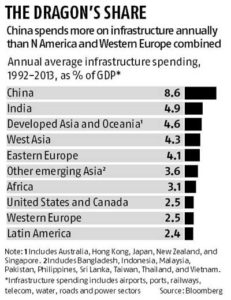

Despite a crying need for better infrastructure, investment in it has actually fallen in 10 major economies since the financial crisis, including the US, according to a new study by the McKinsey Global Institute. Meanwhile, China is still going gangbusters on roads, bridges, sewers, and everything else that makes a country run.

“China spends more on economic infrastructure annually than North America and Western Europe combined,” according to the report published Wednesday.

Economists around the world have been arguing that now is a great time to invest in infrastructure because interest rates are super-low and the global economy could use the spending jolt. “Is anyone proud of Kennedy airport?” Harvard University economist Lawrence Summers likes to ask.

The MGI report cites 10 countries where infrastructure spending fell as a share of gross domestic product from 2008 to 2013: the US, UK, Italy, Australia, South Korea, Brazil, India, Russia, Mexico, and Saudi Arabia. The study counts 11 economies, but that’s because it lists the European Union as a separate entity.

In contrast to the widespread declines, the institute says, infrastructure spending grew as a share of GDP in Japan, Germany, France, Canada, Turkey, South Africa and China. The chart from the MGI report shows China’s strength in infrastructure spending. Its bar is the highest. There’s such a thing as too much infrastructure spending, of course. At current rates of investment, China, Japan, and Australia are likely to exceed their needs between now and 2030, the McKinsey & Co-affiliated think tank says. To fund more public infrastructure, the report favours raising user charges such as highway tolls, among other measures.

To encourage more private investment in infrastructure, MGI argues for increasing “regulatory certainty” and giving investors “the ability to charge prices that produce an acceptable risk-adjusted return.”

An eBay sign is seen at an office building in San Jose, California May 28, 2014.

Online retailers would be banned from stopping a customer in one EU country buying from a website based in another, under a proposal issued on Wednesday to make it easier for consumers to shop across the bloc.

The European Commission said its law would stop “geoblocking” where companies limit access to their websites based on user location, often forcing customers to use versions based in their own country, sometimes with higher prices.

“In the online world, all too often consumers are blocked from accessing offers in other countries,” the Commission said in a statement.

“Such discrimination has no place in the single market.”

The law would affect companies such as Amazon, eBay and Zalando as well as to sales of services provided in a specific location, for example car rental, accommodation and concert tickets.

It would not initially apply to copyright-protected items such as e-books, music and games, although those might be included soon, the Commission said. So for the time being a German citizen would still be unable to buy a Spotify subscription in, for example, Estonia, where it is much cheaper.

The music industry welcomed the exemption, saying that to include such services in the geoblocking proposal would be “a serious blow for cultural diversity.”

Under Wednesday’s proposal, which requires the approval of the European Parliament and national governments to become law, retailers would not be allowed to block access to websites based on a user’s location or to re-route customers to a website version based in their own country without their consent.

Amazon already makes its websites accessible to customers anywhere in Europe, and says 98 percent of its own stock is available to shoppers from any European country.

While e-commerce websites will not be allowed to prevent customers in one EU country buying products in another, they will not be forced to deliver cross-border.

Therefore, an Italian buying a TV from a German website would either have to arrange their own delivery or collect it at the trader’s premises.

The Commission hopes the new rules will increase the proportion of consumers who buy online from another country, currently only 15 percent.

“The European Commission is doing the right thing by helping solve practical problems faced by online businesses, particularly small and medium sized businesses,” said eBay’s’ Paul Todd, Senior Vice President of EMEA (Europe, Middle East and Africa).

A business group said the proposal failed to address the reasons companies use geoblocking, such as differing VAT rates and consumer protection rules.

“This is like putting a sticking plaster on a broken leg,” said John Higgins, director general of DIGITALEUROPE, which represents companies such as Sony, Google and Dropbox.

In a separate proposal, the EU executive sought to increase the transparency of prices for cross-border parcel delivery and to give national authorities the power to assess whether they are affordable.

FTA with EU: India to take up ‘stock-taking exercise’ for a free trade agreement with the EU later this month, after a gap of three years, and pitch for greater market access in services..

India will undertake a “stock-taking exercise” for a free trade agreement with the EU later this month, after a gap of three years, and pitch for greater market access in services once the stage is set for further negotiations, a senior commerce ministry official said.

Before engaging in serious formal talks on the EU-India Bilateral Trade and Investment Agreement (BTIA), a “stock-taking exercise” will be undertaken, as some contours of the earlier negotiations have to be altered, keeping in view the changes that have taken place since the talks were stuck in 2013, Arvind Mehta, additional secretary in the commerce ministry, told FE.

For instance, India has further liberalised many sectors for foreign investments, including some of the areas where the EU had interests, over the past three years. For instance, the FDI cap in insurance has been raised to 49% from 26% and 100% FDI is allowed in telecoms. In private sector banking, full fungibility of foreign investment is now permitted and accordingly FIIs/FPIs/QFIs can now invest up to a sectoral limit of 74%, with certain conditions.

