Non-resident investors who do not provide permanent account number will no longer have to face higher tax deduction at source.

The income tax department has eased norms for non-resident investors, who will not be subjected to a higher rate of 20% tax deduction at source or TDS on their interest earnings, royalty or technical fee if they furnish some personal details and tax residency certificate from their home country and a few other easily available documents.

“Provisions of Sec 206AA shall not apply in respect of payments in the nature of interest, royalty, fees for technical services and payments on transfer of any capital asset,” the Central Board of Direct Taxes said in a notification. Section 206AA of I-T Act provides that if an investor does not have permanent account number or PAN, he or she will be liable to withholding taxes on payments at the rate of 20% or as per tax treaty with the country where investor is resident, whichever is higher.

This clause forced non-resident investors to seek PAN, making investment process difficult.

Under the new rules 37BC, investors will instead need to provide their personal details such as e-mail and contact number, residential address and tax residency certificate from the government of their home country.

In case the country does not provide tax residency certificate, the investor can provide tax identification number or any other unique identification number issued by the country of residence. This will spare investors the hassles of securing PAN in India and attendant compliance that comes with having this number.

Finance minister Arun Jaitley had said in his budget speech in February that some concession would be provided in this regard. “Non-residents without PAN are currently subjected to a higher rate of TDS. It is proposed to amend the relevant provision to provide that on furnishing of alternative documents, the higher rate will not apply,” Jaitley had said, without spelling out the details.

Attractive interest rates in India saw overseas Indians pour $1.92 billion more into non-resident Indian (NRI) deposits in FY2016 vis-à-vis FY2015, according to Reserve Bank of India data.

Overall, NRI deposit inflows in FY2016 amounted to $15.977 billion ($14.057 billion in FY2015).

In FY2015, NRI deposit inflow had dropped to $14.057 billion after topping $38.406 billion in FY2014.

Year-on-year, NRI deposits increased by about 10 per cent to stand at $126.854 billion as at March-end 2016. Carry trade (NRIs borrowing in foreign currencies and parking these funds as deposits with banks in India) may have lured overseas Indians to save money with banks in India, say bankers.

In the April-March 2016 period, NRIs parked $2.492 billion as against $1.001 billion in the year-ago period in FCNR (B) deposits, according to RBI’s monthly bulletin.

FCNR (B) account can be opened in the names of two or more non-resident Indians provided all the account holders are persons of Indian nationality or origin. The account can be opened in any permitted currency — a foreign currency which is freely convertible. The term of the repatriable deposits is of not less than one year and not more than five years.

In the April-March 2016 period, NRIs saved $12.384 billion as against $12.20 billion in the year-ago period in NR (E)RA deposits.

Non-Resident (External) Rupee Account deposits can be opened in the names of two or more non-resident individuals provided all the account holders are persons of Indian nationality or origin.

NR(E)RA deposits, which are denominated in rupees and are repatriable, can be in the form of savings, current, recurring, and fixed deposits. Interest rates offered by banks on these deposits cannot be higher than those offered by them on comparable domestic rupee deposits.

NRIs parked $1.101 billion in rupee-denominated Non-Resident Ordinary Rupee Account Scheme (NRO Account) in FY2016 as against $856 million in FY2015. NRIs can hold these accounts jointly with residents. These deposits are usually not repatriable except under certain conditions.

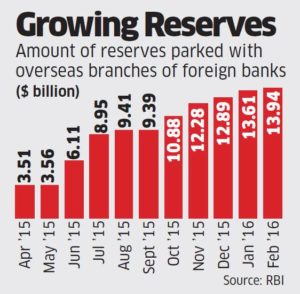

The amount of foreign exchange reserves that the Reserve Bank of India keeps with overseas banks has more than tripled, signalling that it may be preparing to intervene more effectively in the currency market due to impending volatility because of global factors and the possible exodus of about $30 billion of non-resident Indian deposits.

Total funds parked with the overseas branches of foreign banks rose to $13.9 billion in February from $3.5 billion in April last year, according to Reserve Bank of India data posted on its website. The central bank issues the information as a signatory to the International Monetary Fund’s special data dissemination standard, a guide to member countries on putting economic data in the public domain. The country’s foreign currency assets in the same period dipped from $351.9 billion to $348.4 billion.

“The rise in deposit component in reserves suggests RBI may be waiting for the right time to invest in overseas assets or parking it in highquality liquid assets for intervention to manage potential currency volatility,” said Vijayan Subramani, managing director, DBS Bank. “Our central bank looks for offshore (sovereign) investment at the right level with a prudent mix of diversification, be it US Treasury or European sovereign bonds.”

