Inter-ministerial body FIPB today cleared six foreign direct investment proposals worth about Rs 180 crore.

The Foreign Investment Promotion Board has cleared six proposals including those of Janalaxami Finance and Turmeric Vision, a Finance Ministry official said.

The panel headed by Economic Affairs Secretary Shaktikanta Das had considered 15 proposals.

The official further said four investments proposals were rejected while decisions on five were deferred for want of more inputs.

India allows FDI in over 90 per cent sectors via automatic route. However, investment proposals in sensitive sectors like telecom and banking go through FIPB.

In last two years, the government has taken a series of reforms measures to liberalise FDI regime. Last month, it announced FDI liberalisation in nine sectors such as civil aviation, retail and private security services. This was the current government’s second round of relaxation in these rules.

During 2015-16, FDI into the country increased by 29 per cent to $40 billion from $30.93 billion in the previous fiscal.

JPMorgan Chase & Co today said it has received Reserve Bank’s approval to open three more branches in the country.

The bank will open new branches at New Delhi, Devanahalli (near Bengaluru) and Paranur (near Chennai) in the next few months, it said in a statement.

“We are seeing an increasing level of cross-location and cross-border activity among our clients as they capture business opportunities driven by the country’s economic growth.

These branches will further enhance our capability to better serve our clients in India and overseas,” JPMorgan Chase Bank India MD and CEO Madhav Kalyan said.

JPMorgan will provide all existing products and services through these new branches, including cash management, trade finance and foreign-currency payments.

At present, the bank serves its clients from Mumbai branch.

“Our strategy is to follow our clients’ priorities. The expansion endorses our long-term commitment to India, a key market for JPMorgan, as well as for many of our clients,” JPMorgan South & South East Asia CEO Kalpana Morparia said.

The Reserve Bank of India has advised banks and financial institutions to submit data on defaulting borrowers from December 2014 onwards to Credit Information Companies (CICs) and not to the RBI.

Releasing this information, obtained through a portal complaint, Delhi-based Right to Information activist Subhash Chandra Agrawal said on Friday that it is significant to note that the RBI has not so far complied with the Supreme Court order of December 12, 2015, in the RBI vs PP Kapoor (Civil 94 of 2015) case, where it wanted the RBI to make public details of the top 100 loan defaulters among industrialists.

The details required including the names of the businessmen, firm name, principal amount, interest amount, date of default, and date of availing the loan.

In a June 24 letter addressed to Agrawal in response to his PG Portal complaint dated April 24, the RBI said it has submitted to the Supreme Court a list of defaulters above Rs. 500 crore in a sealed cover and claimed that the said information is confidential and requested that it may not be revealed to the public.

The matter is still under consideration of the Supreme Court.

India will maintain its growth rate of 7.6 per cent GDP growth in 2016-17, which would accelerate to 7.7 per cent in 2017-18 and 7.8 per cent in 2018-19, the World Bank said on Monday.

But for this, India will need to “activate the stalled engines”, including agricultural growth and rural demand, trade and private investment, while ensuring demand from urban households and public investments.

In its report ‘India Development Update- Financing Double Digit Growth’, the World Bank said the economy’s potential growth rate is about 7.4 per cent to 7.5 per cent.

“The outlook for the coming year is favourable and robust,” said Frederico Gil Sander, Senior Country Economist, World Bank, and main author of the report.

The report, also prescribed means for India to attain the elusive double-digit growth. This would depend on various factors, including higher participation of women in the labour force, productivity growth such as business environment reform agenda and GST as well as a pick-up in private investment.

The World Bank’s forecast is however, not as optimistic as the Finance Ministry that is eyeing 8 per cent growth this fiscal after 7.6 per cent growth last fiscal.

However, Onno Ruhl, Country Director, World Bank (India), said improved global prospects would also be necessary for double-digit growth in the domestic economy.

