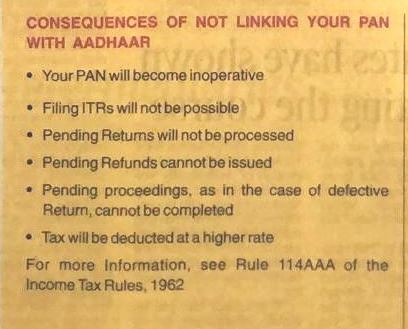

Govt has declared March 31, 2023 as the deadline for linking PAN and Aadhaar. Failing to link will make PAN inactive.

It is mandatory to link Permanent Account Numbers (PAN) to Aadhaar by March 31, 2023.

The last date to link Permanent Account Number (PAN) to Aadhaar is nearing soon. According to the Central Board of Direct Taxes (CBDT), the apex body of the Income Tax department, it is mandatory to link Aadhaar to Permanent Account Numbers (PAN) by March 31 this year, failing which the PAN will become ‘inoperative’ on April 1. The previous deadline for linking was March 31, 2022, but the government extended it with a Rs. 1000 penalty fee.

PAN and Aadhaar are both unique identification cards that serve as proof of identity and are required for verification.

Benefits of linking PAN with Aadhaar

– Multiple PAN Cards: Linking of PAN and Aadhaar eliminates the possibility of an individual having more than one PAN Card, thereby reducing fraudulent activities.

– Prevent Tax Evasion: The Income Tax Department will be able to detect any form of tax evasion after PAN is linked with Aadhaar.

-Income Tax Returns: The process of filing income tax returns will become significantly simpler because individuals will no longer be required to provide proof that they have filed their income tax returns. Since Aadhaar holds all the information about an individual including biometric verification, the linking will initiate a faster return filing process.

– Linking your Aadhaar to PAN will prevent the tax return process from being cancelled and will also help in summarising one’s taxes attached to the Aadhaar for furture references.

Steps to link PAN with Aadhaar via web portal:

1. Visit the Income Tax e-filing official websites- eportal.incometax.gov.in or incometaxindiaefiling.gov.in

2. Register on the portal with your PAN as the user ID if not registered already.

3. Log into the portal.

4. A pop-up window will appear to link PAN with Aadhaar or go to ‘Profile Settings’ on the Menu bar and click on Link Aadhaar.

5. Relevant details like name, date of birth, and gender will already be mentioned as per the PAN card details.

6. Verify the details with Aadhaar. If the details match, enter the Aadhaar number and click on the link now button.

7. A message will pop up saying that the Aadhaar has been successfully linked to the PAN.

Other methods of linking PAN with Aadhaar:

1. People can also visit the following websites for the linking process- https://www.utiitsl.com/ and https://www.egov-nsdl.co.in/

2. Through SMS: Type the following message UIDPAN<12 digit Aadhaar><10 digit PAN>. The message can be sent to 567678 or 56161.

3. Visiting nearby PAN service centres: The linking process can also be done manually by visiting the nearby PAN service centre.

Unable to link ?

– You may be unable to link your PAN to Aadhaar in some cases. The most common reason for rejection is a mismatch between the information in your PAN and Aadhaar. Ideally, your demographic information (name, gender, and date of birth) should match in both the documents.

– If there is a minor mismatch between your Aadhaar Name and the actual data in Aadhaar, a One Time Password (Aadhaar OTP) will be sent to the mobile phone registered with Aadhaar. Ensure that PAN and Aadhaar have the same date of birth and gender.

– In a rare case where Aadhaar name is completely different from name in PAN, then the linking will fail and you will be prompted to change the name in either Aadhaar or in PAN database.

– However, once the corrections have been made, you will able to link the PAN and Aadhaar.

