Atmanirbhar economic package: ITR deadline extended to Nov 30, 2020 for FY 2019-20 and tax audit from September 30, 2020 to 31st October 2020.”

The Central Government has extended the all due dates of all Income Tax Returns for the Financial Year 2019-20 amid COVID-19 outbreak.

Due date of all income-tax return for FY 2019-20 will be extended from 31st July, 2020 & 31st October, 2020 to 30th November, 2020 and Tax audit from 30th September, 2020 to 31st October, 2020.

The Finance Minister Nirmala Sitharaman also said that, All pending refunds to charitable trusts and non-corporate businesses & professions including proprietorship, partnership, LLP, and Co-operatives shall be issued immediately.

The Date of assessments getting barred on 30th September, 2020 extended to 31st December, 2020 and those getting barred on 31st March, 2021 will be extended to 30th September, 2021.

The Period of Vivad se Vishwas Scheme for making payment without an additional amount will be extended to 31st December, 2020.

In the union budget 2020, the following section 115BAC shall be inserted in the Income Tax Act, with effect from the 1st day of April, 2021, with new income tax slabs and lower rates. These income tax rates are optional and are available to those who are willing to forego some exemptions and some deductions.

Direct Taxes

1. Tax rate reduced for new companies to 22% and for manufacturing companies 15%

2. New simplified personal tax regime for Individual tax payers. The revised slab can be availed if they do not claim deductions and certain exemptions.

For income :

Upto 5,00,000 nil

Rs 5,00,000 -7,50,000: 10%

Rs 7,50,000 – 10,00,000 : 15%

Rs10,00,000 – Rs 12,50,000 20%

Rs 12,50,000- Rs 15,00,000 : 25%

More than Rs 15,00,000 : 30%

3. Companies not required to deduct dividend distribution tax and will be taxed only in the hands of the recipient. Parent company to be allowed deduction of dividend received subsidiary

4. Concessional tax rate of 15% extended to power generation companies

5. Investment made in Infrastructure and other specified sectors

6. Tax rate of 194LC at 5% for interest payment to non resident in respect of money borrowed or bond issued upto June 30,2023 and for 194LD at 5% for interest on borrowing from foreign institutional or qualified investor and municipal bonds

7. Interest payment on bonds listed on exchange by ILFS – 4%

8. Option to Cooperative societies to pay tax at 22% with no exemption or deduction. Exempt from alternative minimum tax

9. Affordable housing tax breaks extended by one year. Additional 1.5 lakhs tax benefit on interest paid on affordable housing loans to March 2021

10. Turnover threshold for tax audit raised to Rs 5 crore from Rs 1 crore

11. 100% tax concession to sovereign wealth funds on investment in infra projects

12. Income from Charitable institutions fully exempt from taxation. Donation to such institution allowed as deduction.

13. Registration of charity institutions to be made completely electronic, donations made to be pre-filled in IT return form to claim exemptions for donations easily.

14. Faceless appeals against tax orders on lines of faceless assessments

15. For tax payers who have appeals pending only disputed tax is to be paid by tax payer and no interest or penalty if the same is paid within March 31,2020. Post March 31,2020 certain amount levied uptill June 30,2020

16. Startup ESOP taxes deferred by 5 years Other Areas

1. New scheme to provide subordinate debt to MSME

2. Decriminalise some norm violations in Companies Act

3. Increase the bank deposit insurance from Rs 1 lakh to Rs 5 lakh

4. New system for instant allotment of PAN

5. A new scheme NIRVIK to be launched this year itself for exporters

6. A debt ETF consisting of government securities will be launched.

7. For NBFCs and HFCs, liqduity constraints will be addressed.

8. FPI Limit in corporate bonds will be raised to 15% from 9%.

9. LIC to be listed at stock exchanges

Two important changes in Income tax (TDS/TCS)

— TCS to be collected by seller whose turnover exceeds Rs. 10 cr. In previous year from each buyer on amount exceeding 50 lacs @0.1% for sale of goods.

-TDS rate u/s 194J for technical payment changed from 10% to 2% to avoid litigations in respect of 194J Vs 194C

The Central Board of Direct Taxes (CBDT) has decided to extend the deadline for filing of ITRs and Tax Audits Reports by a month. Given the relentless demands by Chartered Accountants (CAs) and tax consultants, the CBDT has given a breather till October 31. It will also provide some respite to smaller companies too, who are struggling with GST filings.

Last night, the CBDT tweeted: “On consideration of representations recd from across the country, CBDT has decided to extend the due date for filing of ITRs & Tax Audit Reports from 30th Sep, 2019 to 31st of Oct, 2019 in respect of persons whose accounts are required to be audited. Formal notification will follow”.

