Prime Minister Narendra Modi, today met with Japan Prime Minister Shinzo Abe and signed the Civil Nuclear Deal between India and Japan. PM Narendra Modi, after signing the deal said, “Our strategic partnership is not only for the good & security of our own societies. It also brings peace, stability & balance to region.” PM Modi added, “I wish to thank Prime Minister Abe for the support extended for India’s membership of the Nuclear Suppliers Group.”

This move comes after six years of negotiation. After the Fukushima Nuclear Power Plant disaster, the nuclear deal negotiations were halted due to political resistance in Japan.

After many years, the deal was signed today on November 11. This nuclear treaty will bring Japan’s export nuclear technology to our country, and it will be a necessary step towards India’s nuclear deals with the US, France and other countries.

Soon after hitting the demonetization masterstroke in India, Prime Minister Narendra Modi left for his second visit to Japan in order to seal the civilian nuclear deal between the two countries. This is Modi’s fourth visit to Japan over the last decade (twice as PM and twice as Gujrat Chief Minister).

Soon after landing in Japan, Modi tweeted, “Reached Japan. Looking forward to fruitful deliberations that will boost economic and cultural ties between India and Japan.”

Statement from the Press:

Commenting on the issue, a top Japanese government official said, “Terrorism, which has been an outlier subject in Japan’s national discourse, was brought closer home in July, when seven of our own — five men and two women, who were associated with the Japan International Cooperation Agency — were killed in a terrorist attack in Dhaka.

Both the countries are expected to sign around 10 different agreements which highlight issues like skill development, culture etc. Nevertheless, the prime focus of this meet was the possible signing of the civilian nuclear deal that was initiated in June 2010 but got stuck after the Fukushima disaster in December 2015.

Commenting on the possible signing of the deal, Kumao Kaneko, a former Japanese diplomat and negotiator on nuclear issues, said that the NTP has been a treaty of “convenience and expediency”. Though India adheres to NPT principles, but has not inked the treaty yet. By signing the agreement, Japan is doing the correct thing, however, the Abe government will have to work hard in the Diet (Japan’s parliament) to get the naysayers on board.

India and the UK are expected to sign business deals exceeding GBP 1 billion (Rs 83,00 crore) during the three-day visit of British Prime Minister Theresa May, who is here on her first bilateral visit outside Europe since assuming office in July.

Describing her talks with Prime Minister Narendra Modi as good and productive, May said as leaders, they both were working to improve the livelihoods of their citizens creating jobs, developing skills, investing in infrastructure and supporting technologies of the future.Talking about Modi’s vision of smart cities, May said they have agreed on a new partnership that will bring together government, investors and experts to work together on urban development, unlocking opportunities worth GBP 2 billion for British businesses over the next five years.

This will focus on the dynamic state of Madhya Pradesh with plans for more smart cities than anywhere else and the historic city of Varanasi.

Four rupee-denominated bonds worth a total of 600 million pounds ($748 million) are expected to be listed in London in the next three months, Theresa May said.

The latest four bonds will provide financing to expand India’s highway and rail networks and meet its plans to boost energy efficiency and renewable energy, the government said.

They will be issued by Indian government-backed corporates Indian Railway Finance Corporation, Indian Renewable Energy Development Agency, Energy Efficiency Services Limited, and National Highways Authority of India by the end of January 2017. May said since July, more than 900 million pounds rupee-denominated bonds have been issued in London, equivalent of more than 70 percent of the global offshore market.

“This government will continue to work closely with both India and our financial services sector to ensure our growing rupee bond market continues to help finance India’s ambitious infrastructure investment plans,” May said in a statement. These rupee-denominated or masala bonds as they are called, unveiled in 2015, are an opportunity for Indian firms to raise money, while giving international investors access to higher yields in a zero-yield world.

They are also a way to borrow overseas, they are also an attempt to make the tightly-controlled rupee more widely available in global markets, similar to the way in which China has moved to sell more yuan debt to overseas investors. Alongside this, the UK has agreed to invest GBP 120 million in a joint fund that will leverage private sector investment from the City of London to finance Indian infrastructure.

DIPP notifies 100% FDI in more financial services The commerce and industry ministry notified 100 percent foreign direct investment in ‘other financial services’ carried out by NBFCs.

The move will help attract foreign capital into the country. “The government has liberalised its FDI policy in Other Financial Services and non-banking finance companies (NBFCs), the DIPP said in a press note.

Other financial services will include activities which are regulated by any financial sector regulator – RBI, SEBI, IRDA, Pension Fund Regulatory and Development Authority, National Housing Bank “or any other financial sector regulator as may be notified by the government in this regard,” it said.

