ICAI have launched Unique Document Identification Number (UDIN) facility which is a unique number, which will be generated by the system for every document certified/ attested by a Chartered Accountant and registered with the UDIN portal available at https://udin.icai.org/ with effect from 1st July 2018.

It has been noticed that financial statements and documents were being certified/attested by third persons, in lieu of Chartered Accountants. As these statements are being relied upon by the authorities as true statements and certificates, UDIN can be generated by a practicing CA by registering his/her documents/ certificates on UDIN Portal for verification.

A practicing Chartered Accountant can generate a UDIN for certificate/ document attested by him either in individual capacity or as a partner.

At present, this facility is recommendatory. But ICAI is mulling to make the same compulsory in near future, so as to curb the menace of fake or forged documents.

No change is possible in the data already registered by a Chartered Accountant in the online system. Therefore, members are requested to thoroughly check the details in preview option before submission of their application.

Information filled in can be edited/ modified any number of times before the submission. But once it is submitted, it cannot be edited.

The UDIN once generated can be withdrawn or cancelled with narration. Hence if any user search for this UDIN, appropriate narration indicated by Member with the date of revoke will be displayed for reference.

The Securities and Exchange Board of India (Sebi) on Thursday eased several rules relating to Initial Public Offers (IPO), rights issues, buybacks and takeovers. The regulator’s board approved these changes as also those relating tenures of managing directors of market intermediaries. The capital markets watchdog reduced the time for announcing the price band of initial […]The Securities and Exchange Board of India (Sebi) on Thursday eased several rules relating to Initial Public Offers (IPO), rights issues, buybacks and takeovers.

The regulator’s board approved these changes as also those relating tenures of managing directors of market intermediaries. The capital markets watchdog reduced the time for announcing the price band of initial public offers (IPO) from five working days before the opening of the issue to two working days. This will give companies more time to fix the price band.

Companies now need to provide investors with financial disclosures — for public issues and rights issues — for only three years. Currently, information is provided in the offer documents for five years. Also, companies need to provide only consolidated audited financial disclosures in the IPO offer document; audited standalone financials of the issuer and subsidiaries must be disclosed on the company website.

Following a board meeting on Thursday, the capital markets regulator tweaked the buyback norms. The buyback period has been defined as the time between the board resolution or the date of declaration of results for a special resolution authorizing the buyback of shares and the day on which the shares are paid.

Also, Sebi has amended the takeover rules. It has given companies additional time to revise the open offer price upwards till one working day before the start the tendering period.

The Sebi board also approved some recommendations of R Gandhi committee on regulations relating to market infrastructure institutions (MIIs). For rights issues the threshold for submission of the draft letter of offer to Sebi has been increased to Rs.10 crore as against the earlier prescribed Rs 50 lakh. The regular also tweaked the rules relating to the underwriting of all non-SME public issues. If 90% of the fresh issue of share is subscribed, the underwriting will be restricted to that portion only. Accordingly, the requirement to underwrite 100% of the issue without regard to the minimum subscription requirements has been deleted.

Sebi also reduced minimum anchor investor size to Rs 2 crore from the existing Rs 10 crore, for SME issuances. This will allow companies to attract more anchor investors for an issue.

The board has permitted eligible domestic and foreign entities to hold up to 15% shareholding in case of Depository and Clearing Corporation. Moreover, multilateral and bilateral financial institutions, as notified by the government, have also been recommended to hold up to 15% in an MII. Moreover, Sebi has decided to limit the tenure of managing directors of an MII for a for a maximum of two terms of up to 5 years each or up to 65 years of age, whichever is earlier. The requirement would also apply to incumbent MDs of MIIs.

The regulator is also looking into the issues regarding IPO ICICI Securities in ICIC AMC bought the large stake.The regulator had sought details of a significant investment made by ICICI Prudential Mutual Fund in the IPO of ICICI Securities. “Yes we are looking into that, and we have sought some information from them, and we are yet to get their replies,” Tyagi said.

Last week, the Parliament cleared a bill to further amend the Companies Act.

The financial statements and annual returns of all company must be filed on time with the ROC / MCA each year. As per Companies Act, 2013, non-filing of annual return is an offence, consequences of which affect the directors, as well as the company.

Hence, it is a must for every company to file with the MCA:

1. The annual return within 60 days of the Annual General Meeting and

2. The Financial Statement, within 30 days of the Annual General Meeting.

The various consequences and the penalties for not filing annual return of a company (Forms MGT-7 & AOC-4) are highlighted here.