The report also warned that near-and medium-term risks stem from the banking sector and “its ability to finance private investment which continues to face several impediments in the form of excess global capacity, regulatory and policy challenges, in addition to corporate debt overhang”.

It has also suggested two key reforms in the financial sector — accelerating the ongoing transformation of banks to become more market oriented and competitive; and also to address the problem of non-performing assets (NPAs).

“India’s financial sector has performed well on many dimensions and can be a reliable pillar of future economic growth,” said Sander.

RBI top-level changes

While urging for more reforms in the banking sector such as giving fresh capital to banks for governance reforms or giving them tools to manage stress in their balance sheets, the World Bank declined to comment on the impact the top-level change at the Reserve Bank of India (RBI) will have on these measures.

“We respect the RBI Governor’s decision to return to academia. India has a long history of sound macro-economic policy making and effective and conservative supervisor. There is no reason to expect that it will change,” said Ruhl when asked whether the decision by RBI Governor Raghuram Rajan to not seek a second term would impact banking reforms.

In what showed a mindset shift among India’s policymakers, the government on Monday opened the floodgates for foreign direct investment (FDI) by easing the terms for nine sectors

In what showed a mindset shift among India’s policymakers, the government on Monday opened the floodgates for foreign direct investment (FDI) by easing the terms for nine sectors. Showing scant signs of legacy inhibitions, it virtually paved the way for even foreign airlines to acquire their Indian counterparts, removed the condition of domestic access to state-of-the-art technology for 100% FDI in the defence sector and put in abeyance the fractious 30% local sourcing norm for FDI in single-brand retail of advanced-technology products.

Despite the local pharma industry’s oft-expressed fear of being swamped by Big Pharma, foreign firms can now take majority (up to 74%) ownership in Indian drugmakers via the automatic route, which could again catalyse big-ticket M&A activity in the sector.

With the relaxations in the aviation sector, even a foreign airline could acquire 100% ownership in an India airline company by working in concert with a related party, according to some analysts. For example, a Qatar Airways could acquire a GoAir by directly picking up a 49% in the Indian firm and lapping up the balance equity through the West Asian nation’s sovereign wealth fund, Qatar Investment Authority.

Analysts, however, said the government seems to have tightened the sourcing rule in single-brand retailing, instead of giving a blanket exemption from such a rule for entities having “cutting-edge” technology, as was the case earlier. For instance, Apple will be exempted from the local sourcing rule for three years and have a relaxed sourcing regime for another five years if it wants to set up its own retail store, as its technology has already been described as “cutting edge” by a government panel. However, the company will still have to start local sourcing from the fourth year itself, thanks to the insistence of the finance ministry, which wanted that the Make in India programme get a boost. Similarly, Chinese company LeEco will be subjected to the same conditions if its claim of having “cutting edge” technology is endorsed by the panel headed by department of industrial policy and promotion secretary Ramesh Abhishek. However, another Chinese smartphone maker, Xiaomi, which recently withdrew its application for such a waiver, will have to comply with the mandatory 30% sourcing rule from the beginning should it wish to set up its own retail store.

Commenting on the new FDI policy for airlines, Amber Dubey, partner and India head of aerospace and defence at KPMG in India, said: “The avoidable controversies on settling ‘ownership and control’ issue is now over. Foreign airlines can now focus on the customers and competition rather than wasting time on legal and regulatory issues.”

“The likely increase in competition will bring down prices and enhance air penetration in India, both international and domestic. Indian carriers can now look for enhanced valuations in case they wish to raise funds or go for partial or complete divestment,” he added.

Calling the new norms a “bit tricky”, Amrit Pandurangi, senior director, Deloitte Touche Tohmatsu India, said, “Foreign airline investment is restricted to 49% and FDI investment in this sector has been opened up to 100%, so if the beyond the portion of the equity is by a related entity, then that needs to be tested.”

