Clarification to be handy for India Inc as the government had recently allowed corporate India to vaccinate their employees at the companies’ premises.

In a significant boost to corporate India looking to undertake CSR around the COVID-19 pandemic, the corporate affairs ministry (MCA) has clarified spending of CSR funds for setting up “makeshift hospitals and temporary Covid care facilities” would be treated as an eligible CSR activity.

This would be permitted as an eligible Corporate Social Responsibility (CSR) activity under schedule VII of the companies Act regarding promotion of healthcare, including preventive healthcare and, disaster management respectively, the MCA said in a circular.

The MCA has said that companies may undertake the activities of setting up makeshift hospitals and temporary Covid care facilities in consultations with the State governments. This will be allowed so long as companies comply with the Companies ( CSR Policy) rules 2014 and the circulars related to CSR issued by the ministry from time to time, it added.

Handy for India Inc

This clarification from MCA may come in handy for India Inc as the government had recently allowed corporate India to vaccinate their employees at the companies’ premises without them having to go to vaccination Centres.

Recently there has been a lot of debate on whether India Inc can treat the inoculation expenses that they want to spend on behalf of their employees as an eligible CSR spend or not.

While the current thinking is that the Centre may not agree to such expenses undertaken solely for employees as being counted as CSR activity, however the latest move to allow corporates to set up makeshift hospitals and temporary Covid care facilities as an eligible CSR activity would certainly encourage India Inc to take up such activities.

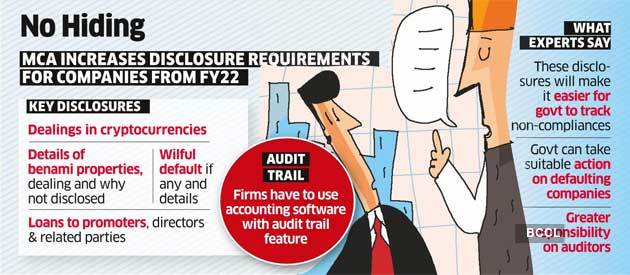

Starting April 1, companies must state if they have been declared wilful defaulters by banks, financial institutions or other lenders. The ministry also mandated companies to record audit trails of their accounts. Firms using accounting software to maintain their books need to use features that can record the audit trail of each transaction and create an edit log, including the date of such changes.

India Inc will have to declare investments in cryptocurrencies, relationships with dissolved companies and loans extended to related parties, among a host of other disclosures mandated by the government to improve transparency.

Starting April 1, companies must state if they have been declared wilful defaulters by banks, financial institutions or other lenders.

The ministry of corporate affairs announced a new set of disclosures rules under the Companies Act on Wednesday, significantly enhancing financial and general reporting requirements for companies.

The ministry also mandated companies to record audit trails of their accounts. Firms using accounting software to maintain their books need to use features that can record the audit trail of each transaction and create an edit log, including the date of such changes.

Amending the Companies (Accounts) Rules, the ministry said firms must ensure the audit trail feature on the accounting software cannot be disabled. The move is aimed at curbing backdated entries and will affect mainly smaller companies as the bigger ones already use such software, according to Shalu Kedia, a partner at Nangia & Co.

Additional disclosures to be made under schedule III of the Companies Act, 2013, relate to matters such as corporate social responsibility spending, cryptocurrency dealings, benami property, relationship with struck-off, or dissolved, companies, and ageing of payables & receivables with vendors.

These disclosures will make it easier for the government to track non-compliance and take action against defaulting companies, experts said.

“Earlier, the companies were only required to disclose trade payables and receivables, but there was no requirement to provide ageing details. This disclosure will mandate the company to disclose the ageing payment cycle for MSMEs and non-MSME vendors,” said Nischal Arora, a partner at Nangia Andersen LLP.

Dealings in cryptocurrencies must be disclosed with details of the profit or loss on such transactions, amounts of such currency held and deposits or advances from any person for trading or investing in these currencies.

“While the government is already working on a bill on cryptocurrency, the disclosure for such currency has made it clear that the government wants to gather data on cryptocurrency,” said Arora.

Another important change was related to the disclosure of any benami property holdings.

“This disclosure is another step to improve transparency for the stakeholders as they will have to disclose any proceeding that has been initiated or pending against the company for holding any benami property and also provide a reasoning and view on the same,” said Amit Maheshwari, a partner at AKM Global.

The additional disclosures will make it mandatory for companies to provide details of shortfall in CSR spending for the previous years, including reasons for not meeting targets.