Such foreign investment would be subject to conditionalities, including minimum capitalisation norms, as specified by the concerned regulator or government agency, it said.

The press note, however, did not specify the sectors which have been opened up for automatic route. The present regulations on NBFCs stipulate that FDI would be allowed on automatic route for only 18 specified NBFC activities after fulfilling prescribed minimum capitalisation norms mentioned therein.

In the Budget 2016-17 Speech, Finance Minister Arun Jaitley had announced about this liberalisation.

Currently, 100 percent FDI through automatic route is permitted in 18 NBFC activities including merchant banking, under writing, portfolio management services, financial consultancy and stock broking. In 2015-16, foreign direct investment in India grew by 29 percent year-on-year to USD 40 billion.

A man is silhouetted against the logo of the World Bank at the main venue for the International Monetary Fund (IMF) and World Bank annual meeting in Tokyo October 10, 2012. REUTERS/Kim Kyung-Hoon

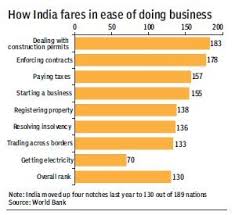

As the World Bank looks set to release its annual ranking of countries in the ease of doing business later this week, India expects to improve its position from last year’s 130 out of 189 economies. The optimism stems from the fact that, for a second straight year, the country expects its ranking in “getting electricity’’ to improve substantially on the back of some “remarkable work” done by states, a senior government official told FE.

Last year, India was placed at 70 of the 189 countries in “getting electricity”, compared with 99 in the previous year. This had helped the country improve its ranking in the overall ease of doing business by 4 notches.

The government also believes that its “targeted intervention” to improve performance in difficult parameters — including dealing with construction permits and enforcing contracts — where the country has been faring badly for years now will start to pay, the official said.

So while it will take some time to correct the course in certain legacy issues, especially in enforcing contracts, the DIPP believes the much-improved performance of states will be reflected in the country’s ranking for the years to come.

For instance, while only two states (Gujarat and Andhra Pradesh) had scored over 70% in a 98-point action plan for the ease of doing business — jointly decided by them and the Centre — last year, as many as 16 states have scored over 70% so far this year, that too on a 340-point action plan, showed the latest data by the Department of Industrial Policy and Promotion (DIPP). Importantly, 10 states have scored over 90% so far this year (Andhra Pradesh and Telangana top the charts in 2016, each scoring over 99%).

The latest ranking of the World Bank takes into account reforms done up to the end of May, except in case of taxation.

The performance in access to electricity has been impressive, the official said. For instance, in Mumbai, the time required for getting a new electricity connection has been reduced to an average of around 15 days from 67 days earlier. The number of procedures involved has been cut down to just 3 from 7. Similarly, in Delhi, people can get connections in just 15 days now from as many as 140 days a few years earlier. The number of document required has been reduced to just 2 from 7 earlier. Access to electricity is crucial as it also has bearing on performance in some other aspects of the ease of doing business.

In “dealing with construction permits”, where the country was ranked at 183 of the 189 countries, the performance has improved. For instance, in Delhi and Mumbai, common online application form has been adopted for seeking construction permits. People don’t have to get no-objection certificates from anyone, as municipal corporations will get these certificates for them online. Earlier, some 18 no-objection certificates from different departments were required to be obtained by individuals for getting construction permits.

Also, in a metro like Delhi which has traditionally fared badly in handling construction permits, the documents required for this purpose has now been cut to just 14 from 39 earlier. Nine departments involved in the process of the sanction of buildings have been integrated online. The drawing of the construction plan is “auto-checked” by a software and no site inspection is necessary. Reforms on this parameter have been even quicker in other parts of the country.

On enforcing contracts in which India was placed at 178, the government has decided to set up commercial courts in a big way after the Commercial Courts, Commercial Division and Commercial Appellate Division of High Courts Bill was signed into a law on January 1.

Although the exact data on the formation of such courts are yet to be compiled precisely, roughly a dozen such courts are learnt to have been set up, especially in Delhi, Mumbai, Gujarat and Himachal Pradesh, to settle high-value business disputes.

All pending suits and applications on commercial disputes involving a claim of Rs 1 crore or more in high courts and civil courts will be transferred to the relevant commercial division or courts. The decision to set up such courts is in sync with the Narendra Modi government’s aim of making India a global arbitration hub. The government plans to introduce e-summon system and efforts are on to expedite the process of getting a verdict, said the official.

