Weak asset quality will continue to plague credit profile of banks, with their profitability remaining under pressure till the next fiscal, says a report.

Weak asset quality will continue to plague credit profile of banks, with their profitability remaining under pressure till the next fiscal, says a report.

“Asset quality will remain a negative driver of the credit profiles of most rated banks in the country and the stock of impaired loans. Non-performing loans and standard restructured loans will still rise during the horizon of our outlook that lasts till the next financial year,” Alka Anbarasu, a vice-president and senior analyst at Moody’s, said in a report today.

The report is jointly penned by Moody’s and its domestic arm ICRA Ratings.

The report said the pressure on asset quality largely reflects the system’s legacy problems, as relating to the strong credit growth seen in 2009-12, when corporate investments rose significantly.

It, however, said aside from the legacy issues, the underlying asset trend for banks will be stable because of a generally supportive operating environment.

“While corporate balance sheets stay weak, a further deterioration in key credit metrics such as debt/equity and interest coverage ratios has been arrested,” the report said.

As per Karthik Srinivasan, a senior vice-president at ICRA, “while bank profitability is not expected to be as weak as the levels seen in the financial year 2015-16, the weakness in asset quality will continue to drag on profitability indicators, with return on equity remaining in the single digits for the financial years 2016-17 and 2017-18.”

Anbarasu said the pace of asset quality deterioration over the next 12-18 months should be lower than what was seen over the last five years, and especially compared to the financial year 2015-16.

She considers the Reserve Bank’s asset quality review in December 2015 as an important catalyst in pushing banks to recognise some large accounts as being impaired.

“We now estimate the ‘true’ level of impaired loans for Indian banks to be around 1-1.5 percentage points higher than the latest reported numbers,” Anbarasu said.

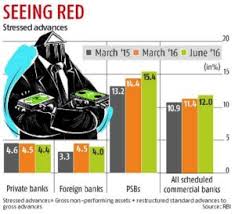

The latest Financial Stability Report by the RBI had said the gross non-performing advances ratio increased to 9.1 per cent from 7.8 per cent between March and September 2016, pushing the overall stressed advances ratio to 12.3 per cent from 11.5 per cent.

Moody’s said given the magnitude of stressed assets in the system, it expects the banks to increase their focus on resolving some of the large problem accounts.

“We expect an increased pace of debt restructuring under various schemes offered by RBI, including the scheme for sustainable structuring of stressed assets (S4A), strategic debt restructuring (SDR) and the 5:25 scheme,” the report said.

“Nevertheless, weak reserving levels and continued pressure on profitability will limit the ability of the banks to proactively resolve problem assets under these schemes,” Anbarasu said.

Icra said a muted level of credit off-take — on the back of weak demand, increasing competition and greater disintermediation — will continue to exert downward pressure on lending rates.

It said the overall capitalisation levels of most of the public sector banks remain moderate to weak, given that they need to attain the regulatory minimum tier-I requirement of 9.5 per cent by March 2019.

The current plan of infusing Rs 45,000 crore during 2016-17 and 2018-19, of which Rs 16,414 crore have already been infused in the current year, is below ICRA’s estimate of capital requirements of Rs 1,50,000-1,80,000 crore.