Taxpayers who have not filed GST returns for two months or quarters up to June 2021 will not be able to generate e-way bills from August 15.

The Goods and Service Tax network on 4th August 2021 has decided to resume the blocking of e-way bill generation facility on the EWB portal, for all the taxpayers in terms of Rule 138 E (a) and (b) of the CGST Rules, 2017, from 15th August onwards.

1. As you might be aware that the facility of blocking E way bill generation had been temporarily suspended due to pandemic, in terms of Rule 138 E (a) and (b) of the CGST Rules, 2017, the E Way Bill generation facility of a person is liable to be restricted, in case the person fails to file their return in Form GSTR-3B / statement in CMP-08, for a consecutive period of two months / Quarters or more.

2. The government has now decided to resume the blocking of EWB generation facility on the EWB portal, for all the taxpayers in terms of Rule 138 E (a) and (b) of the CGST Rules, 2017, from 15th August onwards.

3. Thus, after 15th August 2021, the System will check the status of returns filed in Form GSTR-3B or the statements filed in Form GST CMP-08, and restrict the generation of EWB in case of: Non filing of two or more returns in Form GSTR-3B for the months up to June, 2021 and Non filing of 02 or more statements in Form GST CMP-08 for the quarters up to April to June, 2021

4. To avail continuous EWB generation facility on EWB Portal, you are therefore advised to file your pending GSTR 3B returns/ CMP-08 Statement immediately.

5. For details of blocking and unblocking EWB click on below links :

The tax filing due dates were extended by the CBDT in view of the difficulties being faced by taxpayers and other stakeholders in the electronic filing of these forms.

The Central Board of Direct Taxes (CBDT) has extended the due dates for electronic filing of various Forms under the Income-tax Act, 1961. Considering the difficulties reported by the taxpayers and other stakeholders in the electronic filing of certain Forms, CBDT has taken this step.

The Central Board of Direct Taxes (CBDT) has issued an order extending due dates for various compliance forms including the Quarterly statement in Form No. 15CC, Equalization Levy Statement in Form No.1, the Statement of Income paid or credited by an investment fund to its unit holder in Form No. 64D and the Statement of Income paid or credited by an investment fund to its unit holder in Form No. 64C.

(i) The Quarterly statement in Form No. 15CC to be furnished by an authorized dealer in respect of remittances made for the quarter ending on 30th June 2021 required to be furnished on or before 15th July 2021 under Rule 37BB of the Rules. as extended to 31° July 2021 vide Circular No 12 of 2021 dated 25.06.2021, may be filed on or before 31st August 2021.

(ii) The Equalization Levy Statement in Form No.1 for the Financial Year 2020- 21, which was required to be filed on or before 30. June 2021. as extended to 31s1July, 2021 vide Circular No 12 of 2021 dated 25 06.2021. maybe filed on or before 310 August 2021;

(iii) The Statement of Income paid or credited by an investment fund to its unit holder in Form No. 64D for the Previous Year 2020-21, required to be furnished on or before 15. June 2021 under Rule 12CB of the Rules, as extended to 151″ July 2021 vide Circular No.12 of 2021 dated 25.06 2021, maybe furnished on or before 15. September,2021;

(iv) The Statement of Income paid or credited by an investment fund to its unit holder in Form No. 64C for the Previous Year 2020-21, required to be furnished on or before 30. June 2021 under Rule 12CB of the Rules, as extended to 3f” July 2021 vide Circular No.12 of 2021 dated 25.06.2021, maybe furnished on or before 30. September 2021.

Further, considering the non-availability of the utility for e-filing of certain Forms, the Board has extended the due dates for electronic filing of such Forms as (i) Intimation to be made by a Pension Fund in respect of each investment made by it in India in Form No. 10BBB for the quarter ending on 300 June 2021, required to be furnished on or before 311July,2021 under Rule 2DB of the Rules, may be furnished on or before 30° September 2021, and (ii) Intimation to be made by Sovereign Wealth Fund in respect of investments made by it in India in Form II SWF for the quarter ending on 30° June 2021, required to be furnished on or before 31st July 2021 as per Circular No 15 of 2020 dated 22.07.2020 may be furnished on or before 30° September 2021.