While India feels the flexibilities shown by it in further opening up to foreign investments should be considered positively by the EU, it also expects some reciprocal measures by the 28-member bloc to address its concerns, especially on data privacy and market access in the services sector. However, there will be no binding commitments until India’s core concerns are addressed suitably, Mehta said. The BTIA negotiations cover boosting goods and services trade as well as investment.

India seeks a data secure status because the high compliance cost with EU’s data protection laws will hit small and medium enterprises (SMEs) of India and make them un-competitive.

Mehta said India will be betting for a trade facilitation agreement (TFA) in services at the World Trade Organisation — similar to the TFA in goods — that would focus on liberalised visa regime, long term visas for business community and freer movement of professionals for the greater benefit of both India and the world. India will pursue it vigorously in negotiations for the BTIA as well as Regional Comprehensive Economic Partnership. RCEP is a proposed FTA between the Asean members and the six states with which it has forged FTAs, including India.

India is keen on services, as they account for over a half of its GDP. The EU is India’s largest trade partner, accounting for close to 15% of trade in both goods and services. It is a major market for Indian textiles, garments, pharmaceuticals, gems and jewellery and IT. The EU is also the largest source of FDI inflows to India, accounting for over one-fourth of the total. However, India ranks only ninth among the EU’s top trade partners, making up for just about 2% of its total merchandise goods in 2014.

BTIA talks were to be revived last year, but the EU’s surprise ban on 700 products of GVK shocked India, which then called off the negotiations. Prior to that, the negotiations centred around India’s demand for.

The EU is interested in further liberalisation of FDI in multi-brand retail and insurance, and closed sectors like accountancy and legal services. The underutilised private banking space in India is another draw. India’s intellectual property regime (IPR), which is unlikely to allow ever-greening of patents, remains a concern for European pharma majors. Moreover, the EU has been seeking a cut in the high import duties on assembled vehicles and wines and spirits. In case of assembled vehicles, the import duties remain in the range of 60-75%.

* Dollar at highest since March vs currency basket, euro down

* China’s yuan strengthened after IMF decision

* U.S. stocks down ahead of data; Asia dips, Europe up

* ECB stimulus expectations lift European stocks

* Oil rises ahead of ECB meeting, OPEC on Friday (Updates to afternoon, adds commentary)

* * * * * * * * * *

The dollar hit an eight-and-a-half-month high against major currencies Monday as the prospect of further European Central Bank stimulus dragged the euro down to its weakest since mid-April, while oil prices retreated.

Global stock markets were mixed, with Wall Street falling ahead of a crucial payroll report Friday, while European shares rose. Still, the three major U.S. indexes were set to end the month higher for a second straight month.

The jobs report is arguably the most important U.S. economic indicator due out before the Federal Reserve decides on Dec. 16 whether or not to raise interest rates for the first time in nearly a decade.

“The market has largely priced in a December hike and it would have to take a pretty significant miss with the jobs report to give the Fed some pause before its next meeting,” said Randy Frederick, managing director of trading and derivatives for Charles Schwab in Austin.

The Dow Jones industrial average fell 49.9 points, or 0.28 percent, to 17,748.59, the S&P 500 lost 6.37 points, or 0.3 percent, to 2,083.74 and the Nasdaq Composite dropped 16.24 points, or 0.32 percent, to 5,111.28.

The week is expected to highlight the divergent economic policies in the United States and the euro zone, which may set the tone for markets early next year.

European shares were lifted by the prospect of the ECB unveiling an extension of its bond-buying program at a Thursday meeting. The pan-European FTSEurofirst 300 index rose 0.4 percent for a 2.3-percent monthly gain.

The dollar index, which measures the greenback against a basket of major currencies, was up 0.16 percent despite disappointing data on U.S. business sentiment and pending home sales. It hit its highest point since mid-March and was set for its biggest monthly rise since January.

“The market’s really kind of looking through the numbers that are coming out right now and more looking towards the end of the week and central bank discussions,” said Douglas Borthwick, managing director at Chapdelaine Foreign Exchange in New York.

The euro fell 0.2 percent against the dollar to its lowest point since April.

The MSCI index of world stocks was off 0.4 percent and on track for a 0.9 percent decline for November.

Brent futures were lower and U.S. crude gave back earlier gains on Monday as a pre-OPEC-meeting rally and run-up in U.S. refined oil products faltered.

U.S. crude futures settled down 6 cents, at $41.65. Brent crude, the global benchmark ended down 25 cents, at $44.61 per barrel.

Gold, on track for its worst month since June 2013, traded up 0.7 percent at $1,065.86 an ounce.

U.S. Treasuries prices rose modestly Monday on hesitation ahead of speeches from top Federal Reserve speakers throughout the week. Benchmark 10-year Treasuries rose 2/32 in price to yield 2.221 percent, down from 2.222 on late Friday. The 30-year bond was up 6/32 in price to yield 2.99 percent.

European Central Bank (ECB) President Mario Draghi adddresses the European Banking Congress at the Old Opera house in Frankfurt, Germany November 20, 2015.

