Section 12 (A) of IBC allows for a withdrawal of an insolvency application if 90% of the creditors’ committee (CoC) by voting share approving it.

Terming the current insolvency process and its outcomes as ‘super success, Ministry of Corporate Affairs sees total recovery amount touching Rs 2.8 lakh crore through resolutions with the settlement of two key accounts, including some others — Essar Steel, where financial creditors have approved the resolution and Bhushan SteelNSE 5.27 % and Power.

“The 100 cases that have been settled through resolution accounts, Rs 1.8 lakh crore have been netted which is not a small amount and the accounts sitting on margin (Bhushan Steel and Power & Essar Steel), another Rs 1 lakh crore along with some other mid-sized resolutions can come, so Rs 2.8 lakh crore out of Rs 10 lakh crore of NPA that time is not a small amount, IBC is a super success”, says MCA senior officials on the insolvency processes

In case of Essar Steel, the CoC has approved the resolution process but the process got stuck after operational creditor Standard Chartered moved NCLAT for higher share from the funds. The debt-ridden steel firm had Rs 42,000 crore coming from the resolution plan of global steel major ArcelorMittal.

JSW Steel had revised its offer for Bhushan Power & Steel from Rs 11,000 crore to Rs18,000 crore and later to over Rs 19,000 crore which the CoC had approved.

And it is not just resolution process-led recoveries, the official said pre-resolution processes have also yielded results in 6,500 cases netting Rs 3 lakh crore on dead assets.

“6500 cases settled involving claims of close to Rs 3 lakh crore where they have been have settled before admission. And now after 12 (A) has been introduced, another 100 cases which are at stages of 90% CoC approval are moving towards out of court settlements. Both (in and outside resolutions and NCLT) are happening. About 500 cases have got settled through the court process and 6,500 cases settled even before admission”, said the officials.

Section 12 (A) of IBC allows for a withdrawal of an insolvency application if 90% of the creditors’ committee (CoC) by voting share approving it.

MCA officials dismissed the notion of high haircuts through resolution process. They said: “It (IBC) is super success. There should not be any brouhaha over haircuts. Will anybody pay more than what is the value? Suppose an asset is used for 20 years, there is nothing more to it, there is a Rs 50,000 crore loan, liquidation value is Rs 1,000 crore, so you get (the creditors) Rs 1,000 crore only.”

“Wherever a resolution has taken place, creditors are getting 200% of the liquidation value. So definitely value maximisation is the context, demand and supply will fix the value”, the officials said.

Insolvency and Bankruptcy Board of India has published draft rules dealing with insolvency resolution process of individuals and firms on its website . The existing insolvency and bankruptcy code, at present, applies only to corporate defaulters

The government on Tuesday expanded the scope of the new insolvency rules to bring individual businesses under its purview.

On Tuesday, the Insolvency and Bankruptcy Board of India (IBBI) published the draft rules dealing with insolvency resolution process of individuals and firms on its website (www.ibbi.gov.in) ; public comments can be submitted till 31 October.

Once notified, even individual businesses such as proprietorships will come under the bankruptcy regime. This will enable an orderly bankruptcy resolution within the purview of a transparent rules-based regime. The existing insolvency and bankruptcy code, at present, applies only to corporate defaulters.

“These rules shall apply to matters relating to the insolvency resolution process for individuals and firms under Part III of the code,” said the draft rules issued by IBBI.

Part III of the Insolvency and Bankruptcy Code, 2016, deals with insolvency and bankruptcy of individuals and partnership firms.

According to a statement issued by IBBI on Tuesday, the draft rules and regulations have been submitted by a working group which was formed to recommend the strategy and approach for implementation of the provisions of the Insolvency and Bankruptcy Code, 2016, dealing with insolvency and bankruptcy in respect of guarantors to corporate debtors, i.e., personal guarantors, and individuals having businesses.