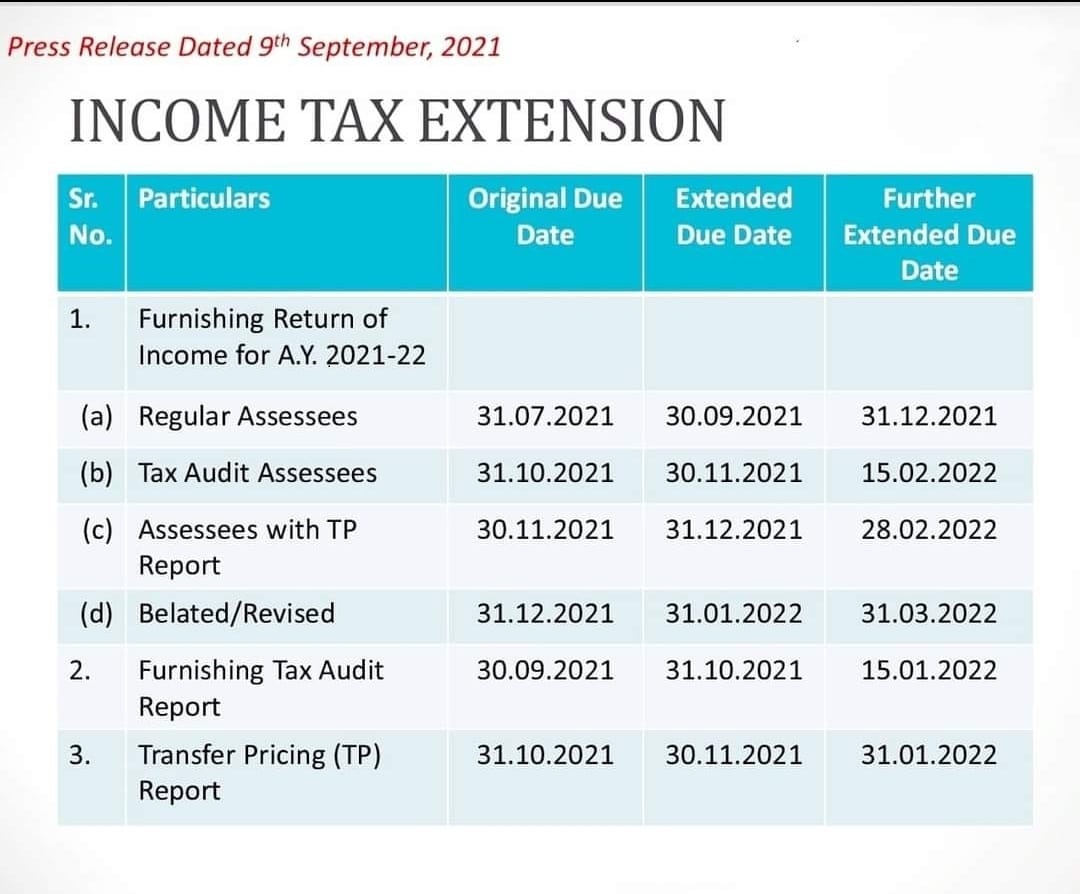

• This is the second time this financial year the government has extended the deadline of filing ITR for individuals whose accounts are not required to be audited. • The ITR filing deadline has been extended due to the many technical issues related to the government’s newly launched tax filing portal. • The deadline of filing belated/revised ITR has been extended by two months to March 31, 2022.

The government on Thursday extended the deadline to file income tax return (ITR) for FY 2020-21 by 3 months to December 31, 2021 from September 30, 2021. The extension of the deadline is for those individuals whose accounts are not required to be audited and who usually file their income tax return using ITR-1 or ITR-4 forms, as applicable.

In a statement, the Finance Ministry said that the decision has been on consideration of difficulties reported by the taxpayers and other stakeholders in filing of Income Tax Returns and various reports of audit for the Assessment Year 2021-22 under the Income Tax Act, 1961.

