The department said it was the final call for filing of belated or revised ITRs for assessment years 2016-17 and 2017-18

The Income Tax Department on Friday urged those who deposited “large amounts of cash” post demonetisation and all companies to file their returns by March 31, failing which they may face penalty and prosecution.

It also cautioned eligible trusts, political parties and associations to file their income tax returns by this final deadline and “come clean”.

The department, in public advertisements issued in leading dailies, said it was the final call for filing of belated or revised ITRs for assessment years 2016-17 and 2017 -18.

It underlined that there was still time for these categories of taxpayers and that they should avoid last minute rush and file the ITRs well before the deadline.

“If you have deposited large amounts of cash in your bank account/made high value transactions, please consider the same while filling your ITRs.

“Non-filing or incorrect filing of return of income may result in penalty and prosecution,” the public advisory said. It said all companies, firms and limited liability partnership concerns were also required to do so.

The deadline is also applicable, it said,to trusts, associations and political parties whose income prior to claim of exemptions exceeds the minimum chargeable to tax. Individuals and Hindu Undivided Families having income more than Rs 2.5 lakh and senior citizens with income of over Rs 3 lakh (60-80 years of age) and Rs five lakh (over 80 years of age) too need to file their returns for the mentioned assessment years, it said.

India’s foreign exchange reserves swelled by USD 4.12 billion to a new high of USD 421.914 billion on a healthy increase in the core currency assets and uptick in the gold stock, the Reserve Bank said today.

The total reserves had risen by USD 3 billion to USD 417.89 billion in the previous reporting week.

The reserves had crossed the USD 400-billion mark for the first time in the week to September 8, 2017 but have been fluctuating since then.

However, there has been a continuous surge since the start of this year for the fifth straight week. In reporting week to February 2, foreign currency assets, a major component of the overall reserves, rose by USD 3.025 billion to USD 396.769 billion, the RBI said.

Expressed in US dollar terms, the foreign currency assets include the effect of appreciation or depreciation of the non-US currencies such as the euro, the pound and the yen held in the reserves.

The value of gold reserves rose USD 1.092 billion to USD 21.514 billion during the week, the central bank said.

The country’s special drawing rights with the International Monetary Fund rose by USD 3.2 million to USD 1.547 billion, while the country’s reserve position with the Fund jumped by USD 4.3 million to USD 2.084 billion during the reporting week, the central bank said.

Budget 2018 has been presented by the Finance Minister Arun Jaitley and here are the key takeaways:

Personal tax

While the personal income tax structure remains the same-that is no new tax slab and no higher exemption limits-as a as a small concession, Jaitley has announced a standard deduction of Rs 40,000 for salaried taxpayers. This will be in lieu of the existing transport allowance and medical expense reimbursement. However, other medical reimbursements in case of hospitalisation will continue.

According to him, the existing allowances amount to Rs 30,000 so the actual tax benefit here on would be Rs 10,000 more for each taxpayer. This move is expected to benefit 2.5 crore people-25-30% of the total taxpayer base–and reduce paperwork along the way. The revenue cost of this concession is pegged at Rs 8,000 crore.

But if he is putting money in your wallets, his other hand is also taking cash away. The education cess levied on the tax you pay (also applicable on corporation tax) has gone up by 1%. The new 4% Health and Education Cess is expected to help the government collect an additional amount of Rs 11,000 crore.

Senior citizens

Apart from farmers and the gareeb nagrik, it is the older demographic that stands to gain the most from the latest Budget. To begin with, tax exemption of interest income from bank deposits has been raised to Rs 50,000 from the current Rs 10,000. He has also proposed to raise the deduction under health insurance premium under Section 80D of the Income Tax Act to Rs 50,000 (from Rs 30,000 currently). In case of senior citizens with critical illnesses the deduction will be Rs 1 lakh. Moreover, Fixed Deposit/Post office interest to be exempt till Rs 50,000. These concessions are expected to give senior citizens extra tax benefit of Rs 4,000 crore.

In addition to tax concessions, the government has proposed to extend the Pradhan Mantri Vaya Vandana Yojana up to March 2020 under which an assured return of 8% is given by Life Insurance Corporation of India (LIC). The existing limit on investment of Rs 7.5 lakh per senior citizen under this scheme is also being enhanced to Rs 15 lakh.