A. Consequences – for Directors

The Directors of a company are responsible for ensuring the compliance of the company with all applicable rules and regulations. When a company defaults on compliance or dues payable, the Directors are held responsible for the default. The following are penal consequences for a Director of a company for default of non-filing of the Annual Return.

Director Disqualification

In case a company has not been filed its Annual Return for three continuous financial years, then every person who has been a director or is currently the director of the specific company could be disqualified under the Companies Act, 2013. If a Director is disqualified, his/her DIN would become inactive and the person would not be eligible to be appointed as a Director of any company for a period of five years from the date of disqualification. Further, disqualified Directors would not also be allowed to incorporate another company for a period of five years.

Fine & Imprisonment

A director of the company can be punished if the company has not been filed even after 270 days from the date when the company should have originally filed with additional penalty. Any Director who has defaulted in the filing of annual return of a company can also be penalized with an imprisonment of a term extended up to six months or with a fine of an amount not lesser than fifty thousand rupees and it might extend up to five lakh rupees, or with both imprisonment and fine. However, this provision provided under the Companies Act, 2013 is rarely used.

In addition, if any information filed by a Director or any other person in the annual return is false by any nature or if he/she failed to mention any fact or material that is true can be punished with imprisonment for a term which is not lesser than six months and which could extend up to 10 years. Further, he/she can also be liable for payment of a fine which is not lesser than the amount subject to the fraud involved and it may extend to an amount three times of the sum concerned with the fraud.

B. Consequences of Default – For Company

The following are some of the penal consequences for a company that has not filed its annual return:

Penalty

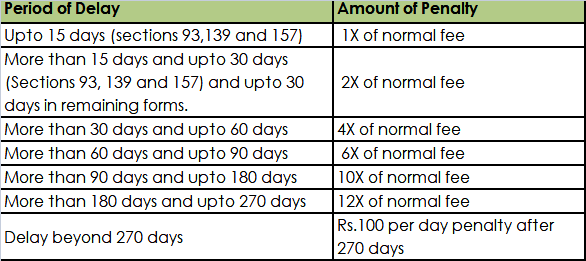

Normally, the Government fee for filing or registering any document under the Companies Act required or authorized to be filed with the Registrar is Rs.200. A private limited company would be required to file form MGT-7 and form AOC-4 each year and the government fee applicable if filed on time would be Rs.400. In case of delay in filing of annual return, the penalty as mentioned would be applicable:

The penalty for not filing a company’s annual return (Form MGT-7 and Form AOC-4) is increased to Rs.100 per day w.e.f.July 1, 2018.

Strike-Off

In case the company has not filed its Annual Return for the last two financial years continuously, then such companies would be termed as an “inactive company”. On such a classification, the bank account of the company could be frozen. Further, the Registrar could also issue a notice to the Company and initiate strike-off of the company from the MCA records.

In case you need any assistance to file annual return for your company, you can contact us at Director@Sunkrish.com

The Union Budget 2018-19 has rationalised the I-T Act provision relating to prosecution for failure to furnish returns.

Seeking to crackdown on shell companies, the government has proposed to remove exemption available to firms with tax liability of up to Rs 3,000 from filing I-T returns beginning next fiscal.

The Union Budget 2018-19 has rationalised the I-T Act provision relating to prosecution for failure to furnish returns.

Thus, a managing director or a director in charge of the company during a particular financial year could be liable for prosecution in case of any lapse in filing I-T returns for any financial year beginning April 1.

“The income tax departments would now track investments by these companies. Also, the focus will be on those firms that show less profit and also those who file I-T returns for the first time,” a senior finance ministry official said.

There are around 12 lakh active companies in the country, out of which about 7 lakh are filing their returns, including annual audited report, with the ministry of corporate affairs. Of this, about 3 lakh companies show ‘nil’ income.

The Section 276CC of the Income Tax Act provided that if a person wilfully fails to furnish in due time the return of income, he shall be punishable with imprisonment and fine.

However, no prosecution could be initiated if the tax liability of an assessee does not exceed Rs 3,000.

The government has amended the provision with effect from April 1, 2018 and removed the exemption available to companies.

“In order to prevent abuse of the said proviso by shell companies or by companies holding benami properties, it is proposed to amend the provisions… so as to provide that the said sub-clause shall not apply in respect of a company,” it said.

The official said that as many as 5 lakh are companies not filing returns and they could be a potential source of money laundering. “These could be small firms which are engaged in honest business, but there could be some which are a potential threat. We have to look into the data.”

Nangia & Co Managing Partner Rakesh Nangia said though the amendment has been brought about to prevent abuse by shell companies/benami properties, checks similar to those placed in the law for invoking GAAR, should be in place to avoid genuine hardship.

