

The board wants the department to examine all pending demands, according to permanent account number (PAN) and assessment years.

It also removed demands which are creating duplication and are lying in the system. Besides, officials were asked to reconcile brought-forward cases, especially on TDS, based on the information available on the Traces portal for TDS units. The interim action plan also instructed officials to dispose of all applications concerning granting registration to charitable trusts received upto March 31.

Meanwhile, the direct tax board told its officials to upload manual orders on the systems, especially those under Section 263. It deals with appeals where the principal commissioner or commissioner may call for and examine the record of any proceeding. He or she may consider an order passed by the assessing officer to be erroneous, if it is prejudicial to the interests of the revenue.

Earlier, such registrations/approvals were granted without any specific expiry period unless specifically withdrawn by concerned tax authority. Under the new law introduced by Finance Act 2020 and effective from June 1, 2020, all such registrations/ approvals would now be issued with an expiry period of 5 years.

In a relief to religious trusts, educational institutions and other charitable institutions, the income tax department on Friday deferred by 4 months till October 1 the requirement of registration of these entities.

In a relief to religious trusts, educational institutions and other charitable institutions, the income tax department on Friday deferred by 4 months till October 1 the requirement of registration of these entities.

“In view of the unprecedented humanitarian and economic crisis, the CBDT has decided that the implementation of new procedure for approval/ registration/notification of certain entities shall be deferred to 1st October, 2020,” an official statement said.

Finance

Act 2020 prescribed substantial changes in law pertaining to

registration/approval of trusts and charitable institutions, whose

income are exempt under section 10(23C), Section 11 or for the purpose

of Section 80-G of the Act for tax deductible donations.

Earlier,

such registrations/approvals were granted without any specific expiry

period unless specifically withdrawn by concerned tax authority.

Under

the new law introduced by Finance Act 2020 and effective from June 1,

2020, all such registrations/ approvals would now be issued with an

expiry period of 5 years.

Further, all trusts/charitable institutions already having approval or registration were also supposed to file applications for renewal of there registration/approval within 3 months of new law coming into force, i.e. August 31, 2020.

Nangia

Andersen Consulting Shailesh Kumar said “in light of COVID-19 outbreak

and consequent lockdown, giving relief to the taxpayers, this timeline

has been deferred by 4 months. Thus, new law which was supposed to come

in effect from 01 June 2020 would now come in effect from 01st October

2020.

“All

existing trusts/ charitable institutions would now need to file

applications for renewal of their registrations/ approvals by December

31, 2020 instead of earlier August 31, 2020,” he added.

The

statement said various representations were received to the finance

ministry expressing concerns over the implementation of new procedure

from June 1, 2020 due to outbreak of coronavirus (COVID-19) and

consequent lockdown and there have been a number of requests to defer

the applicability of new procedure.

“This is a welcome move and provides expected relief in light of genuine hardships created by COVID-19. The entities benefited by this circular would be religious trusts, hospitals, educational institutions or other public charitable institutions created for welfare of public and allows exemption from income tax on account of their activities and charitable purpose,” Kumar added.

Consulting

firm AKM Global Tax Partner Amit Maheshwari said, “This is a welcome

clarification as in the absence of this extension, it was extremely

difficult to comply with these procedures. Several representations had

been made on this matter and this is indeed a welcome move.”