Corporate tax

Jaitley has announced that companies with a turnover of up to Rs 250 crore will now be taxed at 25% (from 30%). According to him, this move will benefit 99% of companies and the revenue foregone is pegged at Rs 7,000 crore in 2018-19. After this, out of about 7 lakh companies filing returns, only about 7,000 companies will remain in 30% tax slab.

The other bit of bad news is that the FM proposed to tax long term capital gains exceeding Rs 1 lakh on sale of equity shares/units of Equity oriented Fund at 10%, without allowing any indexation benefit. To justify his move, he pointed out that the total amount of exempted capital gains had surged to nearly Rs 360,000 crore, as per returns filed for assessment year 2017-18, and that the return on equity was attractive even without exemptions. A major part of this gain has reportedly accrued to corporates and LLPs. So while retail investors will also be hurt by this move, the impact will be most felt by corporates.

However, existing investors will be exempted from capital gains tax up to January 31, 2018. All gains made thereafter this cut-off date will be taxed. This move could earn the government Rs 20,000 crore in revenue in the first year. The revenues in subsequent years may be more.

Petrol/diesel prices

In a rejig of excise duty on petroleum products, the union government has cut basic excise duty on petrol and diesel by Rs 2. The Modi government has also abolished additional excise duty on fuel by Rs 6. Despite that petrol prices are likely to remain the same as a new road cess of Rs 8 per litre has been introduced.

Farmers

The Union Budget 2018 seems to have been the shot in arm it was predicted to be for the slowing agricultural sector of India. Staying true to government’s electoral promise of doubling farmers’ income by 2022, Jaitley kept the minimum support price (MSP) of kharif crops and all rabi crops at one and a half times the production cost of the crops. Currently, most of the rabi crops get that benefit.

In addition, an Agri-Market Infrastructure Fund of Rs 2000 crore will be set up for developing agricultural markets. Jaitley further allotted Rs 500 crore under Operation Greens-to be launched on the lines of ‘Operation Flood’-to address price volatility of perishable commodities and to promote Farmer Producers Organizations (FPOs), agri-logistics, processing facilities and more.

As per provisions of Budget 2018, government will encourage organic farming by FPOs and Village Producers Organizations (VPOs) in large clusters, preferably of 1000 hectares each. Women Self Help Groups will also be encouraged to take up organic agriculture in clusters under National Rural Livelihood Programme. Also, a sum of Rs 200 crore have been allocated to support organized cultivation of highly specialized medicinal and aromatic plants and aid small and cottage industries that manufacture perfumes, essential oils and other associated products.

Significantly, calling bamboo “green gold”, the finance minister announced the launch of a restructured National Bamboo Mission with an allocation of Rs 1,290 crore. The government will also set up two new funds for the fisheries sector and animal husbandry sector with a total corpus of Rs 10,000 crore.

Explaining that India’s agri-exports potential is as high as $100 billion against current exports of $30 billion, Jaitley wants export of agri-commodities to be liberalized. “I also propose to set up state-of-the-art testing facilities in all the forty two Mega Food Parks,” he added.

Lastly, the Budget not only proposed to raise institutional credit for agriculture to Rs 11 lakh crore for 2018-19 (up from Rs 10 lakh in the current fiscal) but also addressed the issue of air pollution due to burning crop residue. The Finance Ministry said that a special scheme will be implemented to support the efforts of the governments of Haryana, Punjab, Uttar Pradesh and the NCT of Delhi to address air pollution and to subsidize machinery required for disposal of crop residue.

The icing on the cake is the announcement of 100% tax deduction for first five years to companies registered as farmer producer companies with a turnover of Rs 100 crore and above.

Poor families

“From ease of doing business, our government has moved to ease of living for the poor and middle class,” Jaitley said in his speech. But he actually meant only poor families, who have been extended a plethora of schemes and allocations. Take the new National Health Protection Scheme under which annual health coverage of up to Rs 5 lakh per family will be offered for secondary and tertiary care hospitalization. This is expected to benefit over 10 crore vulnerable and under-privileged families. “This will be the world’s largest government funded health care programme,” Prime Minister Narendra Modi said in his address soon after the Budget speech.

