The RBI will embark on its biggest banking clean-up exercise after President Pranab Mukherjee promulgated an ordinance authorising it to issue directions to banks to initiate insolvency resolution process in the case of loan default.

The tweak in the rules will help the Modi government tackle toxic loans that have crossed the Rs 6 lakh crore mark.

So, what does this mean?

1) The ordinance promulgated by the government on bad loans has now empowered the RBI to issue directions to banks for resolution of stressed assets. This basically implies the central bank can issue directions to any banking company or banking firms to initiate insolvency resolution process with respect to a default under the provisions of the Insolvency and Bankruptcy Code, 2016.

2) It has also empowered RBI to issue directions to banks for resolution of stressed assets.

3) The law will also empower RBI to set up sector related oversight panels that will shield bankers from later action by probe agencies looking into loan recasts.

4) RBI will be able to give specific solutions with regard to hair cut for specific cases and also, if required, look at providing relaxation in terms of current guidelines.

What is RBI’s target?

The central bank wants to resolve 60 largest delinquent-loan cases in nine months, a person familiar with the matter told Bloomberg.

Why is it being done now?

Ridding bank balance sheets of stressed assets is key to reviving credit growth and furthering Prime Minister Narendra Modi’s goal of creating more jobs in the $2 trillion economy.Various schemes proposed by RBI to resolve the problem have been unsuccessful, with lenders reluctant to write down assets sufficiently and company owners unwilling to negotiate repayment plans.

Stressed assets — bad loans, restructured debt and advances to companies that can’t meet servicing requirements — have risen to about 17 percent of total loans, the highest level among major economies, data compiled by the government shows.

India’s foreign exchange reserves surged by whopping $2.671 billion to $366.781 billion for the week ended March 2017 on account of increase in foreign currency assets, the Reserve Bank said today.

In the previous week, the reserves had risen by $98.6 million to $364.109 billion.

Foreign currency assets (FCAs), a major component of the overall reserves, rose by $2.645 billion to $343.101 billion in the reporting week, the RBI said.

Expressed in US dollar terms, FCAs include the effects of appreciation/depreciation of non—US currencies, such as the euro, pound and the yen held in the reserves.

Gold reserves remained unchanged at $19.914 billion.

The special drawing rights with the International Monetary Fund was up by $10 million to $1.444 billion; India’s reserve position with the Fund, too, increased by $15.9 million to $2.320 billion, RBI said.

– Nifty surpasses March 2015 peak, Sensex gains as much as 2.1%. – Bigger-than-expected victory seen as endorsement of reforms

Indian equities rallied to a record and the rupee climbed the most since 2013 after Prime Minister Narendra Modi’s resounding victory in state elections boosted expectations for a continuation of his reform agenda.

The NSE Nifty 50 Index climbed 1.7 percent to 9,087, crossing its March 2015 record close, as the market reopened after a holiday. The India VIX Index, a gauge of expected stock-price swings, touched an all-time low. The rupee surged 1.2 percent to 65.8175 per dollar, the strongest level since November 2015. The central bank was seen buying dollars in early trade to cap gains but moved away later, Mumbai-based traders said.

“This win will give Modi the confidence to push ahead with more reforms and not pursue populist policies,” Sampath Reddy, chief investment officer at Bajaj Allianz Life Insurance Co., said by phone. The insurer, which oversees 480 billion rupees ($7.3 billion) of assets, is bullish on financial-services companies and metal producers, he said.

Modi’s Bharatiya Janata Party won 312 seats in the 403-member assembly of Uttar Pradesh, according to the Election Commission of India, up from 47 in 2012. The results in India’s largest state were seen as a litmus test of Modi’s popularity and reforms, including opening up the country to more foreign investment and seeking to introduce a goods and services tax, ahead of general elections in 2019.

While exit polls released last week suggested a large BJP victory was possible in Uttar Pradesh, the scale of the win was stark in a state that has long been divided along religious and caste lines. It is also a repudiation of political foes who assumed that Modi’s disruptive Nov. 8 move to junk high-value currency notes would be politically unpopular.