RBI governor Raghuram Rajan has long warned of volatility in global financial markets because of divergent monetary policies with some central banks poised to normalise interest rates while others have taken them into negative territory to free up liquidity and generate economic activity. Furthermore, more than $30 billion of FCNR (Foreign Currency Non-Resident) deposits that were attracted in 2013 to boost foreign exchange reserves, are due to mature this year.

The central bank seems to be preparing to defend the rupee against volatility that could result from this money being pulled out.

“Our estimate is that that scheme came with a lot of leverage, that banks were offering loans to people who invested in that scheme and we anticipate that will not be renewed because we are not going to offer the same favourable terms again,” Rajan told reporters recently. “So we are actually estimating a fairly low rollover rate on the FCNR. The good news is we are fully prepared for whatever exit takes place and we will monitor market conditions. We think at this point that we do not anticipate volatility, but if there is, we will deal with it.”

Governed by rules and conventions of banking secrecy, banks in Switzerland and tax havens divulge information only after account holders give their consent.

Even NRIs with offshore bank accounts cannot keep the taxman at bay by obtaining quick relief from the court of law. In order to prove their innocence, such persons will have to instruct the overseas banks to share information on the accounts with the Indian tax office.

And, only after the details released by the bank show that the money lying in the account does not belong to the person who has been pulled up (for hiding offshore assets), can he escape the glare of tax officials.

The Bombay High Court recently dismissed the writ petition filed by an NRI — an alleged beneficiary of a trust linked to an account with HSBC Geneva — after she refused to sign the “consent waiver” form to let HSBC share the information on the account. Governed by rules and conventions of banking secrecy, banks in Switzerland and tax havens divulge information only after account holders gives their consent.

The court, in its order dated April 5, said, “In the normal course of human conduct if a person has nothing to hide and serious allegations/questions are being raised about the funds, a person would make available the documents which would put to rest all questions which seem to arise in the mind of the authorities.”

Since the court did not allow the withdrawal of petition, the order is likely to be used by the tax office which is trying to fish out bank account and transaction details from those it suspects to have accounts with HSBC Geneva.

According to the base note that the French government had shared with New Delhi, the petitioner Soignee R Kothari, along with six other individuals and two trusts, are beneficiaries of an account held by one White Cedar Investments with HSBC Geneva; the seven individuals in turn are beneficial owners of the two trusts.

As on 26 March 2006, the account had a balance of more than $44 million. The department had served Ms Kothari a notice to reopen assessment for the assessment year 2006-07.

She has later agreed (in a rejoinder before the court) to sign the consent waiver form with a modification — as ‘alleged beneficiary’ rather than ‘holder or beneficiary’ of the account in HSBC Geneva.

“With this, the Bombay High Court has precluded any alleged holder of overseas bank account from seeking alternative remedy by way of a writ. However, their right to contest any addition of income by the tax authorities would still survive. Thus, while NRIs can prove that they are outside jurisdiction of Indian tax authorities, they cannot wriggle out of investigation by virtue of being NRIs,” said senior chartered accountant Dilip Lakhani. The other six alleged beneficiaries of the trust are Arun Ramniklal Mehta, Russell Mehta, Viraj Russell Mehta, Rihen Harshad Mehta, Naina Harshad Mehta and Priti Harshad Mehta.

The court said that this bank statement if obtained from HSBC Geneva “would reveal and/or possibly give clues as to the source of amounts deposited in the Account No. 5091404580.” “If a person has nothing to hide, we believe the person would have co-operated in obtaining bank statements,” said

Giving the much needed reforms impetus to the economy, Prime Minister Narendra Modi-led NDA government on Tuesday announced Foreign Direct Investment (FDI) reforms in as many as 15 sectors.

According to the government’s release, “The crux of these reforms is to further ease, rationalise and simplify the process of foreign investments in the country and to put more and more FDI proposals on automatic route instead of government route where time and energy of the investors is wasted.”

These FDI reforms are set to benefit sectors such as agriculture and animal husbandry, plantation, defence, broadcasting, civil aviation and manufacturing. “Further refining of foreign investments in key sectors like construction where 50 million houses for poor are to be built. Opening up the manufacturing Sector for wholesale, retail and e-Commerce so that the industries are motivated to Make In India and sell it to the customers here instead of importing from other countries,” the release added..

The proposed reforms also enhance the limit of Foreign Investment Promotion Board (FIPB) from current Rs 3,000 crore to Rs 5,000 crore. The proposal also contains many other long pending corrections including those being felt by the limited liability partnerships as well as NRI owned companies who seem motivated to invest in India. Few other proposals seek to enhance the sectoral caps so that foreign investors don’t have to face fragmented ownership issues and get motivated to deploy resources and technology with full force.

