Insolvency and Bankruptcy Board of India (IBBI) has formulated a Special Resolution Process (SRP) for MSMEs who find their financial position unmanageable due to Covid crisis.

While presenting the ‘Atma Nirbhar Bharat’ package Finance Minister had announced to come out with a Special insolvency resolution framework for MSMEs under section 240A of the Insolvency and Bankruptcy Code.

According to sources close to the development, the scheme would be available to corporate MSMEs, that is, units incorporated as Companies or LLP.

The salient features of the scheme are proposed to be:

— If an MSME finds it unable to meet its financial obligations, the insolvency resolution process could be initiated on the occurrence of default of at least Rs.1 lakh

— It can be triggered by the MSME promoter/ owner only (not by the Financial or other creditors)

— During the process of resolution, the MSME owner remains in control and keeps running the unit but all legal proceedings to take control of assets by creditors are stopped.

— It provides first right of offer to promoters of the MSME to submit resolution plans

— It proposes a simplified claim verification process and preparation of information memorandum

— It expands the scope of interim finance to facilitate rescue financing of the CD during COVID-19 with the approval of 3/4th financial creditors in value.

Federation of Indian Micro and Small & Medium Enterprises (FISME) which facilitated a consultation round of MSME associations with IBBI shared that most participants found the scheme potentially useful.

According to Lucknow based V K Agarwal Managing Director of Shashi Cables Ltd and former FISME President, the scheme seemed to be modelled on insolvency provisions under US chapter-11, was very promising indeed but some way needed to be found to make financial creditors to come on board and cooperate.

The scheme envisages appointment of an Insolvency Professional (IP) as Resolution Professional to conduct the process, with the consent of the unrelated financial creditors having at least 25% of the outstanding financial claims.

The scheme is under final stages of approval and is expected to be announced soon.

The IBBI’s discussion paper said that the processes under the Insolvency and Bankruptcy Code (IBC) require a unique combination of skill sets in terms of subject matter knowledge and management skills for an IP and at different stages of transactions, different sets of skills are called for.

In what may bring about major reform and efficiency in the insolvency regime in India, the Insolvency and Bankruptcy Board of India (IBBI) has proposed to limit the number of cases an insolvency professional can handle to five as it noted that few insolvency professionals (IP) are handling too many cases

In a recent discussion paper, the board noted the “skewed” work allocation and has come up with a matrix for allocation of cases.

Citing observations by courts and tribunals, the paper said: “Keeping in mind the provisions of the Companies Act, 2013, the skewed work allocation amongst the IPs and the observations of the Supreme Court or Adjudicating Authority, and given the expansive and intense responsibilities of an IP in corporate processes, it is proposed to issue necessary guidelines to IPs advising them to limit the maximum number of assignments handled by them, to five, at a given point of time.”

As per the proposed matrix an insolvency resolution professional (IRP) can handle a total of five cases of resolution or liquidation, including voluntary liquidation, wherein the turnover of the corporate debtors is less than or equal to Rs 1,000 crore. As the matrix progresses, an IRP handling the case of a corporate debtor with the turnover of Rs 50,000 crore would be able handle only that very case, and no more.

“On the basis of information available, it is observed that a few IPs are handling too many assignments under the Code, which is detrimental to the institution of IP in the long run,” it noted.

The IBBI’s discussion paper said that the processes under the Insolvency and Bankruptcy Code (IBC) require a unique combination of skill sets in terms of subject matter knowledge and management skills for an IP and at different stages of transactions, different sets of skills are called for.

A spike in one area of expertise will not be sufficient to create a uniform experience for stakeholders. Further, it cannot be ignored that no two IPs possess identical sets of qualification, experience, skills and expertise, it said.

“Similarly, no two CIRPs are same as it involves diverse businesses, complex corporate structures, varied stakeholders. The said restriction on an IP will put a check on undesirable instances of delay and disturbance to the processes led by IPs while simultaneously handling too many assignments under the Code.”