To boost cross-border trade, the number of documents required for trade has been restricted to just 2-3 from as many as a dozen in certain cases earlier. Importantly, the finance ministry is learnt to have sanctioned Rs 2,500 crore for the upgrade of the IT and some other systems of the Customs departments.

Foreign venture capital entities can now invest in unlisted Indian companies without Reserve Bank of India approval.

The venture capital firm will, however, have to be registered with market regulator SEBI. The investment can be made in an Indian company in 10 specific sectors or in any start-up.

The central bank on Thursday amended the regulations governing foreign venture capital investors (FVCI) in order to further liberalise and rationalise the investment regime and to give a fillip to foreign investment in start-ups.

According to the RBI, the 10 sectors in which SEBI-registered FVCIs can invest without its nod are: biotechnology, IT, nanotechnology, seed research and development, discovery of new chemical entities in pharmaceutical sector, dairy industry, poultry industry, production of bio-fuels, hotel-cum-convention centres with over 3,000 seating capacity, and infrastructure sector. FVCIs can also invest in equity, equity-linked instruments or debt instruments issued by an Indian ‘start-up’ irrespective of the sector in which it is engaged. The RBI said a start-up will mean an entity (private limited company, registered partnership firm or a limited liability partnership) incorporated or registered in India not prior to five years, with an annual turnover not exceeding Rs. 25 crore in any preceding financial year.

These start-ups should be working towards innovation, development, deployment or commercialisation of new products, processes or services driven by technology or intellectual property and satisfying certain conditions as given in the Foreign Exchange Management Regulations, 2016.

The RBI also said FVCIs can invest in units of a venture capital fund (VCF) or a Category-I alternative investment fund (AIF) or units of a scheme/fund set up by a VCF or by a Category-I AIF.

In a circular issued to banks authorised to deal in foreign exchange, the RBI said: “In order to further liberalise and rationalise the investment regime for FVCIs and to give a fillip to foreign investment in the start-ups, the extant regulatory provisions have been reviewed, in consultation with the Government of India.”

The consideration for all investments by an FVCI can be paid out of inward remittance from abroad through normal banking channels or out of sale/maturity proceeds of or income generated from investment already made. There will be no restriction on transfer of any security/instrument held by the FVCI to any person resident in or outside India.

Foreign investors pumped in more than Rs. 20,000 crore into the capital market in September, making it the highest net inflow in 11 months.

This also marks the third consecutive month of positive inflows (equity and debt).

The trend is likely to continue in the coming weeks as regulator SEBI has decided to offer well-regulated foreign investors direct entry to invest in corporate bonds, say experts.

They attributed the latest flurry of capital to factors such as sound progress in roll-out of GST, better corporate earnings and the US Fed’s decision not to lift interest rates.

Sentiment turned better after the current account deficit (CAD) narrowed sharply to just $300 million, or 0.1 per cent of GDP, in the June quarter and domestic passenger vehicle sales grew for the 14th straight month in August, they added.

According to depositors’ data, net investment by FPIs stood at Rs. 10,443 crore in equities last month while the same for debt was Rs. 9,789 crore, taking the total inflow to Rs. 20,233 crore ($3 billion).

This was the highest net inflow in the capital markets since October 2015 when FPIs had infused Rs. 22,350 crore.

The latest inflow has taken the FPI investment tally in equities to Rs. 51,293 crore in 2016 while the same for the debt market stands at Rs. 2,441 crore, resulting in a net inflow of Rs. 53,734 crore.

The country’s forex reserves continued to scale new highs, with the week to September 9 adding $3.513 billion to the kitty, which hit a new life-time peak of $371.279 billion, RBI data showed today.

The reserves had increased by $989.5 million to $367.76 billion in the previous reporting week.

The reserves are more than sufficient to cover nearly 13 months of exports.

The surge indicates that new RBI Governor Urjit Patel is continuing with his predecessor Raghuram Rajan’s policy of building up the forex reserves. The three-year tenure of Rajan saw the RBI adding a net of $92 billion to the kitty.

Foreign currency assets (FCAs), a major component of the overall reserves, swelled by $3.509 billion to $345.747 billion for the week ended September 9, the Reserve Bank said.

FCAs, expressed in dollar terms, include the effect of appreciation/depreciation of non-US currencies such as the euro, pound and the yen held in the reserves.

Gold reserves, however, were unchanged at $21.64 billion at the end of the reporting week, the apex bank said.

The country’s special drawing rights with the International Monetary Fund increased by $5.3 million to $1.493 billion, while the reserve position with the fund was down by $1.3 million to $2.395 billion, it added.