More than 90 days after the roll-out of the goods and services tax (GST), lenders are gravitating to sanctioning working capital loans, especially to micro and small units, against documents used in the new tax regime.

They are no longer looking at just sales of the units concerned to decide on loan sanctions.

Banks are looking at input credit in deciding how much working capital loans they should advance.

The country’s largest lender, State Bank of India, and Union Bank of India, also a public sector bank, have started giving loans, especially to micro, small and medium enterprises (MSMEs) after assessing their input tax credit claims.

A public sector bank executive said the large number of small and medium enterprises (SMEs) had been included under the ambit of formal trade with the introduction of the GST.

SMEs are facing a working capital crunch because in the absence of proper financial returns, they are unable to access bank credit.

In the traditional route, banks make working capital assessments based on sales, as indicated in the balance sheet.

Besides this, entrepreneurs are facing a credit crunch because in the GST regime SMEs are entitled to input tax credit, and it is stretching their operating cycle.

A Punjab National Bank (PNB) official said the banking system is shifting to looking at the history of transactions such as GST credit-based decisions about credit, especially for SMEs.

SBI Chief General Manager (SME) V Ramling said using GST claims by banks would give SMEs the time to manage their working capital requirements till the time they got input tax credit. It will also help stabilise SMEs to run their operations without any hurdles.

SBI said the loan would be sanctioned outside Assessed Bank Finance (ABF) at 20 per cent of the existing fund-based working capital limit or 80 per cent of input tax claim due on purchases, whichever is lower.

Units and companies seeking a loan under the product need to give a certificate from their chartered accountant, confirming the input credit claims.

Stressed loans near $10-billion mark; total bad loans seen at over $130 billion; 250 NCLT cases across 10 benches

While many of the loan exposures had turned toxic in 2015 and 2016, bankers were looking to recover their dues via other schemes such as the strategic debt restructuring or the S4A (scheme for sustainable structuring of stressed assets ) and 5/25.

While many of the loan exposures had turned toxic in 2015 and 2016, bankers were looking to recover their dues via other schemes such as the strategic debt restructuring or the S4A (scheme for sustainable structuring of stressed assets ) and 5/25.

With defaults on loans and corporate bonds nudging $10 billion in 2017 so far and the total quantum of bad loans estimated to have crossed $130 billion, the number of cases at the National Company Law Tribunal (NCLT) has jumped to around 250 across 10 benches. At the end of March, fewer than 40 cases had been referred to the tribunal. Banks are hoping to recover their loans via the Insolvency and Bankruptcy Code(IBC) and have already referred a dozen large accounts to the tribunal following a recommendation from the Reserve Bank of India (RBI). They are expected to approach the tribunal for another two dozen accounts.

Apart from banks, also knocking on the doors of the NCLT are other creditors such as non-banking financial companies and asset reconstruction companies. A few corporate debtors too have approached the tribunal.

While many of the loan exposures had turned toxic in 2015 and 2016, bankers were looking to recover their dues via other schemes such as the strategic debt restructuring or the S4A (scheme for sustainable structuring of stressed assets ) and 5/25.

Consequently, several of the exposures had not been classified as non-performing assets. With the RBI asking banks to refer the cases to the NCLT, the tribunal has been inundated with cases.

Industry watchers believe that given the quality of the fixed assets — plant and machinery — at many of the companies is of good quality, the firms are unlikely to be liquidated. However, buyers will come in only if banks take big haircuts since just about 45-50% of the debt is believed to be sustainable.

Of the 12 cases referred to the NCLT, 11 have been admitted. While some of the companies — Essar Steel, Bhushan Steel and Monnet Ispat — raised objections, the tribunal overruled these.

Bhushan Steel, which owes banks a whopping Rs 44,447 crore, had earlier objected to the insolvency proceedings alleging that State Bank of India (SBI) had inflated the dues by around Rs 100 crore.