The Board was of the view that with limits in place, quality of output is expected to improve and it will facilitate the realisation of the objective of value maximisation as enshrined in the Code.

The major inputs for violation will be through complaints and therefore, the cost of surveillance for the Board may not be significant. Further, this will be conducive for development of the market for professionals as more talent will be drawn towards IP profession, it added.

The IBBI has sought public comments on the proposal till July 25, 2020.

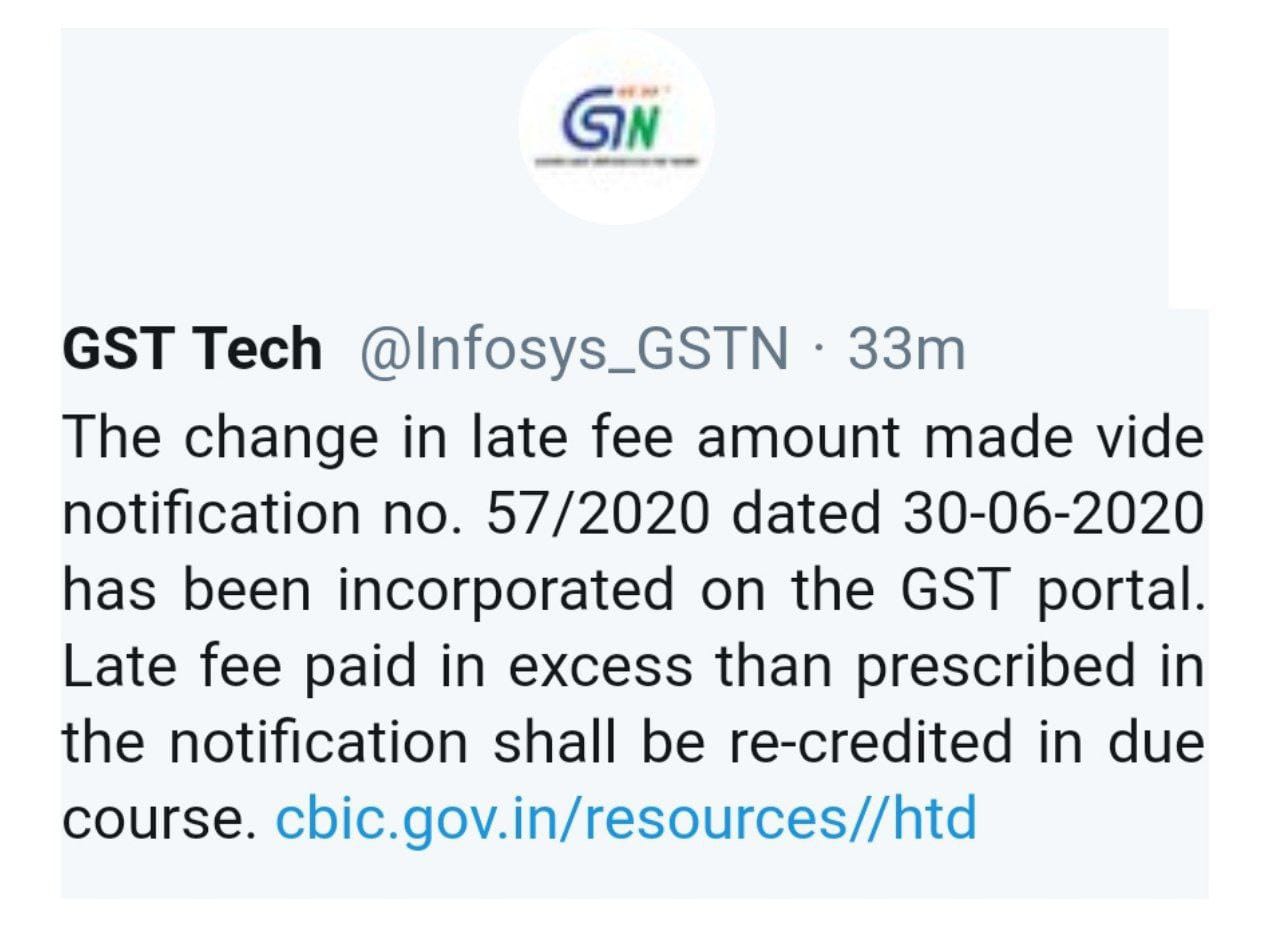

The change in late fee amount made vide notification no. 57/2020 dated 30-06-2020 has been incorporated on the portal. Late fee paid in excess than prescribed in the notification shall be re-credited in due course.