“Uttar Pradesh is a state where mandates have tended to be mostly divisive, so the result is a mandate for development, which has been sorely missing in the state,” Gautam Sinha Roy, a fund manager at Mumbai-based Motilal Oswal Asset Management Co., said by phone. “Markets will now start assigning higher probability to a BJP victory in the 2019 polls.”

India’s economic growth has been 7 percent or more in each of the last four quarters, which has helped lure $3.4 billion of foreign funds into local stocks and bonds this year. Mutual funds bought shares for seven months through February, including a record $2.1 billion in November. The S&P BSE Sensex has risen 11 percent in 2017, and the rupee is up 3.2 percent against the dollar.

“We expect the Reserve Bank of India to more actively cap further rupee gains given the sharp swing higher in the real effective exchange rate in recent months,” Divya Devesh, an Asia FX strategist at Standard Chartered Bank in Singapore, said by e-mail. He forecasts the rupee at 69 rupees to the dollar by year-end.

Pricey Valuations

The Nifty came off an intraday high of 9,122.75 as investor focus turned to a near-certain interest rate hike from the Federal Reserve this week and expected revival in corporate profitability. The Nifty and the Sensex are valued at about 21 times forward earnings, the highest level since April 2010.

“Valuations look stretched and investors are cautious with the Fed meeting round the corner,” said Sushant Kumar, a fund manager at RAAY Global Investments Pvt. in Mumbai. “Stocks have priced in the expected increase in rates. The focus is on Fed’s outlook.” The Nifty may reach 10,000 by March 2018, accompanied by as much as 14 percent expansion in earnings of its 50 members, he said.

Still, the scale of the BJP’s victory paves the way for further reforms and should lead to more inflows, supporting asset prices, according to Vikas Gupta, chief investment strategist at OmniScience Capital Pvt. in Mumbai.

“For international investors, India is one of the few emerging markets that has everything going for it: demographics, economics and politics,” he said. “With elections settled, it is clear that the federal government is now going to be fully in charge of the parliament.”

Official data released on Tuesday showed that demonetisation hasn’t pushed the economy into a retreat as most feared, with its short-term adverse impact. (Source: Reuters)

Official data released on Tuesday showed that demonetisation hasn’t pushed the economy into a retreat as most feared, with its short-term adverse impact to a large extent restricted to construction and financial services. Real GDP growth in the December quarter, in the midst of which the note ban came into effect, came in at a respectable 7% (though lower than 7.4% in the previous quarter) and the gross value added (GVA) was 6.6%, with the difference explained by robust indirect taxes and reining in of subsidies.

Upward revision of GVA estimates for 2015-16 led to downward corrections in GVA for Q1 and Q2 of the current fiscal but despite this, there were marginal upward revisions in the rates of GDP expansion in these quarters, thanks to a surge in indirect taxes.

Solid performance by the “agriculture and allied sectors”, pump-priming by the government on the consumption side, better-than-expected performance by mining and manufacturing sectors and a seasonal — though larger-than-usual — pick-up in private consumption masked whatever negative effect the note swap exercise had on the economy, going by the Central Statistics Office’s data.

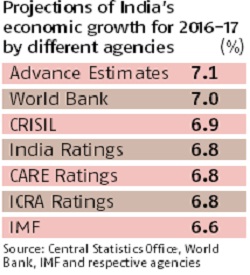

However, as the GDP was slowing even before demonetisation and the note swap has indeed had an incremental adverse effect on it, both GDP and GVA growth for 2016-17 have been projected to be much lower than in the previous year. In the second advance estimate, the CSO has kept the GDP growth estimate for the current financial year at 7.1%, the same as in the first advance estimate released in early January, and GVA growth at 6.7%. But given that 2015-16 GDP growth, which was seen at 7.6% at the time of the first advance estimate, was subsequently revised to 7.9%, the CSO’s latest take on 2016-17 growth is virtually more sanguine than its previous estimate.

