Flipkart received India’s largest ever PE investment of $2.5 billion in a single round from Softbank

Private equity firms invested $23.8 billion across 591 deals in 2017, making it the biggest year for PE investments in India, says a report.

According to deal tracker Venture Intelligence, the investment value is 39 per cent higher than the previous high of $17.1 billion (recorded in 2015) and 55 per cent higher than $15.4 billion invested during 2016. In terms of number of deals the year 2017 saw 21 per cent less activity as compared to 2016 (731 deals), indicating large number of big-ticket transactions.

“The year witnessed 31 investment deals with size greater than USD 200 million, aggregating to $15.4 billion or 65 per cent of the total investments,” the report said. These figures include venture capital investments, but exclude PE investments in real estate.

In terms of industries, IT/ ITeS companies accounted for 45 per cent of the value pie attracting $10.7 billion worth investments across 325 transactions.

Flipkart received India’s largest ever PE investment of $2.5 billion in a single round from Softbank and another $1.4 billion from strategic investors Tencent, eBay and Microsoft. Softbank also invested $1.4 billion in mobile wallet and payments firm One97 Communications, which owns the Paytm brand. BFSI (Banking, Financial Services and Insurance) companies continued to enjoy the second spot attracting $4.40 billion across 61 transactions.

The sector was led by Bain Capital’s $1.04 billion investment in Axis Bank — the largest ever single investment in the sector — and Warburg Pincus’ $384 million pre-IPO investment in ICICI Lombard General Insurance.

On the back of its two mega bets (Flipkart and Paytm), Softbank emerged as the largest investor during the year with investments totaling over $4 billion (including a $250 million investment in Oyo Rooms).

Other top investors include Canadian pension fund CPPIB with $2 billion investments across five companies; while Warburg Pincus invested $1.6 billion across nine companies, and KKR invested about $680 million.

China’s Tencent emerged as a significant strategic investor in the Indian Internet and mobile sector with investment of $1.1 billion across home grown leaders like Flipkart, Ola, Byjus Classes and Practo.

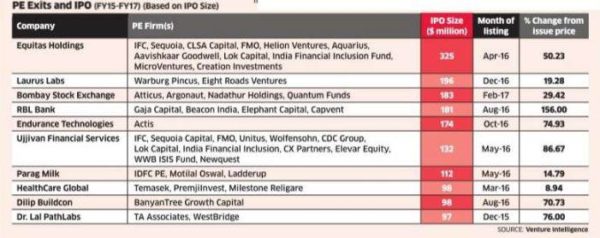

Private equity investors make big money in IPO exits. This is well known. But what is less known is that retail and other investors have also been making decent money after the exits. The largest IPO exits in the last three years made 1-14 times returns for private equity firms. But after listing, retail, HNIs and institutional investors have gained 9-156% in these firms, thanks to a strong stock market, data from Venture Intelligence show.

If the market rises further, the gains will only increase and private equity-like, super sized returns may still be possible. Investment bankers attribute this to the rising interest in equity market as well as strong fundamentals. “Stocks being valued attractively and appetite for IPOs have helped these companies,“ said Dharmesh Mehta, MD, Axis Capital. Financial stocks have obviously beaten the rest with RBL Bank surging 156% since listing in August 2016 followed by Ujjivan Financial Services with a gain of 87%.

Other gainers include Dr Lal PathLabs which has jumped 76% and Dilip Buildcon which has moved up 71%. In FY17, PE firms sold their complete stakes in 14 IPOs, as compared to 16 in FY16 and seven in FY15. According to Ajay Saraf, executive director, ICICI Securities, a PE exit augurs well for investors as the company could be expected to have better corporate governance and better fundamentals.

PE firms usually enter into sectors that have potential to do well and this gives comfort to investors while buying these stocks, said Saraf. “The PE exit trend is likely to gain further momentum going ahead,“ added Saraf.

High margins and volumes are two reasons why banks are exploring the market in thrift credit

From being passive lenders to microfinance institutions (MFIs) till about five years earlier, banks have turned out to be active players in the business of small loans.

As on end-December 2016, banks accounted for 37 per cent (Rs 36,683 crore) of microfinance portfolio of Rs 98,625 crore; five years earlier, a handful of MFIs accounted for more than half.

High margins and volumes are two reasons why banks are exploring the market in thrift credit.

Most of them in MFI lending are private sector ones. A majority of this portfolio is with 11 banks — Axis, Bandhan, DCB, Equitas, HDFC, ICICI, IDFC, Kotak Mahindra, RBL and YES.