CBIC had vide Noti 57/2020 has stated that that maximum Late Fee for Form GSTR 3B has been capped at Rs. 500 for tax period July 2017 to July 2020 subject to returns being filed before 30th September 2020.

But portal was not updated and it has levied late fees as per old calculation. Hence, GSTN Tech twitter posted that “The change in late fee amount made vide notification no. 57/2020 dated 30-06-2020 has been incorporated on the GST portal.

Late fee paid in excess than prescribed in the notification shall be re-credited in due course.”

[To be published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i)] Government of India Ministry of Finance (Department of Revenue) Central Board of Indirect Taxes and Customs Notification No. 57/2020 – Central Tax

New Delhi, the 30th June, 2020

G.S.R…..(E).— In exercise of the powers conferred by section 128 of the Central Goods and Services Tax Act, 2017 (12 of 2017) (hereafter in this notification referred to as the said Act), read with section 148 of the said Act, the Government, on the recommendations of the Council, hereby makes the following further amendments in the notification of the Government of India in the Ministry of Finance (Department of Revenue), No. 76/2018– Central Tax, dated the 31st December, 2018, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub- section (i) vide number G.S.R. 1253(E), dated the 31st December, 2018, namely :–

In the said notification, after the third proviso, the following provisos shall be inserted, namely: –

“Provided also that for the class of registered persons mentioned in column (2) of the Table of the above proviso, who fail to furnish the returns for the tax period as specified in column (3) of the said Table, according to the condition mentioned in the corresponding entry in column (4) of the said Table, but furnishes the said return till the 30th day of September, 2020, the total amount of late fee payable under section 47 of the said Act, shall stand waived which is in excess of two hundred and fifty rupees and shall stand fully waived for those taxpayers where the total amount of central tax payable in the said return is nil:

Provided also that for the taxpayers having an aggregate turnover of more than rupees 5 crores in the preceding financial year, who fail to furnish the return in FORM GSTR-3B for the months of May, 2020 to July, 2020, by the due date but furnish the said return till the 30th day of September, 2020, the total amount of late fee under section 47 of the said Act, shall stand waived which is in excess of two hundred and fifty rupees and shall stand fully waived for those taxpayers where the total amount of central tax payable in the said return is nil.”.

2. This notification shall be deemed to have come into effect from the 25th day of June, 2020.

[F. No. CBEC-20/06/08/2020-GST]

(Pramod Kumar)

Director, Government of India

Note: The principal notification No. 76/2018-Central Tax, dated 31st December, 2018 was published in the Gazette of India, Extraordinary, vide number G.S.R. 1253(E), dated the 31st December, 2018 and was last amended vide notification number 52/2020 – Central Tax, dated the 24th June, 2020, published in the Gazette of India, Extraordinary, Part II, Section 3, Sub-section (i) vide number G.S.R.405 (E), dated the 24th June, 2020.

The levy is applicable only for large cash withdrawals. The intent is to minimize cash transactions and expand digital payments to enlarge the ambit of organized transactions over time.

In order to tighten the noose on those who don’t file income tax returns (ITR) despite earning taxable income and discourage cash transactions, the Finance Act 2020 introduced higher TDS (Tax Deducted at Source) rates on cash withdrawals for those who do not file ITR. The rates are applicable from 1 July.