Loans granted to promoters, directors and related parties that are repayable on demand or without specific repayment terms from companies must be declared in terms of amount and percentage to total loans granted.

While this will push firms to regularly service their loans, it “will be helpful for the investor and other lenders to be aware about these types of companies before making any investment or lending the money,” Maheshwari said.

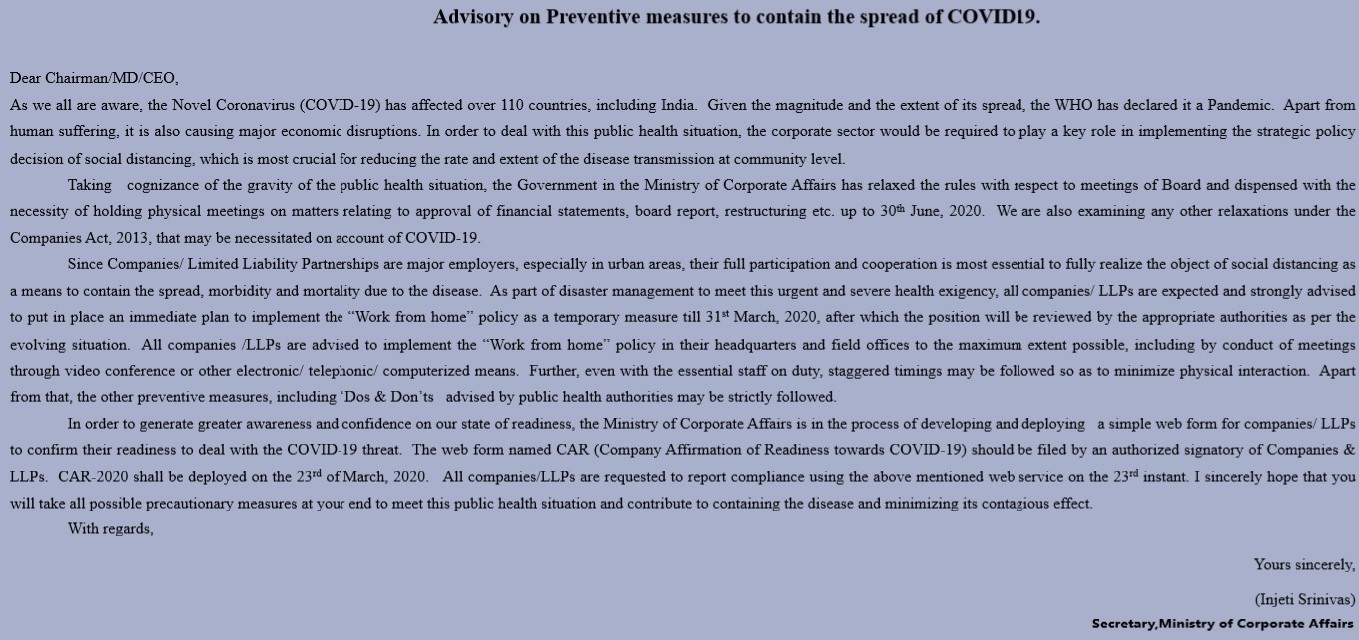

Advisory on Preventive measures to contain the spread of COVID19

Advisory on Preventive measures to contain the spread of COVID19

The Ministry of Corporate Affairs ( MCA ) is in the process of developing and deploying a simple web form named CAR (Company Affirmation of Readiness towards COVID-19) for companies/LLPs to confirm their readiness to deal with the COVID-19 threat.

Since the wake of the Novel Coronavirus(COVID-19) affecting over 110 countries including India, the WHO had declared it a Pandemic. Apart from human suffering, it is also causing major economic disruptions. In order to contain the spreading of the virus, the corporate sector is required to play a key role in implementing the strategic policy decision of social distancing, which is most crucial in reducing the rate and extent of disease transmission at the community level.

Taking cognizance of the gravity of the public health situation, the Government in the Ministry of Corporate Affairs has relaxed the rules with respect of Board and dispensed with the necessity of holding physical meetings on matters relating to approval of financial statements, board report, restructuring etc., up to 30th June, 2020. They are also examining any other relaxation under the Companies Act, 2013 that may be necessitated on account of COVID-19.