“Though the taxman may be driven by compulsions to ensure proper tax compliance, care must be taken while taking such action. In most developing countries, prosecution for tax matters is applied only in cases of serious tax frauds and not in general compliance matters,” Nangia said.

The Budget announcement follows the recommendation of the task force on shell companies, which was set up in February last year.

In the government’s fight against black money, shell companies have come to the fore as they are seen as potential for money laundering.

Till the end of December 2017, over 2.26 lakh companies were deregistered by the MCA for various non-compliances and being inactive for long.

Shell companies are characterised by nominal paid-up capital, high reserves and surplus on account of receipt of high share premium, investment in unlisted companies, no dividend income and high cash in hand.

Also, private companies as majority shareholders, low turnover and operating income, nominal expenses, nominal statutory payments and stock in trade, minimum fixed asset are some of the other characteristics.

Since last year, the Central Board of Direct Taxes (CBDT) — the apex policy making body of the I-T department — has been sharing with the MCA specific information like PAN data of corporates, Income Tax returns (ITRs), audit reports and statement of financial transactions (SFT) received from banks.

Qualified accounts can be flagged on the ministry’s portal, thereby, helping regulators to keep a check on suspicious entities

The ministry of corporate affairs (MCA) says work has begun for an “early warning system” regarding shell companies.

The term is used to refer to a company without active business operations or much of assets. This by itself isn’t illegitimate but they could be used as a manoeuvre for financial operations of a suspect or illegitimate nature.

Currently, there is no way to check shell companies systemically, an official said. Chartered accountants (CAs) do come out with qualified accounts of such companies but these come in a random way on the ministry’s MCA21 portal. Qualified accounts refer to bits of information about which CAs have doubts or disagreement with the audited entity’s management.

After the hoped-for early warning system comes, qualified accounts would be flagged on the ministry’s portal, helping it and other regulators to check on such entities. “We are yet to work out the nitty gritty of this system but are on the job,” another official said.

He said this would do away with the current system of random inspections to identify such companies. The portal will have filings by CAs in such a way that regulators will be alerted, he said.

Earlier, minister of state for corporate affairs P P Chaudhary had said the government would try to use the information technology tool of artificial intelligence in this regard.

CAs told Business Standard that an early warning system by itself wouldn’t change things by much. There should also be stringent norms to make auditors more independent. One of them said it is a company’s promoters who appoint the auditor, which means the latter does not retain the independence to openly report facts. So, a CA’s appointment would need to move away from promoters.

The ministry had recently issued rules to limit the number of subsidiaries a company may have — no more than two layers. This will apply prospectively but existing companies have to disclose details of their entire list of subsidiaries to the registrar of companies within 150 days. Banks and insurance companies are excluded from this rule.

With no limit on the number of subsidiaries, regulators found it difficult to track illicit transactions.

The income tax (I-T) department and the Ministry of Corporate Affairs (MCA) have signed a pact to regularly share data, including PAN and audit reports of firms, to crack down on shell companies, the government said on Thursday.

The pact aims at curbing the menace of money laundering, black money, and misuse of corporate structure by shell companies, a finance ministry statement said. It added a memorandum of understanding for Automatic and Regular Exchange of Information was signed between the MCA and the Central Board of Direct Taxes (CBDT) on September 6 and took effect the same day.

Under the pact, tax authorities will now relay audit reports of corporate entities and specific information from their I-T returns, along with PAN data, to the MCA.

Besides, financial statements filed by corporate entities with the Registrar of Companies, returns of allotment of shares, and statements of financial transactions received from banks will now be shared between the two departments.

“A data-exchange steering group has also been constituted for the initiative. It will meet periodically to review the data exchange status and take steps to further improve the effectiveness of the two agencies,” the finance ministry added.

The MoU will ensure that both the MCA and the CBDT have seamless PAN-CIN (corporate identity number) and PAN-DIN (director identity number) linkage for regulatory purposes.

“The information shared will pertain to both Indian firms as well as foreign ones operating in India,” the statement said.

The data will also be shared for the purpose of carrying out scrutiny, inspection, investigation and prosecution.

The government has already said that about 100,000 directors will be disqualified for their association with shell companies. The MCA is in the process of cancelling the registration of 209,000 companies that have not been carrying out business activities for a long period. Besides, banks have been asked to restrict operations of these companies’ bank accounts by their directors or their authorised representatives.

Following deregistration of over 200,000 companies, currently there are about 1.1 million companies with active status.