While the CSO’s GDP estimate for 2016-17 is evidently higher than that of most others, many analysts said the growth assumed by it for the second half (6.8%) was optimistic. “Given the fact that the fall from H1 to Q3 is not much, I don’t think that we should then necessarily assume that the rebound in Q4 is going to be very sharp,” said Aditi Nayar, economist at Icra. Stating that the GDP number is better than expected, Saugata Bhattacharya, chief economist at Axis Bank, said, “Since growth slowdown (due to demonetisation) has been shallower than expected, and in line with the RBI’s projections, the probability of rate cuts going ahead has come down.”

The minutes of the monetary policy committee’s meeting released last week indicated that it changed its stance from “accommodative” to “neutral” because the growth drag from demonetisation is expected to fade soon. India Ratings reiterated its view that “much of the impact of demonetisation will be visible in Q4FY17 leading to an overall GDP growth of 6.8% in 2016-17”.

Economic affairs secretary Shaktikanta Das said: “This year’s GDP (growth) is around 7%, based on available numbers. Nothing can be deciphered on anecdotal evidence. Demonetisation only impacted consumption in some cities, since most purchases happened on credit or debit cards. The so-called negative impact, if relevant, was only temporary.”

The 7% GDP growth forecast for the third quarter helped India maintain the coveted tag of the world’s fastest-growing major economy despite demonetisation, better than China’s 6.8% in the December quarter.

While analysts pointed out the lack of congruity between the CSO’s estimate and other high-frequency data and corporate results, chief statistician TCA Anant said all available data have been made use of in the second advance estimate, including corporate performance up to the December quarter, sales of commercial vehicles, railway freight, etc, for the first “9/10 months of the financial year”.

According to the CSO, with production growth of foodgrains during 2016-17 kharif and rabi seasons being 9.9% and 6.3%, respectively, the farm sector grew a robust 6% in Q3 from 3.8% in the previous quarter and compared with a 2.2% contraction in the year-ago quarter. Despite the anecdotes of industrial clusters hit by the note ban during the period, manufacturing grew a healthy 8.3% in Q3 on a robust base of 12.8% in the year-ago quarter and compared with 6.9% in Q2 this fiscal. Mining also posted a smart recovery from a fall of 1.3% in Q2 to a robust expansion of 7.5% in Q3. The bad performers on the output side was “financial services, etc”, which posted a modest 3.1% growth in Q3 compared with 7.6% in the previous month, and construction which grew just 2.7% in the December quarter.

Government final consumption expenditure (GFCE) posted a 19.9% growth in Q3 against 15.2% in the previous quarter, the CSO said. Given that 17% growth in GFCE is estimated for the whole of 2016-17, it needs to grow at 17.4% in Q4. Considering that the Centre, as is seen from the April-January fiscal data separately released by the Controller General of Accounts, has slowed down spending in the later months of the year, the spending boost must come from PSUs.

Although both Dussehra and Diwali fell in the December quarter, the 10.1% growth reported by CSO in the private consumption expenditure looked puzzling to most analysts (but some said use of old notes for consumption might have contributed to the rise). So was the 3.5% growth in gross fixed capital formation, which was declining for the previous three quarters.

Given that nominal GDP growth has been projected at 11.5% for 2016-17, compared with 10% in the last fiscal, it may offer more leeway to the government to improve spending in the next fiscal and yet contain fiscal deficit, which is expressed as a ratio of the nominal GDP, at the targeted 3.2%.

Discrepancies — the difference between the supply and demand side of GDP — turned negative after a gap of four quarters (-Rs 6,767 crore) in the December quarter, compared with Rs 45,378 crore in the second quarter and Rs 30,645 crore in the first quarter. In the last quarter of 2015-16, discrepancies touched a massive Rs 1,43,210 crore, causing a flutter then and raising doubts about the credibility of the country’s data collection mechanism. When private final consumption expenditure, gross fixed capital formation, government final consumption expenditure, change in stocks, valuables, and net exports exceed the overall GDP (based on the supply side data), discrepancies turn negative.