The Board has clarified that “the above said forms, e-filed, after the expiry of time limits provided as per Circular No. 2 of 2021 dated 25.06.2021 or as per the relevant provisions, till date will stand regularized accordingly.”

From pre-filled income tax return forms to quick refunds — the new portal has a tons of features to make tax filing journey easy and convenient.

The tax department has launched the much-awaited new portal of filing income tax return (ITR) — www.incometax.gov.in — on Monday night.

The new e-filing portal (www.incometax.gov.in) is aimed at providing taxpayer convenience and a modern, seamless experience to taxpayers;

New taxpayer friendly portal integrated with immediate processing of Income Tax Returns(ITRs) to issue quick refunds to taxpayers;

All interactions and uploads or pending actions will be displayed on a single dashboard for follow-up action by taxpayer;

Free of cost ITR preparation software available online and offline with interactive questions to help taxpayers fill ITR even without any tax knowledge, with pre-filling, for minimizing data entry effort;

New call center for taxpayer assistance for immediate answers to taxpayer queries with FAQs, Tutorials, Videos and chatbot/live agent;

All key portal functions on desktop will be available on Mobile App which will be enabled subsequently for full anytime access on mobile network;

New online tax payment system on new portal will be enabled subsequently with multiple new payment options using net-banking, UPI, Credit Card and RTGS/NEFT from any account of taxpayer in any bank, for easy payment of taxes.

From pre-filled income tax return forms to quick refunds — the new portal has a tons of features to make your tax filing journey easy and convenient. The aim is to provide a “modern and seamless experience to taxpayers”.

The initiative of the Income Tax department to make the tax portal tax payer friendly and more easy to navigate is applaudable. The videos, FAQ and various tutorials and the ITR preparation software to ease the discomfort of new tax payers who may not be computer savvy is a good start. While its early to comment on the ease of use for which one needs to access the portal, the portal does indicate issuance of quicker tax return processing and faster refunds, which is a welcome step.

The latest features of the new income tax filing portal www.incometax.gov.in are listed below:

1) The new portal will process the the income tax returns immediately, said the Central Board of Direct Taxes. This will help the taxpayers to get the quick refunds of their income tax returns.

2) There will be a single dashboard for all the interactions and pending return. The taxpayers can easily see all their interactions together in a place. This will make following up of pending notices easier and convenient.

3) The taxpayers will get a free interactive software which will guide them to file ITR forms. Now, ITRs 1, 4 (online and offline) and ITR 2 (offline) will be available. “Facility for preparation of ITRs 3, 5, 6, 7 will be made available shortly,” CBDT said.

4) The option of pre-filled ITR forms will be available on the new website. “Taxpayers will be able to proactively update their profile to provide certain details of income including salary, house property, business or profession which will be used in pre-filling their ITR,” the Ministry of Finance said.

5) To answer all your queries while filing ITR forms, there will be call centre for prompt assistance. A chatbot will also be available to help the taxpayer filing their returns along with detailed manual, videos and FAQs.

6) The other functionalities for filing income tax forms, adding tax professionals, submitting responses to notices in faceless scrutiny or appeals will be available on the new e-filing portal.

7) It must be noted that the new tax payment system will be launched on June 18 after the advance tax instalment date, the ministry of finance said.

8) Given the new portal launching and advance tax payment due date falling on June 15, to avoid any inconvenience in the tax payment process to the taxpayer, this will be launched on June 18 2021. However, for all other features/functionalities, the website can be used as soon as launched. Users can still make payment through existing process and file their tax returns on the new portal.

9) “The mobile app will also be released subsequent to the initial launch of the portal, to enable taxpayers to get familiar with the various features,” it further added.

