As part of Government of India’s Ease of Doing Business (EODB) initiatives, the Ministry of Corporate Affairs would be shortly notifying & deploying a new Web Form christened ‘SPICe+’ (pronounced ‘SPICe Plus’) replacing the existing SPICe form.

SPICe+ would save as many procedures, time and cost for Starting a Business in India and would be applicable for all new company incorporation w.e.f 15th February 2020

Key Features of Spice+

SPICe+ would be an integrated Web Form i.e. fill form online like GST registration forms. The new web form would Facilitate on-screen filing and real time data validation for seamless incorporation of companies.

Information once entered can be saved and modified. All Check form and Pre-scrutiny validations will happen on web form itself.

DSC validation and other validations will happen at Upload Level

Once the SPICe+ is filled completely with all relevant details, the same would then have to be converted into pdf format, with just a click of the mouse button, for affixing DSCs.

Digitally signed applications can then be uploaded along with the linked forms as per the existing process.

Changes/modifications to SPICe+ (even after generating pdf and affixing DSCs), can also be done by editing the same web form

Spice+ would have 2 parts:

a) Part A : for name reservation for new incorporation

b) Part B : Part B offering a bouquet of services i.e.

Incorporation

DIN allotment

Mandatory issue of PAN / TAN

Mandatory issue of EPFO / ESIC registration

Mandatory issue of Profession Tax registration (Maharashtra)

Mandatory Opening of Bank Account for the Company

Allotment of GSTIN (if so applied for)

Part A can be filed first for reserving name or Part A & B can be filed together at one go.

Re submission would be easy, if required.

Registration for EPFO and ESIC shall be mandatory for all new companies incorporated w.e.f 15 February 2020 and no EPFO & ESIC registration nos. shall be separately issued by the respective agencies.

Registration for Profession Tax shall also be mandatory for all new companies incorporated in the State of Maharashtra w.e.f 15th February 2020.

All new companies incorporated through SPICe+ (w.e.f 15th February 2020) would also be mandatorily required to apply for opening the company’s Bank account through the AGILE-PRO linked web form.

Declaration by all Subscribers and first Directors in INC-9 shall be auto-generated in pdf format and would have to be submitted only in Electronic form in all cases, except where:

Total number of subscribers and/or directors is greater than 20 and/or

Any such subscribers and/or directors has neither DIN nor PAN

– The Central government will provide required approvals to such companies for winding up instead of the tribunal – MCA notifies the Companies (Winding Up) Rules, 2020, vide Notification dt. 24 January 2020, comprising of Rules 1 to 191 and Forms WIN 1 to WIN 95, applicable for winding up under the Companies Act 2013 w.e.f. 1 April, 2020

The Ministry of Corporate Affairs (MCA) on Tuesday notified rules for winding up of companies, making it easier for smaller firms to wind up businesses without taking approval.

The rules have provided summary procedures for liquidation of companies with asset size of Rs 1 crore and which have not accepted deposits exceeding Rs 25 lakh and turnover less than Rs 50 crore and total loan under Rs 25 lakh.

The Central government will provide required approvals to such companies for winding up instead of the tribunal.

The rules said, “…wherever the word Tribunal is mentioned, it shall be read as Central Government and with further directions issued by the Central Government as may be necessary, from time to time.”

G.S.R. (E).- In exercise of the powers conferred by sub-sections (1) and (2) of section 468 and sub-sections (1) and (2) of section 469 of the Companies Act, 2013 (18 of 2013), the Central Government hereby makes the following rules, namely:-

Part 1: GENERAL

1. Short title, commencement and application.-

(1) These rules may be called the Companies (Winding Up) Rules, 2020.

(2) They shall come into force on the 1st day of April, 2020.

(3) These rules shall apply to winding up under of Companies Act 2013 (18 of 2013).

2. Definitions.-

In these rules, unless the context or subject matter otherwise requires, –

(a) “Act” means the Companies Act, 2013 (18 of 2013);

(b) “Form” means a Form annexed to these rules;

(c) “Registrar” means the Registrar of the National Company Law Tribunal or National Company Law Appellate Tribunal and includes such other officer of the Tribunal or Bench thereof to whom the powers and functions of the Registrar are assigned;

(d) “Registry” means the Registry of the Tribunal or any of its Benches or of the Appellate Tribunal, as the case may be, which keeps records of the applications and documents relating thereto;

(e) “Section” means section of the Act;

(f) words and expressions used and not defined in these rules but defined in the Act shall have the meanings respectively assigned to them in the Act.

