Non-banking finance companies could well outpace commercial banks, struggling to grow amid muted loan expansion and bad loan burden, said global rating company Moody’s.

But, NBFCs too are exposed to certain risks emanating from their fast-faced growth in loan against properties, which they are in a position to mitigate with larger share in mortgaged loans.

Non-bank financial companies (NBFCs) in India (Baa3 positive) will demonstrate broadly stable asset quality, but delinquencies will likely rise over the next 1-2 quarters, as demonetisation adversely affects collections across asset classes, said Moody’s Investors Service in a note.

“While the 90+days delinquency rate in the commercial vehicle (CV) loan segment largely stabilized in the first half of the fiscal year ending 31 March 2017, such delinquencies should build up in the near term due to the adverse impact of demonetisation and tighter recognition norms for non-performing assets (NPAs),” said Alka Anbarasu, a Moody’s Vice President and Senior Analyst.

Moody’s also notes that the growth in loans against property (LAP) has outpaced overall retail credit growth in recent years, but relatively loose underwriting practices–combined with intensifying competition – will translate into higher asset quality risk for this segment.

Furthermore, over the past 3 years, NBFCs have gained some market share in the origination of retail lending, on the back of the faster growth exhibited by such entities when compared to the banks.

This is particularly the case when compared to public sector banks, which face significant challenges on their asset quality and overall solvency profiles.

“Nevertheless, we expect that competitive pressures from the banking sector will remain intense as banks are increasing targeting of the retail segment to offset weakness in their corporate lending. In addition, retail lending, particularly housing loans, is more capital efficient for the banks,” said Anbarasu.

And, while the NBFCs’ capitalization levels are adequate, with average Tier 1 ratios in excess of 14%, capital generation will lag credit growth. Access to external capital will therefore be key in sustaining the NBFCs’ growth momentum.

On funding, Moody’s expects that the NBFCs’ funding profiles will broadly remain stable, and funding costs should moderate gradually, given the reduction in systemic rates.

In addition, the NBFCs’ profitability and capital, as well as funding and liquidity levels, will stay broadly stable.

The NBFCs are growing at a fast pace, and have gained market share in the origination of retail credit. And, their share of LAP pose a potential source of risk, with such loans growing at a rapid compound annual growth rate of about 25% over the last four years compared to 17% for overall retail credit.

Moody’s says that the NBFCs’ exposure to potential risks from LAP is broadly offset by their share of stable mortgage loans, because favorable demographics and economics, tax incentives for home loans and an increasingly affordable housing segment support asset quality.

Moody’s expects that the loss given default for both home loans and LAP will be limited, in light of the underlying collateral.

IMF in its note titled ‘Global Prospects and Policy Challenges’ said, “Further subsidy reduction and tax reforms, including a robust design and full implementation of the Goods and Services Tax (GST), are necessary to attain medium-term fiscal consolidation plans.”

India’s economic growth is expected to pick up once the effects of cash shortages linked to the currency exchange initiative fade, the International Monetary Fund (IMF) has said. Prime Minister Narendra Modi on November 8 had announced scrapping of old Rs 500 and Rs 1000 notes, pulling out 86 per cent of the total currency in circulation.

Noting that India’s fiscal deficit is expected to continue narrowing in the near-term, the IMF in its note titled ‘Global Prospects and Policy Challenges’ said, “Further subsidy reduction and tax reforms, including a robust design and full implementation of the Goods and Services Tax (GST), are necessary to attain medium-term fiscal consolidation plans.”

It further observed that in some emerging economies like China and India reducing excessive corporate leverage and improving bank’s balance sheets or adopting more prudent risk-management practices, including to reduce currency and maturity balance sheet mismatches, will help reduce vulnerabilities to global financial conditions, possible capital outflows, and sharp currency movements.

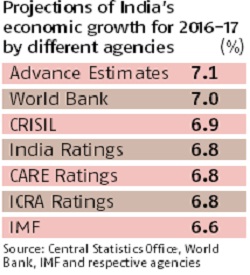

The government last month pegged GDP growth at 7.1 per cent for 2016-17 despite the note ban. The Central Statistics Office (CSO) had put the figure for October-December at 7 per cent, compared to 7.4 per cent in the second quarter and 7.2 per cent in the first.