As part of disaster management to meet this urgent and severe health exigency, all companies/LLPs are strongly advised to put in place an immediate plan to implement the “Work from Home” in the Headquarters and field offices to the maximum extent possible, including by conduct of meeting through video conference or other electronic/telephonic/computerized means. They further instructed that even with the essential staff on duty, staggered timings may be followed so as to minimize physical interaction. Apart from that, the preventive measures including the Do’s and Don’t’s advised by the public health authorities are to be strictly followed.

The Webform named CAR will be deployed on 23rd March 2020. All companies/LLPs are requested to using compliance with the web form named CAR on the 23rd of March instant while following all possible preventive measures to contain the disease and its contagious effect.

Frequently Asked Questions on (CAR) – 2020

1. To whom is this form applicable?

To All Companies / LLP including small companies, private companies, One Person Company (OPC) .All Companies/LLP include the companies, whether incorporated in India or not, but having operations in India.

2. When will the form be deployed?

The form is expected to be deployed on 23rd March, 2020 and is required to be submitted by 30th March, 2020 (extended by a week).

3. Is there any fees for filing the form?

No.

4. Who can file the form on behalf of Companies / LLP?

CS, CFO, Managing Director, Director, Designated Partners or Authorized person who has been authorised for such purposes.

5. Whose Mobile number has to be entered in the form?

In case of Director / Designated Partner signing the form their mobile number will be automatically prefilled from database. In all other case, the Mobile Number shall be editable should be that of the person who is authenticating the form as it has to be verified by a One Time Password (OTP).

6. What if my organization does not have a whole time / permanent employee?

The form still has to be filed, but the Company / LLP will be eased of future compliance burden, if any.

7. Till when does such policy needs to be in place?

The policy needs to be in place till 31st March, 2020 as per present scenario but may be extended based on the review made by appropriate Govt. Authorities.

8. What if I do not adhere to filing of such web form?

There has not been any information on the same but going by the intent of the form, non – filing of it may not lead to any penal outcome.

9. On what basis can I prepare “Work from Home” policy?

This shall be prepared based on the guidelines and advisory issued by the Government from time to time to check the spread of COVID – 19.

10. How to track the filing of form?

Once the form is filed, a system based acknowledgement will be sent to:

The government had issued new norms for auditors, seeking more disclosures in reports, a move which comes after a series of corporate scams and frauds surfaced over the past few years.

CARO 2020 – Companies (Auditor’s Report) Order, 2020

MCA in place of existing the Companies (Auditor’s Report) Order, 2016, has notified CARO 2020 after consultation with the National Financial Reporting Authority constituted under section 132 of the Companies Act, 2013.

Auditor’s report to contain matters specified in paragraphs 3 and 4. – Every report made by the auditor under section 143 of the Companies Act on the accounts of every company audited by him, to which this Order applies, for the financial years commencing on or after the 1st April, 2019, shall in addition, contain the matters specified in paragraphs 3 and 4, of the CARO 2020.

Provided this Order shall not apply to the auditor’s report on consolidated financial statements except clause (xxi) of paragraph 3.

It shall come into force on the date of its publication in the Official Gazette.

CARO 2020 – Key changes/highlights

Matters to be included in auditor’s report, in CARO 2020 – the reporting clauses are more extensive and detailed than were in CARO2016

Unlike CARO 2016, which required reporting on all fixed assets, new reporting requirements pays attention to Property, Plant, Equipment and intangible assets.

Reporting on revaluation of Property, Plant and Equipments by company

Reporting of proceedings under the Benami Transactions (Prohibition) Act, 1988.

Reporting of compliances if company was sanctioned working capital limits in excess of Rs.5 crores or more from banks or financial institutions.

– whether the quarterly returns or statements filed by the company with such banks or financial institutions are in agreement with the books of account of the Company, if not, to give details;

Reporting of investments in or in providing of any guarantee or security or granting any loans or advances to companies, firms, Limited Liability Partnerships or any other parties.

Reporting of compliances with RBI directives and the provisions the Companies Act with respect to deemed deposits.

Reporting with respect to transactions not recorded in the books of account surrendered or disclosed as income in the income tax proceedings.