Part II: WINDING UP BY TRIBUNAL

3. Petition for winding up.-

(1) For the purposes of sub-section (1) of section 272, a petition for winding up of a company shall be presented in Form WIN 1 or Form WIN 2, as the case may be, with such variations as the circumstances may require, and shall be presented in triplicate.

(2) Every petition shall be verified by an affidavit made by the petitioner or by the petitioners, where there are more than one petitioners, and in case the petition is presented by a body corporate, by the Director, Secretary or any other authorised person thereof, and such affidavit shall be in Form WIN 3.

4. Statement of affairs.- The statement of affairs, as required to be filed under sub-section (4) of section 272 or sub-section (1) of section 274, shall be in Form WIN 4 and shall contain information up to the date which shall not be more than thirty days prior to the date of filling the petition or filling the objection as applicable and the statement of affairs shall be made in duplicate, duly verified by an affidavit, and affidavit of concurrence of the statement of affairs shall be in Form WIN 5.

5. Admission of petition and directions as to advertisement.- Upon filing of the petition, it shall be posted before the Tribunal for admission of the petition and fixing a date for the hearing thereof and for appropriate directions as to the advertisements to be published and the persons, if any, upon whom copies of the petition are to be served, and where the petition has been filed by a person other than the company, the Tribunal may, if it thinks fit, direct notice to be given to the company and give an opportunity of being heard, before giving directions as to the advertisement of the petition, if any, and the petitioner shall bear all costs of the advertisement.

6. Copy of petition to be furnished.- Every contributory of the company shall be entitled to be furnished by the petitioner or by his authorised representative with a copy of the petition within twenty four hours of his requiring the same on payment of five rupees per page.

7. Advertisement of petition.- Subject to any directions of the Tribunal, notice of the petition shall be advertised not less than fourteen days before the date fixed for hearing in any daily newspaper in English and vernacular language widely circulated in the State or Union territory in which the registered office of the company is situated, and the advertisement shall be in Form WIN 6.

8. Application for leave to withdraw petition.-

(1) A petition for winding up shall not be withdrawn after presentation without the leave of the Tribunal subject to compliance with any order of the Tribunal, including as to costs.

(2) An application for leave to withdraw a petition for winding up which has been advertised in accordance with the provisions of rule 7 shall not be heard at any time before the date fixed in the advertisement for the hearing of the petition.

Large unlisted companies may have to make quarterly or half-yearly filings, like their listed counterparts, as the government is considering amendments to the Companies Act to mandate more frequent disclosures in the aftermath of the IL&FS collapse.

The ministry of corporate affairs (MCA) is expected to prescribe a threshold for the disclosure requirement as it does not want to burden all companies, as a bulk of them are small companies, sources told TOI. The idea is to track the systemically important companies, which pose a risk to the entire system. “It will be an enabling amendment and MCA will decide on timing and extent of disclosures later,” said a source.

The assessment in the government is that there is a massive lag, often up to 18 months related to annual filings by companies, many of which have been non-compliant in the past. An entity like the beleaguered IL&FS was not on the radar till it collapsed and MCA is hoping that periodic disclosures would reduce the chances of such failures going undetected. Currently, companies are required to annually file the consolidated financial statement, balance sheet, profit & loss account, annual returns, directors’ report and certified true copy of board resolution with the designated RoC.

The proposal to increase disclosures is expected to be part of a set of amendments to be taken up by a group of ministers chaired by home minister Amit Shah, with defence minister Rajnath Singh, finance & corporate affairs minister Nirmala Sitharaman, commerce & industry minister Piyush Goyal and law & justice minister Ravi Shankar Prasad among the nine members of the committee, sources told TOI.

The ministerial panel, referred to as alternate mechanism by the Narendra Modi administration, will largely look at the recommendations of the company law panel, which submitted its report. While MCA was pushing for the introduction of the Bill during the recently concluded Winter Session, the legislation will now be placed before the Parliament as soon as it is cleared by ministers. The ministry is hoping to introduce the Bill during the budget session.

On November 18, 2019 the Companies (Meetings of Board and its Powers) Second Amendment Rules, 2019 (“Amendment Rules“) amended certain threshold limits prescribed by the Rules.

