It already touched a new high of $393.61 billion as on August 11, 2017, and the pace of forex reserves accretion has been the strongest since 2005.

India’s foreign exchange reserves are set to hit the $400-billion mark. It already touched a new high of $393.61 billion as on August 11, 2017, and the pace of forex reserves accretion has been the strongest since 2005.

The gain in the country’s forex reserves has been one of the strongest in Asia in the past 12 months.

India remains among the top-ten countries in forex reserve position and has a comfortable import cover of 12 months, as against the norm of three months.

India’s forex reserves touched an all-time low of $5.8 billion at end of March 1991, which could barely finance three weeks’ worth of imports.

It led the Centre to airlift national gold reserves as a pledge to the IMF in exchange for a loan to cover balance of payment debts.

The rise in forex reserves has been because of robust foreign direct and institutional investment flows, which made the rupee appreciate over 6% since January this year.

As a result of high forex reserves, the Economic Survey volume 2 has highlighted that most reserve-based external sector vulnerability indicators have improved.

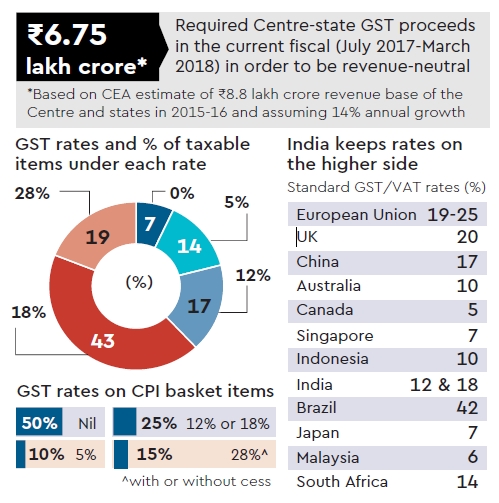

India embraced the goods and services tax (GST) on the intervening night of Friday-Saturday, in a move that marked the culmination of the country’s long and chequered journey toward a uniform, all-encompassing, pan-India indirect tax system.

India embraced the goods and services tax (GST) on the intervening night of Friday-Saturday, in a move that marked the culmination of the country’s long and chequered journey toward a uniform, all-encompassing, pan-India indirect tax system. The GST would militate against and cut out the cascade of multiple taxes which jack up product prices. The official launch of the tax preceded a grand ceremony in the central hall of Parliament attended by the president and prime minister, along with members of both Houses and the GST Council. Some Opposition parties including the Congress, Trinamool Congress and Left did not attend the ceremony, citing protests against GST by small and medium-scale entrepreneurs, traders, weavers and informal-sector workers.

Although the design of the new destination-based tax on consumption with its multiple rates, sub-optimal coverage and complicated rules is unmistakably inferior to an “ideal GST”, even independent tax experts welcomed the launch, calling it a transformational move. However, trenchant critics would say the imperfect GST has merely enabled cross-utilisation of credit between the central and state VAT chains and is, therefore, akin to the 2004 Cenvat rules that allowed such cross-credit facility between central excise and service tax.

But these critics might have taken too dim a view; GST is a momentous event for thee reasons: One, it puts in place a federal, rules-bound indirect tax system that would curtail the scope of rate differentials for the same products among states (one-product-one-tax) ; two, it could potentially slash India’s high logistics costs by speeding up movement of goods across state borders and even within states and thereby make the country’s goods and services more competitive; and three, thanks to the availability of seamless input tax credits, GST would discourage tax evasion and expand the revenue base for the government without hurting the businesses or the consumers. The GST will subsume excise duty and state VAT (along with the corresponding taxes on imports), service tax, octroi, entry tax, purchase tax, central sales tax, and entertainment tax, but not the basic Customs duty which is the tariff on imports.

Earlier, the GST Council, which met for an hour, decided to reduce the tax rate on fertilisers from 12% proposed earlier to 5%, a move that would nullify the chances of prices of these key farm inputs rising under GST. The gap between the current tax incidence on fertilisers and the 12% rate had created a practical difficulty in recovering the differential from fertiliser stocks lying with manufacturers and dealers as MRPs are printed on them. Also, the ministry of finance tweeted, the rate for “exclusive parts of tractors” have been reduced to 18% from 28%.