Analysts expect the exports sector to contribute more to GDP growth in the coming quarters, despite the demonetisation blues, thanks primarily to a favourable base. In real terms, the export growth for 2016-17 has been projected at 2.3%, compared with -5.4% in the last fiscal. Despite demonetisation, merchandise exports rose 2.3% in November, 5.7% in December and 4.3% in January.

India’s economic growth would slow to about six per cent in the second half of this financial year (October-March) due to demonetisation, against 7.2 per cent in the first half, the International Monetary Fund (IMF) said on Wednesday.

India’s representative in IMF Subir Gokarn said the growth projections came at a time when hard data was unavailable. He described the assessment as “unduly pessimistic”. In the medium term, however, the IMF is hopeful that implementation of the Goods and Services Tax could raise India’s growth rate to more than eight per cent.

The Fund said the cost of recapitalising public sector banks would be affordable even under a negative scenario. In a report on India, the IMF said growth would gradually rebound in 2017-18.

In January, it had cut India’s growth estimate to 6.6 per cent for 2016-17 due to the note ban, against 7.6 per cent estimated earlier. Growth was estimated to be 6.2 per cent in the fourth quarter of the financial year.

Taking both the estimates into consideration, the IMF said, third quarter growth might fall below six per cent.

The Central Statistics Office will come out with the third quarter gross domestic product (GDP) data and the revised advance estimates on the coming Tuesday. Its first advance estimates had shown economic growth at 7.1 per cent in 2016-17, against 7.6 per cent the previous year. The office had not taken into account the effect of demonetisation.

Commenting on IMF’s revision of growth rates, Gokarn said, “While we do not question the methodologies used to revise the estimates, the fact is that there isn’t very much hard data to base the revisions.” He said different assumptions about the impact would obviously lead to different conclusions. While virtually all forecasters have revised their projections for 2016-17 downwards, the range was relatively wide, he added.

To buttress his points, Gokarn said the World Bank and the Asian Development Bank have pegged growth at seven per cent, after accounting for change in the currency policy. The authorities’ estimate was 7.1 per cent. IMF directors supported India’s efforts to tackle illicit financial flows, but noted the strains that have emerged from the currency exchange initiative. They called for action to quickly restore the availability of cash to avoid further payment disruptions, and encouraged prudent monitoring of the potential side-effects of the initiative on financial stability and growth. On tackling India’s $130 billion in stressed loans, the IMF said “recapitalisation costs should be manageable” at between 1.5 and 2.4 per cent of the GDP forecast, according to Reuters.

Of that, the government’s share would be between 1.0 and 1.6 per cent of GDP over the four years to March 2019, assuming 40 per cent of the loans have to be provided against. “It’s very positive that both the Reserve Bank of India (RBI) and the government are putting a shared focus on addressing the balance-sheet problem,” IMF Resident Representative Andreas Bauer told a conference call.

The chief economic advisor, Arvind Subramanian, on Wednesday backed a call by the RBI to set up an institution similar to “bad bank”, saying urgency was needed to address troubled loans weighing on the banking sector.

In a special report on corporate and banking sector risks in India, the IMF said recapitalisation costs would be “significantly higher if there is a policy shift to more conservative provisioning requirements”.

In case of a rise in the provisioning ratio to 70 per cent, cumulative recapitalisation needs would increase to 3.3-4.2 per cent of forecast GDP in the financial year to March 2019, with a government share of 2.2-2.8 per cent, the IMF said.

The IMF said with temporary demand disruptions and increased monsoon-driven food supplies, inflation was expected at about 4.75 per cent by early 2017— in line with the Reserve Bank of India’s inflation target of 5 per cent by March 2017.