10) Taxpayers and other stakeholders will take some time to familiarize with the various features of new portal. The tax department urged all to remain patient for the initial period after the launch as it will be a major transition in the tax filing system.

The Ministry of Corporate Affairs (MCA), considering requests to waive additional fee for late filing of statutory forms which fall due between 1 April and end of May owing to the COVID-19 restrictions and disruption, has granted extra time without additional fee for filing statutory forms till the end of July, 2021

The ministry of corporate affairs (MCA) has offered relaxation in certain compliance requirements for businesses, including a longer interval between two board meetings in view of the hardships during the second wave of the pandemic.

Companies are normally required to hold a minimum of four board meetings in a year with the interval between them not exceeding 120 days. This has now been relaxed by 60 days so that the interval could go up to 180 days, the ministry said in a notification issued on Monday.

The ministry also said in a separate notification that it has received several requests to waive the additional fee for late filing of statutory forms which fall due between 1 April and end of May in view of the covid-19 restrictions and disruption.

The ministry said these requests have been examined and taking into account the difficulties due to resurgence of coronavirus infections, extra time without additional fee has been granted till the end of July for filing statutory forms. In the case of filing forms to report creation or modification of a charge (lien or claim) on the assets of a company under various circumstances, the ministry has issued another notification granting relief. Accordingly, in cases where due date had expired before 1 April, extra time has been granted till end of May.

The finance ministry has already given relief for various compliance requirements related to income tax and goods and services tax (GST), besides exempting basic customs duty and agriculture cess on various medical supplies used in the prevention and treatment of coronavirus disease. The pandemic has taken a heavy toll on lives with over 222,000 deaths.

The central government has not favoured a lockdown of the country during the second wave, but several states had to impose curbs on movement and assembly of people to break the chain of infections. India has so far vaccinated over 15 crore people, or roughly 12% of the population. The second wave is expected to slow India’s economic recovery from an expected 7.7% contraction in FY21.

COVID -19 relief for taxpayers. Last chance to revise ITR for financial year 2019-20

In view of the adverse circumstances arising due to the severe Covid-19 pandemic and also in view of the several requests received from taxpayers, tax consultants & other stakeholders from across the country, requesting that various compliance dates may be relaxed, the Government has extended certain timelines on Saturday.

In the light of multiple representations received (supra) and to mitigate the difficulties being faced by various stakeholders, the Central Board of Direct Taxes (CBDT) has, under section 119 of the Income-tax Act, 1961(the Act), provided the following relaxation in respect of compliances by the taxpayers:

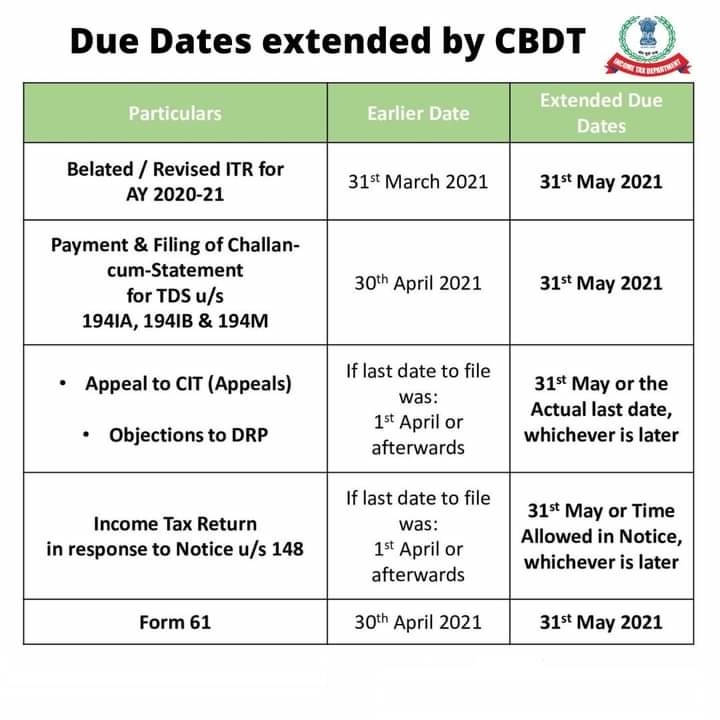

a) Appeal to Commissioner (Appeals) under Chapter XX of the Act, for which the last date of filing under that Section is 1st April, 2021 or thereafter, may be filed within the time provided under that Section or by 31st May, 2021, whichever is later;