Among domestic airlines, the Rahul Bhatia-controlled Interglobe Enterprises holds close to 43% in IndiGo, Ajay Singh has a 60% stake in SpiceJet and Naresh Goyal holds 51% in Jet Airways. While Tata Sons holds 51% in both Vistara Airlines and AirAsia India, GoAir is wholly owned by the Wadia Group.

In defence, the decision to scrap the condition of access to “state-of-the-art technology” for FDI beyond 49% (through government route) will make it easier for foreign investors to invest in India. Already, Russian firm Kalashnikov is reportedly looking for local partners for manufacturing in India. Similarly, Swedish defence major Saab is learnt to be looking at more than 49% FDI in defence in its joint venture with a local partner to make the Gripen aircraft in India.

The government’s move to allow 100% FDI through the automatic route (earlier it was up to just 49%) in the broadcast carriage industry, comprising teleports, cable, direct-to-home (DTH) players, HITS (head-end-in-the sky) and mobile TV operators will provide a breather to the cable industry which has been struggling with the process of digitalisation of cable TV. The government has also allowed 74% FDI (49% under automatic route and through government approval beyond this ceiling) in private security agencies. Earlier, only 49% of FDI through government route was allowed.

Also allowed now is 100% FDI in animal husbandry (including breeding of dogs), pisciculture, aquaculture and apiculture under the automatic route under controlled conditions. It has been decided to do away with this requirement of ‘controlled conditions’ for FDI in these activities.

“For establishment of branch office, liaison office or project office or any other place of business in India if the principal business of the applicant is Defence, Telecom, Private Security or Information and Broadcasting, it has been decided that approval of Reserve Bank of India or separate security clearance would not be required in cases where FIPB approval or license/permission by the concerned Ministry/Regulator has already been granted,” a PMO statement said..

Monday’s is the second largest FDI liberalisation initiative by the Modi government, after the steps taken in November 2015. Prime Minister Narendra Modi tweeted: “In two years, Govt brings major FDI policy reforms in several key sectors… India now the most open economy in the world for FDI; most sectors under automatic approval route.” He added: “Today’s FDI reforms will give a boost to employment, job creation & benefit the economy.”

In what seemed to indicate that the government’s intention was indeed to let foreign airlines acquire Indian firms and thereby augment their capital and fleet strength for the benefit of air travellers, economic affairs secretary Shaktikanta Das said that Monday’s reforms in the sector were a “game changer”.

India’s FDI inflows increased to $55.5 billion in FY16 from $36 billion in FY14. Net FDI inflows stood at $36 billion in FY16 compared with $32.6 billion in FY15.

Commerce and industry minister Nirmala Sitharaman, however, rejected assumptions that the government decided to announce so many FDI policy reforms in one go to divert public attention from RBI governor Raghuram Rajan’s decision to not continue at the central bank after his current tenure ends on September 4. The reforms are a result of months of deliberations among various departments and are not announced in a hurry to divert attention, she affirmed.

In order to make the registration process of new non-banking finance companies smoother and hassle-free, the Reserve Bank of India has revised the application form for registration of these companies and the checklist of documents to be submitted.

The number of documents to be submitted by NBFC applicants has been reduced from the existing set of 45 documents to seven to eight in the revised process, the central bank said in a statement.

The RBI said henceforth there would be two different types of applications for non-deposit taking NBFCs (NBFC-ND) based on sources of funds and customer interface.

The first type (Type-I) will be a NBFC-ND not accepting public funds/ not intending to accept public funds in the future and not having customer interface/ not intending to have customer interface in the future.

“Public funds” include funds raised either directly or indirectly through public deposits, commercial paper, debentures, inter-corporate deposits and bank finance but excludes funds raised through issue of instruments compulsorily convertible into equity shares within a period not exceeding 10 years from the date of issue.

“Customer interface” means interaction between the NBFC and its customers while carrying on its business.

The second type (Type-II) will be NBFC-ND accepting public funds/ intending to accept public funds in the future and/or having customer interface/intending to have customer interface in the future

Fast track mode

The RBI said processing of cases for Type-I of NBFC-ND applicants would be on fast track mode. As these companies will not have access to public funds and will not have customer interface, they will be subjected to less intensive scrutiny/ due diligence.