“So far, the rules were only in respect of the Corporate Insolvency Resolution Process (CIRP) and the rules concerning individuals and partnership firms were yet to come,” said Satwinder Singh, partner at Vaish Associates, a law firm. “The jurisdiction for corporate, companies, limited liability partnership (LLP) lies before the National Company Law Tribunal (NCLT) and with the Debt Recovery Tribunal (DRT) for individuals and firms. The provisions relating to insolvency and bankruptcy of individuals and firms had not been notified earlier, so now the IBBI has come out with the draft rules.”

Harsh Pais, partner at law firm Trilegal, said, “It is a positive step towards consolidating the bankruptcy regime for individuals, for whom there was no systematic approach previously. For companies, at least there was recourse to the Companies Act, whereas for individuals there were only some archaic laws from the early 1900s, which were hardly relied upon in practice.”

Most of the small and medium enterprises (SMEs) take the legal form of either partnership or proprietorship firms. Though the loans are smaller in value, SME borrowers far outnumber companies, resulting in their borrowings exerting a significant influence in the financial sector’s stability.

Bankruptcy resolution is high on the agenda of the central government, which is keen to improve the ease of doing business in India and attract more private investments from domestic and overseas sources. An efficient exit route from failed projects is an essential factor that lenders consider before participating in projects.

The Insolvency and Bankruptcy Board of India (IBBI), which has so far registered 940 insolvency professionals (IPs), is in the process of granting registration to about 100 more such professionals, according to its whole time member Navrang Saini.

The Insolvency and Bankruptcy Board of India (IBBI), which has so far registered 940 insolvency professionals (IPs), is in the process of granting registration to about 100 more such professionals, according to its whole time member Navrang Saini. “It is a continuous process, the applications come to us through insolvency professionals agencies, we examine the applications and carry out due diligence and then we grant registration to them,” said Saini while addressing an Assocham conference on IBC and RERA. The IBBI had received three applications for registration as information utility (IU) out of which two applicants have been granted in-principle approval and it is in the process of examining the third one.

“We are in the process of giving approval to one of the IU, we may give the final registration if they meet all criteria, we have already given in-principal approval to two IUs and out of that I hope one will start functioning by end of this month, the third application is still under examination with the board,” Saini said.

As on September 12, 3,437 cases have been filed out of which 354 cases have already been admitted by the various benches of NCLT. Out of these, 337 have already been rejected. “To deal with such a large number of insolvency related matters, we need institutional infrastructure,” he said.

Rules for registered valuers are to be made by ministry of corporate affairs which is in the process of notifying and issuing the same.

The board has already invited suggestions on the regulations which have already been notified by the board and it will receive the suggestions up to December 31 and come out with the amendments based on the suggestions received and advisory committees constituted for this purpose by March 31, 2018.

The IBBI chief said as per the Insolvency and Bankruptcy Code (IBC), resolution is left with the imagination of the market participants and they are free to take any call in regards to an entity, which is down with indebtedness.

Resolution of indebtedness of a firm will be the top priority of all constituents of the insolvency and bankruptcy mechanism in the interest of the stakeholders, and it will think about liquidation only if it finds that the resolution is hard to come by, Insolvency & Bankruptcy Board of India (IBBI) chairperson MS Sahoo said on Wednesday.

“In such a process, the first endeavour is resolution. If it is not resoluble then they think about liquidation. The endeavour of the law, insolvency professionals and committee of creditors is to first find out a resolution plan,” Sahoo said while speaking at a conference organised by PHD Chamber of Commerce and Industry.

The IBBI chief said as per the Insolvency and Bankruptcy Code (IBC), resolution is left with the imagination of the market participants and they are free to take any call in regards to an entity, which is down with indebtedness. The government is just trying to create an enabling environment.

The government’s effort is also to empower the market participants in every field and that is what has been the focus of the insolvency code where one gets not just the freedom to enter into a business, but also enjoys the freedom to exit the business.

“In our scheme of things, we have segregated the role of the state and the role of the market. We have also segregated commercial aspects from judicial aspects. Bankruptcy code says that insolvency professionals will run the company; but for a resolution, the decision of resolution will be taken by the market, that is the committee of creditors,” he said.