The Fund said domestic risks flow from a potential further deterioration of corporate and public bank balance sheets, as well as setbacks in the reform process, including in GST design and implementation, which could weigh on domestic demand-driven growth and undermine investor and consumer sentiment.

On the upside, IMF said larger than expected gains from GST and further structural reforms could lead to significantly stronger growth; while a sustained period of continued-low global energy prices would also be very beneficial to India.

The FIPB, headed by economic affairs secretary Shaktikanta Das, deferred 6 proposals, including that of Gland Pharma with the proposed FDI inflow of Rs8,800 crore.

Inter-ministerial body, foreign investment promotion board (FIPB) on Tuesday approved 15 investment proposals, including that of Apollo Hospitals, Hindustan Aeronautics Ltd, Dr. Reddy’s Laboratories and Vodafone, envisaging foreign investment of Rs12,200 crore. “15 out of 24 FDI proposals were approved while three were rejected,” people familiar with the matter said.

The FIPB, headed by economic affairs secretary Shaktikanta Das, deferred 6 proposals, including that of Gland Pharma with the proposed FDI inflow of Rs8,800 crore.

These proposals were deferred for further consultation and want of more information, sources added. Among the proposals approved, Twinstar Technologies will alone bring foreign capital of about Rs9,000 crore into the country.

Besides, proposal of Apollo Hospitals worth Rs750 crore and public sector Hindustan Aeronautics worth Rs170 crore for helicopter manufacturing also got green signal from the board.

The government has already announced winding up of FIPB by putting in place a new mechanism, a move which will further improve ease of doing business.

Finance minister Arun Jaitley in his Budget 2017-18 announced abolishing FIPB saying 90% of the foreign investment approvals are via automatic route and only 10% go to the board.

Currently, FIPB offers single-window clearance for applications on FDI in India that are under the approval route. The sectors under automatic route do not require any prior approval and are subject to only sectoral laws.

India allows FDI in most sectors through the automatic route, but in certain segments that are considered sensitive for the economy and security, the proposals have to be first cleared by the FIPB. With growth in FDI in important sectors like services and manufacturing, overall foreign inflows in the country rose by 30% to $21.62 billion during the first half of 2016-17. FDI in the country grew by 29% to $40 billion in 2015-16 as against $30.94 billion in the previous financial year.

India is expected to attract moderate FII inflows of $15-$20 billion in 2018, with headwinds such as the muted outlook for corporate earnings and continued compression in debt spreads relative to advanced economies, rating agency ICRA said in a report on Tuesday.

“With the muted outlook for corporate earnings and emerging sectoral concerns regarding Indian software and pharmaceuticals exports to the US, the net FII equity inflows are likely to be restricted below $5 and $10 billion respectively in FY17 (2016-17) and FY18 (2017-18), in our view,” said ICRA Senior Vice President and Group Head-Financial Sector Ratings, Karthik Srinivasan.

The agency expects aggregate FII debt outflows in FY17 of $6-$8 billion, followed by aggregate inflows of $5-$10 billion during FY18.

“Indian bond yields are unlikely to ease significantly below current levels, given the limited further monetary easing expected from the Reserve Bank of India.

“Moreover, the supply of net long term borrowings of the government is likely to increase in FY2018 from Rs 4.1 trillion in FY2017, as the central government is likely to budget a fiscal deficit range between 3 and 3.5 per cent of the GDP,” he said.

The Indian markets had witnessed record FII outflows of $11.3 billion during Q3 (third quarter) FY17 on the back of a combination of international and domestic factors, including the risk-off sentiment triggered by the outcome of the US presidential election in November 2016 and the tightening of monetary policy by the US Federal Reserve in December 2016.

The RBI will embark on its biggest banking clean-up exercise after President Pranab Mukherjee promulgated an ordinance authorising it to issue directions to banks to initiate insolvency resolution process in the case of loan default.

The RBI will embark on its biggest banking clean-up exercise after President Pranab Mukherjee promulgated an ordinance authorising it to issue directions to banks to initiate insolvency resolution process in the case of loan default.