India’s growth was higher than China’s 6.8 per cent for October-December of 2016. The growth numbers were better than those projected by RBI (6.9 per cent) and international agencies like IMF (6.6 per cent) and OECD (7 per cent) in view of the cash recall. The Organisation for Economic Cooperation and Development (OECD) in February last year had projected the country’s growth at 7.4 per cent for 2016-17. Buoyed by higher-than-expected growth, Finance Minister Arun Jaitley has also said a 7 per cent expansion in the third quarter belies the exaggerated claims of note ban impact on the rural economy.

World Bank CEO Kristalina Georgieva pegs India’s GDP growth rate at 7% for 2016-17, says ongoing reforms, GST implementation augur well for the economy

The government’s decision to ban high-value banknotes as part of efforts to stamp out corruption will have a profound and positive impact on India’s economy, World Bank chief executive Kristalina Georgieva said.

Demonetisation may have caused some hardship to people living in the cash economy but in the long run the move will help foster a clean and digitized economy, Georgieva said.

“What India has done will be studied (by other countries). There hasn’t been such demonetisation in a country so big,” Georgieva told Hindustan Times in an interview late on Wednesday.

The World Bank CEO’s appreciation for the 8 November move which banned Rs500 and Rs1,000 bills, comes after the International Monetary Fund said in November that it supported India’s efforts to fight corruption through currency control measures.

Georgieva compared the move to that of the European Union, which is also phasing out high denomination bills but over a longer period of time.

“While demonetisation has, in the short term, created some impact on businesses dependent on cash, in the long term the impact will be positive… The reforms India is targeting are profound,” she said.

She also said the government’s financial inclusion programme along with the move towards digital payments and direct transfer of subsidies will help the poor.

Georgieva, who was in India for two days, travelled on a local train in Mumbai and visited the world’s biggest slum in Dharavi. She said she found that people were eager to get a better life and were willing to pay more for improved services. Georgieva also appreciated the competition among states to improve ease of doing business. “India is the bright spot in today’s global economy and it is visible in the country’s performance and more so in the aspirations of the people here,” she said.

“Our growth projection for India for this year is 7%. The signs are positive with the reform process underway and GST (goods and services tax) expected to be implemented soon.”

The Organisation of Economic Cooperation and Development (OECD) has supported India’s demonetisation drive, asserting that immediate impact of the move on Indian economy will be transient.

The Organisation of Economic Cooperation and Development (OECD) has supported India’s demonetisation drive, asserting that immediate impact of the move on Indian economy will be transient.

“Implementing the demonetisation has had transitory and short- term costs but should have long-term benefits,” OECD said on Tuesday in its report, Economic Survey of India. OECD Secretary-General Angel Gurria said the impact of demonetisation on consumption pattern may just have been limited to the quarter ended December 31, 2016.

The Paris-based global policy forum projected a GDP growth rate of 7 percent in the current financial year, while estimating it to grow to 7.3 percent in FY18 and 7.7 percent in FY19.

The OECD comments come a few hours before the Central Statistics Office (CSO) releases Gross Domestic Product (GDP) growth estimates for Q3FY17 and the second full year advance estimates for 2016-17. The GDP estimates released in January projected that India would grow 7.1 percent in 2016-17 from 7.9 percent in the previous year.

Amid signs of slide in consumer goods sales and muted investment activity because of the cash crunch, it is highly likely that the CSO will sharply revise downwards India’s GDP growth in its second advance estimates. Economic Affairs Secretary Shaktikanta Das, who was also present at the launch of the report, said that the benefits and outcomes of demonetisation would be positive from next quarter. “The process of remonetisation is nearly complete. Any adverse impact of consumption in that quarter is not likely to spill over next year. So that is over and behind us,” Das said.

“The shift towards a less cash economy and formalisation should, however, improve the financing of the economy and availability of loans (as a result of the shift from cash to bank deposits) and should promote tax compliance,” the report said.