This apart, several public sector banks have increased their MFI exposure, through business correspondents (BCs).

“We see a lot of synergies with the microfinance sector. More, it is quite well-regulated and growing at a fast rate, providing a lot of business opportunities,” said an official in charge of a bank’s microfinance operations.

Also, over the past 18 months, banks have also been aggressive in taking equity stakes in MFIs. Last year, Kotak Mahindra Bank acquired Bengaluru-based BSS Microfinance.

RBL acquired 10 per cent in Utkarsh Micro Finance, which recently graduated into a small finance bank (SFB).

In July last year, IDFC Bank acquired Trichy-based Grama Vidiyal Microfinance, its second deal in the MFI space. Earlier, IDFC had taken 10 per cent in east-based ASA International India Microfinance.

In March last year, DCB Bank had acquired a 5.81 per cent stake in Odisha-based Annapurna Microfinance. Earlier, RBL had acquired 30 per cent in Swadhaar FinServe, a company acting as a BC.

Non-banking financial companies (NBFCs) have also shown interest. In 2015, Manappuram Finance had acquired Asirvad Micro Finance, a Chennai-based NBFC-MFI.

With a number of MFIs graduating to SFBs, the number in the MFI space is likely to further increase. And, even after graduating into a bank, they are likely to keep much of their lending to microfinance. Bandhan Bank, earlier an MFI, has even after close to two years into operation as a bank still got over 80 per cent of its lending portfolio concentrated in microfinance.

“Over the past three years, banks have shown a high level of interest in microfinance, part of a diversification strategy. Also, at least for two to three years, the new SFBs are likely to focus on microfinance as they build their deposit base,” says Ratna Vishwanathan, chief executive officer, Microfinance Institutions Network.

Seven of the proposed SFBs, some of which have transformed to a bank, together account for 46 per cent of the MFI portfolio, amounting to Rs 26,228 crore.

Official data released on Tuesday showed that demonetisation hasn’t pushed the economy into a retreat as most feared, with its short-term adverse impact. (Source: Reuters)

Official data released on Tuesday showed that demonetisation hasn’t pushed the economy into a retreat as most feared, with its short-term adverse impact to a large extent restricted to construction and financial services. Real GDP growth in the December quarter, in the midst of which the note ban came into effect, came in at a respectable 7% (though lower than 7.4% in the previous quarter) and the gross value added (GVA) was 6.6%, with the difference explained by robust indirect taxes and reining in of subsidies.

Upward revision of GVA estimates for 2015-16 led to downward corrections in GVA for Q1 and Q2 of the current fiscal but despite this, there were marginal upward revisions in the rates of GDP expansion in these quarters, thanks to a surge in indirect taxes.

Solid performance by the “agriculture and allied sectors”, pump-priming by the government on the consumption side, better-than-expected performance by mining and manufacturing sectors and a seasonal — though larger-than-usual — pick-up in private consumption masked whatever negative effect the note swap exercise had on the economy, going by the Central Statistics Office’s data.

However, as the GDP was slowing even before demonetisation and the note swap has indeed had an incremental adverse effect on it, both GDP and GVA growth for 2016-17 have been projected to be much lower than in the previous year. In the second advance estimate, the CSO has kept the GDP growth estimate for the current financial year at 7.1%, the same as in the first advance estimate released in early January, and GVA growth at 6.7%. But given that 2015-16 GDP growth, which was seen at 7.6% at the time of the first advance estimate, was subsequently revised to 7.9%, the CSO’s latest take on 2016-17 growth is virtually more sanguine than its previous estimate.

While the CSO’s GDP estimate for 2016-17 is evidently higher than that of most others, many analysts said the growth assumed by it for the second half (6.8%) was optimistic. “Given the fact that the fall from H1 to Q3 is not much, I don’t think that we should then necessarily assume that the rebound in Q4 is going to be very sharp,” said Aditi Nayar, economist at Icra. Stating that the GDP number is better than expected, Saugata Bhattacharya, chief economist at Axis Bank, said, “Since growth slowdown (due to demonetisation) has been shallower than expected, and in line with the RBI’s projections, the probability of rate cuts going ahead has come down.”

The minutes of the monetary policy committee’s meeting released last week indicated that it changed its stance from “accommodative” to “neutral” because the growth drag from demonetisation is expected to fade soon. India Ratings reiterated its view that “much of the impact of demonetisation will be visible in Q4FY17 leading to an overall GDP growth of 6.8% in 2016-17”.