The central government notified the Companies (Meetings of Board and its Powers) Second Amendment Rules, 2019 on 18 November 2019. The amendment rules amend sub-clause 3 of rule 15 of the Companies (Meetings of Board and its Powers) Rules, 2014. The amendment rules alter the various transaction thresholds within which the board may authorize a related party transaction without referring the matter to the shareholders pursuant to section 188(1) (Related party transactions) of the Companies Act, 2013.

Rule 15 provides for conditions applicable to the board taking up, discussing and approving a related party contract or arrangement. The first proviso to section 188(1) of the act provides that no contract or arrangement which exceeds certain monetary thresholds, in relation to the company’s paid-up share capital or otherwise, may be entered into without the prior approval of the shareholders by a resolution. The thresholds in relation to this proviso to section 188(1) of the act are prescribed by the rules and have been amended through the amendment rules as follows:

For a contract or arrangement in relation to a sale, purchase or supply of any goods, previously the threshold, was the lower of: (1) 10% or more of the turnover of the company; or (2)₹1 billion. The amendment rules have relaxed the threshold and fixed it at 10% or more of turnover of the company.

Similarly, for a contract or arrangement for selling or otherwise disposing of, or buying property of any kind, previously the threshold for requiring a shareholder resolution was the lower of: (1) 10% or more of the turnover of the company; or (2)₹1 billion. The amendment rules have relaxed the threshold and fixed it at 10% or more of turnover of the company.

The amendment rules has similarly amended the threshold for a contract or arrangement in relation to leasing of property any kind, and in relation to availing or rendering of any services (directly, or through the appointment of an agent). The amendment rules now fix the threshold at 10% or more of turnover of the company.

Accordingly, the ministry has relaxed the thresholds and made it simpler for companies to ensure ease of business, and the ease of entering into related party transactions.

Nature of Related Party Transactions

Earlier Threshold Limit*

Amended Threshold Limit*

Sale, purchase or supply

of any goods or material (directly or through an agent).

Amounting to ten percent (10%) or more of turnover or Rs. 100 Crore, whichever is lower.

Amounting to ten percent (10%) or more of the turnover of the company.

Selling or otherwise

disposing of, or buying, property of any kind (directly or through an agent).

Amounting to ten percent (10%) or more of net worth or Rs. 100 Crore, whichever is lower.

Amounting to ten percent (10%) or more of the turnover of the company.

Leasing of property of

any kind.

Amounting to ten percent (10%) or more of net worth or 10 percent (10%) or more of turnover Rs. 100 Crore, whichever is lower.

Amounting to ten percent (10%) or more of the turnover of the company.

Availing or rendering of any services (directly or through an agent)

Amounting to ten percent(10%)or more of turnover or Rs. 50 Crore, whichever is lower

Amounting to ten percent (10%) or more of the turnover of the company

*limits specified above shall apply for transaction or transactions to be entered into either individually or taken together with the previous transactions during a financial year.

Appointment to any

office or place of profit in the company, subsidiary company or associate company

Remuneration exceeding

Rs. 2,50,000 per month

No Change

Underwriting the

subscription of any securities or derivatives of the company

Remuneration exceeding

one percent (1%) of net worth

Deactivation of DIN for non-compliance of KYC by company Directors has since been marked as ‘Deactivated due to non-filing of DIR-3 KYC’.

The Ministry of Corporate Affairs website (“MCA”), MCA has stated that the DINs which have not complied with the requirement of filing DIR-3 KYC have been marked as ‘Deactivated due to non-filing of DIR-3 KYC’.

The last date for filing DIR-3 KYC for the financial year 2018-19 has expired on 14th October 2019.

The process of deactivating the non-compliant DINs was in progress and has since been completed by MCA. The form DIR-3 KYC and web service DIR-3 KYC were not available for filing during the pendency of this activity.

Filing of DIR-3 KYC and DIR-3 KYC WEB can be made after completion of the scheduled activity, as above when the form & service are re-deployed on the portal after payment of applicable fees.

The DINs which have not complied with the requirement of filing DIR-3 KYC has since been marked as ‘Deactivated due to non-filing of DIR-3 KYC’.

Such DINs are not allowed to be used for filing any e-forms on the MCA21 portal.