Nonetheless, SBI’s petition was admitted by the NCLT, which ordered the interim resolution professional (IRP) to take charge of the company. The IRP, along with a committee of creditors, is currently working on a resolution plan.

The central bank has recently sent a second list of defaulters like Videocon Industries, IVRCL and Visa Steel that banks must take to the bankruptcy court if stress is not resolved by December 13.

These defaults, in turn, have put pressure on banks’ balance sheets which have reported a remarkable rise in bad loans in the June quarter of FY18. India’s largest bank SBI saw its gross bad loan ratio — total non-performing loans as a percentage of its total loans — rise 86 basis points sequentially to 9.97%.

SBI has an exposure of Rs 50,247 crore to the 12 accounts referred to the NCLT and the total provision on those accounts stood at Rs 19,943 crore. SBI chairman Arundhati Bhattacharya told reporters during the results press conference that the bank requires incremental provision of Rs 8,571 crore with respect to the 12 accounts in FY18.

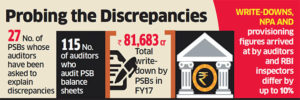

According to RBI data, PSU banks in FY17 have written off Rs 81,683 crore against Rs 2.49 lakh crore in the past five years.

The Reserve Bank of India (RBI) has questioned scores of auditors at 27 public sector banks on the process and logic they had used to compute and report write-downs at the lenders, two people close to the development told ET.

The RBI has sought written explanation on differences in the write-down assessments by its own inspectors and those certified by the auditors. A write-down is a reduction in the estimated and nominal value of an asset, and is charged off as a loss to the profit and loss account for the relevant period. In some cases, the RBI has also questioned the provisioning methodology and non-performing asset (NPA) figures arrived at by the auditors at a few public sector banks, sources told ET.

The banking regulator is examining whether auditors at these state-run lenders followed RBI guidelines on write-downs, provisioning and NPAs. “This is part of RBI’s annual assessment. Auditors will have to explain how they provisioned for NPA and how they calculated write-downs,” said a person aware of the matter.

The write-downs, NPA and provisioning figures arrived at by the auditors and RBI inspectors differ by up to 10%.

WRITE-DOWNS & PROVISIONING

According to RBI data, PSU banks in FY17 have written off Rs 81,683 crore against Rs 2.49 lakh crore in the past five years. In a few cases, the audit reports of some of these lenders do not reflect these write-downs, said one of the persons cited above. Most banks do not separately report write-downs in their accounts, combining them often with quarterly provisioning.

Most Indian public sector banks use more than one auditor due to the enormous size of their balance sheets. Most auditors are mid-to-small Indian firms that audit several branches. The 27 public sector banks collectively employ 115 auditors, according to data analysed by the ET Intelligence Group.

According to the people in the know, auditors at State Bank of India, Punjab National Bank, Bank of Baroda, Canara Bank, Allahabad Bank and Bank of India (BoI) were sent the show-cause notices about two weeks ago.

ET’s detailed email queries to the regulator and the affected lenders – SBI, PNB, BoB, IDBI, Indian Overseas Bank, Canara Bank, BoI, Oriental Bank of Commerce (OBC) and Allahabad Bank – did not elicit any response.

REGULATOR HAS PRIVILEGED ACCESS’

According to a major bank’s auditor who did not wish to be identified, the differences are not unexpected. “The RBI has access to information an auditor may not. Like, if a loan in bank X has gone toxic, the auditor of bank Y may not know, but the RBI would,” he said. He added that there is a time lapse between auditors preparing an account and the RBI conducting inspections. “What you must look at is the impact on the P&L of a bank due to divergence. In most cases, that is not much,” he said.

To be sure, there may have been ‘technical’ errors in interpreting the writedown rules, resulting in the differences. “There is a direct impact of the new accounting standards on the way write-downs are arrived at,” said a senior executive at a top audit firm. “Under the old accounting system, the rules around write-downs were not as precise, and there is a possibility that some auditors may have ignored this.”