Those who haven’t filed ITR for the past three financial years will have to pay TDS at the rate of 2%, if the amount withdrawn from the bank is above ₹20 lakh but doesn’t exceed ₹1 crore in a financial year. If the amount withdrawn exceeds ₹1 crore, TDS will be deducted at the rate of 5% under Section 194N of the Income-tax Act, 1961, for those who do not file ITR.

However, if you withdraw cash above ₹1 crore in a FY, you will still have to pay TDS whether you file ITR or not. In July 2019, the government, through Section 194N, had first introduced TDS at the rate of 2% on cash withdrawals above ₹1 crore in a financial year. This continues to be applicable.

“It is important to note that TDS shall be required to be deducted only when the aggregate amount of cash withdrawal during the FY by an individual from one or more of his bank accounts exceeds ₹20 lakh or ₹1 crore, as the case may be,” said Parizad Sirwalla, partner and head, global mobility services, tax, KPMG in India.

Further, tax will be deducted only on the amount exceeding the said thresholds. “If the individual withdraws a sum of money on regular intervals, the bank or financial institution will have to deduct TDS from the amount once the total sum withdrawn exceeds the threshold in a FY,” said Sirwalla.

For example, if person A has filed his ITR and if he withdraws cash up to ₹1 crore, then no TDS will be applicable. In case person A withdraws cash, which is more than ₹1 crore, then only 2% TDS will be applicable. If person A has withdrawn ₹1.25 crore in two transaction of ₹75 lakh in and ₹50 lakh, the TDS liability will only be on the excess amount that is ₹25 lakh.

On the other hand, if person B has not filed his ITR for the last three financial years and if he withdraws cash between ₹20 lakh and ₹1 crore, then 2% TDS will be applicable. In case person B withdraws cash which is more than ₹1 crore, then 5% TDS will be applicable.

“In case, the individual does not furnish the PAN to the bank or financial institution, then a TDS at a higher rate of 20% will become applicable,” said Sirwalla.

TDS will be applicable on withdrawals from banks, co-operative banks and post offices. The limit will apply on all accounts in the same bank. So, if you have multiple accounts with the same bank, then TDS will be applicable once you breach the mandatory limit across all the accounts or in any one of the account with the same bank. But for accounts with different banks, the limit will apply separately.

Banks will need to keep track of cash withdrawals and once the limit is breached, they will need to deduct TDS.

“Banks are asking declaration from people to ensure they have filed a return in the past three years or in any one of the last three years. This is done by banks for easier tracking as they wouldn’t know if the person has filed ITR or not,” said Sandeep Sehgal, director, taxes and regulatory, AKM Global.

The purpose of slapping this TDS is to minimize cash transactions and push digital payments.

“The levy is applicable only for large cash withdrawals in excess of ₹20 lakh/100 lakh per annum, as the case may be. The intent is to minimize cash transactions and expand digital payments to enlarge the ambit of organized transactions over time. So if individuals need to avoid this TDS levy, they should ensure that their cash withdrawals are restricted to the bare minimum and that the bulk of their payments happen through banking or digital means,” said Divakar Vijayasarathy, founder and managing partner, DVS Advisors LLP.

The Government has also extended PAN-Aadhaar linking deadline.

In view of the challenges faced by taxpayers in meeting the statutory and regulatory compliance requirements across sectors due to the outbreak of Novel Corona Virus (COVID-19), the Government brought the Taxation and Other Laws (Relaxation of Certain Provisions) Ordinance, 2020 [the Ordinance] on 31st March, 2020 which, inter alia, extended various time limits.

In order to provide further relief to the taxpayers for making various compliances, the Government has issued a Notification on 24th June, 2020, the salient features of which are as under:

I. The time for filing of original as well as revised income-tax returns for the FY 2018-19 (AY 2019- 20) has been extended to 31st July, 2020.

II. Due date for income tax return for the FY 2019-20 (AY 2020-21) has been extended to 30th November, 2020. Hence, the returns of income which are required to be filed by 31st July, 2020 and 31st October, 2020 can be filed upto 30th November, 2020. Consequently, the date for furnishing tax audit report has also been extended to 31st October, 2020.