Comprehensive reporting requirement for default in the repayment of loans / other borrowings or in the payment of interest

– whether the company is a declared wilful defaulter by any bank or financial institution or other lender;

– whether term loans were applied for the purpose for which the loans were obtained; if not, the amount of loan so diverted and the purpose for which it is used may be reported;

– whether funds raised on short term basis have been utilised for long term purposes, if yes, the nature and amount to be indicated

Reporting on treatment by auditor of whistle-blower complaints received during the year by the company

Reporting on internal audit system

– whether the company has an internal audit system commensurate with the size and nature of its business;

– whether the reports of the Internal Auditors for the period under audit were considered by the statutory auditor;

Reporting on cash losses

Reporting on resignation of the statutory auditors

Reporting on uncertainty of company capable of meeting its liabilities

Reporting transfer of unspent CSR amount to Fund specified in Schedule VII

Reporting on qualifications or adverse remarks by the auditors in the CARO reports of companies included in the consolidated financial statements

It is expected that CARO, 2020 will improve the overall quality of reporting by the auditors and thereby lead to “greater transparency and faith in the financial affairs of the companies.”

New EPF Act may oblige small firms with 10 or more staff to deduct PF from workers’ salary

Government plans to amend the Employees Provident Fund Act to bring more workers under the ambit of retirement fund body EPFO by reducing the threshold for coverage of firms to 10 workers, Lok Sabha was informed today.

Labour and Employment Minister Bandaru Dattatreya said the plan is to amend the law so that firms with ten employees can also be brought under the ambit of EPFO to ensure more workers come under the umbrella of social security.

At present, it is mandatory under the Employees’ Provident Fund and Miscellaneous Provisions Act for firms having 20 or more workers to subscribe to social security schemes run by the Employees’ Provident Fund Organisation.

In his written reply, he said no proposal is under the consideration of the government to allow EPFO subscribers to contribute voluntarily towards pension scheme in addition to their employers’ mandatory contribution.

He said effort is on to bring more unorganised workers under the ambit of various social security schemes for which more projects are being unveiled. “There is more focus on these workers,” he said.

Responding to the ‘plight’ of beedi workers following the introduction of 85 per cent pictorial norm on tobacco products, Dattatreya said the Labour Ministry is working to impart vocational skills to beedi workers.

He said several representations were received regarding “adverse consequences” of the Health Ministry’s notification prescribing 85 per cent pictorial warning on tobacco products.

He said at a meeting chaired by him in April, concerns were raised by stakeholders. The report of the meeting was conveyed to the Health Ministry.

He said beedi workers are covered under group insurance scheme and provided assistance of Rs 10,000 in case of natural death and Rs 25,000 in case of accidental death. Rs 1500 is also provided for the funeral of deceased workers.

Financial assistance of Rs 5000 is given to widows or widowers of beedi workers under social security schemes for wedding of their first two daughters.

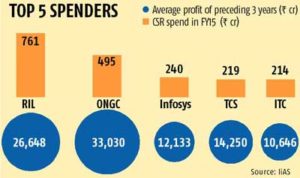

The move to make corporate social responsibility (CSR) spending mandatory has resulted in a spurt in social spending by India Inc. Spending on CSR activities by the top 100 companies increased to Rs 5,240 crore in 2014-15. The figure had stood at Rs 3,000 crore in 2012-13, when CSR spending was voluntary. Corporate governance firm Institutional Investor Advisory Services (IiAS) projects spending will increase to Rs 8,500 crore in the current financial year.

The Companies Act, 2013, requires companies above a certain financial threshold to spend at least two per cent of their average net profit of the preceding three years on CSR. Although CSR spending is compulsory, the Act has taken a ‘comply or explain’ approach, where a company has to provide reasons if the spending is less than the stipulated amount.

According to IiAS, CSR spends in FY15 were 26 per cent lower than the prescribed amount.

“Even as CSR is entering corporate consciousness, the next two to three years will remain a ‘learning period’ for industry,” the governance firm said in a note on Tuesday.

India Inc takes to social causes

IiAS has tracked the spending of BSE 100 companies, where 95 companies qualify under the profitability criteria for mandatory spending. The remaining five companies were not required to spend as they made average losses in the preceding three years.

State-owned firms set aside lesser amount compared to private sector firms. In FY13, public sector units (PSUs) spent 0.6 per cent of their average profits in the preceding three years. In comparison, non-PSUs spent one per cent of their average profit before tax of the preceding three years.

The trend continued in FY15. The CSR spends of the S&P BSE 100 companies aggregated 1.5 per cent of their three-year average profits. Non-PSUs spent 1.6 per cent and the 21 PSUs spent 1.3 per cent of their average profit in the preceding three years, IiAS noted.

Close to Rs 61 crore of the CSR spends by India Inc in FY15 was towards the Prime Minister’s National Relief Fund and seven companies contributed Rs 47 crore towards Swachh Bharat Kosh.