Sahoo also pitched for a market driven institutional mechanism to facilitate and enable mergers and acquisitions with minimum regulations that can conveniently safeguard the legitimate interests of concerned stakeholders. “Why can’t we have that kind of framework where approvals of the authorities are minimised, institutions work and everything is delivered by the market?” he asked.

Tough stance taken by govt, RBI makes borrowers cautious

Indian banks are beginning to spot a welcome change in their customers’ behaviour: borrowers who have seen their accounts classified as stressed or non-performing are approaching the lenders with proposals to resolve such accounts in a time-bound manner.

The tough stance taken by the central government and the Reserve Bank of India to end the festering bad loan crisis in the Indian banking sector has caught many borrowers by surprise and they are scrambling to put together resolution plans to avoid harsher penalties including insolvency proceedings, bankers said. Even a couple of months ago, it was difficult to get these clients to the negotiation table.

“I can definitely say that we are in a much better position than even six months ago. We are seeing traction from a section of our borrowers to come up with proposals for resolution of stressed accounts,” said Rajkiran Rai G, managing director and CEO, Union Bank of India. “However, it is too early to say if this is the end of the problem. We will have to see how the discussions shape up,” he added.

Borrowers with outstanding amounts between Rs 500-1,500 crore are the most active in trying to resolve their stressed accounts, and they are looking at various options including scouting for investors and sale of non-core assets, two senior bankers with state-run banks said on conditions of anonymity. A large number of these borrowers are from the steel, power and telecom sectors. Some of the larger corporates with outstanding amounts between Rs 1,500-5,000 crore have also taken initiative to resolve their stressed accounts. On an average, these account for about 50% of the current gross non-performing assets of the banking system, the bankers said.

In June, the RBI’s Internal Advisory Committee (IAC) had said 12 accounts totaling about 25% of the current gross NPA of the banking system would qualify for immediate reference under the Insolvency and Bankruptcy Code (IBC). At present, proceedings against all the 12 accounts are on in various benches of the National Company Law Tribunal across the country. For accounts that do not qualify under the above criterion, IAC had recommended that banks should finalise a resolution plan within six months. “In cases where a viable resolution is not agreed upon within six months, banks should be required to file for insolvency proceedings under IBC,” the RBI had said.

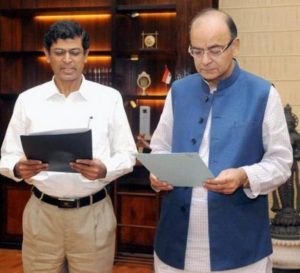

Union Minister for Finance, Arun Jaitley administering the oath to Madhusudan Sahoo as the Chairperson of the Insolvency and Bankruptcy Board of India (IBBI), in New Delhi.

The Insolvency and Bankruptcy Board of India (IBBI) has powers to start probe against service providers registered with it without intimating them, according to new regulations.

IBBI, which is implementing the Insolvency and Bankruptcy Code (IBC), has notified the regulations for inspection and investigation of service providers registered with it.

Insolvency professional agencies, professionals, entities and information utility are considered as service providers under the Code.

The Code, which provides for a market-determined and time-bound resolution of insolvency proceedings, became operational in December 2016.

As per the regulations, the investigation authority has to serve a notice intimating the entity concerned about the probe at least ten days in advance.

However, the requirement could be done away with on grounds such as apprehensions that the records of the particular service provider might be destroyed before the probe starts.

State Bank of India seeks applications for empanelment, sets stiff conditions

The Reserve Bank of India’s (RBI’s) move to push 12 large non-performing assets (NPAs) of the banking system into the insolvency process has created a massive business opportunity of up to Rs.2,500 crore for insolvency professionals.

To put the numbers in perspective, the RBI list comprises four companies with dues of over Rs.35,000 crore each. Even if one puts together all the few hundred cases handled by the six-month old framework, it would be a struggle to cross Rs.20,000 crore.

While the huge influx is likely to test the capacity of most players who are literally months old in the profession and present a steep learning curve, it will be a great stimulus for entry of stronger hands and investment in the segment.

