The Ministry of Corporate Affairs (MCA) has decided to give 21 lakh India Inc directors another 15 days to reactivate their Director Identification Numbers (DINs) by filing Know-Your-Customer (KYC) details upon paying a reduced fee. The decision was taken by Finance and Corporate Affairs minister Arun Jaitley on Wednesday. The notification regarding the extension of deadline is as below.

The Ministry of Corporate Affairs (MCA) has decided to give 21 lakh India Inc directors another 15 days to reactivate their Director Identification Numbers (DINs) by filing Know-Your-Customer (KYC) details upon paying a reduced fee. The decision was taken by Finance and Corporate Affairs minister Arun Jaitley on Wednesday. The notification regarding the extension of deadline is as below.

As you are aware the last date for filing form DIR-3 KYC without fee has expired on 15th September 2018. The process of deactivating the non-compliant DINs has since been completed and their status has been updated as ‘Deactivated due to non-filing of DIR-3 KYC’. However, the non-compliant DIN holders may file DIR-3 KYC with a fee of Rs.500 (Rupees Five Hundred Only) from 21st September till 5th October 2018(both days inclusive) to get their DINs reactivated. From 6th October 2018 onwards, a fee of Rs.5000 (Rupees Five Thousand Only) becomes payable for reactivation.

DINs, the unique identification numbers, of nearly 21 lakh directors were deactivated by the MCA following non-filing of KYC details.

“The directors will be given another 15-day extension to reactivate their DINs by filing the e-form along with a nominal fee, which is being kept much lower than the current late fee of Rs 5,000,” top government sources said.

Many individuals and professional bodies, including the Institute of Chartered Accountants of India (ICAI) and Institute of Companies Secretaries of India (ICSI), have written to the government seeking extension in the date of submission for KYC without any additional fee. They have citied practical difficulties such as time-consuming process of obtaining digital signatures, video verification, reaching out to foreign directors and Kerala floods among the reasons for the delay.

“It took us an average time of one to one-and-a-half hour to do one KYC filing. It is quite time consuming to get the digital signature and then feed the client details on MCA software. Many a times the site shows glitches,” said Ashok Tyagi, a company secretary, who is looking forward to an extension in the filing time.

After the last date for filing of the e-KYC form, the MCA deactivated DINs of nearly 21 lakh directors, about 63% out of a total of 33 lakh directors registered in the country after they failed to furnish their KYC details. Only 12.15 lakh directors filed their KYC details within the stipulated time.

DIN is the unique number allotted to the directors on the Boards of registered companies without which they can’t sign any compliance document on behalf of the company.

According to some government officials, not more than two lakh directors are likely to come forward to file KYC over next 15 days. “A large number of directors will be dummy directors or the ones having multiple DINs,” said an official.

The MCA launched the e-KYC form under the MCA 21 system on July 14, this year. All the 33 lakh directors were required to provide their personal details such as e-mail address, Permanent Account Number (PAN) and Aadhaar number in an e-filing with the government in a major clean-up drive on ‘fly by night and dummy directors’. The directors also had to upload their short videos introducing themselves. The directors who could not comply with the new rule could, however, get their DINs activated provided they paid a sum of Rs 5,000 as late fee.

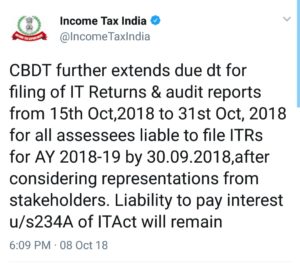

The Central Board of Direct Taxes (CBDT) has further extended due date for filing Income Tax Returns and Audit Reports to October 31st.

The Central Board of Direct Taxes (CBDT) has further extended due date for filing Income Tax Returns and Audit Reports to October 31st.