The income tax return (ITR) filing deadline for FY 2020-21 for individuals has already been extended, from the normal deadline of July 31, 2021. However, the new income tax e-filing portal has been marred by glitches and other problems from inception. Finance minister Nirmala Sitharaman has given Infosys, the company which set up the new income tax portal, time till September 15, 2021 to fix all the problems.

Last year too, the government has extended the due date of filing ITR for individuals four times – first from July 31 to November 30, 2020, then to December 31, 2020, and finally to January 10, 2021.

“On consideration of difficulties reported by the taxpayers in filing of Income Tax Returns(ITRs) & Audit reports for AY 2021-22 under the ITAct, 1961, CBDT further extends the due dates for filing of ITRs & Audit reports for AY 21-22. Circular No.17/2021 dated 09.09.2021 issued,” I-T Department tweeted on Thursday.

The due date of furnishing of report of audit under any provision of the Act for the previous year 2020-21, has been extended to January 15, 2022.

The due date of furnishing report from an accountant by persons entering into international transaction or specified domestic transaction under section 92E of the Act for the previous year 2020-21, is now January 31, 2022.

Again, the IT Department has decided to extend the due date of furnishing of Return of Income for the AY 2021-22, to February 15, 2022, among several other extensions.

The due date of furnishing of Return of Income for the Assessment Year 2021-22, which was December 31, 2021 has also been extended to February 28, 2022.

The due date of furnishing of belated or revised return of Income for the AY 2021-22 has been further extended to March 31, 2022.

Missing the ITR filing deadline would have had penal consequences. A late filing fee of Rs 5,000 would be levied if the ITR is filed by an individual after the expiry of the deadline.

Do keep in mind that government has also extended the deadline of filing belated ITR by one month from new deadline of December 31, 2021, to January 31, 2022. If the ITR is not filed by January 31, 2022, then the individual will not be able to file ITR for FY 2020-21, unless a notice is issued by the income tax department.

A late filing fee of Rs 5,000 along with penal interest at the rate of 1 per cent per month will be levied on the non-payment of tax dues in this case.

In the reporting week, the increase in the forex kitty was due to a rise in foreign currency assets (FCAs), a major component of the overall reserves, as per weekly data by the Reserve Bank of India (RBI).

The country’s foreign exchange reserves increased by $889 million to a lifetime high of $621.464 billion in the week ended August 6, 2021, RBI data showed on Friday.

In the previous week ended July 30, 2021, the reserves had surged by $9.427 billion to reach $620.576 billion.

In the reporting week, the increase in the forex kitty was due to a rise in foreign currency assets (FCAs), a major component of the overall reserves, as per weekly data by the Reserve Bank of India (RBI).

FCAs rose by $1.508 billion to $577.732 billion in the reporting week.

Gold reserves were down by $588 million to $37.057 billion in the reporting week, the data showed.

The special drawing rights (SDRs) with the International Monetary Fund (IMF) dipped by $1 million to $1.551 billion.

The country’s reserve position with the IMF also fell by $31 million to $5.125 billion, as per the data.

This provides an opportunity to the ICAI members to expand their professional horizons and to foster working relations between the two accounting institutes. The Institute of Chartered Accountants of India (ICAI) and Chartered Accountants Australia and New Zealand (CA ANZ) will have an opportunity to play the leadership role in addressing new challenges facing the profession in a globalized environment.

The Cabinet, chaired by Prime Minister Shri Narendra Modi, has approved a fresh Memorandum of Understanding (MoU) between the Institute of Chartered Accountants of India (ICAI) and Chartered Accountants Australia and New Zealand (CA ANZ).

Impact:

The MOU intends to develop mutually beneficial relationship in the best interest of members, students and their organizations and is expected to provide an opportunity to the ICAI members to expand their professional horizons and to foster working relations between the two accounting institutes. The two accountancy institutes will have an opportunity to play the leadership role in addressing new challenges facing the profession in a globalized environment.

Benefits:

The engagement between the two Institutes is expected to result in greater employment opportunities for Indian Chartered Accountants and also greater remittances back to India.