NITI Aayog member Bibek Debroy on Friday rebutted the claim that GST would produce 1.5% increase in GDP. “For an imperfect GST, I have no idea what is the figure. This particular figure (1.5%) was for ideal GST,” he said. Chief economic adviser Arvind Subramanian had told FE earlier that even though “we have not got as much base expansion and as much reduction in complexities as we would have liked”, there was still a huge reduction in complexities. “I expect a 10% expansion in the (tax) base due to just invoice-matching,” he had said.

While the government has iterated that the GST would not stoke inflation — GST will be zero on 50% of consumer price index basket and 5% on another 10% — former finance minister P Chidambaram said that the new tax could be inflationary in the short run. However, Subramanian said that with with actual tax incidence to be substantially lower under GST due to input tax credit, a downward bias on prices was to be expected. Firms disposing of stocks could also have a dampening effect on prices in the short run, he added.

Even as the industry is keeping its fingers crossed, the government has assured them that the anti-profiteering provision built into the relevant GST laws to prevent companies from not passing on the tax benefit under GST to consumers would be sparingly used. “I sincerely hope that we don’t have to really use the anti-profiteering mechanism,” Jaitley had said on Thursday. Chidambaram, however, sharply criticised the mechanism, saying it was wrong to assume that “the element of taxes decide at what price I sell my goods”. Since tax is only one of the things that make up costs, he said, if tax falls, it does not mean there should be a corresponding reduction in prices.

Even though 68 lakh businesses have already been issued provisional IDs by GSTN, the IT backbone for the new system, and the deadline for first filing of returns have been postponed to August 20 — invoice-wise returns can be filed as late as the first week of September — concern over the transition pains remained. Arun Kumar, chairman and CEO at KPMG in India, said: “The focus should now be on making the transition seamless and effective. Making compliance cost-effective, particularly for smaller businesses, is extremely important. The potential benefits of this landmark-reform will become real when the benefits of rationalised taxation accrue to consumers and business benefits from cost-efficiencies in logistics and streamlined processes.”

According to Shyamal Mukherjee, chairman, PwC India, “We are confident (that GST) will boost investors’ confidence in India, incentivise manufacturing and fuel the growth of the economy.” When asked about the quantum of extra growth due to GST by a TV channel earlier in the day, the chief economic adviser, however, merely said GST’s effect on the economy would be “positive”. “The medium-term impact of GST on macroeconomic indicators is expected to be extremely positive. Inflation will be reduced as cascading of taxes will be eliminated,” CII director general Chandrajit Banerjee said, adding that exports would emerge as more competitive in global markets, while FDI was likely to be encouraged.

Foreign exchange reserves touched a record high of $381.96 billion as on June 16, compared $381.16 billion in the previous week, the Reserve Bank of India said in its weekly statistical supplement on Friday. Foreign currency assets (FCAs), the largest component of the foreign exchange reserves, increased to $358.08 billion from $357.28 billion in the previous week, central bank data showed. Expressed in US dollar terms, FCAs include the effects of appreciation/depreciation of non-US currencies, such as the euro, pound and the yen, held in the reserves. So far in 2017, foreign exchange reserves have grown 6% and have touched record levels five times since April, as the RBI has aggressively been buying dollars to prevent a sudden jump in the rupee.

The central bank has been buying dollars on a daily basis, both in the spot market as well as in the forward market, to limit the appreciation of the local currency, which has been gaining steadily, traders said. The rupee has gained about 5% since the beginning of the year. Among other factors, strong demand for the local currency from foreign portfolio investors (FPIs) looking to invest in Indian assets has caused the rupee to appreciate. FPIs have bought Indian shares and bonds worth around $22 billion so far in 2017. Given India’s low current account and fiscal deficits, and the advantage it offers in terms of interest rate differential, traders expect the inflows to continue in the near-term.

The central bank has always maintained that it does not want to influence the exchange rate for the rupee, but would take steps, including intervention in the spot market, to curb extreme volatility. According to the latest available data, the RBI’s outstanding net forward purchases in April stood at $13.55 billion, up from $10.84 billion in the previous month. On the other hand, net purchase in the spot market dropped to $0.57 billion in April from $3.54 billion in March. The RBI publishes data on the sale and purchase of dollar with a lag of two months.

Foreign fund inflows hit a record high. So far this year, India has seen an inflow of nearly Rs 1.25 lakh crore.

The Indian rupee has been one of the best performing currencies among the emerging markets since the beginning of 2017, thanks to robust macroeconomic factors and attractive domestic bond yields. As a result, foreign fund inflows have hit a record.