b) Objections to Dispute Resolution Panel (DRP) under Section 144C of the Act, for which the last date of filing under that Section is 1st April, 2021 or thereafter, may be filed within the time provided under that Section or by 31st May, 2021, whichever is later;

c) Income-tax return in response to notice under Section 148 of the Act, for which the last date of filing of return of income under the said notice is 1st April, 2021 or thereafter, may be filed within the time allowed under that notice or by 31st May, 2021, whichever is later;

d) Filing of belated return under sub-section (4) and revised return under sub-section (5) of Section 139 of the Act, for Assessment Year 2020-21, which was required to be filed on or before 31st March, 2021, may be filed on or before 31st May, 2021;

e) Payment of tax deducted under Section 194-IA, Section 194-IB and Section 194M of the Act, and filing of challan-cum-statement for such tax deducted, which are required to be paid and furnished by 30th April, 2021(respectively) under Rule 30 of the Income-tax Rules, 1962, may be paid and furnished on or before 31st May, 2021;

f) Statement in Form No. 61, containing particulars of declarations received in Form No.60, which is due to be furnished on or before 30th April, 2021, may be furnished on or before 31st May, 2021.

The above relaxations are the latest among the recent initiatives taken by the Government to ease compliances to be made by the taxpayers with the aim to grant respite during these difficult times.

The GST revenues during April 2021 are the highest since the introduction of GST even surpassing collections in the last month

The gross GST revenue collected in the month of April is at a record high of Rs. 1,41,384 crore of which CGST is Rs. 27,837 crore, SGST is Rs. 35,621, IGST is ₹68,481 crore (including Rs. 29,599 crore collected on import of goods) and Cess is Rs. 9,445 crore (including Rs. 981 crore collected on import of goods).

“Despite the second wave of COVID-19 pandemic affecting several parts of the country, Indian businesses have once again shown remarkable resilience by not only complying with the return filing requirements but also paying their GST dues in a timely manner during the month,” according to a statement by Ministry of Finance.

The GST revenues during April 2021 are the highest since the introduction of GST even surpassing collections in the last month (March’2021). In line with the trend of recovery in the GST revenues over past six months, the revenues for the month of April 2021 are 14% higher than the GST revenues in the last month of March’2021.

During the month, the revenues from domestic transaction (including import of services) are 21% higher than the revenues from these sources during the last month.

GST revenues have not only crossed the Rs. 1 lakh crore mark during successively for the last seven months but have also shown a steady increase. These are clear indicators of sustained economic recovery during this period.

Closer monitoring against fake-billing, deep data analytics using data from multiple sources including GST, Income-tax and Customs IT systems and effective tax administration have also contributed to the steady increase in tax revenue. Quarterly return and monthly payment scheme has been successfully implemented bringing relief to the small taxpayers as they now file only one return every three months.

Providing IT support to taxpayers in the form of pre-filled GSTR 2A and 3B returns and ramped up System capacity have also eased the return filing process.

During this month the government has settled Rs. 29,185 crore to CGST and Rs. 22,756 crore to SGST from IGST as regular settlement.

The total revenue of Centre and the States after regular and ad-hoc settlements in the month of April’ 2021 is Rs. 57,022 crore for CGST and Rs. 58,377 crore for the SGST.

Only the bare minimum changes necessitated due to amendments in the Income-tax Act, 1961 have been incorporated in the forms, CBDT said in the notification for the new ITR forms, in view of the ongoing crisis due to COVID-19 pandemic.