Details:

The Memorandum of Understanding (MoU) between the Institute of Chartered Accountants of India (ICAI) & Chartered Accountants Australia and New Zealand (CA ANZ) would mutually recognize the qualification and admit the Members in good standing by prescribing a bridging mechanism between the two Institutes. The ICAI and CA ANZ aim to establish a mutual co-operation framework for the advancement of accounting knowledge, professional and intellectual development, advancement of the interests of their respective members and contribute positively to the development of the accounting profession in Australia, New Zealand and India.

Implementation strategy and Targets:

The MoU provides for mutual recognition of qualification of members of other body, who have achieved membership by completing the Examination, professional program and practical experience membership requirements of the two parties.

Background:

The Institute of Chartered Accountants of India (ICAI) is a statutory body established by an Act of Parliament of India, The Chartered Accountants Act, 1949′, to regulate the profession of Chartered Accountancy in India. Chartered Accountants Australia and New Zealand (CA ANZ), emerged from the merger of the Institute of Chartered Accountants in Australia and the New Zealand Institute of Chartered Accountants in October 2014.

The Double Tax Avoidance Agreement (DTAA) is essentially a bilateral agreement entered into between two countries. The basic objective is to promote and foster economic trade and investment between two Countries by avoiding double taxation.

WHAT IS DOUBLE TAXATION OF INCOME?

When the same income is taxed more than once, due to levying of tax by two or more jurisdictions, on the same income asset or financial transaction, this results in double taxation. This may happen, when an assessee – an Individual or a company, is taxed more than once for the same income in India, either on the basis of place of residence or on the basis of source of accrual, which leads to double taxation.

Countries have started entering into Double Taxation Avoidance Agreements (DTAA) with other countries to resolve double taxation issue so as to ease out the tax burden of their taxpayers. This relief for taxes paid in foreign country is given to taxpayer while taxing the same income in India, which is termed as Foreign Tax Credit (FTC).

B. HOW DOUBLE TAXATION AVOIDANCE AGREEMENT (DTAA) WORKS?

In any country, the tax is levied based on 1) Source Rule and 2) the Residence Rule.

The source rule holds that income is to be taxed in the country in which it originates irrespective of whether the income accrues to a resident or a non-resident whereas the residence rule stipulates that the power to tax should rest with the country in which the taxpayer resides.

If both rules apply simultaneously to a business entity and it were to suffer tax at both ends, the cost of operating on an international business would become prohibitive and would deter the process of globalization. It is from this point of view that Double Taxation Avoidance Agreements (DTAA) have become significant.

Where the Central Government has entered into an agreement with the Government of any country outside India or specified territory outside India, for granting relief of tax, or as the case may be, avoidance of double taxation, then, in relation to the assessee to whom such agreement applies, the provisions of this Act shall apply to the extent they are more beneficial to that assessee.

Impact of Double Taxation Avoidance Agreement:

1. WHERE DTAA EXISTS (SECTION 90):

There are two methods of granting relief under Double Taxation Avoidance Agreement.

Exemption method – A particular income is taxed in one of the both countries and exempted in the other

Example- For the Income from Dividend, Interest, royalty and fees for technical services Source Rule is applicable in treaty with Greece, Libyan and United Arab Republic. So for citizen of these 3 countries if the dividend, interest, royalty or fees for technical services is arising in India, then it will be solely taxable in India only and for a resident if such income is arising in any of these 3 countries then the income will solely be taxed in these 3 countries and it will not at all be taxable in India.

Tax Credit method- The income is taxed in both the countries as per the treaty and the country of residence will allow the tax credit / reduction for the tax charged in the country of Origin.

Example- Mr. A (an Indian resident) has received salary from a US company for job in US. Since Mr. A is a resident so his global Income will be taxable in India. In this case, source country is US (since the service has been rendered in US) and resident country is India. So at the time of computation of tax liability of Mr. A, the tax paid in US will be allowed as set off against his total tax liability but limited to the tax payable on such foreign income at Indian tax rates.