On November 8, Prime Minister Narendra Modi announced that existing 500 and 1000 rupee notes would cease to be legal tender, thereby sucking out 86 percent of the currency in circulation from the economy. The survey, however, said that the temporary cash shortage and wealth destruction, as fake currency and illegal cash will not be redeemed. T

he report further said that the implementation of the goods and services tax (GST) reform will contribute to making India more integrated market. “By reducing tax cascading, it will boost competitiveness, investment and job creation.

The GST reform — designed to be initially revenue-central — should be complemented by a reform of income and property taxes,” the OECD survey said.

The survey pointed out that investment is still held back by relatively high corporate income tax rates, slow land acquisition process, weak corporate balance sheets and high non-performing loans which weigh on banks’ lending and infrastructure bottlenecks.

Key recommendations of OECD included raising revenue, especially from property and personal income taxes, ensuring that government debt to GDP ratio returns to a declining path, as well as strengthening of public bank balance sheets by recapitalising them and promoting bank consolidation.

It also suggested simpler and flexible labour laws and a gradual reduction in corporate income tax from 30% to 25%, while broadening the tax base.

Official data released on Tuesday showed that demonetisation hasn’t pushed the economy into a retreat as most feared, with its short-term adverse impact. (Source: Reuters)

Official data released on Tuesday showed that demonetisation hasn’t pushed the economy into a retreat as most feared, with its short-term adverse impact to a large extent restricted to construction and financial services. Real GDP growth in the December quarter, in the midst of which the note ban came into effect, came in at a respectable 7% (though lower than 7.4% in the previous quarter) and the gross value added (GVA) was 6.6%, with the difference explained by robust indirect taxes and reining in of subsidies.

Upward revision of GVA estimates for 2015-16 led to downward corrections in GVA for Q1 and Q2 of the current fiscal but despite this, there were marginal upward revisions in the rates of GDP expansion in these quarters, thanks to a surge in indirect taxes.

Solid performance by the “agriculture and allied sectors”, pump-priming by the government on the consumption side, better-than-expected performance by mining and manufacturing sectors and a seasonal — though larger-than-usual — pick-up in private consumption masked whatever negative effect the note swap exercise had on the economy, going by the Central Statistics Office’s data.

However, as the GDP was slowing even before demonetisation and the note swap has indeed had an incremental adverse effect on it, both GDP and GVA growth for 2016-17 have been projected to be much lower than in the previous year. In the second advance estimate, the CSO has kept the GDP growth estimate for the current financial year at 7.1%, the same as in the first advance estimate released in early January, and GVA growth at 6.7%. But given that 2015-16 GDP growth, which was seen at 7.6% at the time of the first advance estimate, was subsequently revised to 7.9%, the CSO’s latest take on 2016-17 growth is virtually more sanguine than its previous estimate.

While the CSO’s GDP estimate for 2016-17 is evidently higher than that of most others, many analysts said the growth assumed by it for the second half (6.8%) was optimistic. “Given the fact that the fall from H1 to Q3 is not much, I don’t think that we should then necessarily assume that the rebound in Q4 is going to be very sharp,” said Aditi Nayar, economist at Icra. Stating that the GDP number is better than expected, Saugata Bhattacharya, chief economist at Axis Bank, said, “Since growth slowdown (due to demonetisation) has been shallower than expected, and in line with the RBI’s projections, the probability of rate cuts going ahead has come down.”

The minutes of the monetary policy committee’s meeting released last week indicated that it changed its stance from “accommodative” to “neutral” because the growth drag from demonetisation is expected to fade soon. India Ratings reiterated its view that “much of the impact of demonetisation will be visible in Q4FY17 leading to an overall GDP growth of 6.8% in 2016-17”.

Economic affairs secretary Shaktikanta Das said: “This year’s GDP (growth) is around 7%, based on available numbers. Nothing can be deciphered on anecdotal evidence. Demonetisation only impacted consumption in some cities, since most purchases happened on credit or debit cards. The so-called negative impact, if relevant, was only temporary.”

The 7% GDP growth forecast for the third quarter helped India maintain the coveted tag of the world’s fastest-growing major economy despite demonetisation, better than China’s 6.8% in the December quarter.

While analysts pointed out the lack of congruity between the CSO’s estimate and other high-frequency data and corporate results, chief statistician TCA Anant said all available data have been made use of in the second advance estimate, including corporate performance up to the December quarter, sales of commercial vehicles, railway freight, etc, for the first “9/10 months of the financial year”.