The government will also establish 1.5 lakh Health and Wellness Centres under the Ayushman Bharat programme to provide comprehensive health care-including for non-communicable diseases and maternal and child health services-free essential drugs and diagnostic services. The Budget has earmarked Rs 1200 crore for this flagship programme.

In line with the government’s “Housing for All by 2022” promise, Jaitley announced that a dedicated Affordable Housing Fund will be set up, funded from priority sector lending shortfall and fully serviced bonds authorized by the government.

Also on the cards are free LPG connections to 8 crore poor women-up from the initial target of 5 crore beneficiaries-under the Ujjwala Scheme; two crore more toilets under Swachh Bharat mission, and a whopping Rs 16,000 crore allocation for the Saubhagya Yojana, under which four crore poor households are being provided with electricity connection free of charge.

Railways

Jaitley has proposed an ambitious plan for Indian Railways with a focus on modifications and safety rather than new train lines. He announced a capital expenditure allocation of Rs 1.48 lakh crore-the highest ever-for capacity expansion, maintenance of tracks, transforming almost the entire network into broad gauge, redevelopment of railway stations, producing upend coaches, the bullet train project, safety policies and more.

The FM announced that Wi-Fi, CCTVs will be provided in every station and escalators will be provided in stations with more than 25,000 footfalls. In the coming year, there will be a focus on upgradation of signalling and use of fog safety devices. He added that 600 railway stations across the country have been picked for modernisation and 4,000 km of railway network is set to be commissioned for electrification.

According to him, the coming year will be dedicated to building world-class trains and a railway institute will be set up in Vadodara, where the workforce behind high speed railway projects would be trained. There will also be a special focus on the upliftment of suburban trains in Mumbai and Bengaluru.

Education

“In order to further enhance accessibility of quality medical education and health care, we will be setting up 24 new Government Medical Colleges and Hospitals by upgrading existing district hospitals in the country. This would ensure that there is at least one medical college for every three parliamentary constituencies and at least one government medical college in each state,” said Jaitley.

Significantly, by 2022, every block with more than 50% scheduled tribe population and at least 20,000 tribal people will have ‘Ekalavya’ school at par with Navodaya Vidyalas. Jaitley also announced a new scheme for revitalizing school infrastructure, with an allocation of Rs 1 lakh crore over four years. He added that an integrated BEd programme will be initiated for teachers, to improve the quality of teachers.

Custom duties

Custom duty on mobile phones increased from 15% to 20%. The duty applicable on some mobile phone parts and accessories has been hiked to 15% and that on certain parts of TVs to 15%. “To help the cashew processing industry, I propose to reduce customs duty on raw cashew from 5% to 2.5%,” added Jaitley.

Significantly, Budget 2018 has levied a “social welfare surcharge” at 3-10% on imports in place of the Education Cess and Secondary and Higher Education Cess currently in place.

Non-corporate taxpayers operating in IFSC to be charged alternate minimum tax at concessional rate of 9% at par with minimum alternate tax applicable for Corporates.

In order to promote trade in stock exchanges located in International Financial Services Centre (IFSC), the Union Finance and Corporate Affairs Minister Arun Jaitley proposed to provide two more concessions for IFSC.

Presenting the General Budget 2018-19 in Parliament Jaitley proposed to exempt transfer of derivatives and certain securities by non-residents from capital gains tax. Further, the Finance Minister added that non-corporate taxpayers operating in IFSC shall be charged Alternate Minimum Tax (AMT) at concessional rate of 9% at par with Minimum Alternate Tax (MAT) applicable for corporates.

The Government had endeavored to develop a world class international financial services centre in India. In recent years, various measures including tax incentives have been provided in order to fulfil this objective.

A monthly collection of around ₹80,000 cr appears sufficient to meet the Centre’s and States’ needs

The Goods and Services Tax (GST) collections for December 2017 show an increase, but despite this there are concerns that the tepid collections since July could pose a problem on the fiscal deficit front.

However, a closer look at the numbers shows that these fears are misplaced. The Centre’s tax collection, as per the CGA (Controller General of Accounts), appears to be on track to achieving the Budget estimates for 2017-18. There are, however, many trouble spots in the new regime.

The complexity of the GST, which combines many of the indirect taxes of the Centre and States, has made it quite difficult to estimate the expected monthly collection target.