Therefore DTAA determines which method to be used first and, if the income is taxable only in one country then exemption method shall be used, but if the same is taxable in both countries then tax credit method comes into play.

In case where Bilateral agreement has been entered under section 90 of the Income Tax Act, 1961 with a foreign country then the assessee has an option either to be taxed as per the Double Taxation Avoidance Agreement (hereinafter referred as “DTAA”) or as per the normal provisions of Income Tax Act 1961, whichever is more beneficial to assessee.

Example- As per DTAA between India and Germany, tax on Interest is specified @ 10% whereas under Income Tax Act 1961, it depends on slab rates for individuals & HUF and flat rates (generally 30%) for other kind of assessees (like firm, company etc). Hence, one can follow DTAA and pay tax @ 10% only.

2. WHERE DTAA DOES NOT EXIST (SECTION 91):

i. If any person who is resident in India in any previous year, in respect of income which arose outside India (and which is not deemed to accrue or arise in India), and paid in any country with which there is no agreement under section 90 for the relief or avoidance of double taxation, then he shall be entitled to the deduction from the tax payable in India,

ii. Deduction shall be lower of:

Tax calculated on such double taxed income at the Indian rates.

Tax calculated on such double taxed income at the rate of tax of the said country

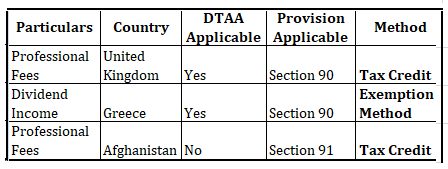

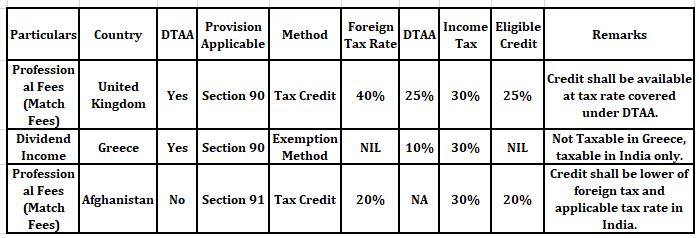

Example :Suppose Indian Sportsman, resident of India who earns foreign income in form of match fees being professional and dividend income as his other foreign income from the below mentioned countries, then in such case following provisions and method shall govern his taxability:

Therefore, both Tax Credit method u/s 90 and Section 91 deals with Foreign Tax Credit, but still having DTAA is beneficial because assessee is taxed at rate beneficial to him, which is not so in case of NO DTAA.

C. HOW CREDIT OF FOREIGN TAX IS AVAILED IN INDIA?

Rule 128 governs the credit of taxes paid on income earned in foreign country. An assessee shall be eligible to claim credit of foreign tax paid if he complies with provisions stated under Rule 128 of the Income Tax Rules which are discussed as follows:

1. Analysis of Rule 128 introduced under Indian Income Tax Rules

Applicability of the rules

The rules came into force with effect from 1.4.2017 applicable only for resident assessee for the amount of foreign taxes paid by him in a foreign country. The credit is available only if income corresponding to the taxes is offered for tax or assessed to tax in India during the year in which the credit is claimed.

In the cases where the income for which the foreign taxes paid or deducted is offered to taxes for more than one year, the credit will be given across the years in the same proportion to which the income is offered to tax in India during the year in which credit is claimed.

2. Foreign Tax Credit Defined under sub-rule 2:

i. FTC in case of DTAA countries: Taxes that are covered under the said agreement.

ii. FTC in case of other countries (No DTAA): Tax payable under the law in force in that country in the nature of income-tax referred in Section 91.

The LOWER OF tax payable under the act on such income or the foreign tax paid is eligible as FTC. However, while considering the foreign tax paid, it cannot exceed the amount arrived as per DTAA with that country.