Rakesh Nangia, managing partner, Nangia & Co, said, “Seamless exchange of information on PAN records and audit report between the MCA and the CBDT will equip the government to crack down on shell companies, thereby cleaning the economy of devices used for generating and circulating the menace of black money.”

Abhishek Goenka of PwC sought to caution the authorities that the data should be used with adequate safeguards, and does not become a basis for blanket notices.

Prior to this, the government had identified over 100,000 directors for disqualification. These directors have been associated with shell companies. The MCA has put the SFIO on the job to investigate these directors.

The MCA is in the process of cancelling the registration of 209,000 companies that have not been carrying out business activities for a long period. Besides, banks have been asked to restrict operations of these companies’ bank accounts by their directors or their authorised representatives.

Tax payers who were supposed to file their income tax returns by September 30 now have some more time on their hands. The government has extended the deadline to file income tax returns for such tax payers until October 31.

“The ‘due-date’ for filing Income Tax Returns and various reports of audit prescribed under the Income-tax Act,1961 has been extended from 30th September, 2017 to 31st October, 2017 for all taxpayers who were liable to file their Income Tax Returns by 30th September, 2017,” Ministry of Finance said.

This time tax payers will have to quote their 12-digit Aadhaar number or the 28-digit Aadhaar enrolment number while filing the income tax return.

You will have to keep the Form 16, which you got from their employer handy. If you don’t have it, get it asap. Download the Form 26AS from the Income Tax e-filing website. Form 26AS is a consolidated tax statement which states tax credit statement of all taxes received by the Income Tax Department against your PAN number. You will need it to tally with your Form 16.

Availability of the detail of bank accounts in which the refund is to be credited is a precondition for direct credit of refund in bank accounts. Refund generated on processing of return of income is currently credited directly to the bank accounts of the tax-payers. Non-residents, who are claiming refund but do not have bank accounts in India may furnish details of one foreign accounts in ITR for issuance of refund.

Bank accounts details

A tax payer is also required to disclose his/her bank account number along with the IFSC code. However, dormant accounts which have been in use for the past three years or more need not to be mentioned.

Due-date for filing Income Tax Returns & various reports of audit prescribed under the IT Act,1961 has been extended to October 31, 2017.

According to the Income Tax Department now, tax payers have to disclose information of cash deposited in their bank account aggregating to Rs 2 lakh from November 11 to 30 December, 2016.

Ensure that ITR is compliant with amount deposited in bank accounts during the period of demonetisation

Besides that, if any assessee has any unexplained income or investments, he has to report such unexplained income in the new ITR forms and such amount will be taxable at the tax rate of 60 percent plus surcharge and cess.

Tax deductions

If you are claiming tax deductions under 80C, you should keep the following details handy:

Investment details (eg: LIC, PPF, NSC)

Home loan

LTA

Medical

Consequences of Late filing of Return

According to ClearTax, if there are any taxes which are unpaid, penal interest at 1 per cent per month or part thereof will be charged till the date of payment of taxes .Also Penalty of Rs 5,000 may be charged. The penalty is not levied in all cases and depends upon the circumstances of the case.

For returns of FY 2017-18 and onwards, penalty of Rs 5,000 will be charged for returns filed after due date but before 31st December. If returns are filed after 31st December, a penalty of Rs 10,000 shall apply. However, penalty will be Rs 1,000 for those with income upto Rs 5 lakh.

Who has to file?

Every person whose gross total income exceeds the taxable limit must file an Income Tax Return (ITR)

Who has to file?

Every person whose gross total income exceeds the taxable limit must file an Income Tax Return (ITR)

Who has to e-file?

Individuals & HUF having total income exceeding Rs 5 lakh or claiming any refund in the return (excluding individuals of the age of 80 years or more who are furnishing return in Form no. ITR-1 or ITR-2).

Individual or HUF, being a resident other than not ordinarily resident, having any foreign asset/income or claiming any foreign tax relief.

ICAI have launched Unique Document Identification Number (UDIN) facility which is a unique number, which will be generated by the system for every document certified/ attested by a Chartered Accountant and registered with the UDIN portal available at https://udin.icai.org/ with effect from 1st July 2018.

ICAI have launched Unique Document Identification Number (UDIN) facility which is a unique number, which will be generated by the system for every document certified/ attested by a Chartered Accountant and registered with the UDIN portal available at https://udin.icai.org/ with effect from 1st July 2018.

He said this would do away with the current system of random inspections to identify such companies. The portal will have filings by CAs in such a way that regulators will be alerted, he said.

He said this would do away with the current system of random inspections to identify such companies. The portal will have filings by CAs in such a way that regulators will be alerted, he said.