It already touched a new high of $393.61 billion as on August 11, 2017, and the pace of forex reserves accretion has been the strongest since 2005.

India’s foreign exchange reserves are set to hit the $400-billion mark. It already touched a new high of $393.61 billion as on August 11, 2017, and the pace of forex reserves accretion has been the strongest since 2005.

The gain in the country’s forex reserves has been one of the strongest in Asia in the past 12 months.

India remains among the top-ten countries in forex reserve position and has a comfortable import cover of 12 months, as against the norm of three months.

India’s forex reserves touched an all-time low of $5.8 billion at end of March 1991, which could barely finance three weeks’ worth of imports.

It led the Centre to airlift national gold reserves as a pledge to the IMF in exchange for a loan to cover balance of payment debts.

The rise in forex reserves has been because of robust foreign direct and institutional investment flows, which made the rupee appreciate over 6% since January this year.

As a result of high forex reserves, the Economic Survey volume 2 has highlighted that most reserve-based external sector vulnerability indicators have improved.

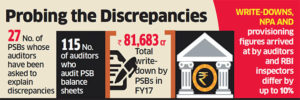

According to RBI data, PSU banks in FY17 have written off Rs 81,683 crore against Rs 2.49 lakh crore in the past five years.

The Reserve Bank of India (RBI) has questioned scores of auditors at 27 public sector banks on the process and logic they had used to compute and report write-downs at the lenders, two people close to the development told ET.

The RBI has sought written explanation on differences in the write-down assessments by its own inspectors and those certified by the auditors. A write-down is a reduction in the estimated and nominal value of an asset, and is charged off as a loss to the profit and loss account for the relevant period. In some cases, the RBI has also questioned the provisioning methodology and non-performing asset (NPA) figures arrived at by the auditors at a few public sector banks, sources told ET.

The banking regulator is examining whether auditors at these state-run lenders followed RBI guidelines on write-downs, provisioning and NPAs. “This is part of RBI’s annual assessment. Auditors will have to explain how they provisioned for NPA and how they calculated write-downs,” said a person aware of the matter.

The write-downs, NPA and provisioning figures arrived at by the auditors and RBI inspectors differ by up to 10%.

WRITE-DOWNS & PROVISIONING

According to RBI data, PSU banks in FY17 have written off Rs 81,683 crore against Rs 2.49 lakh crore in the past five years. In a few cases, the audit reports of some of these lenders do not reflect these write-downs, said one of the persons cited above. Most banks do not separately report write-downs in their accounts, combining them often with quarterly provisioning.

Most Indian public sector banks use more than one auditor due to the enormous size of their balance sheets. Most auditors are mid-to-small Indian firms that audit several branches. The 27 public sector banks collectively employ 115 auditors, according to data analysed by the ET Intelligence Group.

According to the people in the know, auditors at State Bank of India, Punjab National Bank, Bank of Baroda, Canara Bank, Allahabad Bank and Bank of India (BoI) were sent the show-cause notices about two weeks ago.

ET’s detailed email queries to the regulator and the affected lenders – SBI, PNB, BoB, IDBI, Indian Overseas Bank, Canara Bank, BoI, Oriental Bank of Commerce (OBC) and Allahabad Bank – did not elicit any response.

REGULATOR HAS PRIVILEGED ACCESS’

According to a major bank’s auditor who did not wish to be identified, the differences are not unexpected. “The RBI has access to information an auditor may not. Like, if a loan in bank X has gone toxic, the auditor of bank Y may not know, but the RBI would,” he said. He added that there is a time lapse between auditors preparing an account and the RBI conducting inspections. “What you must look at is the impact on the P&L of a bank due to divergence. In most cases, that is not much,” he said.

To be sure, there may have been ‘technical’ errors in interpreting the writedown rules, resulting in the differences. “There is a direct impact of the new accounting standards on the way write-downs are arrived at,” said a senior executive at a top audit firm. “Under the old accounting system, the rules around write-downs were not as precise, and there is a possibility that some auditors may have ignored this.”

To make compliance easy for businesses, the GST Council has allowed businesses to initially file their returns on self-assessment basis in the first two months of the GST rollout.