At a press conference in August 2017, Finance Minister Arun Jaitley said that the collections in July were better than the target of ₹91,000 crore for that month. This figure has been used since then as a ball-park figure for measuring monthly GST collections.

If we use this figure, GST collections in October (₹83,346 crore), November (₹80,808 crore) and December (₹86,703 crore) are well short of the target. But that may not really be the case.

To estimate the targeted monthly GST collection, we worked backward to see the projected revenue in the Budget estimate for 2017-18 from goods and services that have been put under GST. While service taxes have mostly moved under GST, only about a third of excise duty collections are under GST since the taxes on many petroleum products are still outside the new regime. Under Customs duty, almost 64 per cent of the collections are now under GST.

Using this basis, around ₹43,000 crore of GST need to be collected by the Centre monthly towards its indirect tax collections. A portion of this will devolve to the States as part of their share in the Centre’s revenue.

States totally have to be disbursed ₹43,000 crore every month, assuming 14 per cent annual growth from their 2015-16 revenue. Working with these numbers, a monthly GST collection of around ₹80,000 crore appears sufficient to meet the Centre’s and States’ needs.

Actual numbers

The fact that the Centre has not fallen short in its indirect tax collections is borne out by the numbers from the CGA. Gross tax revenue of the Centre for the period between April to November 2017 was ₹10,87,302 crore, up 16.5 per cent from the amount collected in the same period in 2016-17.

Interestingly, gross indirect tax collection of the Centre in this period was up 18.2 per cent, having risen from ₹5,08,924 crore to ₹6,01,904 crore.

While the devolution to States was 25 per cent higher, the Centre’s net tax revenue has managed to increase 12.59 per cent, showing that the Finance Minister will not have too much difficulty in balancing the fisc.

The catch

While the Centre’s collections are on track, allocations to States can pose a problem. “Due to the fact that IGST revenue is disbursed over a period of time, there is a thinking amongst States that there is a revenue shortfall,” explains Gautam Khattar, Partner, Indirect tax, PwC.

Disputes on input-tax credit claimed by businesses in the provisional GSTR 3B form are another issue that could impede calculations. “Definitely, this is the major concern for the Department because invoice matching is the backbone of GST,” says Vishal Raheja, DGM, Taxmann.

India-focused funds together raised about $3.1 billion in 2017, according to Preqin data.

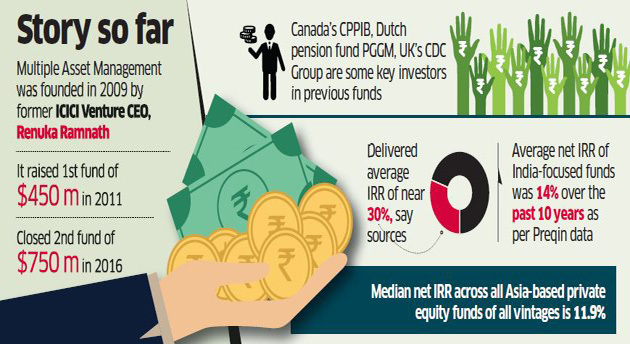

Multiples Alternate Asset Management, the private equity fund founded by former ICICI Venture CEO Renuka Ramnath, is set to raise as much as $1billion in what could be one of the largest capital-raising plans by a domestic asset manager.

The programme, which is expected to start in February, will target pension funds, sovereign wealth funds and university endowments in North America, Europe, the Middle East and South East Asia, two people with knowledge of the matter said.

The proposed fund will be equivalent to almost one-third of the capital raised by 29 India-focused private equity and venture capital funds in 2017.

The fund is being launched with appetite for long-term capital after a relative lull of almost a decade. Big-ticket asset owners such as pension and sovereign funds have started putting in money since last year, especially after Moody’s Investors Service upgraded India’s sovereign rating outlook, which lifted sentiment towards one of the fastest-growing economies.

Multiples raised its first fund of $400 million in 2011 and its second fund of $750 million in 2016. It has delivered an average internal rate of return (IRR) of 30% to investors, sources said.

The average net IRR of India-focused funds was 14% over the past 10 years, according to London-based data tracker Preqin, compared with the median net IRR of 11.9% across all Asia-based private equity funds of all vintages.