According to the insolvency law, the entire process of corporate insolvency needs to be managed by a resolution professional appointed by a committee of creditors. The resolution professional, who will effectively become the chief executive officer of the business during the process period of 180 days, can charge a fee for his services. Besides, banks are also looking to appoint insolvency professionals to populate committees of creditors, which need to be formed for each of these companies.

With over Rs. 2.5 lakh crore debt coming in the top 12 companies in the first list, a one per cent charge works out to Rs. 2,500 crore. While this would be a ballpark figure, regulations do not prescribe a limit or range of fees, leaving a free hand for market forces. Globally, insolvency professionals work on various structures such as a fixed fee, time and effort-based charges, or a percentage of realisation. In some cases, a combination of these three methods could also be used. Banks would have pricing power, but good insolvency professionals would have their levers to charge a decent number, given the complexities involved and short supply.

Pavan K Vijay, managing director of Corporate Professionals, a Delhi-based firm that is looking at this opportunity, says the move gives a big boost to the nascent profession. “Even if the one per cent number does not work out, as there are bound to be negotiations, it could be around Rs.1,500 crore to Rs.2,000 crore. It is not small.”

The State Bank of India (SBI), the country’s largest lender, which also has the lion’s share of these 12 large accounts, has begun the process of empanelling insolvency professionals by issuing advertisements recently.

“The bank (SBI) seeks to empanel IRPs (insolvency resolution professionals) as resolution professionals in applications filed before the National Company Law Tribunal for resolution and/or liquidation proceedings, including for representing the bank in the committee of creditors as per the provisions of the code/and the regulations,” said the advertisements issued early last week.

Other banks are likely to follow similar processes in selecting insolvency professionals, as the public sector is generally process driven, regulatory officials say.

According to the Insolvency and Bankruptcy Board of India (IBBI) website, there were some 977 registered insolvency professionals in the inaugural limited period criteria and another 350 in the regular category, which requires passing the national insolvency examination. Lawyers, chartered accountants, and company secretaries form a majority. However, not all of them might be able to handle the large mandates. Given the large accounts it handles, the SBI has set stiff eligibility criteria for the applicants. It wants people with experience in debt restructuring, who are also experts in company law, etc. The application window closes early next week. Since the big accounts bring with them a lot of complexities, individual professionals might not be able to handle the entire task, Vijay said.

Several top lawyers such as Shardul Shroff and Pallavi Shroff of Shardul Amarchand Mangaldas, Alok Dhir of Dhir & Dhir, Bahram Vakil and Dushyant Dave are among the registered insolvency professionals. These would have established infrastructure and people to support their functions.

Also, the insolvency law provides for Insolvency Professional Entities (IPEs), which are corporate structures where two or more professionals can come together as partners or directors. However, there are only seven such registered IPEs as of today, according to the IBBI website. These are IRR Insolvency Professionals, a firm floated by Delhi-based lawyer Alok Dhir, AAA Insolvency Professionals, Witworth Insolvency Professionals, Gyan Shree Insolvency Professionals, A2Z Insolvency Services, Turnaround Insolvency and Nangia Insolvency Professionals.

Sandeep Gupta of Witworth, which is already handling a few mandates, feels while the opportunity is big, capacity and capabilities also need to be built up. “It is the beyond the means of an individual to handle a book size of several thousand crores. A company of such a size would have numerous non-financial creditors as well. These need to be handled in a given time frame. The resolution professional would need adequate support in terms of people and infrastructure,” he said.

For instance, Gupta said, he might hire a few freelance chief financial officers to manage one of the big accounts. Considering all this, calculating fee on a percentage basis could be misleading. It should be calculated, based on time and effort put in by the insolvency professional, he argued.

The SBI advertisement asks applicants to provide “tentative fees proposed to be charged” for various roles such as interim resolution professional, resolution professional on behalf of the committee of creditors or for being appointed as an insolvency professional to represent the bank in the committee of creditors. The bank also wanted to know whether the applicant would be “willing to abide by the fees decided by the bank.”