The first tax returns under the new Goods and Services Tax (GST) regime can be filed from Saturday and the facility will remain open till August 20, GST Network CEO Navin Kumar said today.

Businesses can start filing their first GST returns and pay taxes for July on the portal of GST Network — the IT infrastructure provider for the new indirect tax regime, beginning August 5, he told PTI here.

To make compliance easy for businesses, the GST Council has allowed businesses to initially file their returns on self-assessment basis in the first two months of the GST rollout.

So, the GST returns for July and August will be filed on the Goods and Services Tax Network (GSTN) portal by filling up GSTR 3B form.”We will start the facility of filing interim return form GSTR 3B by August 5 and any registered entity who has transacted business in July will have to file the return by August 20,” Kumar told PTI.

GSTN has tied up with 25 agency banks authorised by the RBI to collect taxes, he said.

“We have tied up with all major banks, both private and public. The facility for tax payment is already on and Integrated GST is being collected. Along with filing of returns by August 20, payments for central and state GST will also come in,” said Kumar, in-charge of the biggest technology backbone created for the new indirect tax regime.

Over 71.30 lakh excise, service tax and VAT payers have migrated to the GSTN portal with 13 lakh fresh registrations.

The final GST returns for July will have to be filed by these businesses by September 5 instead of August 10.

Companies will have to file sale invoice for August with GST Network by September 20 instead of September 10 earlier. The sales returns for September will have to be filed by October 10.

Tough stance taken by govt, RBI makes borrowers cautious

Indian banks are beginning to spot a welcome change in their customers’ behaviour: borrowers who have seen their accounts classified as stressed or non-performing are approaching the lenders with proposals to resolve such accounts in a time-bound manner.

The tough stance taken by the central government and the Reserve Bank of India to end the festering bad loan crisis in the Indian banking sector has caught many borrowers by surprise and they are scrambling to put together resolution plans to avoid harsher penalties including insolvency proceedings, bankers said. Even a couple of months ago, it was difficult to get these clients to the negotiation table.

“I can definitely say that we are in a much better position than even six months ago. We are seeing traction from a section of our borrowers to come up with proposals for resolution of stressed accounts,” said Rajkiran Rai G, managing director and CEO, Union Bank of India. “However, it is too early to say if this is the end of the problem. We will have to see how the discussions shape up,” he added.

Borrowers with outstanding amounts between Rs 500-1,500 crore are the most active in trying to resolve their stressed accounts, and they are looking at various options including scouting for investors and sale of non-core assets, two senior bankers with state-run banks said on conditions of anonymity. A large number of these borrowers are from the steel, power and telecom sectors. Some of the larger corporates with outstanding amounts between Rs 1,500-5,000 crore have also taken initiative to resolve their stressed accounts. On an average, these account for about 50% of the current gross non-performing assets of the banking system, the bankers said.

In June, the RBI’s Internal Advisory Committee (IAC) had said 12 accounts totaling about 25% of the current gross NPA of the banking system would qualify for immediate reference under the Insolvency and Bankruptcy Code (IBC). At present, proceedings against all the 12 accounts are on in various benches of the National Company Law Tribunal across the country. For accounts that do not qualify under the above criterion, IAC had recommended that banks should finalise a resolution plan within six months. “In cases where a viable resolution is not agreed upon within six months, banks should be required to file for insolvency proceedings under IBC,” the RBI had said.

Bad debts at Indian lenders, especially state-run banks, have climbed to a 15-year high and may increase further, a central bank study showed.

Bad debts at Indian lenders, especially state-run banks, have climbed to a 15-year high and may increase further, a central bank study showed. Under the baseline scenario in a “macro stress test,” the industry’s gross bad-loan ratio may increase to 10.2 percent by March 2018 after climbing to 9.6 percent in March 2017, the highest since 2002, according to the Reserve Bank of India’s Financial Stability Report released Friday. Stressed assets, including soured debt and restructured loans, eased slightly to 12 percent in March 2017 from 12.3 percent in September 2016.