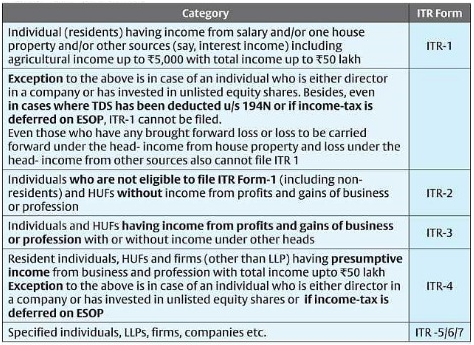

Keeping minimum change and with the view to minimise compliance burden, The Central Board of Direct Taxation (CBDT) has notified new income tax return forms — ITR-1 to ITR-7, for the Assessment Year 2021-22, the ministry of finance said in a statement on April 1.

In this new ITR form for AY 2021-22, the taxpayers will now have dedicated space in each of the ITR forms — Sahaj (ITR-1), Form ITR-2, Form ITR-3, Form ITR-4 (Sugam), Form ITR-5, Form ITR-6, Form ITR-7 and Form ITR-V to describe their investments, CBDT said.

ITR Form 1 (Sahaj) and ITR Form 4 (Sugam) are simpler Forms that cater to a large number of small and medium taxpayers. Sahaj can be filed by an individual having income up to Rs 50 lakh and who receives income from salary, one house property / other sources (interest etc).

Similarly, Sugam can be filed by individuals, Hindu Undivided Families (HUFs) and firms (other than Limited Liability Partnerships (LLPs) having total income up to Rs 50 lakh and income from business and profession computed under the presumptive taxation provisions.

Individuals and HUFs not having income from business or profession (and not eligible for filing Sahaj) can file ITR-2, while those having income from business or profession can file ITR Form 3.

Persons other than individual, HUF and companies i.e. partnership firm, LLP etc can file ITR Form 5. Companies can file ITR Form 6. Trusts, political parties, charitable institutions etc claiming exempt income under the Act can file ITR-7.

There is no change in the manner of filing of ITR forms as compared to last year, the CBDT said.

Key points :

♦ ITR-1 cannot be filed in case tax has been deducted u/s 194N

As per, Section 194N – TDS 194N is required to be deducted if amount of cash withdrawn exceeds –

Exceeds Rs 20 lakhs in case of non-filers of return

Rs 1 crore in all other cases

from banking company or co-operative bank or post-office from one or more accounts maintained by taxpayer.

If tax has been deducted u/s 194N, a person can file –

ITR 2

ITR 3

ITR 4

♦ TDS deducted u/s 194N cannot be carried forward to subsequent years.

It means Credit for tax deducted u/s 194N can be taken in previous year relevant to Assessment year in which tax has been deducted.

♦ Option has been given to Individual or HUF as per Section 115BAC.

From A.Y 2021-22 option is available to Individual & HUF whether to opt New Scheme or not. This option for lower tax regime, by foregoing certain exemptions and deductions, is given to Assessees to select new scheme-Section 115BAC and are required to file Form-10IE before filing the return u/s 139(1).

♦ Change in Schedule 112A-LTCG from sale of equity share or unit of equity oriented fund on which STT is paid.

Sale price per share/unit now added in Schedule 112A, which was not earlier provided.

♦ Dividend also taxable from A.Y 2021-22- As we know Dividend Income taxable from A.Y 2021-22 in hands of Assessee from A.Y 2021-22 so we are required to give quarterly break-up of Dividend received in order to get relief from interest levied u/s 234C.

♦ Changes in Section 44AB- The threshold limit to get books of account audited increased from Rs 1 crore to 10 crores, if the following conditions are satisfied-

His aggregate of all receipts in cash during the previous year does not exceeds 5 % of such receipts.

His aggregate of all payments in cash during the previous year does not exceeds 5 % of such payments