Companies and financial institutions have mopped up close to Rs 56,000 crore by way of fund-raising through equities so far in 2017. This is about 20% higher than the amount of Rs 46,733 crore raised in 2016.

Companies and financial institutions have mopped up close to Rs 56,000 crore by way of fund-raising through equities so far in 2017. This is about 20% higher than the amount of Rs 46,733 crore raised in 2016. The fund-raising has been helped by a booming stock market; the Sensex has gained by 22% in the year so far.

On Monday, the benchmark gauge closed at 32,514.94.The Nifty has put on 23.10% in 2017 closing Monday’s session at 10,077.10.Since the beginning of the year, firms have mopped up Rs 55,905 crore through initial public offerings (IPO), offers for sale (OFS), Qualified Institutional Placements (QIP), and rights issues among others, data from Prime Database showed.

A significant portion — close to 61% — of the total equity raised this year has been by way of QIPs at Rs 34,182 crore. State Bank of India (SBI)’s Rs 15,000 crore offer has been the biggest in 2017 so far — the lender had issued around 52.21 crore new shares at a price of Rs 287.25.

The issue was aimed at augmenting the bank’s capital adequacy ratio and for general corporate purposes.This is the highest in the past eleven years. Banks constituted 84% of the amount raised through QIPs.

Market participants said the need for Tier 1 capital and the necessity to meet Basel III requirements as the reasons for banks opting for QIPs.

After QIPs, the maximum amount of money was raised through IPOs in 2017.

In 2017, companies raised Rs 14,026 crore through IPOs. Listing gains and returns by newly listed companies as also the positive sentiment in the broader market are among the reasons attributed to the trend.

BSE, HUDCO, CDSL, Avenue Supermarts, Shankara Building Products and S Chand and Company are some of the companies who completed their IPOs in the last seven months.

The newly listed companies have given good returns to investors, the BSE IPO index a gauge of newly listed companies rose by 40% year to date.

Small enterprises raised Rs 716 crore through SME IPOs, this is the highest since 2012.

Market participants said the buoyancy in the primary market is set to continue with more than a dozen companies gearing up to hit the market with their offerings.

State Bank of India seeks applications for empanelment, sets stiff conditions

The Reserve Bank of India’s (RBI’s) move to push 12 large non-performing assets (NPAs) of the banking system into the insolvency process has created a massive business opportunity of up to Rs.2,500 crore for insolvency professionals.

To put the numbers in perspective, the RBI list comprises four companies with dues of over Rs.35,000 crore each. Even if one puts together all the few hundred cases handled by the six-month old framework, it would be a struggle to cross Rs.20,000 crore.

While the huge influx is likely to test the capacity of most players who are literally months old in the profession and present a steep learning curve, it will be a great stimulus for entry of stronger hands and investment in the segment.

According to the insolvency law, the entire process of corporate insolvency needs to be managed by a resolution professional appointed by a committee of creditors. The resolution professional, who will effectively become the chief executive officer of the business during the process period of 180 days, can charge a fee for his services. Besides, banks are also looking to appoint insolvency professionals to populate committees of creditors, which need to be formed for each of these companies.

With over Rs. 2.5 lakh crore debt coming in the top 12 companies in the first list, a one per cent charge works out to Rs. 2,500 crore. While this would be a ballpark figure, regulations do not prescribe a limit or range of fees, leaving a free hand for market forces. Globally, insolvency professionals work on various structures such as a fixed fee, time and effort-based charges, or a percentage of realisation. In some cases, a combination of these three methods could also be used. Banks would have pricing power, but good insolvency professionals would have their levers to charge a decent number, given the complexities involved and short supply.

Pavan K Vijay, managing director of Corporate Professionals, a Delhi-based firm that is looking at this opportunity, says the move gives a big boost to the nascent profession. “Even if the one per cent number does not work out, as there are bound to be negotiations, it could be around Rs.1,500 crore to Rs.2,000 crore. It is not small.”