However, the certificate of registration issued to Type I – NBFC-ND companies will be conditional. These companies will be prohibited from accessing public funds and having customer interface, the RBI said.

In case Type-I companies intend to avail public funds or intend to have customer interface in the future, they are required to take approval from the Reserve Bank of India, Department of Non-Banking Regulation.

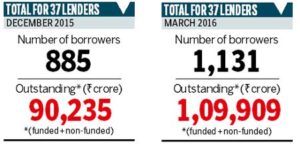

More than a thousand borrowers have outstandings that are substantially larger than the amounts sanctioned to them by banks, data sourced from Reserve Bank of India (RBI) shows. The total outstandings of 1,131 borrowers, at Rs 1,09,909 crore, were 150% more than the amount sanctioned, as on March 2016, data accessed by FE reveal. At the end of December 2015, the outstandings were Rs 90,235 crore.

Bankers and ex-bankers that FE reached out to attributed the pile-up in outstandings to short-term requirements of borrowers that were met by banks to help them tide over a cash crunch. Overdue interest, they said, could be another cause for the high outstandings. One senior banker observed that there were occasions when the capacity of the borrower to repay the additional amount was not assessed properly. “At times, limits get exceeded without a proper assessment of the customer’s ability to service the loan,” he said.

A former executive director of a public sector bank said one reason for the actual outstanding exceeding the permitted limits was that lenders tended to sanction ad hoc non-funded letters of credit (LC) even before the limits were okayed by the consortium. “Sometimes ad hoc LCs are opened for amounts which are bigger than those agreed to by the consortium. Since consortiums take anywhere between six months and a year to sanction limits, the money is disbursed since business cannot wait,” he explained, adding that such loans serve as working capital.

A former chairman of a state-owned bank said if the customer was unable to service the loan, the interest piled up pushing up the outstanding amount. “If the interest hasn’t been paid for three or four years, the amounts can become large,” he pointed out.

An RBI document on the Central Repository of Information on Large Credits notes that if outstanding loans exceed 150% of the limit, a “warning message should be displayed to the user on generation of the instance document”.

Ashvin Parekh, managing partner, Ashvin Parekh Advisory Services, observed the main reason for the outstandings surpassing the sanctions was “temporary accommodation and loans against receivables”.

Parekh explained that at times borrowers approached banks for funds to be able to take delivery of imports. “The customer promises to pay back the amount from receivables so bankers do accommodate such requests,” he said.

Total non-performing assets (NPAs) of the banking system stood at Rs 5.8 lakh crore at the end of March 2016 and total provisions were Rs 1.43 lakh crore.

The central bank has been trying to help banks tackle bad loans by allowing them to convert debt into equity and more recently into convertible redeemable preference shares. However, banks have not been able to find buyers for any of the assets under strategic debt restructuring scheme.

FE had earlier reported that bank loans that aren’t NPAs just yet but could turn toxic amount to over Rs 6 lakh crore or close to 9% of total advances, citing RBI data. The total troubled loans of Rs 6,24,119 crore at the end of December 2015 were 9% higher than the Rs 5, 73,381 crore at the end of June 2015.

While Rs 3,06,180 crore worth of loans were classified in the SMA-1 category where repayments are overdue between 30 and 60 days, another Rs 3,17,939 crore was in the SMA-2 category where repayments are overdue between 60 and 90 days. These Special Mention Accounts follow a fiat from the RBI in 2014 asking banks to put in place a mechanism to red-flag troubled loan accounts early in the day so that these could be dealt with speedily. If the loan is not serviced after 90 days it must be classified as an NPA.

Inter-ministerial body FIPB today cleared six foreign direct investment proposals worth about Rs 180 crore.

Inter-ministerial body FIPB today cleared six foreign direct investment proposals worth about Rs 180 crore.