3. Utilization of Foreign Tax Credit:

FTC is eligible for adjustment against the tax, surcharge and cess payable under the IT Act. FTC cannot be adjusted against interest, fee or penalty payable under the IT Act. FTC is not available in case foreign tax or part thereof is disputed by the assessee in any manner.

4. Exception & Conditions relating to Foreign Tax Credits:

Credit is allowed in the year in which the income is offered/assessed in India upon the assessee within six months from the end of the month in which dispute is finally settled and assessee furnishes:

Evidence of settlement of dispute

Evidence that the liability for payment of such foreign tax has been discharged and

Undertaking that no refund in respect of such amount is directly or indirectly been claimed. Further, credit for each source of income shall be calculated separately for a specific country and then aggregated. The rate of exchange to be taken for this purpose is TT buying rate on the last day of the month immediately preceding month in which the tax is paid or deducted.

5. Documents required under Foreign Tax Credit:

Furnish FORM 67 duly verified and certified by a Chartered Accountant on or before furnishing return of income u/s 139(1)

Furnishing following certificates or statement specifying:

Nature of income and,

Amount of Tax paid of which statement given by:

Tax authority of that country, or

Person responsible for deduction of such tax, or

Signed by the assessee:

In this case, it should be accompanied with – an acknowledgment of online payment or receipt or bank counterfoil for proof of payment of tax, if tax is paid by the assessee

In case of tax deduction, proof of such Tax deducted at source

D. JUDICIAL PRECEDENTS UNDER FOREIGN TAX CREDIT

1. WIPRO LIMITED F TS – 565 – HC – 2015 (KAR)

The judgment of WIPRO provides that merely because the taxpayer’s income is exempt from tax due to a limited tax holiday provided under the ITA, does not mean that foreign tax credit can be simply denied.

2. TATA SONS [2011] 43 SOT 27 (MUM AT)

Though DTAA with USA provides credit only the tax paid with the Federal Government, credit was extended to the Taxes paid to State taxes as well. It has considered the relief u/s 91 which was beneficial to the assessee than that of the DTAA.

3. VIJAY ELECTRICALS [2015] 54 COM 19 (HYD AT)

Tax credit is available even if the same is not deposited with the overseas Government in the year in which the income is taxable.

Amid a severe hit to the Indian economy by the Covid pandemic in the past eight months, the country’s foreign exchange reserves increased by more than $100 billion since the Covid-induced lockdown was enforced in March-end.

From $469.9 billion in the week ended March 20, 2020, the forex reserves jumped by $102.8 billion to a lifetime high of $572.7 billion in the week ended November 13, 2020, according to the data released by the Reserve Bank of India.

Importantly, the reserves grew by $4.277 billion from the week ended November 6, 2020. The jump was on account of Foreign Currency Assets (FCA), a major component of the country’s reserves, that increased by $5.526 billion to $530.2 billion from $524.7 billion in the preceding week.

However, the gold reserves reduced by $1.233 billion from $37.587 billion to $36.354 billion in the week. On the other hand, the special drawing rights with the International Monetary Fund (IMF) were unchanged from the preceding week at $1.488 billion, the data showed.

Foreign portfolio investors (FPI) have invested Rs 49,553 crore in Indian markets in November so far on the back of high liquidity along with improving global indicators and clarity after the US presidential elections, PTI reported.

The investment stood at Rs 44,378 crore in equities and Rs 5,175 crore in the debt segment between November 3-20 while FPI’s October investment was Rs 22,033 crore.

On the other hand, India saw its highest ever Foreign Direct Investment (FDI) during the first five months April-August of the current financial year. The total inflow was $35.73 billion, according to the Ministry of Commerce and Industry that was also 13 per cent up from the year-ago period.

Meanwhile, bank credit grew 5.67 per cent to Rs 104.04 lakh crore in the fortnight ended November 6, 2020, according to the RBI data.