According to the CSO, with production growth of foodgrains during 2016-17 kharif and rabi seasons being 9.9% and 6.3%, respectively, the farm sector grew a robust 6% in Q3 from 3.8% in the previous quarter and compared with a 2.2% contraction in the year-ago quarter. Despite the anecdotes of industrial clusters hit by the note ban during the period, manufacturing grew a healthy 8.3% in Q3 on a robust base of 12.8% in the year-ago quarter and compared with 6.9% in Q2 this fiscal. Mining also posted a smart recovery from a fall of 1.3% in Q2 to a robust expansion of 7.5% in Q3. The bad performers on the output side was “financial services, etc”, which posted a modest 3.1% growth in Q3 compared with 7.6% in the previous month, and construction which grew just 2.7% in the December quarter.

Government final consumption expenditure (GFCE) posted a 19.9% growth in Q3 against 15.2% in the previous quarter, the CSO said. Given that 17% growth in GFCE is estimated for the whole of 2016-17, it needs to grow at 17.4% in Q4. Considering that the Centre, as is seen from the April-January fiscal data separately released by the Controller General of Accounts, has slowed down spending in the later months of the year, the spending boost must come from PSUs.

Although both Dussehra and Diwali fell in the December quarter, the 10.1% growth reported by CSO in the private consumption expenditure looked puzzling to most analysts (but some said use of old notes for consumption might have contributed to the rise). So was the 3.5% growth in gross fixed capital formation, which was declining for the previous three quarters.

Given that nominal GDP growth has been projected at 11.5% for 2016-17, compared with 10% in the last fiscal, it may offer more leeway to the government to improve spending in the next fiscal and yet contain fiscal deficit, which is expressed as a ratio of the nominal GDP, at the targeted 3.2%.

Discrepancies — the difference between the supply and demand side of GDP — turned negative after a gap of four quarters (-Rs 6,767 crore) in the December quarter, compared with Rs 45,378 crore in the second quarter and Rs 30,645 crore in the first quarter. In the last quarter of 2015-16, discrepancies touched a massive Rs 1,43,210 crore, causing a flutter then and raising doubts about the credibility of the country’s data collection mechanism. When private final consumption expenditure, gross fixed capital formation, government final consumption expenditure, change in stocks, valuables, and net exports exceed the overall GDP (based on the supply side data), discrepancies turn negative.

Analysts expect the exports sector to contribute more to GDP growth in the coming quarters, despite the demonetisation blues, thanks primarily to a favourable base. In real terms, the export growth for 2016-17 has been projected at 2.3%, compared with -5.4% in the last fiscal. Despite demonetisation, merchandise exports rose 2.3% in November, 5.7% in December and 4.3% in January.

India’s economic growth would slow to about six per cent in the second half of this financial year (October-March) due to demonetisation, against 7.2 per cent in the first half, the International Monetary Fund (IMF) said on Wednesday.

India’s representative in IMF Subir Gokarn said the growth projections came at a time when hard data was unavailable. He described the assessment as “unduly pessimistic”. In the medium term, however, the IMF is hopeful that implementation of the Goods and Services Tax could raise India’s growth rate to more than eight per cent.

The Fund said the cost of recapitalising public sector banks would be affordable even under a negative scenario. In a report on India, the IMF said growth would gradually rebound in 2017-18.

In January, it had cut India’s growth estimate to 6.6 per cent for 2016-17 due to the note ban, against 7.6 per cent estimated earlier. Growth was estimated to be 6.2 per cent in the fourth quarter of the financial year.

Taking both the estimates into consideration, the IMF said, third quarter growth might fall below six per cent.

The Central Statistics Office will come out with the third quarter gross domestic product (GDP) data and the revised advance estimates on the coming Tuesday. Its first advance estimates had shown economic growth at 7.1 per cent in 2016-17, against 7.6 per cent the previous year. The office had not taken into account the effect of demonetisation.

Commenting on IMF’s revision of growth rates, Gokarn said, “While we do not question the methodologies used to revise the estimates, the fact is that there isn’t very much hard data to base the revisions.” He said different assumptions about the impact would obviously lead to different conclusions. While virtually all forecasters have revised their projections for 2016-17 downwards, the range was relatively wide, he added.