India got FDI of $19.39 billion in the April-June period, according to government data, up 29.5% over the year earlier. The Modi government has been pushing hard to drum up overseas investment, easing FDI regulations in various sectors including the railways, medical devices, insurance, pension, construction and defence.

Last week, ET had reported that the government plans to launch a series of policy reforms, signalling its intent to get moving again on economic changes and putting the Opposition on notice before Parliament convenes for the winter session.

Key to the Narendra Modi government’s renewed development push will be power, labour and infrastructure, three senior government officials had told ET. Among the highlights are a revival package for power distribution companies, freeing up labour rules and a possible push for the railways, ET had said in its report.

The road map for the phasing out of corporate tax exemptions and reduction in the tax rate to 25% is being drawn up. Besides this, the Startup India, Standup India plan and the rollout of the National Investment and Infrastructure Fund (NIIF) are also being worked on.

A simpler foreign direct investment (FDI) policy, further easing of the external commercial borrowing (ECB) regime and changes in the public-private partnership (PPP) framework to attract more private investment could also announced.

While Indian-incorporated firms (Indian companies) are taxed at 30% plus dividend distribution tax (DDT), non-resident (foreign) companies are taxed at 40% on Indian income without DDT.

Foreign companies with Indian shareholders won’t have to pay taxes here for their worldwide income unless they are managed from India on an everyday basis. If these foreign companies are managed from outside India, whether or not they are promoted by resident Indians, they will have to pay taxes in India only for the income they earn in the country.

This major relaxation is being built into the place of effective management (POEM) rules being finalised by the finance ministry, government sources told FE. The POEM concept that was included in the I-T Act early this fiscal had raised fears among many multinational companies with Indian promoters or major shareholders that New Delhi would lay claim to taxes on their incomes attributable to other geographies.

While Indian-incorporated firms (Indian companies) are taxed at 30% plus dividend distribution tax (DDT), non-resident (foreign) companies are taxed at 40% on Indian income without DDT. Although the tax rates on foreign companies are higher, the prospect of subjecting the worldwide income to taxation here could have potentially hit many MNCs with Indian stakeholders.

The proposed lenient POEM rule, analysts said, would give the likes of UK’s Jaguar Land Rover (which has the Indian parent Tata Motors) a chance to convince the Indian tax authorities that the UK firm’s commercial decisions are taken by the local management there and avoid paying taxes for the income in the UK and elsewhere in India.

Similarly, foreign subsidiaries of state-owned oil companies such as ONGC Videsh’s Imperial Energy incorporated in Cyprus and ONGC Nile Ganga doing oil exploration in Sudan, Syria and Venezuela can potentially show that their managerial and commercial decisions are ‘in substance’ made at the local level although OVL, the Indian holding company, is under the direct administrative control of the government of India. The same is true for HPCL’s Singapore subsidiary Prize Petroleum International.

“Putting a management in place is a shareholder decision, not a management decision. Promoters getting into any other role would amount to overstepping shareholder rights, going by the strict interpretation of law. The POEM as a principle must cover only management decisions,” said Rahul Garg, leader, direct tax, PwC India.

According to experts, seeking permission from an Indian parent on a decision taken by an overseas subsidiary to see if it is in line with the global policy of the parent may not ordinarily amount to the parent exercising management control, unlike the parent passing on a centrally taken decision to the foreign associate. However, where the senior management of foreign associates of Indian firms are based in India or have common board members based in India, the overseas entity may find it hard to prove that management decisions are taken from outside India. Also, foreign associates of Indian companies lacking skilled managerial personnel or do not assume business risks on its own, could have a tough time convincing the taxman in India that they are not Indian residents.

Prior to the Finance Act, 2015, a company was considered an Indian resident if its control and management were wholly in India throughout the financial year. Since some Indian companies sought to avoid resident status and taxes on their worldwide income by holding one or two board meetings outside India, the government changed the residence definition saying that any company, the ‘place of effective management’ of which is in India, would also be a resident company. Tax residence is a place from where key management and commercial decisions necessary for running the company are, in substance, made. According to experts, this OECD definition of tax residence relies on the substance of the organisation’s structure than its legal form. The government is bringing out clarifications as there is not much global guidance on the concept.

Points to note:

* Mere shareholder rights with Indians won’t result in resident status

* Only managerial decisions taken here will make foreign firms Indian residents and liable to pay tax for entire global income here

* Foreign firm has to prove management independence to avoid tax residence if board members are common with that of Indian ones.

Non-resident investors who do not provide permanent account number will no longer have to face higher tax deduction at source.

Non-resident investors who do not provide permanent account number will no longer have to face higher tax deduction at source.