Economic affairs secretary Shaktikanta Das said: “This year’s GDP (growth) is around 7%, based on available numbers. Nothing can be deciphered on anecdotal evidence. Demonetisation only impacted consumption in some cities, since most purchases happened on credit or debit cards. The so-called negative impact, if relevant, was only temporary.”

The 7% GDP growth forecast for the third quarter helped India maintain the coveted tag of the world’s fastest-growing major economy despite demonetisation, better than China’s 6.8% in the December quarter.

While analysts pointed out the lack of congruity between the CSO’s estimate and other high-frequency data and corporate results, chief statistician TCA Anant said all available data have been made use of in the second advance estimate, including corporate performance up to the December quarter, sales of commercial vehicles, railway freight, etc, for the first “9/10 months of the financial year”.

According to the CSO, with production growth of foodgrains during 2016-17 kharif and rabi seasons being 9.9% and 6.3%, respectively, the farm sector grew a robust 6% in Q3 from 3.8% in the previous quarter and compared with a 2.2% contraction in the year-ago quarter. Despite the anecdotes of industrial clusters hit by the note ban during the period, manufacturing grew a healthy 8.3% in Q3 on a robust base of 12.8% in the year-ago quarter and compared with 6.9% in Q2 this fiscal. Mining also posted a smart recovery from a fall of 1.3% in Q2 to a robust expansion of 7.5% in Q3. The bad performers on the output side was “financial services, etc”, which posted a modest 3.1% growth in Q3 compared with 7.6% in the previous month, and construction which grew just 2.7% in the December quarter.

Government final consumption expenditure (GFCE) posted a 19.9% growth in Q3 against 15.2% in the previous quarter, the CSO said. Given that 17% growth in GFCE is estimated for the whole of 2016-17, it needs to grow at 17.4% in Q4. Considering that the Centre, as is seen from the April-January fiscal data separately released by the Controller General of Accounts, has slowed down spending in the later months of the year, the spending boost must come from PSUs.

Although both Dussehra and Diwali fell in the December quarter, the 10.1% growth reported by CSO in the private consumption expenditure looked puzzling to most analysts (but some said use of old notes for consumption might have contributed to the rise). So was the 3.5% growth in gross fixed capital formation, which was declining for the previous three quarters.

Given that nominal GDP growth has been projected at 11.5% for 2016-17, compared with 10% in the last fiscal, it may offer more leeway to the government to improve spending in the next fiscal and yet contain fiscal deficit, which is expressed as a ratio of the nominal GDP, at the targeted 3.2%.

Discrepancies — the difference between the supply and demand side of GDP — turned negative after a gap of four quarters (-Rs 6,767 crore) in the December quarter, compared with Rs 45,378 crore in the second quarter and Rs 30,645 crore in the first quarter. In the last quarter of 2015-16, discrepancies touched a massive Rs 1,43,210 crore, causing a flutter then and raising doubts about the credibility of the country’s data collection mechanism. When private final consumption expenditure, gross fixed capital formation, government final consumption expenditure, change in stocks, valuables, and net exports exceed the overall GDP (based on the supply side data), discrepancies turn negative.

Analysts expect the exports sector to contribute more to GDP growth in the coming quarters, despite the demonetisation blues, thanks primarily to a favourable base. In real terms, the export growth for 2016-17 has been projected at 2.3%, compared with -5.4% in the last fiscal. Despite demonetisation, merchandise exports rose 2.3% in November, 5.7% in December and 4.3% in January.

The Reserve Bank appealed to income tax assessees to pay dues in advance of the due date as well use alternate channels of authorized banks to avoid the rush during end of March.

“Pay I-T dues in advance at RBI or at authorized bank branches. Appeal to income tax assessees to remit their income tax dues sufficiently in advance of the due date,” RBI said in a release.

“It is observed that the rush for remitting Income-Tax dues through the RBI has been far too heavy towards the end of March every year and it becomes difficult for the RBI to cope with the pressure of issuing receipts although additional counters to the maximum extent possible are provided for the purpose”, it said.

RBI said assessees can use alternate channels like select branches of agency banks or the facility of online payment of taxes offered by these banks.

A total of 29 agency banks have been authorized to accept payments of Income-Tax dues. The authorised banks include SBI and its five associates, HDFC Bank, ICICI Bank, Axis, Bank, Punjab National Bank, Bank of Baroda, Bank of India, Indian Overseas Bank.

Among others are Corporation Bank, Dena Bank, Canara Bank, Central Bank of India, Syndicate Bank and others.

RBI said by remitting dues at the designated banks will obviate the I-T assessess’ inconvenience in standing in long queues at the RBI offices.