III. In order to provide relief to small and middle-class taxpayers, the date for payment of self-assessment tax in the case of a taxpayer whose self-assessment tax liability is upto Rs. 1 lakh has also been extended to 30th November, 2020. However, it is clarified that there will be no extension of date for the payment of self-assessment tax for the taxpayers having self-assessment tax liability exceeding Rs. 1 lakh. In this case, the whole of the self-assessment tax shall be payable by the due dates specified in the Income-tax Act, 1961 (IT Act) and delayed payment would attract interest under section 234A of the IT Act.

IV. The date for making various investment / payment for claiming deduction under Chapter-VIA-B of the IT Act which includes section 80C (LIC, PPF, NSC etc.), 80D (Mediclaim), 80G (Donations) etc. has also been further extended to 31st July, 2020. Hence the investment / payment can be made upto 31st July, 2020 for claiming the deduction under these sections for FY 2019-20.

V. The date for making investment / construction/ purchase for claiming roll over benefit / deduction in respect of capital gains under sections 54 to 54GB of the IT Act has also been further extended to 30th September, 2020. Therefore, the investment / construction/ purchase made up to 30th September, 2020 shall be eligible for claiming deduction from capital gains.

VI. The date for commencement of operation for the SEZ units for claiming deduction under section 10AA of the IT Act has also been further extended to 30th September, 2020 for the units which received necessary approval by 31st March, 2020. VII.

VII. The furnishing of the TDS/ TCS statements and issuance of TDS/ TCS certificates being the prerequisite for enabling the taxpayers to prepare their return of income for FY 2019-20, the date for furnishing of TDS/ TCS statements and issuance of TDS/ TCS certificates pertaining to the FY 2019-20 has been extended to 31st July, 2020 and 15th August, 2020 respectively.

VIII. The date for passing of order or issuance of notice by the authorities and various compliances under various Direct Taxes & Benami Law which are required to be passed/ issued/ made by 31st December, 2020 has been extended to 31st March, 2021. Consequently, the date for linking of Aadhaar with PAN would also be extended to 31st March, 2021.

IX. The reduced rate of interest of 9% for delayed payments of taxes, levies etc. specified in the Ordinance shall not be applicable for the payments made after 30th June, 2020. The Finance Minister has already announced extension of date for making payment without additional amount under the “Vivad Se Vishwas” Scheme to 31st December 2020, necessary legislative amendments for which shall be moved in due course of time. The said Notification has extended the date for the completion or compliance of the actions which are required to be completed under the Scheme by 30th December, 2020 to 31st December, 2020. Therefore, the date of furnishing of declaration, passing of order etc under the Scheme stand extended to 31st December, 2020

Deferment of the implementation of new procedure for approval/ registration/ notification of certain entities u/s 10(23C), 12AA, 35 and 80G of the IT Act has already been announced vide Press Release dated 8th May, 2020 from 1st June, 2020 to 1st October, 2020. It is clarified that the old procedure i.e. pre-amended procedure shall continue to apply during the period from 1st June, 2020 to 30th September, 2020. Necessary legislative amendments in this regard shall be moved in due course of time.

The Finance Minister has already announced reduced rate of TDS for specified non-salaried payments to residents and specified TCS rates by 25% for the period from 14th May, 2020 to 31st March, 2021. The announcement was also followed by the Press Release dated 13th May, 2020. The necessary legislative amendments in this regard shall be moved in due course of time

Government banks, including 1,482 urban cooperative banks and 58 multi-state cooperative banks, are now being brought under the supervisory powers of the RBI. RBI’s powers will also apply to the cooperative banks as they apply to scheduled banks.

The Union Cabinet on Wednesday decided to bring all co-operative banks under the Reserve Bank of India through an ordinance. This was announced by Union information and broadcasting minister Prakash Javadekar during a virtual press conference.