This category of ITR is to be filed by those entities that are assessed under section 44AB of the Income Tax Act such as companies, partnership firms, proprietorship among others and their accounts are to be audited before filing.

The new deadline is also required because the CBDT has been intermittently changing the background software required for filing the ITRs.

There was a change in the ITR 6 software utility. Since all tax-filing is now software-driven, the CBDT will require some time to rework the filing process due to the changes in the software.

The old belief that there would be loss in revenue of the Government, if there is a delay in filing ITRs and Tax Audit Reports is wrong as a considerable share of revenue has already got collected due to Tax Deducted at Source and Advance Tax payments.

Filing ITRs and Tax Audit Reports is primarily an administrative exercise to inform the Income Tax Department about the payable tax. By extending the deadline, there would be no revenue loss to the Government. It will give some relief to the CAs fraternity and smaller companies who are struggling with various tax compliances, he said.

The Central Board of Direct Taxes (CBDT) has further extended due date for filing Income Tax Returns and Audit Reports to October 31st.

The due date for filing of Income Tax Returns and Audit Reports for Assessment Year 2018-19 is 30th September, 2018 for certain categories of taxpayers.

The CBDT had earlier extended the date for filing of Income Tax Returns and various reports of Audit to 15th October 2018.

Upon consideration of representations from various stakeholders, CBDT further extends the ‘due date’ for filing of Income Tax Returns as well as reports of Audit (which were required to be filed by the said specified date) from 15th October, 2018 to 31st October, 2018 in respect of the said categories of taxpayers.

However, as specified in earlier order dated 24.09.2018, assessees filing their return of income within the extended due date shall be liable for levy of interest as per provisions of section 234A of the Income-tax Act, 1961.

The government has extended last date for filing of income tax returns (ITRs) for those taxpayers who are required to file their returns along with audit reports from Sept 30 to Oct 15, 2018.

The text of the notification by CBDT is as below:

CBDT has extended the due date for filing Income Tax Returns and audit reports from 30th September 2018 to 15th October 2018. However, there shall be no extension of the due date for purpose of Explanation 1 to section 234A (Interest for defaults in furnishing return) of the Act and the assessee shall remain liable for payment of interest as per provisions of section 234A of the Act.

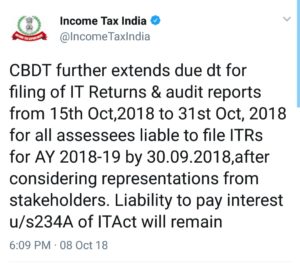

In its tweet, the income tax department has posted – “CBDT extends due date for filing of Income Tax Returns & audit reports from 30th Sept,2018 to 15th Oct, 2018 for all assessees liable to file ITRs for AY 2018-19 by 30.09.2018,after considering representations from stakeholders.”

However, it adds that “Liability to pay interest under section 234A of Income Tax Act will remain.” It is important to note that if one has any unpaid tax liability then penal interest on the same may be leviable.

Typically, tax practitioner bodies ask for an extension from the government, saying they needed more time to file returns for entities where tax audit report or transfer pricing report or other audit reports are required to be filed as per the law.

Even last year, on consideration of representations from various stakeholders and to facilitate ease of compliance by the taxpayers, CBDT had extended the ‘due-date’ for filing Income Tax Returns with audit reports as prescribed under the Income-tax Act,1961 from 31st October, 2017 to 7th November, 2017 for AY 2017-18.

Tax audit is a review of accounts of taxpayers with business or profession from an income tax point of view such as incomes, deduction, compliance with tax laws, etc. Taxpayers with turnover exceeding Rs 1 crore in business (not opted for presumptive taxation scheme) or whose gross professional income is over Rs 50 lakh need to get a tax audit done. Tax audit report needs to be filed on or before the 30 September of the subsequent financial year in case of taxpayers who have not entered into an international transaction.

Some chartered accountants have argued that they have been busy filing returns of individual tax payers like the salaried class till August 30. Consequently they have had little time to devote to preparing the audit reports for those tax payers whose accounts are required to be compulsorily subjected to tax audit. The number of clauses in the audit reports have also increased thereby increasing the time required, they have pointed out. For these reasons they had requested an extension of the deadline for filing tax returns with audit reports.

Highlights:

An audit is a review of accounts of taxpayers with business or profession from an income tax point of view such as incomes, deduction, compliance with tax laws, etc.

Those with turnover exceeding Rs 1 cr in business or whose gross professional income is over Rs 50 lakh need to get a tax audit done.

It is important to note that if one has any unpaid tax liability then penal interest on the same may be leviable.