So far this year, India has seen an inflow of nearly Rs 1.25 lakh crore, including Rs 73,200 crore in bonds, against an outflow of Rs 25,500 crore, a year ago. This is higher than foreign fund inflows in the first half of any previous calendar year, even as only the first week of June has got over so far. Given the present economic scenario, rupee is expected to sustain these levels and remain range bound.

India’s current account deficit has consistently improved over the years — from 4.8% of GDP in 2012-13 to expected 0.9 per cent in 2016-17, helped by weak oil prices, which constitute as much as 40-50 per cent of India’s imports.

With brent crude oil prices continuing to remain weak, down more than 8 per cent in the past two weeks and 1 per cent year-on-year, and the Reserve Bank of India keeping benchmark interest rate unchanged in its Wednesday policy meeting, the rupee is likely to continue to trade at the current levels vis-à-vis the US dollar in the short to medium term.

The resolution of the vexed issue of massive non-performing assets (NPAs) in the banking system is a work in progress and some “visible action” will be initiated over the next few days under the NPA ordinance promulgated recently, finance and defence minister Arun Jaitley said.

The resolution of the vexed issue of massive non-performing assets (NPAs) in the banking system is a work in progress and some “visible action” will be initiated over the next few days under the NPA ordinance promulgated recently, finance and defence minister Arun Jaitley said on Thursday.

“The RBI was taking measures under the existing mechanism. We have now taken other steps and there would be visible action taken under the new mechanism in the next few days,” Jaitley said, addressing media on achievements of the ministries under him over the past three years. The Centre won’t provide any special package to any state to waive farm loans but the states are free to spend from their own budgets should they take any such decision, the minister said.

Here are few excerpts from FM’s media briefing:

On NPAs and other things constraining private investments

Massive toxic assets impact the ability of banks to support growth, although record levels of foreign direct investments (gross FDI inflows touched $60 billion in 2016-17) and higher government spending have offset inadequate private investments to a certain extent. Linked to it (NPAs) is the challenge of wanting to increase private sector investment, even though our FDI and public investments have significantly increased. And of course there is a significant (adverse) impact of the global situation also (on private investments).

“Note ban not sole reason for Q4 GDP slowdown”

Demonetisation could be one of the several factors, and not the sole reason, that contributed to the slowdown of GDP growth to an 8 quarter-low of 6.1% in Q42016-17. What you think is very clear (that note ban dragged down Q4 growth) isn’t very clear. There are several factors which can contribute to GDP in a particular quarter. There was some slowdown visible, given the global and domestic situations, even prior to demonetisation in the last year. Financial services, which used to have 9-10% growth, has come down (to 2.2% in Q42016-17). Under the current global situation, 7-8% growth, which is at the moment the Indian normal, is fairly reasonable by our own standard and very good by global standards.

And I am sure as the impact of all these policies (taken by the government) holds out, growth will gather momentum. There won’t be any adverse impact of GST on GDP growth. The GST by itself should normally add to growth.

(Chief economic adviser Arvind Subramanian pointed out that under the GST, the incidence of tax is going to come down. While there could be some teething problem in implementation, at the most, initially, the tax cut would be positive to both reduce inflation and stimulate consumption).

On Pradhan Mantri Garib Kalyan Yojana

PMGKY wasn’t an isolated scheme in last financial year. First we introduced the Income Disclosure Scheme; after the IDS, there was a (post-demonetisation) phase of people depositing cash in the banking system. And the PMGKY was over and above these. To assess the total amount of (black money) disclosures made, you have to look at all the three collectively.

Revenue secretary Hasmukh Adhia said the response to PMGKY hasn’t been very good; only Rs 5,000 crore has been declared under the scheme. There are mainly two reasons for it. First, even before the scheme was announced, people had tried to deposit their cash in different accounts and tried to “adjust their money”. Secondly, many people found the (PMGKY) rate – 50% tax plus 25% as interest-free for four years – too high).

No central funds for farm loan waiver by states

The Centre won’t provide any special package to any state to waive farm loans but states are free to spend from their own budgets should they take any such decision. The Centre will continue to provide the states funds in accordance with the latest Finance Commission suggestions, and not more to waive farm loans (clarified that states are free to take decision on farm loan waivers from their own budgets but they have to stick to the 3% fiscal deficit target, as stipulated under the fiscal responsibility legislation).

On Air India

As far as AI is concerned, Niti Aayog has given its suggestion to the civil aviation ministry and the ministry will have to explore all the options for divestment or privatisation of the airline. The civil aviation minister will now devise the methodology ( for disinvestment / privatisation). As far the merger of oil PSUs are concerned, the petroleum ministry will have to take a call.