The bank credit stood at Rs 98.46 lakh crore in the fortnight ended November 8, 2019. Moreover, deposits had jumped 10.63 per cent to Rs 143.80 lakh crore from Rs 129.98 lakh crore during the said period.

For improving the ease of doing business in India and to reduce the cost of compliance, RBI has made a review of requirements of submission of various forms and reports under FEMA and has decided to discontinue submission of 17 such returns/ reports with immediate effect.

Discontinuation of Returns/ Reports under Foreign Exchange Management Act, 1999

1. The attention of Authorised Persons is invited to the Master Direction- Reporting under Foreign Exchange Management Act, 1999 dated January 01, 2016, as amended from time to time, and other reporting related instructions issued by the Reserve Bank of India.

2. With a view to improve the ease of doing business and reduce the cost of compliance, the existing forms and reports prescribed under FEMA, 1999, were reviewed by the Reserve Bank. Accordingly, it has been decided to discontinue the 17 returns/ reports as listed in the Annexure with immediate effect.

3. The Master Direction- Reporting under Foreign Exchange Management Act, 1999 dated January 01, 2016, shall accordingly be updated to reflect the above changes. AD banks may bring the contents of this circular to the notice of their constituents.

4. The directions contained in this circular have been issued under Section 10(4) and 11(2) of the Foreign Exchange Management Act, 1999 (42 of 1999) and are without prejudice to permissions/ approvals, if any, required under any other law.

List of Discontinued Reports

Sl. No.

Name of Report

Reporting Entity

Frequency

1

Category-wise transaction where the amount exceeds USD 5000 per transaction

AD Category-II

Monthly

2

Category-wise, transaction-wise statement where the amount exceeds USD 25,000 per transaction

AD Category- II

Monthly

3

Statement of Purchase transactions of USD 10,000 and above (including transactions of their franchisees)

FFMCs and AD Category- II

Monthly

4

Extension of Liaison Offices (LOs)

AD Category-I banks

As and when extension is granted

5

Extension of Project Offices (POs)

AD Category-I banks

As and when extension is granted

6

FII/FPI daily: Daily inflow/outflow of foreign fund on account of investment by FPIs

AD banks

Daily

7

FII/FPI Return (Monthly): Data relating to actual inflow/ outflow of remittances on account of investments by Foreign Institutional Investors (FIIs) in the Indian Capital market

AD Category-I banks

Monthly

8

FVCI reporting: Inflows/outflows of remittances on account of investments by Foreign Venture Capital Investor (FVCIs) and Market value of Investments made by FVCIs

AD Category-I banks/Custodian banks

Monthly

9

Reporting of Inflow/ Outflow details in respect of Mutual Fund by Asset Management Companies

Asset Management Companies

Quarterly

10

Market value of FII Investment in India on fortnightly basis

AD Category-I banks

Fortnightly

11

Market value of FII Investment in India on Monthly basis

AD Category-I banks

Monthly

12

FII holdings as percentage of floating stock

AD Category-I banks

Monthly

13

Form DRR for Issue/ transfer of sponsored/ unsponsored Depository Receipts (DRs)-Hardcopy**

Custodian

At the time of issue/transfer of depository receipts

14

ADR/ GDR Movement Report- two way fungibility

AD Category-I banks

Monthly

15

Repatriation of Sales proceeds of underlying shares represented by FCCBs/ GDRs/ ADRs

Custodian

Monthly

16

GDR/ ADR underlying shares issued, re deposited and released monthly reporting

Custodian

Monthly

17

Monitoring of disinvestments by Overseas Corporate Bodies

AD banks

Monthly

** Please note that it is only the hardcopy filing of form DRR that has been discontinued. The domestic custodian may continue to report the form DRR on FIRMS application in terms of Regulation 4(5) of FEM (Mode of Payment and Reporting of Non-Debt Instruments) Regulations, 2019.