“Yes, we have already started discussions with our existing limited partners and are looking to start marketing roadshows from Febru-ary. We expect the first close by mid of this year and a final close by December,” said one of the two people.

Founded in 2009 by Ramnath, former managing director and CEO of ICICI Venture, the private equity arm of the country’s biggest private lender, ICICI Bank, Multiples manages close to $1billion assets, its website showed. It counts Canada Pension Plan Investment Board and other North American pension money managers and university endowments as its largest limited partners or investors.

These investors have already committed to the fresh fundraising. Some of the investments by Multiples include Arvind, Cholamandalam Investment & Finance, Indian Energy Exchange and RBL. Last January, the firm sold its 14% stake in India’s largest movie hall chain PVR to rival private equity fund Warburg Pincus for Rs 820 crore, making a return on more than three times on its four-year-old investment, in constant currency terms.

India-focused funds together raised about $3.1 billion in 2017, according to Preqin data. This is more than double the money raised by 18 asset managers in 2016. Last year, former Temasek India head Manish Kejriwal’s Kedaara Capital raised about $750 million for its second fund, while IDFC Alternatives raised $350 million.

PE fundraising slowed soon after the Lehman crisis with asset managers struggling to get out of their investments as valuations were rearranged, said the head of a large US fund in India. “The Moody’s upgrade and related strength seen in the economy and continued strong sentiment are expected to keep the India story intact,” he added.

Foreign portfolio investors (FPIs) have invested a phenomenal $3 billion (close to Rs 18,000 crore) in India’s capital markets this month on expectations of high yields as corporate earnings are expected to pick up with the economy gathering momentum after the slowdown due to the chaotic implementation of GST.

The sharp increase in inflows comes after an outflow of over Rs 3,500 crore by foreign portfolio investors (FPIs) from the capital markets in December, data compiled by depositories shows. According to market analysts money pumped in by FPIs has played a key role in fuelling the bull run in the stock markets that saw both the Sensex and Nifty on a record breaking spree in recent weeks.

FPIs infused a net amount to the tune of Rs 11,759 crore in stocks and Rs 6,127 crore in debt during January 1-25 — translating into net inflows of Rs 17,866 crore. For the entire 2017, FPIs invested a collective amount of Rs 2 lakh crore in the country’s equity and debt markets.

The inflow in the current month can be attributed to anticipation of earnings recovery and attractive yields which is expected to further strengthen inflow from foreign investors in the current financial year, said Dinesh Rohira, CEO of 5nance, an online platform providing financial planning services.

However, Quantum MF Fund Manager-Fixed Income Pankaj Pathak believes that FPIs may not be able to repeat this showing in 2018 as withdrawal of liquidity and rate hikes in developed economies pick up. This would provide them with alternative avenues of investment.

The FPI investments have also helped to bolster the country’s foreign exchange reserves which touched an all-time high of USD 414.784 billion in the week to January 19, Reserve Bank data showed. The RBI data showed that the forex reserves rose by USD 959.1 million to touch a record high during the reporting week. In the previous week, the reserves had touched USD 413.825 billion after it rose by USD 2.7 billion.

The reserves had crossed the USD 400-billion mark for the first time in the week to September 8, 2017 but have since been fluctuating. But for the past four weeks the figure has shown a continuous rise. Higher foreign exchange reserves lead to a stronger rupee which in turn reduces the cost of imports as fewer rupees have to be paid to buy the same amount of dollars to pay for items such as crude oil.

A higher foreign exchange kitty also provides a comfortable cushion to finance imports especially at a time when crude prices are shooting up in the international market and the country’s trade deficit has been growing. However, while FPI inflows add to the forex reserves they are considered “hot money” as they can leave Indian shores at short notice and this could send the rupee into a tailspin.

A senior finance ministry official said that foreign direct investment (FDI) is a more stable source of funding for the economy and since it also creates jobs and incomes the government is keen to see an increase in such investments. The Prime Minister’s trip to Davos was aimed at achieving this goal, he pointed out. He said that the government has been working on the ease of doing business which has seen a sharp increase in FDI inflows and this policy will continue in the forthcoming budget. At the same time the government is keen FPI inflows are not disrupted due to tax levies on stocks that create uncertainties, he added.