On “jobless growth”

Jobs aren’t created outside the economic structure. If the economy grows then it’s only natural that the formal sector would create jobs and in this country job creation is even faster in the informal sector. Since there is no firm statistics available on job growth in the informal sector, the term ‘jobless growth’ is being bandied about.

On the amount of demonetised currency

On the total currency given to the banks, the RBI used to give the figures frequently during the process of demonetisation, but now that the exercise is complete, as a responsible institution it can’t give an approximation. Today, every currency note is to be counted and if there are counterfeits these also need to be counted before arriving at the real count. The exercise is enormous and large but the RBI will give the accurate figure when it is complete.

FDI inflows in the services sector rose by about 26% to $8.68 billion in 2016- 17 with the government taking steps to improve ease of doing business and attracting foreign investments.

The services sector, which includes banking, insurance, outsourcing, research and development, courier and technology testing, had received foreign direct investment (FDI) worth $6.89 billion in 2015-16, according to data of the Department of Industrial Policy and Promotion (DIPP).

The government has taken several measures such as fixing timeliness for approvals and streamlining procedures to improve ease of doing business in the country and attract foreign investments.

With FDI growth in key sectors like services and telecom, the overall foreign investment inflows in the country too increased by 9% to $43.5 billion last fiscal.

Increasing FDI inflows in the services sector assumes significance as it contributes over 60% to India’s gross domestic product. The sector accounts for about 18% of the total FDI India received between April 2000 and March 2017, followed by key sectors such as computer software & hardware, construction development and telecommunications.

To further boost FDI inflows in the sector, the government is considering relaxation of policy in areas like single brand retail, multi-brand retail, print media and construction. The government is also focusing on enhancing services exports. It is organizing global services exhibition besides the commerce and industry ministry is looking at relax norms in areas like higher education to attract foreign players.

Foreign investments are considered crucial for India, which needs around $1 trillion for overhauling its infrastructure sector such as ports, airports and highways to boost growth. A strong inflow of foreign investments helps improve the country’s balance of payments situation and strengthen the rupee value against other global currencies, especially the US dollar.

Nina Vaskunlahti, Ambassador of Finland to India Paul Noronha

India is becoming one of the favorite destinations for investments in manufacturing, clean tech, infrastructure and hi-tech for Finnish companies.

Nina Vaskunlahti, Ambassador of Finland to India, in an interview with BusinessLine said, “There is increasing interest in economic cooperation, and Finnish companies are looking for new opportunities in India.”

Investment protection

According to Vaskunlahti, although India’s legislative framework can be a little complicated and the judicial system overworked and under-resourced leading to delays in solving disputes for foreign investors, overall the atmosphere is “welcoming and pretty open”.

However, according to the Ambassador, Finland is worried over India’s move to terminate investment protection agreement with 82 countries. “We are not quite sure what is the purpose of this,” Vaskunlahti said. While the treaty between India and Finland is still in force, according to Vaskunlahti, India and the European Union seem to be stuck over negotiating a new investment protection treaty after a year back India had sent request for renegotiation for the Bilateral Investment Treaty (BIT) to over 80 countries with whom it had earlier signed Bilateral Investment Promotion and Protection Agreements (BIPA).

“As a member of EU, we cannot negotiate on our own, because it’s the EU Commission that has a negotiating mandate,” Vaskunlahti said. “What we have now on the table is called a comprehensive negotiating mandate which covers both free trade agreement and the investment protection agreement. For the moment, nothing much is happening, but efforts and work are being done in background to push it forward.”

The new model of the BIT was cleared by the Union Cabinet in December 2015 and was seen to give more stability to foreign investors and prevent disputes with multinational companies by excluding matters such as government procurement, taxation, subsidies, compulsory licences and national security.

Arbitration mechanism

At the same time, the new model BIT brings in a provision obliging foreign investors to first exhaust the option of local judicial system at least for five years before going to international arbitration mechanism in case of disputes.

Some of the cases when foreign investors challenged India in international arbitrage, invoking clauses of earlier BIPAs include Devas Multimedia, Vodafone, Deutsche Telekom, Sistema and Cairn.

It led the Centre to airlift national gold reserves as a pledge to the IMF in exchange for a loan to cover balance of payment debts.

It led the Centre to airlift national gold reserves as a pledge to the IMF in exchange for a loan to cover balance of payment debts.