In view of the challenges faced by taxpayers in meeting the statutory and regulatory compliance requirements across sectors due to the outbreak of Novel Corona Virus (COVID-19), the Government brought the Taxation and Other Laws (Relaxation of Certain Provisions) Ordinance, 2020 [the Ordinance] on 31st March, 2020 which, inter alia, extended various time limits.

In order to provide further relief to the taxpayers for making various compliances, the Government has issued a Notification on 24th June, 2020, the salient features of which are as under:

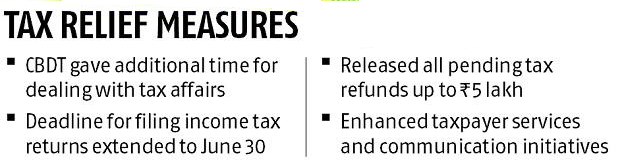

I. The time for filing of original as well as revised income-tax returns for the FY 2018-19 (AY 2019- 20) has been extended to 31st July, 2020.

II. Due date for income tax return for the FY 2019-20 (AY 2020-21) has been extended to 30th November, 2020. Hence, the returns of income which are required to be filed by 31st July, 2020 and 31st October, 2020 can be filed upto 30th November, 2020. Consequently, the date for furnishing tax audit report has also been extended to 31st October, 2020.

III. In order to provide relief to small and middle-class taxpayers, the date for payment of self-assessment tax in the case of a taxpayer whose self-assessment tax liability is upto Rs. 1 lakh has also been extended to 30th November, 2020. However, it is clarified that there will be no extension of date for the payment of self-assessment tax for the taxpayers having self-assessment tax liability exceeding Rs. 1 lakh. In this case, the whole of the self-assessment tax shall be payable by the due dates specified in the Income-tax Act, 1961 (IT Act) and delayed payment would attract interest under section 234A of the IT Act.

IV. The date for making various investment / payment for claiming deduction under Chapter-VIA-B of the IT Act which includes section 80C (LIC, PPF, NSC etc.), 80D (Mediclaim), 80G (Donations) etc. has also been further extended to 31st July, 2020. Hence the investment / payment can be made upto 31st July, 2020 for claiming the deduction under these sections for FY 2019-20.

V. The date for making investment / construction/ purchase for claiming roll over benefit / deduction in respect of capital gains under sections 54 to 54GB of the IT Act has also been further extended to 30th September, 2020. Therefore, the investment / construction/ purchase made up to 30th September, 2020 shall be eligible for claiming deduction from capital gains.

VI. The date for commencement of operation for the SEZ units for claiming deduction under section 10AA of the IT Act has also been further extended to 30th September, 2020 for the units which received necessary approval by 31st March, 2020. VII.

VII. The furnishing of the TDS/ TCS statements and issuance of TDS/ TCS certificates being the prerequisite for enabling the taxpayers to prepare their return of income for FY 2019-20, the date for furnishing of TDS/ TCS statements and issuance of TDS/ TCS certificates pertaining to the FY 2019-20 has been extended to 31st July, 2020 and 15th August, 2020 respectively.

VIII. The date for passing of order or issuance of notice by the authorities and various compliances under various Direct Taxes & Benami Law which are required to be passed/ issued/ made by 31st December, 2020 has been extended to 31st March, 2021. Consequently, the date for linking of Aadhaar with PAN would also be extended to 31st March, 2021.

IX. The reduced rate of interest of 9% for delayed payments of taxes, levies etc. specified in the Ordinance shall not be applicable for the payments made after 30th June, 2020. The Finance Minister has already announced extension of date for making payment without additional amount under the “Vivad Se Vishwas” Scheme to 31st December 2020, necessary legislative amendments for which shall be moved in due course of time. The said Notification has extended the date for the completion or compliance of the actions which are required to be completed under the Scheme by 30th December, 2020 to 31st December, 2020. Therefore, the date of furnishing of declaration, passing of order etc under the Scheme stand extended to 31st December, 2020

Deferment of the implementation of new procedure for approval/ registration/ notification of certain entities u/s 10(23C), 12AA, 35 and 80G of the IT Act has already been announced vide Press Release dated 8th May, 2020 from 1st June, 2020 to 1st October, 2020. It is clarified that the old procedure i.e. pre-amended procedure shall continue to apply during the period from 1st June, 2020 to 30th September, 2020. Necessary legislative amendments in this regard shall be moved in due course of time.

The Finance Minister has already announced reduced rate of TDS for specified non-salaried payments to residents and specified TCS rates by 25% for the period from 14th May, 2020 to 31st March, 2021. The announcement was also followed by the Press Release dated 13th May, 2020. The necessary legislative amendments in this regard shall be moved in due course of time