The State Bank of India (SBI), the country’s largest lender, which also has the lion’s share of these 12 large accounts, has begun the process of empanelling insolvency professionals by issuing advertisements recently.

“The bank (SBI) seeks to empanel IRPs (insolvency resolution professionals) as resolution professionals in applications filed before the National Company Law Tribunal for resolution and/or liquidation proceedings, including for representing the bank in the committee of creditors as per the provisions of the code/and the regulations,” said the advertisements issued early last week.

Other banks are likely to follow similar processes in selecting insolvency professionals, as the public sector is generally process driven, regulatory officials say.

According to the Insolvency and Bankruptcy Board of India (IBBI) website, there were some 977 registered insolvency professionals in the inaugural limited period criteria and another 350 in the regular category, which requires passing the national insolvency examination. Lawyers, chartered accountants, and company secretaries form a majority. However, not all of them might be able to handle the large mandates. Given the large accounts it handles, the SBI has set stiff eligibility criteria for the applicants. It wants people with experience in debt restructuring, who are also experts in company law, etc. The application window closes early next week. Since the big accounts bring with them a lot of complexities, individual professionals might not be able to handle the entire task, Vijay said.

Several top lawyers such as Shardul Shroff and Pallavi Shroff of Shardul Amarchand Mangaldas, Alok Dhir of Dhir & Dhir, Bahram Vakil and Dushyant Dave are among the registered insolvency professionals. These would have established infrastructure and people to support their functions.

Also, the insolvency law provides for Insolvency Professional Entities (IPEs), which are corporate structures where two or more professionals can come together as partners or directors. However, there are only seven such registered IPEs as of today, according to the IBBI website. These are IRR Insolvency Professionals, a firm floated by Delhi-based lawyer Alok Dhir, AAA Insolvency Professionals, Witworth Insolvency Professionals, Gyan Shree Insolvency Professionals, A2Z Insolvency Services, Turnaround Insolvency and Nangia Insolvency Professionals.

Sandeep Gupta of Witworth, which is already handling a few mandates, feels while the opportunity is big, capacity and capabilities also need to be built up. “It is the beyond the means of an individual to handle a book size of several thousand crores. A company of such a size would have numerous non-financial creditors as well. These need to be handled in a given time frame. The resolution professional would need adequate support in terms of people and infrastructure,” he said.

For instance, Gupta said, he might hire a few freelance chief financial officers to manage one of the big accounts. Considering all this, calculating fee on a percentage basis could be misleading. It should be calculated, based on time and effort put in by the insolvency professional, he argued.

The SBI advertisement asks applicants to provide “tentative fees proposed to be charged” for various roles such as interim resolution professional, resolution professional on behalf of the committee of creditors or for being appointed as an insolvency professional to represent the bank in the committee of creditors. The bank also wanted to know whether the applicant would be “willing to abide by the fees decided by the bank.”

RBI Deputy Governor S S Mundra today said the pace of formation of new non-performing assets (NPAs) or bad loans has decelerated although some banks have posted losses for the first quarter of the current financial year due to higher provisioning.

He also said most of the banks are adequately capitalised and the government has promised additional capital if they require.

In a bid to shore up cash-strapped public sector banks, the government last month announced infusion of Rs 22,915 crore capital in 13 lenders including SBI and Indian Overseas Bank to revive loan growth that has hit a two-decade low.

As far as bad loans are concerned, he said, they are showing a mixed trend.

“When I look at individual results, there are number of banks for whom it appears that the worst is over but then there are other banks…still they are in middle of it and they would need to do some work before they get out of it,” he said.

“It would be naive to believe that there won’t be any NPA formation but the pace of new NPA formation has clearly decelerated, that is what the major trend is,” he added.

Gross NPAs of the public sector banks had surged from 5.43 per cent (Rs 2.67 lakh crore) of advances in 2014-15 to 9.32 per cent (Rs 4.76 lakh crore) in 2015-16.