“Government banks, including 1,482 urban cooperative banks and 58 multi-state cooperative banks, are now being brought under supervisory powers of Reserve Bank of India (RBI),” Javadekar said today. These banks will come under the supervision of RBI with immediate effect from date of President’s approval on the ordinance.

After the Punjab and Maharashtra Cooperative (PMC) Banks fiasco last year, the Union Cabinet in February amended Banking Regulation Act to strengthen the cooperative banks in the country. During Budget 2020, Finance Minister Nirmala Sitharaman also announced that cooperative banks will be brought under the ambit of RBI.

There are more than 8.6 crore depositors in over 1,500 urban and multi-state cooperative banks across the country. “Depositors’ money amounting to ₹4.84 lakh crore in the cooperatives banks will stay safe,” Javadekar said while announcing the decision.

The government also announced to provide 2% interest subvention to borrowers under the ‘Shishu’ category of the flagship Pradhan Mantri MUDRA Yojana (PMMY). Under the Shishu category, collateral free loans of up to ₹50,000 will be given to beneficiaries.

“The Union Cabinet has approved the scheme for interest subvention of 2% to Shishu loan category borrowers under PMMY, outstanding as on March 31, 2020, for a period of 12 months to eligible borrowers,” Javadekar said.

Launched in 2015, the Pradhan Mantri MUDRA Yojana provides loans up to ₹10 lakh to non-corporate, non-farm small/micro enterprises. These loans are classified as MUDRA loans under PMMY. Commercial banks, RRBs, small finance banks, MFIs and NBFCs provide MUDRA loans.

In the wake of coronavirus outbreak, the central government decided to extend the tenure of the OBC Commission by six months, Union minister Prakash Javadekar said. The government also announced ₹15,000-crore infrastructure fund to provide interest subvention of up to 3% to private players for setting up of dairy, poultry and meat processing units.

“A fund worth ₹15,000 crore has been approved by the Cabinet that will be open to all and will help in increasing milk production, boost exports and create 35 lakh jobs in the country,” Javadekar told.

• The extension is applicable to both deposits as well as debentures maturing this fiscal • The extension is given in view of the requests received from various stakeholders seeking more time on account of covid-19 • The move comes at a time when businesses are struggling with a weak balance sheet after the national lockdown

The government has given a three-month extension to companies to set aside a part of the deposits and debentures maturing in FY21 in a dedicated account, a statutory requirement under the Companies Act.

The Ministry of Corporate Affairs (MCA) said in a circular that the due date of April end, which was extended till end of June in a circular in March, has been further extended till end of September, 2020.

The circular, signed on Friday, said the extension was given in view of the requests received from various stakeholders seeking more time on account of covid-19.

The extension is applicable to both deposits as well as debentures maturing this fiscal. The Companies (Share Capital and Debentures) Rules of 2014 said every company needs to set up a Debenture Redemption Reserve before end of April every year and deposit in that not less than 15% of the debentures maturing in that year. This investment could be in the form of bank deposits or central and state government securities or specified corporate bonds.

Similarly, companies accepting deposits from its members have to deposit not less than 20% of such deposits maturing in a financial year and in the subsequent financial year in a scheduled bank in a separate account called deposit repayment reserve account. For this requirement under the Companies Act too, the government had in March given three months extra time till end of June. Due dates for both the requirements now stand extended till end of September, 2020.

The move comes at a time when businesses are struggling with a weak balance sheet after the national lockdown to check the spread of coronavirus infections wiped out two months of business. The government’s over ₹20 trillion stimulus package relied mostly on bank credit to businesses rather than on more upfront measures.

The Ministry of Corporate Affairs (MCA) has in the last few months taken a series of steps that will reduce the compliance burden and lower the cost of capital for businesses.

Insolvency and Bankruptcy Board of India (IBBI) has formulated a Special Resolution Process (SRP) for MSMEs who find their financial position unmanageable due to Covid crisis.

Insolvency and Bankruptcy Board of India (IBBI) has formulated a Special Resolution Process (SRP) for MSMEs who find their financial position unmanageable due to Covid crisis.