The world’s two biggest central banks will move decisively in opposing directions next week, with the European Central Bank (ECB) almost certain to ease policy on Thursday and a US jobs report likely to seal the case for a Fed rate hike in December.

Building a solid case for more easing on fears of anemic inflation, the ECB has all but committed itself to action, with the markets now guessing only about what exact steps it will take to kick-start price growth.

Still, there is plenty of room for surprises. The ECB will contemplate a wide range of measures, from a fairly uncontroversial deposit rate cut to more extreme – but highly unlikely – moves such as buying rebundled non-performing loans to resurrect bank lending.

“With expectations high, the risk of disappointment is also high but as concerns are correctly focused on the structural headwinds to the inflation outlook, there is really no point in holding back or saving ammunition at this stage,” Societe Generale said in a note to clients.

ECB President Mario Draghi has done his share to raise expectations. He has warned about increased risks to growth and inflation, and said “we will do what we must” to raise inflation as quickly as possible.

A Reuters poll of more than 50 economists predicted that the ECB would opt for a deposit rate cut to -0.3 per cent from -0.2 per cent, an expansion of its asset buying program to euro 75 billion per month from euro 60 billion, and an extension of that buying beyond September 2016.

There are a range of variations on this pattern, though. The ECB could opt for a deeper deposit rate cut, or it could add assets like corporate or municipal debt to those that it buys. It could even set a staggered deposit rate, punishing those who park large amounts of cash in its vaults.

The biggest complication to all this is the small but significant group of opponents to such action, led by Bundesbank chief Jens Weidmann and board member Sabine Lautenschlaeger, who broke ranks with their Governing Board peers recently to openly oppose further easing.

Overwhelm

Arguing that loose monetary policy poses risks and merely buys time to fix structural problems, Lautenschlaeger has taken a stance against any more steps, especially an expansion of the asset-buying program.

Draghi may have his work cut out bridging the gap between their views, as the ECB rarely votes at meetings and instead decides on policy with the broadest possible consensus.

His opponents could also make it tough for Draghi to continue his practice of promising big things, then exceeding the already heightened expectations.

“Expectations have increased further ahead of next week’s ECB meeting and ECB speakers have not done much to rein in expectations.

Draghi has overdelivered in the recent past but it could be harder this time given how much has been promised,” Deutsche Bank analysts wrote in a note to investors.

Citigroup said that to surprise the markets, the ECB would need to cut the deposit rate, increase its monthly bond-buying and adjust its forward guidance by extending the program or removing its reference to ending it next September.

While the euro area struggles with weak growth and high unemployment, the US is continuing to create jobs quickly. Data on Friday is expected to show that US non-farm payrolls increased by 200,000 in November, keeping the jobless rate at a 7-1/2 year low of 5.0 per cent.

But even if the figures disappointed somewhat, the Fed is still expected to hike at its meeting on December 15-16 given near full employment, with the debate likely shifting to future rate hikes rather than near term moves.

The biggest headwind for the Fed could be the dollar’s rapid firming against major currencies in recent months, which has already effectively tightened monetary conditions. But U.S. trade is less exposed to currency moves than elsewhere, such as in Europe, so the impact on policy is smaller.

Fed Chair Janet Yellen’s testimony to the Joint Economic Committee of the Senate on the economic outlook, due at the same time as Draghi’s press conference, will likely give more clues about the Fed’s next moves.

Among other top central banks, the Reserve Bank of Australia and the Bank of Canada are both expected to keep rates on hold with their respective economic outlooks in line or slightly better than their previous forecasts.

Despite a crying need for better infrastructure, investment in it has actually fallen in 10 major economies since the financial crisis, including the US, according to a new study by the McKinsey Global Institute. Meanwhile, China is still going gangbusters on roads, bridges, sewers, and everything else that makes a country run.

Despite a crying need for better infrastructure, investment in it has actually fallen in 10 major economies since the financial crisis, including the US, according to a new study by the McKinsey Global Institute. Meanwhile, China is still going gangbusters on roads, bridges, sewers, and everything else that makes a country run. In contrast to the widespread declines, the institute says, infrastructure spending grew as a share of GDP in Japan, Germany, France, Canada, Turkey, South Africa and China. The chart from the MGI report shows China’s strength in infrastructure spending. Its bar is the highest. There’s such a thing as too much infrastructure spending, of course. At current rates of investment, China, Japan, and Australia are likely to exceed their needs between now and 2030, the McKinsey & Co-affiliated think tank says. To fund more public infrastructure, the report favours raising user charges such as highway tolls, among other measures.

In contrast to the widespread declines, the institute says, infrastructure spending grew as a share of GDP in Japan, Germany, France, Canada, Turkey, South Africa and China. The chart from the MGI report shows China’s strength in infrastructure spending. Its bar is the highest. There’s such a thing as too much infrastructure spending, of course. At current rates of investment, China, Japan, and Australia are likely to exceed their needs between now and 2030, the McKinsey & Co-affiliated think tank says. To fund more public infrastructure, the report favours raising user charges such as highway tolls, among other measures.