In case the present status of your DIN is ‘Deactivated due to non-filing of DIR-3 KYC’, you are required to file ‘KYC’ using e-form DIR-3 KYC or DIR-3-KYC-WEB service as applicable with prescribed fee of INR 5000 to re-activate your de-activated DIN.

The revised FAQs related to DIR-3 KYC have been updated, giving detailed guidelines as below:

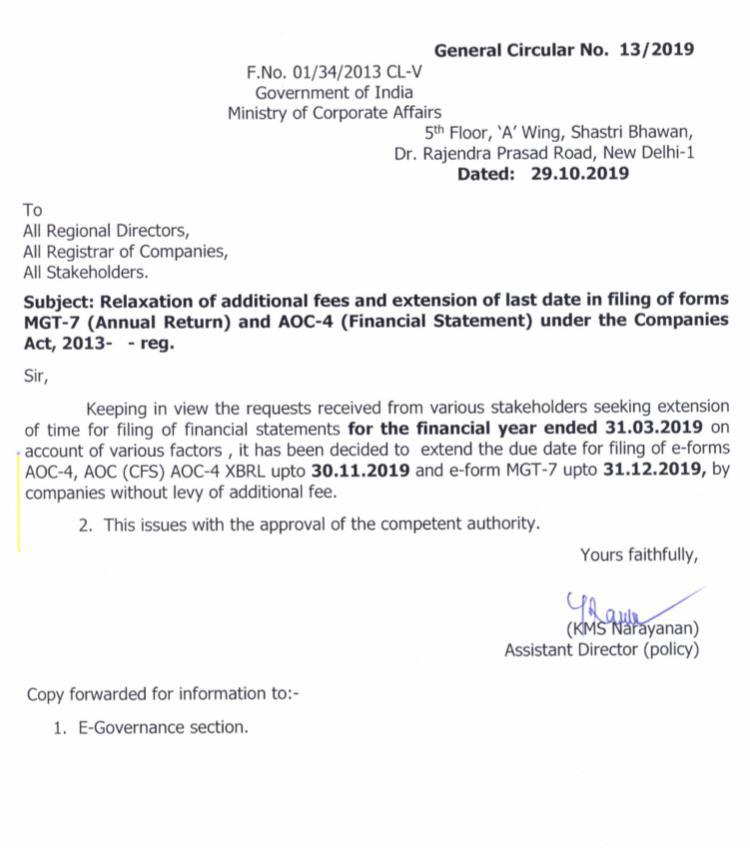

MCA extends due date for filing of AOC 4 and MGT 7 (Financial Statements & Annual Return)

MCA has notified that the due date for filing of financial statements and annual return in e-forms AOC 4, AOC (CFS) and AOC-4 XBRL upto 30 Nov. 2019 and e-form MGT 7 up to 31 Dec. 2019 by companies without levy of additional fee, in view of the practical difficulties faced by various stakeholders and the requests from various professional bodies and businesses, as under:

The due dates for filing Financial Statements – AOC-4, was 30 Oct,2019 and for the Annual Returns – MGT-7 was 30 Nov,2019. Both these are now relaxed by additional 1 more month for filing with Ministry of Corporate Affairs, without levy of additional fee.

The government, in creating disciplinary mechanisms, could consider bringing in disclosure norms for auditors with respect to non-audit services and fees charged by them

The Ministry of Corporate Affairs is planning to amend the Chartered Accountants Act to build disciplinary mechanisms for removing possible conflicts of interest between audit firms and companies they audit.

The government is also looking at ways to address the gaps in the law with respect to network entities of which audit firms are part.

“We need to strengthen the Chartered Accountants Act. Many entities need to be brought within the regulatory remit to create accountability and transparency,” a senior government official told Business Standard.

The government, in creating disciplinary mechanisms, could consider bringing in disclosure norms for auditor with respect to non-audit services and fees charged by them

As part of Government of India’s Ease of Doing Business (EODB) initiatives, the Ministry of Corporate Affairs would be shortly notifying & deploying a new Web Form christened ‘SPICe+’ (pronounced ‘SPICe Plus’) replacing the existing SPICe form.

As part of Government of India’s Ease of Doing Business (EODB) initiatives, the Ministry of Corporate Affairs would be shortly notifying & deploying a new Web Form christened ‘SPICe+’ (pronounced ‘SPICe Plus’) replacing the existing SPICe form.