As per the latest Financial Stability Report by RBI, the Gross NPA ratio for public sector banks may go up to 10.1 per cent by March 2017 under the baseline scenario.

Many banks including Bank of India, Dena Bank, and Central Bank of India, reported losses for the quarter ended June 30, due to a sharp jump in provisions for NPAs on account of an asset quality review mandated by the RBI in December.

Talking about the recapitalisation, Mundra said the Finance Minister has indicated that if there is a need the government would be ready to provide additional capital.

“So, as far as the present situation is concerned I think most of the banks are adequately capitalised to take care of minimum regulatory requirements. We will keep a watch. As we move into the year we will see how things pan out,” he said.

On controversial virtual currency bitcoin, Mundra said: “This entire area fintech as we mentioned…you should not be stifling the innovation. Be mindful and what they call as regulator sand marks means you allow some of the experiments to happen under the control conditions so that the positive or the negative fallouts can be well understood and calibrated.”

India’s privately owned banks are extending new loans faster than their state-run rivals for the first time ever, as government lenders struggle to bring surging bad loans under control.

New credit from private lenders amounted to Rs.3,50,000 crore ($52.4 billion) in the year to 31 March, taking their outstanding advances to Rs.17,90,000 crore, while state banks’ loans grew Rs.2,00,000 crore to Rs.51,20,000 crore, according to a finance ministry document, a copy of which was reviewed by Bloomberg News. Finance ministry spokesman D.S. Malik didn’t respond to two calls to his mobile phone on Tuesday seeking comment.

The stressed-loan ratio for state banks climbed to a 16-year high of 14.34% in the year through March, according to the document. Surging delinquent loans and inadequate risk buffers at India’s government-controlled lenders, which account for more than 70% of loans in the nation’s banking system, have been hindering Prime Minister Narendra Modi’s attempts to revive credit growth in Asia’s third-largest economy.

“Private sector banks will continue to take away market share from state-run banks in coming years,” Siddharth Purohit, a Mumbai-based analyst at Angel Broking Ltd., said by phone. “With limited capital and high bad loans, most state-run banks are not in a position to focus on loan growth.”

The private-sector banks’ faster loan growth is in line with a May 2014 estimate from a central bank-appointed committee, which predicted that the lenders’ share of total Indian banking assets will rise to 32% by 2025, from 12.3% in 2000.

Capital constraints.

Modi needs to revive bank lending as he strives to maintain the fastest growth rate among the world’s major economies. Indian credit grew 9.8% in the 12 months through 13 May, compared with an average of about 14% over the last five years, fortnightly central bank data compiled by Bloomberg show.

Timely capital infusions into constrained public sector banks will aid credit flow, the Reserve Bank of India (RBI) said in its monetary policy statement on Tuesday. Rules requiring government stakes of at least 51% have curtailed state banks’ ability to sell shares, while an audit of loan books by the RBI uncovered more soured debt, making them less capitalized than privately-owned lenders.

While some investors had anticipated the six-month-long central-bank audit, which ended on 31 March, to result in higher non-performing-asset (NPA) disclosures, the scale of losses and statements from bank executives highlighting the uncertain outlook for bad debt have surprised analysts. Thirteen state-owned lenders reported combined losses of Rs.18,000 crore for the year to March, finance ministry data shows.

Government lenders are the worst performers this year on the S&P BSE India Bankex Index, led by Punjab National Bank’s 32% slump and State Bank of India’s 6.4% drop. The gauge has gained 6.1% this year. Bloomberg

More than 90 days after the roll-out of the goods and services tax (GST), lenders are gravitating to sanctioning working capital loans, especially to micro and small units, against documents used in the new tax regime.

More than 90 days after the roll-out of the goods and services tax (GST), lenders are gravitating to sanctioning working capital loans, especially to micro and small units, against documents used in the new tax regime.