To buttress his points, Gokarn said the World Bank and the Asian Development Bank have pegged growth at seven per cent, after accounting for change in the currency policy. The authorities’ estimate was 7.1 per cent. IMF directors supported India’s efforts to tackle illicit financial flows, but noted the strains that have emerged from the currency exchange initiative. They called for action to quickly restore the availability of cash to avoid further payment disruptions, and encouraged prudent monitoring of the potential side-effects of the initiative on financial stability and growth. On tackling India’s $130 billion in stressed loans, the IMF said “recapitalisation costs should be manageable” at between 1.5 and 2.4 per cent of the GDP forecast, according to Reuters.

Of that, the government’s share would be between 1.0 and 1.6 per cent of GDP over the four years to March 2019, assuming 40 per cent of the loans have to be provided against. “It’s very positive that both the Reserve Bank of India (RBI) and the government are putting a shared focus on addressing the balance-sheet problem,” IMF Resident Representative Andreas Bauer told a conference call.

The chief economic advisor, Arvind Subramanian, on Wednesday backed a call by the RBI to set up an institution similar to “bad bank”, saying urgency was needed to address troubled loans weighing on the banking sector.

In a special report on corporate and banking sector risks in India, the IMF said recapitalisation costs would be “significantly higher if there is a policy shift to more conservative provisioning requirements”.

In case of a rise in the provisioning ratio to 70 per cent, cumulative recapitalisation needs would increase to 3.3-4.2 per cent of forecast GDP in the financial year to March 2019, with a government share of 2.2-2.8 per cent, the IMF said.

The IMF said with temporary demand disruptions and increased monsoon-driven food supplies, inflation was expected at about 4.75 per cent by early 2017— in line with the Reserve Bank of India’s inflation target of 5 per cent by March 2017.

The Fund said domestic risks flow from a potential further deterioration of corporate and public bank balance sheets, as well as setbacks in the reform process, including in GST design and implementation, which could weigh on domestic demand-driven growth and undermine investor and consumer sentiment.

On the upside, IMF said larger than expected gains from GST and further structural reforms could lead to significantly stronger growth; while a sustained period of continued-low global energy prices would also be very beneficial to India.

Income Tax officials could soon be at your doorstep if you have deposited a huge amount during the note-swapping exercise last year, and have not yet explained the source of the cash. “We have tried to keep the exercise non-intrusive. But if people have not come forward, then some kind of verification is needed especially in cases that involve deposits of large sums,” a senior income-tax department official told ET.

Under the ‘Operation Clean Money’, the I-T department had sent out SMSes and e-mails to about 18 lakh people who deposited over Rs 5 lakh each during the 50-day window from November 10 to December 30, because the desposits did not tally with their income.

The depositors were asked by the I-T department to explain the source of the money by logging in to its portal. By February 15, about 7.3 lakh people responded to the emails and explained their deposits.

According to the official, the department is now contemplating issuing notices or carrying out surveys in cases where no response has come or the replies are unsatisfactory.

“In cases where responses are not satisfactory, notices would be issued. In some cases where big sums are involved and response is not satisfactory, surveys could be carried out,” the official said, adding that people could be also asked to come to income-tax offices or tax officers may pay them a visit.

People with unexplained deposits during the demonetisation period have the opportunity to avail the Pradhan Mantri Garib Kalyan Yojana (PMGKY) by paying 50 per cent tax and depositing 25 per cent in non-interest bearing scheme for four years.

Incidentally, the I-T department is soon expected to send out the next batch of emails and SMSes, beginning the part two of the ‘Operation Clean Money’, which will target suspicious deposits below Rs 5 lakh identified through data analytics.

The department is examining the voluminous data received from banks on deposits made during the 50-day period. It is also hiring external experts to work on the data to identify splitting of deposits or use of other means to evade notice.

Non-banking finance companies could well outpace commercial banks, struggling to grow amid muted loan expansion and bad loan burden, said global rating company Moody’s.

Non-banking finance companies could well outpace commercial banks, struggling to grow amid muted loan expansion and bad loan burden, said global rating company Moody’s.