Weakness in the Indian banking system is a threat to growth in Asia’s third-largest economy and may stall Prime Minister Narendra Modi’s plan to revive credit growth from near a two-decade low. The soured loans have contributed to a $191 billion pile of zombie debt that’s cast the future of some lenders in doubt and curbed investment by businesses. “The RBI and the government are proactively taking steps to resolve NPA challenges in the banking sector,” Deputy Governor NS Vishwanathan said in a foreword to the report. “We have also activated prompt corrective action to stem the slide in the banking system.”

State-run lenders under performed their peers in the private sector, the report showed, which measures risks to the banking system by tracking factors such as profitability, asset quality and liquidity. Last month, the government gave new powers to the RBI in an effort to clean up the country’s bad-debt mess, which has left banks struggling with billions of rupees in nonperforming loans. The government amended the Banking Regulation Act to enable the RBI to order lenders to initiate insolvency proceedings against defaulters and to create committees to advise banks on recovering their loans.

The RBI in June ordered the banks to use the insolvency courts to find a solution for 12 of the debtors, though it didn’t name the institutions on its list. Earlier in the decade, many Indian steel and construction companies borrowed to fund expansion at a time when the economy was expanding at 9 percent to 10 percent a year. Loans turned sour as that growth slowed, weakening demand for steel used in construction projects.

Foreign exchange reserves touched a record high of $381.96 billion as on June 16, compared $381.16 billion in the previous week, the Reserve Bank of India said in its weekly statistical supplement on Friday. Foreign currency assets (FCAs), the largest component of the foreign exchange reserves, increased to $358.08 billion from $357.28 billion in the previous week, central bank data showed. Expressed in US dollar terms, FCAs include the effects of appreciation/depreciation of non-US currencies, such as the euro, pound and the yen, held in the reserves. So far in 2017, foreign exchange reserves have grown 6% and have touched record levels five times since April, as the RBI has aggressively been buying dollars to prevent a sudden jump in the rupee.

The central bank has been buying dollars on a daily basis, both in the spot market as well as in the forward market, to limit the appreciation of the local currency, which has been gaining steadily, traders said. The rupee has gained about 5% since the beginning of the year. Among other factors, strong demand for the local currency from foreign portfolio investors (FPIs) looking to invest in Indian assets has caused the rupee to appreciate. FPIs have bought Indian shares and bonds worth around $22 billion so far in 2017. Given India’s low current account and fiscal deficits, and the advantage it offers in terms of interest rate differential, traders expect the inflows to continue in the near-term.

The central bank has always maintained that it does not want to influence the exchange rate for the rupee, but would take steps, including intervention in the spot market, to curb extreme volatility. According to the latest available data, the RBI’s outstanding net forward purchases in April stood at $13.55 billion, up from $10.84 billion in the previous month. On the other hand, net purchase in the spot market dropped to $0.57 billion in April from $3.54 billion in March. The RBI publishes data on the sale and purchase of dollar with a lag of two months.

The Reserve Bank of India has widened the scope of its banking ombudsman platform by including issues regarding mis-selling of third-party products, and customer grievances related to mobile banking and electronic banking issues.

The new rule will be effective from July 1, and the banking ombudsmen will enjoy more power in their pecuniary jurisdiction.

Banks sell third-party insurance or MF products to earn a fee, but they were so far not liable to address customer grievances.

Now, the deficiencies arising out of sale of insurance, mutual fund and other third-party products will be looked into.

Banks would now have to take the onus of providing after-sales service on third-party products.

RBI has also simplified the process of making complaints.

Under the amended scheme, a customer would also be able to lodge a complaint against the bank for its non-adherence to RBI instructions with regard to mobile banking and electronic banking services.

The pecuniary jurisdiction of the banking ombudsman to pass an award has been increased from existing, Rs.10 lakh to Rs. 20 lakh.

Ombudsman can direct banks to pay compensation up to Rs. 1 lakh to the complainant for loss of time, expenses incurred as also, harassment and mental anguish suffered.

It led the Centre to airlift national gold reserves as a pledge to the IMF in exchange for a loan to cover balance of payment debts.

It led the Centre to airlift national gold reserves as a pledge to the IMF in exchange for a loan to cover balance of payment debts.