CBDT confirms News of Income Tax Return filing due date extension in Social Media is Fake

CBDT – extension in due date for non-tax audit cases is fake and there are no such plans to extend this deadline beyond 31st July, 2018

CIRCULAR No.4/2018

F.No.370889/25/2018 Government of India Ministry of Finance Department of Revenue Central Board of Direct Taxes

New Delhi, Dated 21st July, 2018

Order under section 139(1) of the Income-tax Act, 1961 (‘the Act’)

This Circular is issued in pursuant to 139(1) of the Tax Act, 1961 is to clarify that rumorsspreading across in media regarding extension in due date for non-tax audit is fake and no such plans to extend this deadline beyond 31st July, 2018. The department already received over 1 crore returns filed electronically.

As per Section 234F of the Income Tax Act, from 1st April 2018, the penalty for late filing income tax return would be as

(a) five thousand rupees, if the return is furnished on or the 31st day of December of the assessment year;

(b) ten thousand rupees in any other case:

Provided further that if the total income of the person not exceed five lakh rupees, the fee payable under this section shall not exceed one thousand rupees. Therefore, the assessees are hereby asked to file their ITRs before the due date to avoid the penalty.

(Sanyam Suresh Joshi)

DCIT, CBDT

Copy to:

1. PS to FM/OSD to FM/PS to MoS(F)/OSD to MoS(F)

2. PS to Secretary (Revenue)

3. Chairman, CBDT

4. All Members, CBDT

5. All Pr. DGsIT/Pr. CCsIT

6. All Joint Secretaries/CsIT, CBDT

7. Directors/Deputy Secretaries/Under Secretaries of CBDT

8. DIT (RSP&PR)/Systems, New Delhi

9. The C&AG of India (30 copies)

10. The JS & Legal Adviser, Ministry of Law & Justice, New Delhi

11. The Institute of Chartered Accountants of India

12. All Chambers of Commerce

13. CIT (M&TP), Official Spokesperson of CBDT

14. O/o Pr. DGIT (Systems) for uploading on official website

The Union Budget 2018-19 has rationalised the I-T Act provision relating to prosecution for failure to furnish returns.

Seeking to crackdown on shell companies, the government has proposed to remove exemption available to firms with tax liability of up to Rs 3,000 from filing I-T returns beginning next fiscal.

The Union Budget 2018-19 has rationalised the I-T Act provision relating to prosecution for failure to furnish returns.

Thus, a managing director or a director in charge of the company during a particular financial year could be liable for prosecution in case of any lapse in filing I-T returns for any financial year beginning April 1.

“The income tax departments would now track investments by these companies. Also, the focus will be on those firms that show less profit and also those who file I-T returns for the first time,” a senior finance ministry official said.

There are around 12 lakh active companies in the country, out of which about 7 lakh are filing their returns, including annual audited report, with the ministry of corporate affairs. Of this, about 3 lakh companies show ‘nil’ income.

The Section 276CC of the Income Tax Act provided that if a person wilfully fails to furnish in due time the return of income, he shall be punishable with imprisonment and fine.

However, no prosecution could be initiated if the tax liability of an assessee does not exceed Rs 3,000.

The government has amended the provision with effect from April 1, 2018 and removed the exemption available to companies.

“In order to prevent abuse of the said proviso by shell companies or by companies holding benami properties, it is proposed to amend the provisions… so as to provide that the said sub-clause shall not apply in respect of a company,” it said.

The official said that as many as 5 lakh are companies not filing returns and they could be a potential source of money laundering. “These could be small firms which are engaged in honest business, but there could be some which are a potential threat. We have to look into the data.”

Nangia & Co Managing Partner Rakesh Nangia said though the amendment has been brought about to prevent abuse by shell companies/benami properties, checks similar to those placed in the law for invoking GAAR, should be in place to avoid genuine hardship.

“Though the taxman may be driven by compulsions to ensure proper tax compliance, care must be taken while taking such action. In most developing countries, prosecution for tax matters is applied only in cases of serious tax frauds and not in general compliance matters,” Nangia said.

The Budget announcement follows the recommendation of the task force on shell companies, which was set up in February last year.

In the government’s fight against black money, shell companies have come to the fore as they are seen as potential for money laundering.

Till the end of December 2017, over 2.26 lakh companies were deregistered by the MCA for various non-compliances and being inactive for long.

Shell companies are characterised by nominal paid-up capital, high reserves and surplus on account of receipt of high share premium, investment in unlisted companies, no dividend income and high cash in hand.

Also, private companies as majority shareholders, low turnover and operating income, nominal expenses, nominal statutory payments and stock in trade, minimum fixed asset are some of the other characteristics.

Since last year, the Central Board of Direct Taxes (CBDT) — the apex policy making body of the I-T department — has been sharing with the MCA specific information like PAN data of corporates, Income Tax returns (ITRs), audit reports and statement of financial transactions (SFT) received from banks.

In the union budget 2020, the following section

In the union budget 2020, the following section